June 30, 2026

The Hidden Architecture of Cobalt Supply Control

When a single nation commands more than 70% of global reserves of a battery-critical mineral, the question is never if it will exercise pricing power, but how and when. For decades, the Democratic Republic of Congo's cobalt dominance was largely academic, its influence diluted by oversupplied markets, fragmented regulation, and limited institutional capacity to enforce meaningful production discipline. That era is over.

What has emerged in its place is something far more sophisticated than a blunt export ban. The DRC has engineered a quota-based supply management architecture that bears closer resemblance to OPEC's production ceiling mechanisms than to the reactive resource nationalism seen elsewhere in Africa. Understanding the mechanics, consequences, and investment implications of Congo cobalt export quotas requires moving well beyond headline price figures.

When big ASX news breaks, our subscribers know first

Why the Quota Model Is More Powerful Than an Export Ban

Resource nationalism typically manifests in one of two forms: outright export prohibition or fiscal renegotiation. Both are blunt instruments. Export bans trigger immediate diplomatic and legal retaliation, while royalty renegotiations take years to resolve through arbitration. The DRC's quota framework avoids both vulnerabilities.

By capping rather than eliminating exports, the DRC retains plausible deniability as a reliable trading partner while simultaneously controlling the volume of cobalt reaching international markets. This distinction matters enormously for market psychology. A ban signals instability; a quota signals strategic intent. Global commodity traders and battery manufacturers respond differently to each, with the latter prompting longer-term repricing of supply risk rather than short-term panic buying.

The regulatory body executing this strategy is ARECOMS, the DRC's strategic minerals regulator. Its mandate extends beyond administration into active market management. ARECOMS holds discretionary authority over quota allocation, enforcement, and redistribution, meaning no single producer can rely on historical allocations as a guarantee of future access. This perpetual uncertainty is itself a supply tightening mechanism, because it discourages producers from making long-term export commitments to downstream buyers.

Breaking Down the 2026-2027 Export Cap Structure

The numerical architecture of Congo cobalt export quotas reveals just how consequential this policy has become. Furthermore, as the DRC cobalt export ban extension demonstrated, the transition toward structured quotas was a deliberate and calculated evolution in policy.

| Quota Component | Volume / Detail |

|---|---|

| 2024 Actual Production | ~204,000 tonnes |

| 2026-2027 Annual Export Cap | 96,600 tonnes (48.2% of 2024 output) |

| Producer Basic Quota Allocation | 87,000 tonnes distributed to operators |

| ARECOMS Strategic Reserve | 9,600 tonnes held by the state |

| 2025 Remaining Quota (Q4 2025 / Q1 2026 extension) | 18,125 tonnes |

| Strategic Reserve as % of National Exports | ~10% |

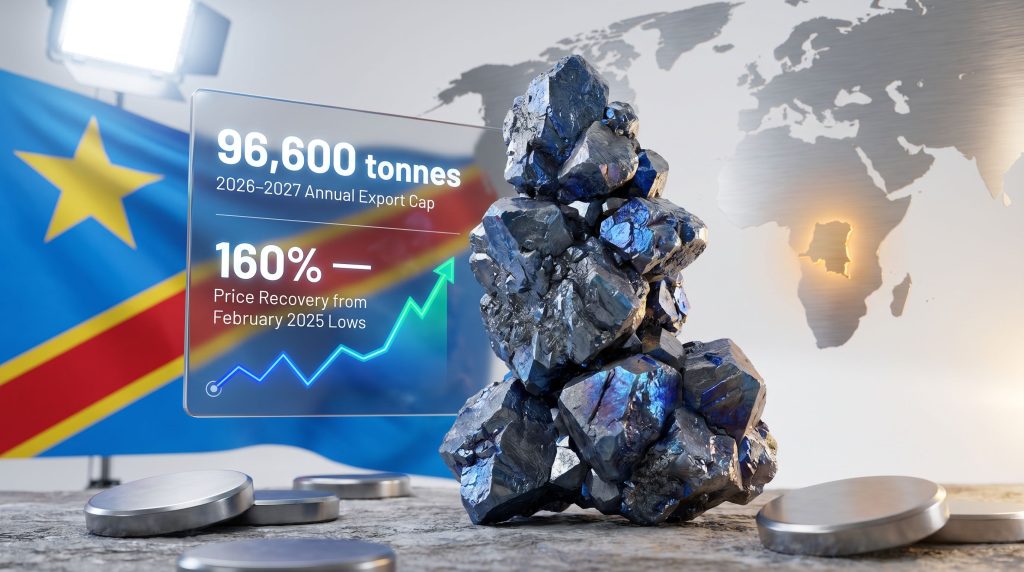

The hard annual ceiling of 96,600 tonnes for both 2026 and 2027 represents less than half of the country's 2024 production output of approximately 204,000 tonnes. This is not a minor administrative adjustment; it is a structural supply constraint of a scale rarely seen in any commodity market outside of OPEC-coordinated oil production cuts.

