May 19, 2026

When Geology Outpaces the Market: The Case for District-Scale Copper Thinking in the Atacama

Sediment-hosted copper deposits occupy a unique place in the global mining landscape. Unlike porphyry systems that require massive infrastructure and years of bulk-tonnage processing to justify development, manto-style mineralisation in arid, infrastructure-rich jurisdictions can transition from discovery to production at a pace and capital intensity that challenges conventional valuation frameworks. When those systems also carry leach-amenable copper mineralogy, the economics become genuinely differentiated.

This is the lens through which the Marimaca Copper Pampa Medina expansion deserves to be examined, not as a news item about drill results, but as a structural revaluation event playing out in slow motion while the broader copper market remains distracted by macro noise. Furthermore, understanding the copper market trends shaping 2025 and beyond provides essential context for why this story matters to investors right now.

When big ASX news breaks, our subscribers know first

From Single Asset to District Operator: The Strategic Pivot That Changes Everything

The Hub-and-Spoke Logic Behind MOD as Processing Anchor

For junior and mid-tier copper developers, the difference between a single-asset company and a district-scale operator is not merely geological. It is a valuation category shift. Single-asset developers are priced on discounted cash flows from one project. District operators command premium multiples because optionality, resource replacement, and production scalability are all embedded in the asset base.

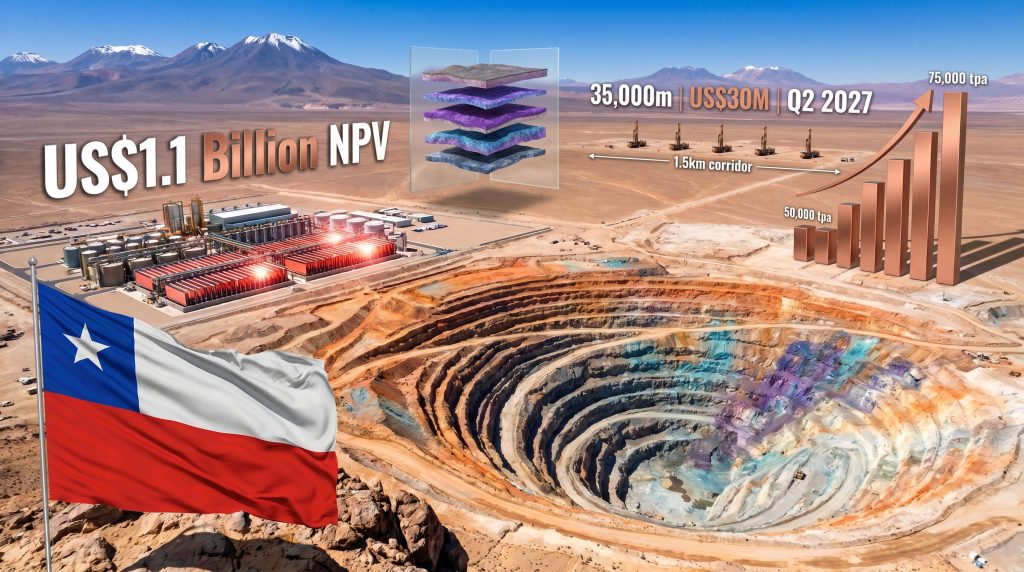

Marimaca Copper (TSX: MARI) is navigating precisely this transition. The Marimaca Oxide Deposit (MOD) has long served as the company's primary value anchor, with a pre-tax NPV8 of US$1.1 billion at US$5 per pound copper and a production design targeting 50,000 tonnes per year of copper cathode. However, Pampa Medina, located approximately 28 kilometres from MOD, is now reshaping the growth ceiling of the entire operation.

The hub-and-spoke development model, where MOD functions as the central processing anchor and Pampa Medina feeds incremental oxide tonnes into the same production chain, is not a speculative scenario. Management has publicly outlined a pathway to 75,000 tonnes per annum cathode production by incorporating Pampa Medina's oxide resources. That represents a 50% production uplift from a single satellite discovery, without the capital intensity of building a standalone second operation.

