May 20, 2026

The Hidden Geology of a Price Revolution: Why Copper's New Baseline Is Not What You Think

Most commodity price cycles follow a predictable arc. Demand surges, supply eventually catches up, prices normalise, and the cycle resets. Copper, however, is increasingly refusing to follow that script. What is unfolding in 2026 is not a cyclical spike fuelled by speculative excess but rather a fundamental repricing of a metal whose physical limitations are colliding head-on with civilisation-scale demand growth. The Cochilco copper price forecast is central to understanding why this requires looking beneath the surface of the price charts and into the geology, infrastructure timelines, and demand mathematics reshaping copper's long-term value floor.

When big ASX news breaks, our subscribers know first

Why Cochilco's Forecast Revision Is Unlike Anything in Recent Memory

Chile's state copper commission, the Comisión Chilena del Cobre or Cochilco, operates as the world's most data-rich copper market intelligence body. Drawing directly from production figures at Codelco, Chile's state-owned mining giant, as well as data from private operators and international trade flows, Cochilco's quarterly reports function as benchmark guidance for institutional investors, sovereign wealth funds, and mining companies globally. Chile's status as the world's largest copper-producing nation, responsible for approximately 22% of global mine output, gives its official forecasts an authority that investment bank models simply cannot replicate.

What makes the latest Cochilco copper price forecast so significant is not merely the number itself, but the speed and magnitude of its upward revision over the past twelve months. Furthermore, the copper price drivers underpinning these revisions are structural rather than transient, which distinguishes this cycle from previous episodes.

| Forecast Period | Published | Cochilco Average Price Forecast |

|---|---|---|

| 2025 and 2026 Outlook | May 2025 | US$4.30/lb |

| 2025 and 2026 Revised | November 2025 | US$4.45/lb (2025) / US$4.55/lb (2026) |

| 2026 Updated Forecast | February 2026 | US$4.95/lb |

| 2026 Latest Forecast | May 2026 | US$5.55/lb |

| 2027 Forward Guidance | May 2026 | US$5.10/lb |

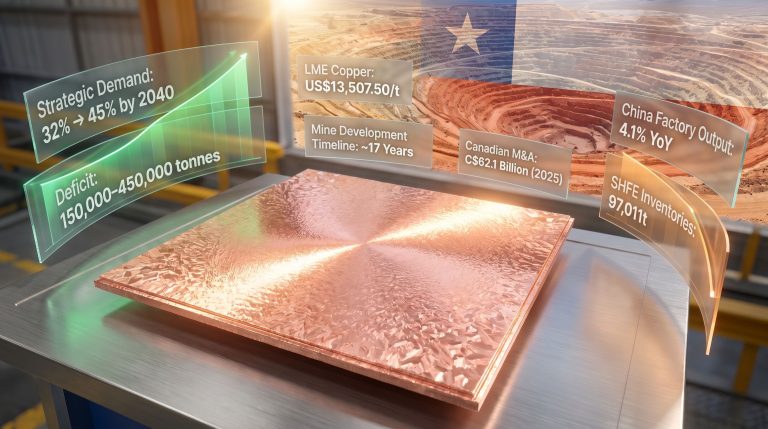

From approximately US$4.25/lb in early 2025 to US$5.55/lb as of May 2026, the commission has revised its 2026 average price forecast upward by roughly 30% within a single year. That is not a routine adjustment. It is a wholesale reassessment of copper's structural reality.

The May 2026 revision was partly anchored by record spot market activity. Copper reached US$6.29/lb on May 12, 2026, followed by a further print of US$6.15/lb on May 19, 2026. These intraday peaks are statistically significant because they compress the annual average upward, but more importantly, they signal that physical market participants are paying real-world premiums well beyond speculative positioning. According to Cochilco's revised price forecasts, these record highs reflect a fundamental shift in how the market values copper's long-term availability.

When a sovereign producer's official price forecast not only tracks but converges with record spot prices, the market is communicating something fundamental: this is not noise, it is a new signal.

The Four Structural Pillars Driving Demand Beyond Cyclical Norms

Energy Transition Infrastructure

Wind turbines, utility-scale solar installations, and grid-scale battery storage systems are all deeply copper-intensive. A single offshore wind turbine can require between 8 and 15 tonnes of copper, while solar photovoltaic installations use roughly 5 tonnes per megawatt of installed capacity. As decarbonisation commitments across the European Union, the United States, and Asia translate from policy into active procurement pipelines, the copper volumes required are becoming structurally locked in across multi-year project timelines.