Of the total cap, 87,000 tonnes flow as basic allocations to registered producers. The remaining 9,600 tonnes, approximately 10% of the national export ceiling, are retained by ARECOMS as a strategic reserve. This reserve functions as a state-controlled buffer stock that ARECOMS can deploy toward projects classified as serving national economic interests, including local cobalt processing and downstream value-addition initiatives.

The Deadline Mechanism: How Forfeiture Amplifies Supply Tightness

Perhaps the most underappreciated element of the quota system is its use of hard forfeiture deadlines as an active supply management tool. Under the current framework, any quota volumes allocated for the first half of 2026 that remain unutilised by June 30 are automatically forfeited and reassigned to ARECOMS's strategic reserve rather than returned to commercial producers.

A secondary customs declaration deadline of July 5 functions as the final gateway for H1 shipments, meaning operators who miss this window lose both their shipment and their quota allocation. Forfeited volumes are also deducted from companies' original allocations with no carry-forward provisions, effectively penalising operators twice: once through lost export revenue, and again through a reduced baseline for future allocation calculations.

This creates a compounding tightness effect. Even when the headline quota figure of 96,600 tonnes appears relatively generous compared to demand, actual export volumes are running at an estimated 33% to 50% of allocated quotas due to administrative bottlenecks, customs processing delays, and logistics challenges. The practical implication is striking: the effective commercial cobalt supply reaching the market may be closer to 30,000-45,000 tonnes annually, far below even the already-constrained headline cap.

The gap between allocated quotas and actual shipments means the cobalt market is structurally tighter than the headline numbers suggest. Administrative friction is doing as much work as regulatory intent in constraining global supply.

How Cobalt Prices Have Responded

The market's reaction to progressive DRC supply tightening has been dramatic. Cobalt prices collapsed through 2023 and into early 2024 under the weight of significant oversupply, with Chinese battery manufacturers and trading houses flooding the market with material accumulated during the post-pandemic demand surge. By February 2025, prices had reached multi-year lows that rendered many non-DRC cobalt projects economically marginal.

The inflection point came when the DRC introduced an initial four-month export suspension in early 2025. This blunt intervention catalysed the first wave of price recovery, demonstrating to the market that Congo was prepared to accept short-term revenue sacrifice in exchange for longer-term price stabilisation. Consequently, the Congo cobalt price impacts that followed confirmed the transition from a blanket ban to a structured quota system reinforced this signal, communicating that supply discipline would be maintained through institutional mechanisms rather than reactive emergency measures.

By mid-2026, cobalt prices had surged approximately 160% from their February 2025 lows, reaching $26 per pound ($57,320 per metric tonne). A related metric, the approximately 92% rebound since March 2025, reflects not speculative froth but structural repricing of a market that had chronically undervalued single-source supply concentration risk.

Timeline of the Cobalt Price Recovery

- 2023-2024: Chronic oversupply drives prices to multi-year lows, with Chinese producers and traders offloading accumulated inventory.

- February 2025: Cobalt prices reach cyclical floor, rendering non-DRC projects economically unviable.

- Early 2025: DRC introduces a four-month export suspension, triggering the first significant price rebound.

- Mid-2025: Transition from export ban to structured quota framework signals institutionalised supply management.

- 2026: Annual export cap of 96,600 tonnes confirmed for 2026-2027; actual exports running at 33-50% of cap due to logistical constraints.

- Mid-2026: Cobalt prices reach $26 per pound, up 160% from February 2025 lows.

The Operator Landscape: Who Bears the Quota Burden

The DRC's largest cobalt producers operate under the same quota framework but with vastly different strategic positions. CMOC (China's largest cobalt producer by DRC output) and Glencore (the world's second-largest cobalt producer) represent the dominant operators, alongside Eurasian Resources Group and Huayou Cobalt.

The competitive dynamic between Chinese-owned operators and Western mining majors within this framework is genuinely novel. Both face identical forfeiture rules and deadline enforcement mechanisms, meaning institutional scale alone does not confer quota security. What matters is operational efficiency in moving material through customs and logistics pipelines within tight compliance windows.

Chinese-affiliated operators carry a structural advantage in this environment. Their integrated supply chains, spanning mine to cathode precursor, mean cobalt can move through processing stages within the DRC before export, reducing the customs declaration complexity that Western miners, who predominantly export raw or intermediate material, must navigate. This processing integration aligns naturally with ARECOMS's stated preference for redirecting forfeited quotas toward operators advancing local beneficiation.

