July 16, 2026

The Geological Clock Ticking Beneath Chile's Copper Heartland

Every major copper-producing district on Earth shares a common fate: as mines age, ore grades fall, extraction costs climb, and the gap between what a deposit once was and what it can still deliver widens irreversibly. This geological reality plays out across decades, and nowhere are its consequences more consequential for global metal markets than in Chile's Atacama region, where the world's largest copper producer is confronting a structural ceiling that no amount of capital spending has yet managed to break through.

Understanding why Codelco copper output flat in coming years has become the defining narrative for global copper supply requires looking beyond quarterly production numbers. The forces at work are geological, financial, operational, and now potentially institutional, converging to create one of the most complex supply-side constraints the copper market has faced in a generation.

When big ASX news breaks, our subscribers know first

Production Reality: What the Numbers Actually Show

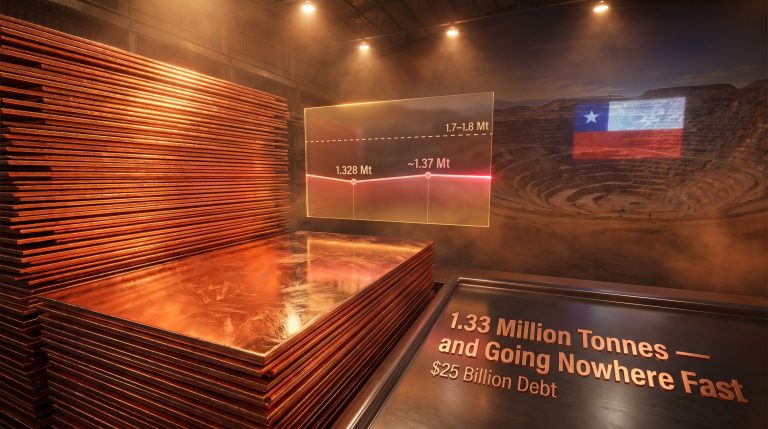

Codelco's output trajectory over the past several years tells a story of partial recovery masking deeper structural fragility. After falling to multi-decade lows during 2022 and 2023, the company managed a modest stabilisation, with 2024 production from its own mines reaching approximately 1.328 million metric tons. That figure represents less than a recovery and more of a floor.

The forward guidance delivered by Codelco's chairperson, Bernardo Fontaine, to a Chilean congressional committee in July 2026 made the near-term picture explicit. According to US News reporting on Fontaine's remarks, output will likely remain close to current levels for the foreseeable future, with the company's 2030 target of 1.7 million metric tons per year now appearing increasingly aspirational rather than operational.

| Period | Approximate Output | Status |

|---|---|---|

| Historical peak (pre-2020) | ~1.7-1.8 million t/yr | Historical high |

| 2022-2023 | ~1.31-1.32 million t | Two-decade low |

| 2024 | ~1.328 million t | Marginal stabilisation |

| 2025 (revised forecast) | 1.33-1.37 million t | Flat; revised down ~30,000 t |

| 2026 (projected) | ~1.344 million t | Flat (+0.7% vs 2025) |

| 2027 (target) | ~1.37 million t own mines / 1.5 million t total | Tentative recovery begins |

| 2030 (long-term target) | 1.7 million t | Increasingly at risk |

To appreciate the significance of this plateau, consider that Codelco alone accounts for roughly 10% of global copper supply. Furthermore, when the world's single largest copper producer cannot grow output, the ripple effects across commodity markets, downstream manufacturers, and energy transition supply chains are substantial. The Codelco production decline narrative has consequently become central to how analysts are modelling medium-term copper supply.

Three Structural Forces Creating the Output Ceiling

Ore Grade Deterioration: The Problem Capital Cannot Quickly Solve

The most fundamental challenge Codelco faces is one that cannot be addressed through operational efficiency improvements alone. Chile's copper porphyry deposits, which have underpinned the country's dominance in global copper supply for decades, are experiencing progressive ore grade decline as higher-grade near-surface material is exhausted and mining pushes deeper into lower-grade rock.