Why Atacama-Based Sediment-Hosted Systems Command Premium Valuations

Chile's Atacama region hosts some of the world's most capital-efficient copper deposits. The combination of exceptional ore oxidation, minimal water competition in legacy oxide systems, proximity to established port and power infrastructure, and a mature mining regulatory environment creates conditions that are increasingly rare globally. In addition, the Chile copper outlook remains broadly constructive, reinforcing the strategic value of assets positioned in this jurisdiction.

Sediment-hosted manto deposits in this context carry an additional premium: their flat-lying geometry often enables low strip-ratio open pit or simple underground development, while their leach-amenable mineralogy avoids the capital-heavy flotation circuits required by sulphide porphyry systems. When grade and continuity align at district scale, these systems have historically attracted major mining company interest or standalone production development, sometimes both.

Pampa Medina Geology: Reading the Drill Data Through a Structural Lens

What Consistent Intercepts Across Every Drill Hole Actually Signals

The most technically significant aspect of the Pampa Medina drill program to date is not any single high-grade intercept. It is the fact that mineralisation has been encountered in every single drill hole completed across the defined footprint. In resource geology, this distinction matters enormously.

Patchy or sporadic mineralisation, even at high grades, creates interpolation uncertainty that inflates the inferred-to-indicated conversion cost and timeline. Continuous mineralisation across a 1.5-kilometre north-south strike and 600 to 800 metres east-west width means that each new drill hole adds tonnage rather than merely refining confidence in existing material.

"Key Geological Insight: Consistent mineralisation across every drill hole over a north-south strike exceeding 1.5 kilometres and an east-west width of 600 to 800 metres is the geological signature of a system with genuine bulk-tonnage potential, not an isolated high-grade lens. This is the geometry that defines economically significant sediment-hosted copper districts globally."

Five Stacked Mantos Across 400 Metres: What This Means for Development Scenarios

One drill hole stands apart in the Pampa Medina dataset. It intersected five stacked manto horizons across 400 metres of mineralised package, a result that fundamentally altered the geological model. Prior to this, the deposit was being evaluated primarily as a series of discrete oxide and shallow sulphide targets. The stacked manto architecture opens two distinct development pathways:

- Large-scale open pit: Targeting the full 400-metre mineralised package at a bulk grade approximating ~0.5% copper, optimised for throughput and cost per tonne of ore

- Selective underground mining: Targeting the highest-grade 20 to 50-metre horizons within the stack, optimising for grade and capital efficiency at the expense of total tonnage

Neither scenario is yet deterministic. The maiden resource estimate, targeted for Q2 2027, will provide the foundation for scenario economics. What is already clear is that the deposit type, analogous to world-class sediment-hosted systems, generates highly competitive unit costs per tonne of ore when developed at scale.

Bornite and Chalcocite: The Mineralogical Advantage That Rewrites the Capex Equation

The dominant copper minerals at Pampa Medina are bornite and chalcocite, both of which are amenable to heap leaching and solvent extraction-electrowinning (SX-EW) processing. This is not a minor technical footnote. Consequently, the copper price drivers favouring low-cost oxide production make this mineralogical profile particularly timely.

| Copper Mineral | Heap Leach Amenability | Typical Recovery Rate | Processing Route |

|---|---|---|---|

| Bornite | High | 75 to 85% | SX-EW / Heap Leach |

| Chalcocite | High | 80 to 90% | SX-EW / Heap Leach |

| Chalcopyrite | Low to Moderate | 30 to 50% | Flotation / Concentrate |

Chalcopyrite is also present in portions of the resource and would likely require conventional flotation and concentrate production, which carries significantly higher capital intensity. The metallurgical balance between these mineral assemblages will be a key variable in the prefeasibility scenario work. Management has confirmed that metallurgical testwork is ongoing.

"Strategic Callout: The dominance of heap-leachable copper minerals at Pampa Medina creates a potential pathway to production expansion at significantly lower capital intensity than conventional sulphide concentrate projects of equivalent scale. For a project already anchored to an SX-EW cathode operation at MOD, this mineralogical alignment is a genuine project economics differentiator."