The practical consequence is that quota redistribution to "national interest" projects disproportionately benefits operators already investing in DRC-based processing infrastructure, creating a regulatory incentive structure that reshapes the competitive landscape over time. For a broader view of how these dynamics affect global cobalt production, the implications extend well beyond the DRC's borders.

Penalties and Enforcement: What Operators Risk

ARECOMS has made clear that quota compliance is non-negotiable. The regulator holds authority to permanently revoke export rights for any of the following violations:

- Failure to ship allocated volumes within prescribed deadline windows

- Unauthorised transfer of quota rights to third parties

- Processing artisanal or third-party cobalt material without regulatory authorisation

- Any breach of broader DRC mining and export regulations

The permanent revocation provision is particularly significant. Unlike financial penalties, which can be absorbed as a cost of business, permanent export bans effectively eliminate an operator's ability to monetise its DRC cobalt assets. This existential enforcement mechanism gives ARECOMS leverage far exceeding its nominal regulatory role.

Downstream Consequences for the Global Battery Supply Chain

The structural reduction in DRC cobalt export availability carries cascading implications for battery cathode manufacturing across Asia, Europe, and North America. In addition, the DRC export suspension analysis highlights how these constraints are reshaping procurement strategies across the entire battery value chain.

Cobalt remains a critical input for two dominant lithium-ion battery chemistries. NMC (nickel-manganese-cobalt) formulations, widely used in electric vehicle applications requiring high energy density and long cycle life, contain cobalt at ratios ranging from 10% to 33% of cathode material by weight. LCO (lithium cobalt oxide) chemistries, prevalent in consumer electronics, are even more cobalt-intensive.

The often-cited alternative, LFP (lithium iron phosphate), eliminates cobalt entirely and has gained significant market share in budget electric vehicles and stationary energy storage. However, LFP's lower energy density limits its suitability for premium long-range vehicle segments and aviation applications, meaning cobalt-intensive chemistries will retain substantial market relevance through the decade.

Technology transitions in battery chemistry take years to complete at scale. Cathode production lines are capital-intensive and built around specific material specifications. Switching from NMC to LFP is not a procurement decision but a multi-year re-engineering process, meaning downstream manufacturers are exposed to DRC cobalt supply constraints regardless of their long-term chemistry roadmaps.

The battery industry's cobalt dependency is not simply a function of current chemistry preferences. It reflects years of capital investment in production infrastructure that cannot be redirected quickly, making DRC supply policy decisions feel like seismic events in Tokyo, Seoul, and Stuttgart simultaneously.

Strategic Responses from Downstream Manufacturers

Battery manufacturers and automotive OEMs are deploying several parallel strategies in response to the new supply environment:

- Inventory build-up: Accelerating strategic stockpiling of cobalt metal and cobalt sulfate ahead of further quota tightening.

- Long-term offtake agreements: Locking in supply directly with DRC operators at current prices to hedge against further price appreciation.

- Cobalt recycling investment: Scaling up hydrometallurgical recycling of end-of-life battery packs as a secondary cobalt source, though volumes remain insufficient to offset primary supply constraints at current EV penetration rates.

- Supply chain geographic diversification: Exploring alternative primary sources, including Australia's cobalt-nickel laterite deposits and the Philippines, though neither jurisdiction can replicate DRC-scale output in the near term.

Canada and Japan have entered discussions on critical minerals cooperation frameworks, including potential joint stockpiling arrangements and co-investment in mining projects outside the DRC. While these initiatives reflect genuine strategic urgency, they address long-term resilience rather than near-term supply gaps.

The next major ASX story will hit our subscribers first

Is the DRC Model a Blueprint for Other Resource Nations?

The DRC's quota architecture is not emerging in isolation. It represents the latest iteration of a broader producer-nation movement toward structured resource sovereignty, distinct from the reactive nationalisations of earlier decades. The Congolese cobalt rivalry between major powers further intensifies the geopolitical stakes of this supply management model.

| Country | Commodity | Policy Mechanism | Objective |

|---|---|---|---|

| DRC | Cobalt | Export quota + state reserve | Price stabilisation, value capture |

| Indonesia | Nickel | Export ban (ore) | Downstream processing growth |

| Zimbabwe | Lithium | Export restrictions | Local beneficiation mandate |

| Chile | Copper / Lithium | State ownership expansion | Revenue maximisation |

| China | Rare Earths | Export controls + quotas | Strategic leverage |

Indonesia's nickel export ban, introduced in 2020 and upheld despite WTO challenges, demonstrated that resource-rich nations can enforce supply controls without fatally undermining foreign investment. According to Benchmark Minerals, the downstream processing ecosystem that subsequently developed in Indonesia, anchored by Chinese nickel smelting investment, validated the economic logic of beneficiation-linked resource nationalism. The DRC has observed this experiment closely, and ARECOMS's preference for redirecting quota capacity toward local processing projects echoes Indonesia's industrial policy playbook precisely.

