August 1, 2026

When the World Runs Out of Time to Build New Mines

Every major commodity cycle eventually confronts a simple arithmetic problem: demand grows faster than new supply can be brought online. For copper, the copper supply shortage and China demand weakness dynamic has been deteriorating for years, but the timeline has now compressed to the point where even optimistic mine development scenarios cannot close the gap before the late 2020s. The average copper mine takes roughly 17 years to move from initial discovery through permitting, construction, and into meaningful production. That figure alone reframes every short-term price movement as a distraction from a structural reality that no quarterly data release can alter.

What makes the current copper market particularly complex is that this long-run scarcity narrative is unfolding at precisely the same moment that near-term indicators are flashing weakness. The result is a genuine analytical tension between what copper prices are doing today and what the copper market almost certainly needs to do over the next decade to incentivise sufficient supply. Understanding which signal to prioritise, and on what timeframe, is the central challenge facing both industrial buyers and capital allocators right now.

When big ASX news breaks, our subscribers know first

The Supply Side: A Structural Problem Built Over Decades

Why Production Growth Has Nearly Stalled

Global refined copper production is forecast to expand by approximately 0.9% in 2026, a rate so modest it barely registers against the electrification demand trajectory being built into infrastructure planning cycles worldwide. This is not a cyclical dip in mine output; it reflects cumulative underinvestment across the exploration and development pipeline stretching back more than a decade. Furthermore, the copper exploration pipeline has been chronically underfunded, meaning the consequences of that underinvestment are only now becoming fully apparent.

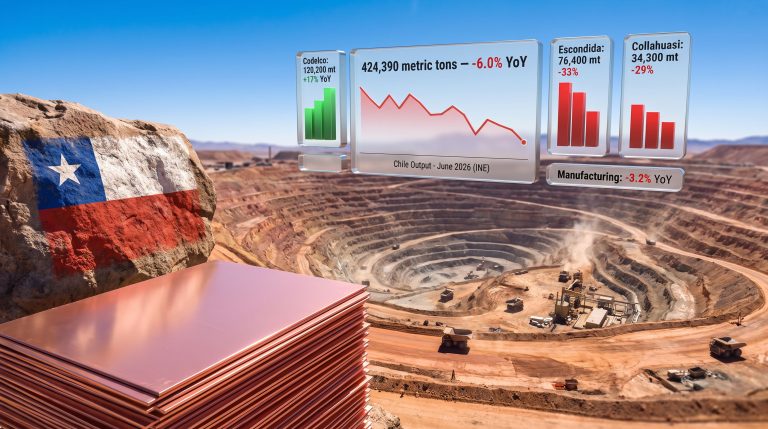

The numbers from BHP's August 2025 outlook are particularly striking. The miner, one of the most analytically rigorous voices in the global copper industry, forecast zero net production growth from Chile between 2031 and 2040, despite rising capital expenditure across both greenfield and brownfield projects. Chile is the world's single largest copper-producing nation, and a flat output trajectory from that jurisdiction through an entire decade carries enormous implications for the global supply-demand balance.

As Fitzroy Minerals President and CEO Merlin Marr-Johnson noted in reference to BHP's assessment, production growth within Chile and globally is proving extremely difficult because the industry is struggling simply to maintain existing output levels, let alone meaningfully expand it, and this dynamic points toward a material repricing of copper over time.

| Supply Constraint Factor | Current Status (2026) | Long-Term Implication |

|---|---|---|

| Global refined copper production growth | ~0.9% forecast for 2026 | Insufficient to meet electrification demand |

| Average mine development timeline | ~17 years from discovery to production | No near-term pipeline relief |

| Chile production growth (2031-2040) | Zero net growth forecast (BHP) | Structural supply gap deepening |

| Codelco 2030 production target | 1.7 million tonnes | Subject to governance and audit risk |

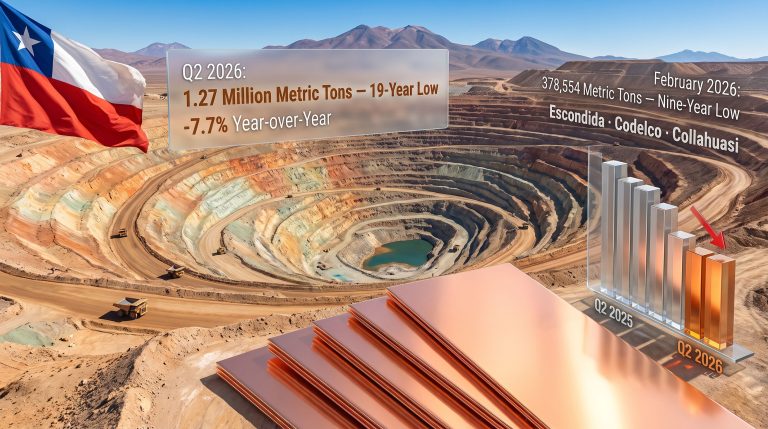

| ICSG projected 2026 deficit | ~150,000-450,000 tonnes (range across forecasts) | Deficit persists regardless of quarterly demand swings |