Expansion Vectors: The 3 to 4 Kilometre Northern and Southwestern Corridors

Current drilling has defined the core discovery zone, but the geological team has identified mineralisation trends extending 3 to 4 kilometres north and at least 1 kilometre southwest of the present footprint. These vectors are based on structural geology interpretation and geochemical sampling rather than confirmed drilling, and should be treated as exploration targets rather than resource extensions.

That said, in sediment-hosted manto systems, structural controls on mineralisation tend to be consistent along strike. If the same depositional horizon extends into these corridors at comparable grades, the total system scale could be substantially larger than the current drilling envelope suggests. The mineral exploration importance of establishing these corridors early cannot be overstated in terms of long-term resource potential.

The Drilling Architecture: How 35,000 Metres and US$30 Million Define a Resource

Why Budget Discipline Reflects Geological Confidence

Marimaca originally allocated a higher drilling budget for Pampa Medina. The reduction to US$30 million was not a capital constraint decision. It reflects the geological reality that exceptional mineralisation continuity requires less drilling density to achieve inferred resource classification.

Standard inferred resource drill spacing for comparable sediment-hosted deposits can be as wide as 1,600 metres. The Pampa Medina program is targeting 150 metres by 150 metres spacing, which is far tighter than the minimum required, but reflects management's objective of establishing a maiden resource with a meaningful confidence level rather than simply meeting the minimum technical threshold.

| Metric | Pampa Medina Program | Comparable Project Benchmark |

|---|---|---|

| Target drill spacing | 150m x 150m | 1,600m (inferred resource standard) |

| Total metres planned | 35,000m | Variable |

| Budget allocated | US$30 million | N/A |

| Drilling completion target | September 2026 | N/A |

| Maiden resource target | Q2 2027 | N/A |

| Resource calculation timeline | 6 to 7 months post-drilling | Industry standard |

The Transition From Discovery Drilling to Resource Delineation

The current program marks a clear transition from Phase I discovery drilling, which involved approximately 10,000 metres to establish the deposit's existence and geometry, to Phase II delineation drilling across 35,000 metres designed to achieve maiden resource classification. This progression is standard in resource development, however the speed of the transition at Pampa Medina is notable.

It is driven directly by the mineralisation consistency that eliminated the need for extensive infill drilling before delineation could begin. Management has been explicit that the Q2 2027 maiden resource will represent a partial snapshot of the identified mineralisation envelope. The resource boundary will be constrained to the drilled area, leaving material outside that footprint unclassified but geologically interpreted.

This framing is important for investors: the maiden resource is a starting point for economic assessment, not a ceiling on total system potential.

MOD as the Valuation Floor: What the Numbers Actually Say

The Enterprise Value Arbitrage That Defines the Current Opportunity

At a market capitalisation of approximately C$1.2 billion and cash holdings of C$160 million, the implied enterprise value for Marimaca approximates the standalone NPV of MOD at conservative discount multiples. This mathematical relationship carries a specific implication: Pampa Medina's oxide expansion potential, known sulphide resource potential, and all exploration upside beyond the current drill footprint are collectively assigned near-zero market value.

"Valuation Snapshot: With enterprise value approximating MOD's standalone NPV at conservative discount multiples, the current market capitalisation implies that Pampa Medina's oxide and sulphide potential carries minimal market attribution. This creates a structural asymmetry where exploration success generates incremental valuation upside against a relatively stable downside floor."

The C$409 Million Capital Raise as a Confidence Signal

In February, Marimaca completed a C$409 million capital raise, a transaction that warrants examination beyond its headline number. Capital raises of this scale in the mid-tier copper development segment are not routine. The willingness of institutional investors to participate at this quantum, given the project stage, reflects conviction in both the MOD economics and the emerging Pampa Medina thesis.

The raise provides construction capital depth for MOD's early works program while simultaneously funding the Pampa Medina delineation campaign. This dual-track capital allocation is deliberate and signals that management is not sequencing these projects but advancing them in parallel, which is the correct strategy given the timeline alignment between MOD's construction decision (early 2027) and Pampa Medina's maiden resource (Q2 2027).