Ore grade is the concentration of copper within a given tonne of rock, typically expressed as a percentage. As grades fall, more material must be mined, moved, crushed, and processed to produce the same volume of refined copper. This creates a compounding cost and throughput problem: energy consumption rises, water usage increases, tailings volumes expand, and processing infrastructure becomes increasingly strained.

- Chilean copper ore grades have declined materially over the past two decades, from an average of roughly 1.0% copper in the early 2000s to estimates closer to 0.6–0.7% today across the country's major operations

- Lower grades increase the stripping ratio at open-pit mines, meaning more waste rock must be removed per tonne of ore processed

- Underground operations face equivalent challenges, where declining grades reduce the economic return per metre of development

- Codelco's structural expansion projects were designed specifically to access deeper, higher-grade sulphide material, but delays have deferred those grade benefits

This is not a problem unique to Codelco. It represents a systemic challenge across Chilean copper mining and, indeed, across virtually every mature copper-producing district globally. However, given Codelco's scale and its role as a foundational pillar of global copper supply, the grade decline effect carries outsized market implications. Chile's copper supply gap is, in large part, a direct consequence of this long-running grade deterioration trend.

The El Teniente Collapse: When Operational Risk Becomes Market Risk

El Teniente, located in the Andes mountains south of Santiago, is one of the largest underground copper mines on Earth by cumulative ore production. Its sheer scale means that any significant operational disruption is a market-relevant event, and in August 2025, that risk materialised with a deadly tunnel collapse that forced a downward revision of approximately 30,000 metric tons from the company's 2025 production forecast.

Beyond the immediate human tragedy, the collapse created a cascading set of operational consequences:

- Access to affected mining panels was suspended pending safety investigations and remediation

- Production sequencing across the mine was disrupted, affecting ore flow to processing facilities

- Recovery and rehabilitation timelines extended the output shortfall into 2026

- The incident added reputational and regulatory complexity to an already challenging operational environment

El Teniente is also the site of a major structural expansion programme, the New Mine Level project, which is designed to extend the mine's productive life by accessing a deeper ore block. That project has experienced both schedule delays and budget pressure, compounding the operational disruption from the collapse.

Project Delays and the Compounding Cost of Deferred Investment

Codelco's structural reinvestment programme represents one of the most ambitious capital programmes in the global mining industry, encompassing the El Teniente New Mine Level and the Chuquicamata Underground transition, among other major initiatives. These programmes were conceived to counteract the grade decline described above and restore Codelco's production capacity to levels approaching its historical peak.

The challenge is that multi-billion-dollar underground mine development projects of this complexity rarely execute on schedule or within original budget parameters. Fontaine's acknowledgement to the congressional committee that these structural projects encountered unexpected delays and costs is a frank admission that the investment thesis underlying Codelco's 2030 target has not played out as modelled.

Delays in large-scale underground mine development are not simply scheduling inconveniences. Each year of delay represents deferred production volume, additional carrying costs on capital already spent, and escalating total project expenditure. When multiple major projects experience simultaneous delays, the cumulative effect on production recovery timelines can be severe and difficult to reverse quickly.

The Chuquicamata Underground project involved transitioning the world's largest open-pit copper mine by volume to underground operations, a technically demanding undertaking with no true precedent at that scale. The engineering challenges inherent in such a transition were arguably underestimated in original project planning.

The Cochilco Audit: An Institutional Risk That Markets Are Watching

Layered on top of the operational and geological challenges is a data integrity question that has significant implications for how investors and market participants interpret Codelco's production trajectory.

Chile's national copper regulatory agency, Cochilco, announced plans to release a preliminary audit of Codelco's 2025 production data in September, following concerns that the company may have improperly included approximately 20,000 metric tons of copper in its annual production report. A separate internal review suggested the overstatement could be as large as 26,875 metric tons.