Declining Ore Grades: The Silent Multiplier

One factor that receives insufficient attention in mainstream copper commentary is the accelerating decline of ore grades at operating mines across Chile and Peru. As head grades fall, the same quantity of mined material yields progressively less contained copper. This means that maintaining flat production volumes requires either processing significantly more ore, or accessing deeper, harder-to-mine resources, both of which drive up operating costs and strip ratios.

The practical consequence is that declining grades function as a hidden tax on the existing supply base. Even mines that report stable or growing ore throughput may be delivering less copper to smelters while consuming more energy, water, and capital per tonne of metal produced. This dynamic is compounding the already-severe constraint imposed by the 17-year development timeline, because it means the existing supply base is quietly eroding at the same time that new supply is structurally delayed.

The Codelco Governance Problem

Overlay onto this picture a governance shock at the world's largest copper producer. On May 14, 2026, Chile's government announced the replacement of Codelco's chairman following a preliminary internal audit revealing that approximately 20,000 metric tonnes of copper had been improperly included in the company's 2025 production report. Mining Minister Daniel Mas tasked the incoming board under Bernardo Fontaine with overseeing an independent external audit.

For market analysts, a reporting discrepancy of this scale at a producer targeting 1.7 million tonnes of output by 2030 raises questions that extend well beyond Codelco itself. When a state-owned producer of this significance faces internal audit findings of this nature, the political risk premium applied to large government-controlled copper supply chains tends to expand across the board. The inverse effect is an uplift in the relative valuation attractiveness of development assets in transparent, rule-of-law jurisdictions where independent auditing frameworks are the standard rather than the exception.

China Demand Weakness: Cyclical Softness or Something More Concerning?

Decoding the April 2026 Data

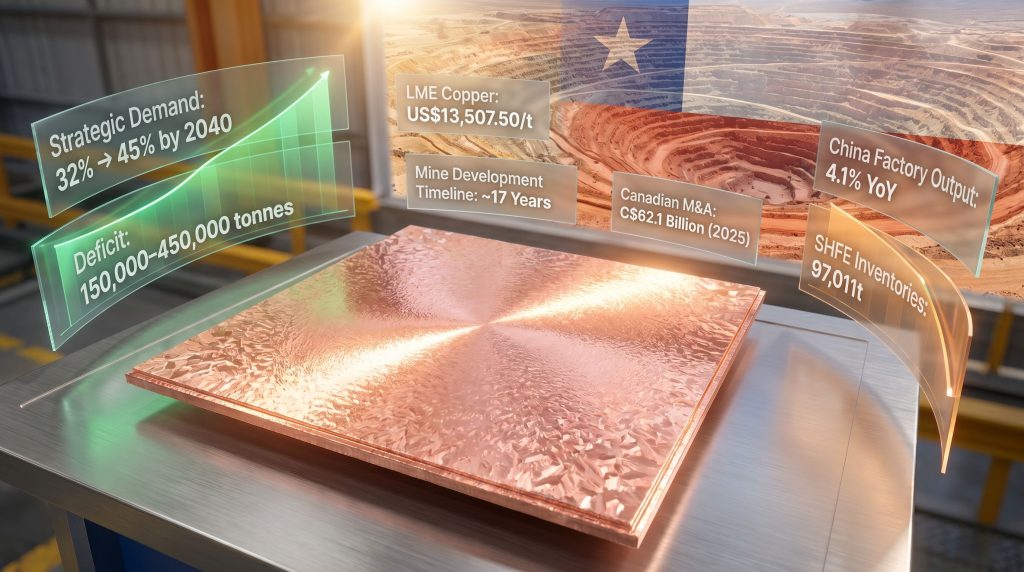

China's National Bureau of Statistics reported factory output growth of 4.1% year-on-year in April 2026, decelerating from 5.7% in March. Retail sales expanded just 0.2%, with both readings missing consensus estimates. Because China accounts for approximately 60% of global refined copper demand, a deceleration of 160 basis points in industrial production translates directly into measurable reductions in cathode and rod order flow. Indeed, according to Global X ETFs, renewed supply risks and Chinese demand trends remain two of the most closely watched variables for any near-term market rebound.