Debt Financing Dynamics at the Mid-Tier Scale

MOD's project financing profile sits in a particularly attractive band for debt markets. At an estimated capital requirement in the ~US$300 million range, the project is large enough to support structured debt financing but small enough to avoid the complexity and syndication challenges of billion-dollar project loans. Management has reported strong lender interest with minimal resistance to the project's fundamentals, reflecting the combination of Chilean jurisdiction quality, MOD's standalone bankability, and the company's substantial equity buffer from the recent raise.

Sulfuric Acid: The Operational Hedge That Most Investors Overlook

Why Acid Cost Volatility Is a Structural Risk for Oxide Copper Producers

Heap leach and SX-EW operations consume sulfuric acid as a primary processing reagent. Acid costs can represent 15 to 25% of total operating costs for oxide copper producers, making price volatility a genuine margin risk. The spot acid market is also influenced by fertiliser production cycles, smelter by-product availability, and shipping logistics, creating cost unpredictability that is structurally difficult to hedge through conventional financial instruments.

Marimaca's solution is elemental sulfur burning, a strategy that converts elemental sulfur into sulfuric acid on-site through a straightforward combustion and absorption process. The chemistry is well-established: one tonne of elemental sulfur produces approximately three tonnes of sulfuric acid, providing a direct self-production pathway.

| Cost Metric | Market Spot Price | Self-Production Estimate | Payback Period |

|---|---|---|---|

| Sulfuric acid (per tonne) | ~US$400 | Below US$250 | 12 to 14 months |

| Conversion ratio | N/A | 1t sulfur = 3t acid | N/A |

Elemental Sulfur as Both a Cost Hedge and a Supply Chain Simplification

Beyond direct cost savings, elemental sulfur burning addresses a logistics challenge that is rarely discussed in investor materials. Sulfuric acid is classified as a hazardous material with significant storage and transport requirements. On-site acid inventory typically requires 30 to 40 days of supply in expensive acid-resistant concrete tankage.

Elemental sulfur, by contrast, can be stored in open-air stockpiles without containment infrastructure, dramatically reducing working capital tied up in inventory and eliminating the logistics complexity of regular acid shipments. The supply source adds another layer of strategic logic, as Canadian oil sands operations generate elemental sulfur as a refining by-product and face increasing pressure to manage this material responsibly. This creates a structural supply surplus at competitive prices, providing Marimaca with both cost certainty and supply reliability from a well-established industrial chain.

The next major ASX story will hit our subscribers first

Construction Readiness: The Critical Path to Early 2027

Permitting Status and Early Works Optionality

MOD's permitting is substantially complete. The two to three remaining approvals are targeted for receipt by October 2026, ahead of the timeline required for a full final investment decision. Critically, existing permits already allow commencement of early works activities, meaning that certain site preparation, infrastructure, and procurement activities can begin before all permits are in hand.

This optionality is significant because it compresses the effective construction timeline. Contractors can be mobilised, long-lead items can be ordered, and site civil works can commence under the existing permit envelope, reducing the gap between FID and first production.

Transformer Availability: The Hidden Critical Path Risk

One supply chain risk that management has flagged, and that receives insufficient attention in standard project analysis, is transformer availability. The global energy transition has created unexpected demand for large industrial transformers, driven partly by grid expansion and renewable energy connections. With copper supply constraints ironically affecting the availability of copper-wound transformers, lead times have extended significantly across the industry.

For MOD, management has identified transformers as a critical path item and is actively managing procurement timing and deposit requirements. This is exactly the kind of operational detail that separates well-managed development projects from those that encounter avoidable construction delays.