If the Cochilco audit confirms a material overstatement, the implications extend well beyond the specific tonnage figure:

- Actual 2025 production would fall to its lowest level since 1998, a figure significantly worse than Codelco's reported numbers suggest

- The credibility of the company's stated production recovery narrative would be materially undermined

- Institutional confidence in Chile's copper production data reporting framework could be damaged

- Codelco's ability to attract joint venture partners and secure financing for expansion projects could be affected by reputational consequences

The distinction between copper produced from a company's own operations and copper sourced through toll processing or third-party arrangements is an important accounting boundary in mining. Whether Codelco crossed that boundary in its 2025 reporting is precisely what the Cochilco audit is designed to determine.

El Abra: Strategic Option or Capital Dilemma?

Against this backdrop of constrained organic production growth, Codelco's leadership has pointed to the El Abra copper mine in Chile's Atacama Desert as a potential priority investment that could contribute meaningfully to the company's long-term output recovery.

El Abra is an open-pit porphyry copper operation that has historically produced through oxide heap leach methods. Its strategic significance lies in a large, largely untapped sulphide ore body beneath the existing oxide resource. Sulphide deposits typically offer higher recoveries through conventional flotation processing and represent longer-mine-life assets compared to oxide operations.

| Factor | Detail |

|---|---|

| Ownership | Codelco 49% / Freeport-McMoRan 51% |

| Proposed expansion capex | $7.5 billion (Freeport-McMoRan plan) |

| Ore type | Sulphide resource with significant untapped potential |

| Processing method | Conventional flotation for sulphide ore |

| Codelco's position | Minority partner requiring careful capital allocation |

| Key risk | High capital requirement relative to Codelco's financial capacity |

Fontaine described El Abra as potentially the best available option for Codelco to deploy whatever investment resources it can access, while emphasising that the $7.5-billion expansion must be evaluated with great care given the capital commitment involved.

For a state-owned enterprise already managing multi-billion-dollar project overruns and operating under Chilean government dividend expectations, committing to a further $7.5-billion joint venture expansion requires sequencing capital priorities with exceptional discipline. The El Abra decision is, consequently, as much a question of financial governance and balance sheet capacity as it is one of operational strategy.

What Flat Codelco Output Means for Global Copper Markets

Supply Constraints in a Demand-Growth Environment

The timing of Codelco's production plateau could not be more consequential from a global supply-demand perspective. Copper demand is forecast to grow substantially through 2030 and beyond, driven by:

- Electric vehicle manufacturing, where copper content per vehicle is roughly three to four times that of a conventional internal combustion engine vehicle

- Grid infrastructure expansion required to support renewable energy deployment and EV charging networks

- Heat pump installation programmes accelerating across Europe and North America

- Data centre construction, where copper wiring density is significantly higher than in traditional commercial buildings

Against this demand trajectory, the inability of the world's largest single copper producer to grow output removes a critical source of incremental supply. The broader copper supply crunch facing global markets is, in this context, materially worsened by Codelco's structural plateau. Furthermore, the Chile copper price outlook reflects these supply pressures directly, with analysts pointing to structural deficits as a key price support mechanism over the medium term.

Scenario Analysis: Three Possible Paths to 2030

Scenario 1: Base Case (Flat-to-Modest Recovery)

Output remains near 1.33–1.37 million tons through 2026. Structural projects contribute incrementally from 2027. The 2030 target is missed, with output reaching approximately 1.45–1.55 million tons. This scenario appears most consistent with current trajectory and execution patterns.

Scenario 2: Accelerated Recovery

El Teniente remediation completes ahead of schedule. El Abra expansion receives investment approval. Structural projects deliver on revised timelines. Output approaches 1.6–1.65 million tons by 2030, partially closing but not fully bridging the gap to the 1.7-million-ton target.

Scenario 3: Target Achievement

All structural projects execute without further material delay. El Abra contributes meaningful production by 2030. No further significant operational disruptions occur. The 1.7-million-ton target is achieved. Given the established pattern of delays and the pending Cochilco audit, this scenario carries the lowest probability.