Two physical market indicators crystallised the demand destruction signal almost immediately:

- Shanghai Futures Exchange (SHFE) on-warrant copper inventories climbed from 88,077 tonnes on May 11 to 97,011 tonnes by May 14, ending a drawdown that had persisted since mid-March

- Chinese spot copper premiums over SHFE contract prices flipped into a discount, a direct signal that buyers are unwilling to pay above the futures price for immediate physical delivery

When both of these indicators move simultaneously in the same direction, they provide a coherent and mutually reinforcing demand destruction signal. The price threshold above which this destruction appears to be occurring is approximately US$13,500 per tonne, suggesting that at current price levels, downstream fabricators and manufacturers are choosing to defer purchases rather than absorb the cost.

Property Sector vs. Industrial Manufacturing: A Critical Demand Split

The nuance that matters most in the China demand analysis is the divergence between construction-related copper consumption and industrial manufacturing demand. China's property investment sector, historically one of the most copper-intensive components of the economy given the wiring, plumbing, and HVAC requirements of residential and commercial construction, continues to contract. Industrial manufacturing output, while decelerating, has not collapsed.

This split matters because it changes the recovery narrative. A rebound in property starts would restore a structural demand pillar that has been absent from the market for several years. A stabilisation in manufacturing output alone, without a property recovery, would provide a softer and less durable demand recovery signal.

Oil at US$110, the Dollar, and the Macro Transmission Chain

How Geopolitical Shocks Become Copper Price Events

The macro trigger that compounded existing China demand concerns in mid-May 2026 was the movement of Brent crude above US$110 per barrel following reported drone attacks on the United Arab Emirates. The transmission mechanism from energy markets to copper prices follows a fairly predictable chain:

- Geopolitical shock drives Brent crude above US$110/bbl

- Elevated oil prices push near-term inflation expectations higher globally

- Rising inflation expectations reduce the probability of Federal Reserve rate cuts in the near term

- Delayed rate-cut pricing provides support for, or actively strengthens, the US dollar index

- A stronger US dollar increases the effective cost of dollar-priced copper for buyers transacting in yuan, euro, or rupee

- Reduced purchasing power for non-US buyers suppresses near-term physical demand and order volumes

The asymmetric effect on the two major copper exchanges illustrated this transmission clearly. LME three-month copper fell 0.35% to US$13,507.50 per tonne, touching an intraday low of US$13,394.50 per tonne, while the SHFE most-active contract fell 1.40% to 104,330 yuan per tonne. The SHFE decline was approximately four times larger in percentage terms, directly reflecting the compounding effect of dollar strength on the yuan-denominated purchasing cost of copper.

For copper developers with feasibility studies modelled at price decks well below current spot, these macro-driven volatility episodes do not alter project economics. Their construction timelines extend years beyond current Federal Reserve rate-decision windows, meaning short-term dollar strength is largely irrelevant to the investment case.

Long-Term Demand: Electrification Is Not Optional

The New Demand Architecture

The long-run copper demand picture is being fundamentally restructured by energy transition and digital infrastructure spending, two categories of demand that are less price-sensitive and less cyclically exposed than traditional construction-driven consumption. Consequently, the copper price drivers underpinning the next decade look materially different from those that shaped the previous cycle.

| End-Use Application | Copper Intensity | Demand Trajectory |

|---|---|---|

| Solar power installations | ~4,000-5,000 tonnes per GW | Accelerating with renewable targets |

| Offshore wind installations | ~8,000-10,000 tonnes per GW | Scaling rapidly through 2030s |

| Hyperscale AI data centres | Up to 4,000 tonnes per facility | Emerging high-growth demand vector |

| Electric vehicles | ~60-80 kg per vehicle | Growing with EV adoption curves |

| Grid expansion and transmission | Multi-decade infrastructure cycle | Policy-driven, less price-sensitive |

Strategic copper demand, defined as consumption from grid infrastructure, electric vehicles, renewable energy installations, and AI data centres, is projected to expand from approximately 32% of total global consumption in 2024 to 45% by 2040. This is not marginal growth layered on top of traditional demand; it is a structural reorientation of where copper goes and who buys it.