Scenario Modelling: Three Outcomes and Their Market Implications

The investment thesis for the Marimaca Copper Pampa Medina expansion ultimately rests on three plausible scenarios for how the discovery resolves over the next 24 to 36 months. Furthermore, copper investment strategies that account for district-scale optionality are increasingly relevant to how sophisticated investors are positioning themselves in this sector.

| Scenario | Pampa Medina Outcome | Production Impact | Valuation Implication |

|---|---|---|---|

| Base Case | Maiden resource confirms 150m+ strike continuity | +25,000 tpa oxide expansion | Moderate re-rating |

| Bull Case | District-scale resource above 500Mt confirmed | Standalone development pathway | Significant re-rating |

| Bear Case | Resource below economic threshold | MOD standalone only | Valuation reverts to NPV floor |

"Investor Framework: When a company trades at a valuation that approximates the NPV of its most advanced asset alone, any additional resource discovery, production expansion, or exploration success represents incremental upside that the market has not yet priced. The relevant question for Pampa Medina is not whether it adds value, but when the market assigns that value and at what magnitude."

Disclaimer: Scenario projections are speculative and based on publicly available company disclosures. They do not constitute financial advice. Investors should conduct independent due diligence before making investment decisions.

Frequently Asked Questions: Marimaca Copper Pampa Medina Expansion

What is the Pampa Medina expansion and why does it matter?

Pampa Medina is a sediment-hosted copper discovery located approximately 28 kilometres from the Marimaca Oxide Deposit in northern Chile. It is being delineated as a potential district-scale sulphide and oxide resource that could expand MOD's annual production from 50,000 to 75,000 tonnes of copper cathode.

What copper minerals have been identified at Pampa Medina?

Drilling has confirmed bornite and chalcocite as the dominant copper minerals, both of which are amenable to heap leaching. Chalcopyrite is also present in portions of the deposit and would require conventional flotation processing. Recent bornite intersections announced by the company have further reinforced confidence in the deposit's mineralogical profile.

When will the maiden resource estimate be published?

Drilling of 35,000 metres across five rigs is targeted for completion by September 2026, followed by six to seven months of resource calculation work, with a maiden inferred resource estimate expected in Q2 2027.

How does the sulfuric acid strategy protect project margins?

By burning elemental sulfur on-site, the company can produce sulfuric acid at below US$250 per tonne compared to spot market prices around US$400 per tonne, with payback on the capital investment estimated at 12 to 14 months. The strategy also eliminates complex acid storage and logistics requirements.

What permits are still required before full construction can begin?

Two to three remaining permits are expected by October 2026. Early works can commence under existing permit approvals ahead of the full final investment decision.

Key Takeaways: The Pampa Medina Expansion in Full Context

| Metric | Detail |

|---|---|

| MOD Pre-Tax NPV8 at US$5/lb Cu | US$1.1 billion |

| MOD Annual Production Target | 50,000 tpa copper cathode |

| Expanded Production Potential (with Pampa Medina) | 75,000 tpa |

| Pampa Medina Strike Length (confirmed) | 1.5 km N-S, 600 to 800m E-W |

| Growth Corridors Identified | 3 to 4 km north, 1 km southwest |

| 2026 Drilling Program | 35,000m across 5 rigs |

| Drilling Budget | US$30 million |

| Maiden Resource Target | Q2 2027 |

| Distance from Pampa Medina to MOD | ~28 km |

| Cash Position | C$160 million |

| Market Capitalisation | ~C$1.2 billion |

| Capital Raise (February) | C$409 million |

The structural case for the Marimaca Copper Pampa Medina expansion rests on a convergence of geological quality, mineralogical processing advantage, and valuation asymmetry that is rarely available in a single mid-tier copper story. MOD provides the production foundation and valuation floor. Pampa Medina provides the growth ceiling, and that ceiling remains undefined at a scale the current market price has not yet begun to reflect.

Readers seeking additional institutional-grade analysis of Marimaca Copper and the Pampa Medina discovery can explore further coverage at Crux Investor, which publishes detailed mining sector research across copper and other critical resource commodities.

Want To Be First When the Next Major Copper Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex mineralogical and resource data into actionable investment insights for both short-term traders and long-term investors. Explore historic examples of major mineral discoveries and their market returns, then begin your 14-day free trial to ensure you're positioned ahead of the market when the next district-scale copper story emerges.