The critical difference is cobalt's market structure. Nickel has multiple large producers across multiple jurisdictions. Cobalt does not. The DRC's 70%-plus reserve concentration gives it pricing leverage that Indonesia could only approximate. This means the DRC's quota system is inherently more consequential for global commodity markets than any comparable single-nation policy intervention in recent memory.

The Structural Shift From Buyer's Market to Seller's Market

The 2022-2024 cobalt market represented an extreme buyer's market, driven by post-pandemic inventory overhang and accelerating Chinese production capacity. Prices fell to levels that, adjusted for inflation, rivalled historical troughs. Producer margins collapsed, exploration investment dried up, and project development outside the DRC stalled entirely.

The DRC's export controls have structurally reversed this dynamic. With ARECOMS retaining discretionary authority over both the volume and destination of cobalt exports, producers and consumers alike must now price in a persistent policy risk premium that did not exist in the pre-2025 market. This premium is not speculative; it reflects the genuine possibility that ARECOMS could tighten quotas further, reassign allocations, or introduce new compliance requirements with limited notice.

Whether the current quota framework represents a permanent feature of the cobalt market or a transitional mechanism tied to specific price recovery targets remains genuinely uncertain. ARECOMS has not published explicit price thresholds that would trigger quota relaxation. As Fastmarkets notes, this leaves producers and downstream buyers to interpret regulatory signals rather than plan against transparent policy benchmarks. This opacity is itself a supply management tool, because it discourages forward selling by producers and incentivises precautionary buying by consumers.

For investors and supply chain strategists, Congo cobalt export quotas through 2027 present a landscape defined by structural constraint, administrative amplification of that constraint, and increasing policy discretion concentrated in a single regulatory body operating with limited external accountability. The era of abundant, predictably-priced DRC cobalt is over. What follows will be shaped as much by ARECOMS's strategic decisions as by any shift in electric vehicle demand.

Frequently Asked Questions: Congo Cobalt Export Quotas

What is the DRC's annual cobalt export cap for 2026 and 2027?

The DRC has established a hard annual export ceiling of 96,600 tonnes for both 2026 and 2027. This represents approximately 48% of the country's 2024 cobalt production of around 204,000 tonnes, making it one of the most significant structural supply constraints in recent commodity market history.

What happens to unused cobalt export quotas in the DRC?

Any quota volumes not utilised by the June 30 deadline for H1 2026 allocations are automatically forfeited and reassigned to ARECOMS's strategic quota reserve. These volumes cannot be carried forward and are deducted from companies' original baseline allocations.

Why are actual cobalt exports running below the quota cap?

Despite the 96,600-tonne annual limit, actual export volumes are estimated at between 33% and 50% of allocated quotas, driven primarily by administrative bottlenecks, customs processing delays, and logistics constraints rather than production shortfalls.

How much have cobalt prices increased since the DRC introduced export controls?

From their February 2025 lows, cobalt prices have risen approximately 160%, reaching $26 per pound ($57,320 per metric tonne) by mid-2026. The recovery began with a four-month export suspension and accelerated as the structured quota system took hold.

What penalties do companies face for violating DRC cobalt quota rules?

ARECOMS holds authority to permanently revoke cobalt export rights for violations including unauthorised quota transfers, processing unapproved material, missing shipment deadlines, or breaching broader mining regulations.

How does ARECOMS allocate cobalt export quotas?

Allocation is based primarily on historical export performance. Of the 96,600-tonne annual cap, 87,000 tonnes are distributed as basic quotas to registered producers, while 9,600 tonnes are retained by ARECOMS as a strategic reserve for state-directed deployment.

This article contains forward-looking analysis regarding commodity markets, regulatory frameworks, and supply chain dynamics. All market price data referenced reflects conditions reported as of mid-2026. Investors and supply chain professionals should conduct independent due diligence before making decisions based on the information presented here. Commodity markets are inherently volatile and subject to rapid change.

Want to Track the Next Major Commodity Supply Shift Before the Market Catches On?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including cobalt and battery metals — cutting through complex market data to surface actionable opportunities the moment they emerge on the ASX. Explore historic examples of major mineral discoveries and their remarkable returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the next structural shift in critical minerals supply.