AI Data Centres as an Emerging Demand Category

Hyperscale data centres represent a genuinely new and underappreciated demand vector for copper that was not meaningfully present in market forecasting models as recently as five years ago. A single large-scale facility can require up to 4,000 tonnes of copper for power distribution infrastructure alone. As AI computing capacity scales aggressively through the late 2020s, the cumulative copper demand from data centre construction could add a meaningful increment to global consumption that existing long-term models have not fully absorbed.

This matters for the supply-demand balance analysis because data centre demand, unlike construction demand, is relatively insensitive to short-term commodity price movements. Technology companies building hyperscale infrastructure are not going to defer a US$2 billion facility because copper temporarily trades at US$13,500 rather than US$11,000 per tonne.

Capital Markets: Investors Are Pricing the Deficit, Not the Headline

Where Strategic Capital Is Actually Flowing

Despite spot price volatility in May 2026, capital markets activity during this period tells a quite different story about institutional and strategic investor positioning. Two examples illustrate the pattern clearly.

Marimaca Copper closed a major treasury and secondary offering on February 26, 2026, raising C$409 million gross, including C$129.2 million in net proceeds from the Canadian treasury component. The company's cash position net of working capital increased to US$147.7 million at March 31, 2026, up from US$62.7 million at year-end 2025, providing at least 12 months of operational funding. The Marimaca Oxide Deposit in Chile's Antofagasta region is targeting 50,000 tonnes per year of copper production within three years.

Critically, the project's definitive feasibility studies were modelled at US$4.30 per pound copper, a price deck that current spot levels have already materially exceeded, expanding projected returns across every economic metric in the study.

Abitibi Metals closed a C$30.75 million private placement on May 15, 2026, with Discovery Silver Corp. acquiring a 9.9% stake alongside participation rights in future financings. The B26 deposit in Quebec's Abitibi Belt hosts 25.3 million tonnes at 2.1% copper equivalent, containing 775 million pounds of copper alongside gold, zinc, and silver credits. The financing funds a 40,000-metre Phase 4 drill program through the first quarter of 2027, advancing resource expansion, infill conversion from inferred to indicated category under NI 43-101, and a Preliminary Economic Assessment.

The CEO of Abitibi Metals described the financing as injecting capital into a still-volatile market, providing the operational capacity to deliver more than 80,000 metres of total drilling and make significant progress toward a full feasibility study.

Canadian mining merger and acquisition activity surged 220% in 2025 to C$62.1 billion, with Eldorado Gold Corporation's approximately C$4 billion acquisition of Foran Mining Corporation establishing a specific valuation benchmark for scalable volcanogenic massive sulphide (VMS) systems in Tier-1 jurisdictions. This precedent is now being applied as a reference point for district-scale VMS assets at earlier development stages.

What Institutional Capital Requires Before Deploying

Across the financing activity visible in the current market cycle, several consistent criteria appear to be determining which copper development assets attract institutional and strategic capital versus which remain unfunded:

- Funded treasury: Cash runway extending at least 12 months without requiring near-term equity issuance into volatile markets

- Defined resource: NI 43-101 or JORC-compliant resource estimates with demonstrated infill conversion potential from inferred to indicated categories

- Jurisdictional quality: Tier-1 mining jurisdictions with established, predictable permitting frameworks

- Capital efficiency: Existing infrastructure that materially reduces restart or development capital intensity versus comparable greenfield builds

- Conservative price deck: Feasibility studies modelled at prices below current spot, providing embedded upside leverage without requiring speculative price assumptions

The next major ASX story will hit our subscribers first

Restart Assets: The Capital Efficiency Argument

Why Existing Infrastructure Changes the Investment Math

One of the more analytically compelling dynamics emerging from the current supply deficit environment is the repricing of restart assets, projects where prior production has left significant infrastructure in place. Selkirk Copper's work at Yukon's past-producing Minto Mine provides a concrete illustration of the capital efficiency argument.

The project has existing infrastructure valued at more than US$330 million, including roads, processing facilities, and power systems. This legacy infrastructure reduces estimated restart capital to approximately US$225 million, compared with US$800-900 million for a comparable greenfield development. The project is targeting 91% copper recovery, concentrate grades of 39-40%, and first production by mid-2028 at approximately 30,000 tonnes per annum copper equivalent. A new 117 Lens discovery returned 12.6 metres at 1.98% copper equivalent within a broader intercept of 86.8 metres at 0.58% copper equivalent from the Phase 2 drill program launched May 1, 2026.