Electric Vehicle Adoption

The copper content differential between electric vehicles and internal combustion engine equivalents is one of the most important and least appreciated figures in commodity markets. A conventional petrol or diesel vehicle contains approximately 20 to 25 kilograms of copper. A battery electric vehicle contains between 60 and 83 kilograms, rising to over 100 kilograms for larger commercial EVs and electric buses.

As global EV fleet penetration continues to compound, the cumulative copper demand increment is material. This is not a marginal uplift; it is a step-change in per-vehicle copper intensity, and consequently, in the volumes that mining operations must deliver each year.

Artificial Intelligence and Data Centre Buildout

Perhaps the most underappreciated demand driver in current commodity forecasts is the physical copper footprint of artificial intelligence infrastructure. A hyperscale data centre can require anywhere from 15 to 30 tonnes of copper in its power distribution, cooling systems, and server interconnects. With hundreds of such facilities announced or under construction globally as of 2026, aggregate copper demand from AI infrastructure buildout is beginning to register in physical market statistics in ways that traditional demand models were simply not designed to capture.

Grid Modernisation and Emerging Market Electrification

Ageing transmission and distribution infrastructure across North America, Europe, and parts of Asia requires wholesale replacement rather than incremental maintenance. Simultaneously, electrification programmes across Sub-Saharan Africa, South and Southeast Asia are adding an entirely new base layer of copper consumption that did not exist in previous demand cycles. This combination of replacement demand in mature economies and greenfield electrification in developing ones creates a demand floor that is broader and more durable than any previous copper supercycle.

What the Global Demand and Supply Numbers Actually Tell Us

Cochilco's Q1 2026 market trends report provides the following demand projections:

| Year | Global Refined Copper Demand | Year-on-Year Growth |

|---|---|---|

| 2026 | 28.2 million metric tons | +1.5% |

| 2027 | 28.8 million metric tons | +2.3% |

The acceleration from +1.5% in 2026 to +2.3% in 2027 is not coincidental. It reflects the compounding effect of energy transition project pipelines moving from planning and permitting phases into active execution and procurement. China remains the dominant demand centre, but European green infrastructure investment and US industrial reshoring are contributing meaningful incremental volumes.

On the supply side, however, the picture is more nuanced than headline growth figures suggest:

| Year | Global Mined Output | Year-on-Year Change |

|---|---|---|

| 2025 (estimated) | ~23.2 million metric tons | baseline |

| 2026 (forecast) | 23.3 million metric tons | +0.5% |

| 2027 (forecast) | 24.39 million metric tons | +4.7% |

A supply growth rate of just 0.5% in 2026 against demand growth of 1.5% is the arithmetic of structural tightness. The projected 2027 supply surge of +4.7%, driven primarily by output growth in the Democratic Republic of Congo, Zambia, Mongolia, Canada, and the United States, represents the primary bullish counter-thesis. However, mining professionals familiar with project execution in these jurisdictions understand that headline growth forecasts carry significant delivery risk.

Project timelines in the DRC and Zambia are routinely extended by infrastructure constraints, political risk, and wet season logistics. Mongolian copper expansion is subject to ongoing negotiations between operators and the government regarding fiscal terms. Even Canadian and US projects face permitting timelines that can extend by years beyond initial schedules. Consequently, the 4.7% supply growth figure for 2027 is a ceiling, not a floor.

Understanding the Market Balance: Why a 12,000-Tonne Surplus Is Meaningless

| Year | Market Balance | Volume |

|---|---|---|

| 2025 | Deficit | -124,000 metric tons |

| 2026 | Marginal Surplus | +12,000 metric tons |

| 2027 | Moderate Surplus | +153,000 metric tons |

The 2025 refined copper deficit of 124,000 metric tons set the supply baseline entering 2026 with depleted physical buffers. The projected 2026 surplus of 12,000 metric tons in a market of 28.2 million metric tons represents a buffer ratio of just 0.04%, which is functionally indistinguishable from equilibrium. Indeed, the ongoing copper supply crunch means this marginal surplus offers virtually no price relief for downstream buyers.

A 0.04% surplus ratio means that a single unplanned shutdown at one major Chilean or Peruvian operation could instantly erase the entire year's supply cushion. This is why spot prices are trading well above even the revised average forecast.

This statistical reality has important implications for how traders and investors should interpret price signals. The refined copper market balance is not a real-time gauge; it is an ex-post accounting. Persistent backwardation, where nearby delivery copper trades at a premium to forward months, is one of the most reliable indicators of genuine physical tightness, and it has been a recurring feature of the copper market throughout 2025 and into 2026.