The next major ASX story will hit our subscribers first

The Governance Dimension: State Ownership and Capital Tension

Codelco's challenges are not purely operational or geological. As a state-owned enterprise, the company operates under a dual mandate that creates inherent structural tension: generating revenue for the Chilean government through dividends while simultaneously funding the multi-billion-dollar reinvestment programmes its ageing mines require.

During periods of elevated copper prices, this tension is manageable. However, when prices soften or costs escalate, the competing demands on Codelco's cash flow become acute. Codelco's top producer status brings with it not only commercial prestige but also significant political scrutiny, as the congressional committee hearing at which Fontaine delivered his flat-output assessment clearly illustrates.

Governance reforms, capital structure decisions, and the eventual resolution of the Cochilco audit will collectively shape whether Codelco can close the gap between its current production reality and its 2030 ambitions. The operational and the institutional are, in this case, deeply intertwined. For further detail on Codelco's recent quarterly figures, the company's official corporate presentation provides a comprehensive breakdown of its first-half 2025 results.

Key Metrics at a Glance

| Metric | Current Status |

|---|---|

| 2024 actual output | ~1.328 million metric tons |

| 2025-2026 outlook | Flat; ~1.33-1.344 million tons |

| 2027 recovery target | ~1.37 million tons (own mines) |

| 2030 long-term target | 1.7 million tons (at increasing risk) |

| Primary constraint | Ore grade decline + project delays + El Teniente collapse |

| Key strategic option | El Abra expansion ($7.5B Freeport-McMoRan project) |

| Regulatory risk | Cochilco audit into 20,000-26,875t reporting discrepancy |

| Market implication | Structural supply constraint supports long-run copper price outlook |

Frequently Asked Questions

Why is Codelco copper output flat in coming years?

Codelco's production has stagnated due to a convergence of geological, operational, and financial pressures. Declining ore grades at ageing mines are reducing extraction efficiency, while major structural expansion projects have encountered significant delays and cost overruns. The El Teniente tunnel collapse in 2025 forced a downward revision of approximately 30,000 metric tons from the year's forecast, and a pending Cochilco audit may reveal that actual output was materially lower than reported.

What is Codelco's production target for 2030 and is it achievable?

Codelco has set a long-term target of 1.7 million metric tons per year by 2030. With current production near 1.33 million tons and structural projects continuing to experience execution challenges, most scenario analyses suggest the target will be missed, with output more likely to reach 1.45–1.55 million tons in a base case.

What is the Cochilco audit examining?

Chile's national copper agency, Cochilco, is conducting a preliminary audit of Codelco's 2025 production data following concerns that the company may have improperly included approximately 20,000 metric tons of copper in its production report. A separate internal review suggested the discrepancy could be as large as 26,875 metric tons, which would place actual 2025 output at its lowest level since 1998.

How does Codelco's output plateau affect copper prices?

As the producer of approximately 10% of global copper supply, Codelco's inability to grow output in a period of rising demand from electrification, EV manufacturing, and grid infrastructure investment reinforces the structural supply deficit narrative that underpins constructive long-term copper price forecasts. The Codelco copper output flat in coming years scenario is, in this sense, a meaningful tailwind for long-run copper valuations.

Disclaimer: This article is intended for informational purposes only and does not constitute financial or investment advice. Production forecasts, scenario analyses, and market projections involve inherent uncertainty and should not be relied upon as predictions of actual outcomes. Readers should conduct their own independent research before making investment decisions.

Want to Position Yourself Ahead of the Next Major Copper Discovery?

While Codelco's structural plateau reinforces the long-run copper supply deficit, Discovery Alert's proprietary Discovery IQ model scans the ASX daily to deliver real-time alerts on significant mineral discoveries — including copper — turning complex data into actionable insights before the broader market reacts. Explore how historic mineral discoveries have generated substantial returns and begin your 14-day free trial today to secure a genuine market-leading edge.