The CEO of Selkirk Copper articulated the capital distinction clearly, noting that most major new mining operations require companies to build ports, roads, power lines, and power plants from scratch, none of which applies at a restart project with existing infrastructure already in place.

| Development Model | Estimated Capital Requirement | Timeline to Production | Key Risk Factor |

|---|---|---|---|

| Greenfield copper mine (comparable scale) | US$800-900 million | 10-17 years | Permitting, capital markets access |

| Infrastructure-backed restart | ~US$225 million | 2-4 years | Resource confirmation, metallurgy |

| Advanced development (permitted) | Variable | 3-5 years | Financing execution, construction |

In a market facing a 17-year average development lag on new greenfield supply, the ability to compress the timeline to production by a decade or more by utilising existing infrastructure is not a marginal advantage. It is potentially the single most important variable in determining which projects can actually deliver copper into the deficit window that opens in the late 2020s.

The Bull-Bear Framework: Getting the Timeframe Right

Short-Term Pressures vs. Long-Term Drivers

The analytical error most commonly made in copper market commentary is treating short-term and long-term forces as if they operate on the same timeframe. They do not, and conflating them produces investment decisions that are miscalibrated to the actual risk and return profile. However, understanding the distinction is central to developing sound copper investment strategies for the years ahead.

Near-term bearish pressures (0-12 months):

- China industrial output deceleration from 5.7% to 4.1% year-on-year in April 2026

- SHFE inventory build reversing a multi-week drawdown, reaching 97,011 tonnes

- Spot premiums flipping to discounts above US$13,500 per tonne

- US dollar index at a one-month high, suppressing non-US purchasing power

- Oil-driven inflation expectations delaying Federal Reserve rate-cut timelines

- Widening contango structure on forward curves signalling near-term physical availability

Long-term structural drivers (2-10+ years):

- 17-year average mine development timeline constraining all new supply responses

- Zero forecast production growth from Chile, the world's largest copper producer, from 2031 to 2040

- Only 0.9% global refined production growth in 2026, insufficient for electrification demand trajectories

- Projected 2026 refined copper deficit of between 150,000 and 450,000 tonnes across major forecasting institutions

- Strategic demand projected to rise from 32% to 45% of global consumption by 2040

- Governance and audit risk at major state-owned producers, including Codelco, reducing supply forecast reliability

| Timeframe | Dominant Force | Price Implication |

|---|---|---|

| 0-6 months | China demand weakness and macro headwinds | Downside pressure and consolidation |

| 6-18 months | Deficit materialisation and inventory normalisation | Price recovery toward incentive levels |

| 2030+ | Structural supply gap and electrification demand | Sustained repricing above US$12,000/t incentive floor |

The copper supply shortage and China demand weakness narrative presents as a contradiction only if both forces are assessed on the same timeline. They are not. Near-term demand softness does not build new mines. It simply delays the point at which the structural deficit becomes visible in inventory drawdowns and spot premiums.

Furthermore, the copper supply crunch that analysts have long warned about is now being validated by the very capital flows and M&A activity reshaping the sector in real time. Investors who conflate near-term softness with the long-term structural picture risk misreading one of the clearest supply signals in recent commodity market history. JP Morgan's copper outlook similarly underscores that structural deficits, rather than cyclical demand fluctuations, are the primary lens through which long-term copper pricing should be assessed.

Key Indicators to Watch

For market participants navigating this environment, five metrics carry the most signal value for determining whether near-term weakness is temporary or has the potential to extend into a more sustained demand contraction:

- SHFE on-warrant copper inventory levels – a sustained reversal below 88,000 tonnes would signal meaningful demand recovery from Chinese buyers

- Yangshan copper premium or discount spread – a return to premium territory signals re-engagement by Chinese physical buyers at prevailing price levels

- US dollar index trajectory – any material weakening reduces the effective cost burden for non-US copper purchasers

- Federal Reserve rate-cut timeline repricing – earlier-than-expected cuts would reduce real rates, weaken the dollar, and remove a key headwind

- China property investment data – stabilisation in property starts would restore the single largest copper-intensive demand sector in the global economy

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Forecasts, projections, and supply-demand estimates referenced throughout involve inherent uncertainty and may not reflect actual outcomes. Readers should conduct their own due diligence before making any investment decisions. Past performance and third-party projections are not guarantees of future results.

Want to Know When the Next Major Copper Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, instantly cutting through complex geological and market data to surface actionable opportunities — whether you're positioning for the structural copper deficit or tracking the next exploration breakthrough. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin your 14-day free trial to ensure you're never the last to know when a market-moving find is announced.