Chile's Domestic Production: The Ore Grade Problem Is Structural

| Year | Chile Mine Output | Year-on-Year Change | Global Share |

|---|---|---|---|

| 2025 (estimated) | ~5.41 million metric tons | baseline | ~22% |

| 2026 (forecast) | 5.3 million metric tons | -2.0% | ~22% |

| 2027 (forecast) | 5.5 million metric tons | +4.0% | ~22% |

Cochilco attributes Chile's forecast 2026 production decline to four overlapping factors:

- Declining ore grades at mature deposits across the Atacama and adjacent mining districts

- Scheduled maintenance shutdowns at major operations including assets within the Codelco portfolio

- Operational constraints including water availability challenges in one of the world's driest mining regions

- Weak early-year performance that compressed the statistical baseline for annual averages

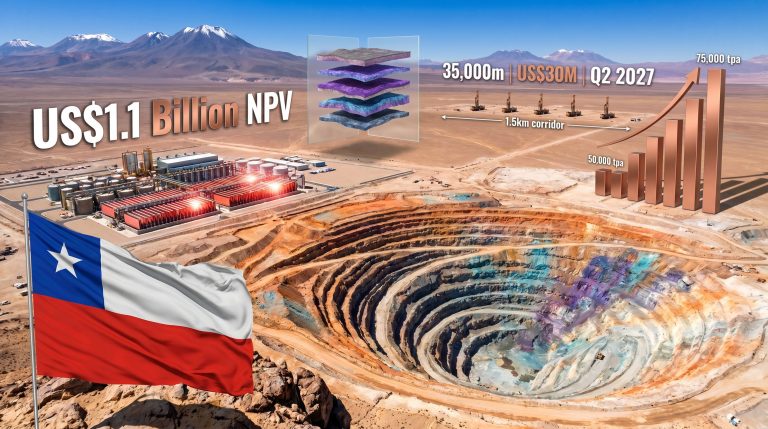

The ore grade issue deserves particular attention because it is the most structurally significant of these four factors. Chile's copper supply gap is partly rooted in grade decline that has been accelerating for decades. In the 1990s, average ore grades at Chilean operations frequently exceeded 1.5% copper. By the mid-2020s, many operations are processing material at 0.5% to 0.7%, sometimes lower.

Grade decline is not recoverable through operational efficiency alone. It requires either accessing deeper higher-grade zones, which involves substantial capital investment, or discovering and developing new deposits, a process that typically takes 15 to 20 years from discovery to first production. This geological reality is one of the most powerful and least visible forces underpinning the long-term copper price thesis.

The next major ASX story will hit our subscribers first

How the Cochilco Forecast Compares to Broader Market Intelligence

Cochilco's methodology differs materially from how investment banks and multilateral institutions model copper prices. Investment bank models incorporate financial derivatives positioning, hedge fund flows, and macro factor sensitivities. Cochilco, by contrast, builds its forecasts from the ground up using actual production data from operating mines, national trade statistics, and direct engagement with operators through Chile's copper market monitoring mandate.

This methodology typically produces more conservative estimates than speculative market pricing. When Cochilco's sovereign producer forecast of US$5.55/lb converges with or even lags behind physical spot prices trading above US$6.00/lb, it signals that the physical market has moved beyond what even a data-rich institutional forecast had anticipated. Furthermore, copper investment strategies must account for this gap between official forecasts and real-world price discovery.

The shape of the copper futures curve also provides information that average forecasts cannot. When copper trades in backwardation, meaning cash prices exceed three-month forward prices, it indicates that buyers are willing to pay a premium for immediate delivery, reflecting genuine inventory scarcity rather than financial speculation.

Risk Factors: Both Directions Matter

Downside Risks to the Bullish Thesis

- Chinese demand deceleration: A sharper contraction in Chinese property construction or manufacturing activity would reduce the world's largest copper consumer's offtake materially

- Trade policy reversal: Re-escalation of US-China tariff tensions could reverse the demand sentiment improvements that supported mid-2025 price recovery

- Above-forecast supply delivery: If DRC, Zambia, and Mongolian projects deliver ahead of schedule, the 2027 surplus could be larger than projected, capping price upside

- Material substitution at extreme prices: Aluminium can partially substitute for copper in power transmission applications above certain price thresholds, though the substitution is technically complex and limited in scope

Upside Risks That Could Extend the Price Rally

- Labour disruptions in Chile or Peru: Both countries have histories of mine worker strikes at major operations. A significant disruption at Escondida, the world's largest copper mine, could alone shift the 2026 market back into deficit

- Geopolitical instability in Central Africa: The DRC's copper belt, which is central to the 2027 supply growth forecast, operates in a geopolitically complex environment where output disruptions have historically been underestimated

- Financial market amplification: Commodity fund inflows and exchange-traded product positioning can amplify physical tightness into price spikes that significantly exceed underlying fundamental values

The asymmetry of risks in this market is notable. Downside scenarios generally require multiple simultaneous negative developments, while a single supply shock in a market with virtually no inventory buffer can trigger significant upside price moves.

Investment and Industry Implications

For mining companies and capital allocators, sustained copper pricing above US$5.00/lb materially transforms project economics. Deposits that were marginal at US$3.50/lb become highly economic, and previously sub-economic resources in higher-cost jurisdictions such as Canada, the United States, and parts of Europe suddenly attract feasibility-level attention. The future of copper mining will consequently be shaped as much by price environment as by technological capability.

However, it is important to note that price alone does not accelerate permitting timelines, reduce community consultation requirements, or fast-track environmental assessments. The lag between a high-price signal and new mine production reaching market remains one of the most structurally important features of the copper supply landscape.

For the broader energy transition, copper price inflation at this scale introduces genuine cost pressures into renewable energy, electric vehicle, and grid infrastructure projects. If copper prices remain structurally elevated through the 2030s, the economics of some transition projects will need to be revisited. Furthermore, as analysts at Kitco note, the strategic case for accelerating copper recycling and secondary supply development becomes increasingly compelling at these price levels.

Frequently Asked Questions: Cochilco Copper Price Forecast

What is Cochilco's latest copper price forecast for 2026?

As of May 2026, the Cochilco copper price forecast for the full year 2026 average stands at US$5.55 per pound, raised from the prior estimate of US$4.95/lb published in February 2026.

What is Cochilco's copper price forecast for 2027?

Cochilco projects copper prices will average US$5.10 per pound in 2027, supported by ongoing structural demand from energy transition, electric vehicles, and AI infrastructure, even as supply growth from new projects accelerates.

Why has the Cochilco copper price forecast risen so sharply?

The revisions reflect a combination of a 124,000-tonne refined copper deficit in 2025, record spot prices above US$6.00/lb in May 2026, and robust demand growth from structural end-use sectors including EVs, renewables, and data centres.

How much copper does Chile produce?

Chile is forecast to produce approximately 5.3 million metric tons of copper in 2026, representing roughly 22% of global mine output.

What is the global copper market balance outlook?

After a 124,000-tonne deficit in 2025, the market is expected to shift to a marginal surplus of just 12,000 tonnes in 2026, before widening to 153,000 tonnes in 2027. The 2026 surplus represents less than 0.05% of total market volume and provides negligible price relief.

Key Takeaways at a Glance

- The Cochilco copper price forecast for 2026 has been revised upward by approximately 30% within twelve months, reaching US$5.55/lb

- Record spot prices of US$6.29/lb on May 12 and US$6.15/lb on May 19 confirm physical markets are operating well above even the revised average

- The 2026 refined market surplus of just 12,000 tonnes in a 28-million-tonne market provides no meaningful price buffer

- Chile's own production is forecast to decline 2% in 2026, driven by ore grade deterioration and operational constraints

- The 2027 supply growth forecast of +4.7% carries significant execution risk across DRC, Zambia, and Mongolian jurisdictions

- Structural demand from EVs, renewable energy, AI infrastructure, and grid modernisation remains the primary long-term price support mechanism

- The geology of declining ore grades at mature Chilean deposits is a structural, multi-decade constraint that no short-term operational fix can resolve

Disclaimer: This article is provided for informational and educational purposes only and does not constitute financial, investment, or professional advice. Commodity price forecasts involve significant uncertainty, and actual outcomes may differ materially from projections. Readers should conduct their own due diligence before making any investment decisions.

Want to Capitalise on the Next Major Copper Discovery Before the Broader Market?

As copper's structural repricing reshapes global mining economics, Discovery Alert's proprietary Discovery IQ model delivers real-time ASX alerts on significant copper and mineral discoveries, transforming complex geological data into actionable investment insights — explore historic discovery returns to understand the opportunity, then begin a 14-day free trial at Discovery Alert to position ahead of the market.