May 19, 2026

Codelco's remarkable journey to reclaim its position as the world's leading copper producer reflects broader industry trends affecting global mining operations. The Chilean state-owned mining giant has demonstrated resilience through strategic operational improvements and technological modernization, positioning itself for sustained market leadership. With automation transforming mining operations worldwide, Codelco's recovery exemplifies how established producers adapt to evolving market conditions while maintaining competitive advantages.

The copper mining sector faces unprecedented challenges from ore grade decline and operational complexity increases. Traditional extraction methods encounter diminishing returns as easily accessible, high-grade deposits become exhausted, forcing producers to implement sophisticated processing technologies and automated systems. This technological evolution represents both opportunity and challenge for established mining entities seeking to maintain competitive positioning in global commodity markets.

Strategic Market Position Analysis: Chile's Mining Dominance

Chile's position in global copper markets reflects decades of geological advantages combined with strategic infrastructure development. Codelco's projected recovery pathway to 1.7 million tonnes by 2030 represents more than production targets; it signals potential shifts in worldwide supply chain dynamics that could reshape industrial planning across multiple sectors.

The concentration of copper production among major players creates supply vulnerabilities that manufacturing sectors increasingly recognise. When combined operations between Chile's state-controlled assets and multinational mining corporations control approximately 25% of global copper output, supply disruptions from operational or geopolitical factors create cascading effects throughout industrial supply chains.

State Ownership Models Versus Private Sector Efficiency

Chile's state-controlled approach to copper mining enables long-term strategic planning horizons that differ fundamentally from quarterly earnings-focused private corporations. This governance structure supports sustained investment during commodity downturns and countercyclical capital deployment strategies that private shareholders might resist.

The operational flexibility inherent in state ownership manifests through sustained exploration budgets, infrastructure modernisation projects, and workforce development initiatives that maintain operational capacity during extended low-price periods. Codelco's ability to generate $5.5 billion in operating cash flow during 2024 demonstrates this strategic advantage, providing reinvestment capital without external financing constraints.

Private mining corporations face different optimisation pressures, balancing shareholder returns against operational investment requirements. This creates tactical advantages during commodity upturns but can limit strategic positioning for long-term market cycles.

Infrastructure Competitive Advantages in Global Markets

Chile's mining sector benefits from established port facilities, transportation networks, and processing infrastructure developed over decades of copper production. These sunk costs create competitive moats that new mining jurisdictions struggle to replicate economically.

The country's emerging renewable energy capacity in northern regions provides potential cost advantages through reduced electricity expenses, which represent significant operational cost components in energy-intensive processing operations. Solar and wind energy deployment specifically targets mining region electricity demand, creating geographic cost advantages.

Regional skilled workforce development represents another infrastructure advantage, with specialised mining expertise concentrated in established production areas. This human capital advantage reduces operational risks and training costs compared to greenfield developments in other jurisdictions.

When big ASX news breaks, our subscribers know first

Technological Modernisation and Production Recovery Strategies

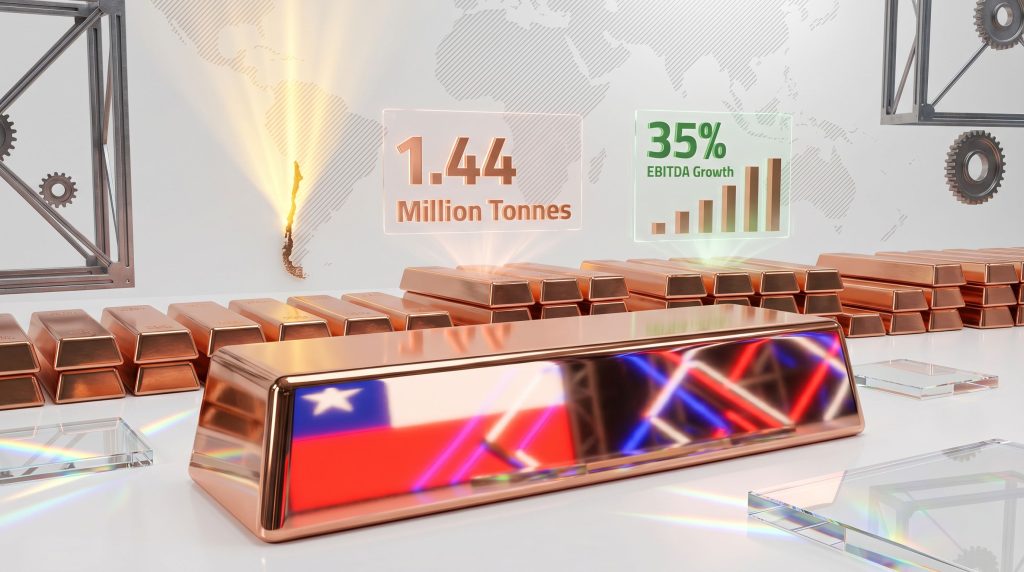

Codelco's production trajectory from 1.34 million tonnes in 2026 to 1.37 million tonnes from owned operations in 2027 reflects operational improvements rather than new asset development. This incremental growth demonstrates technological optimisation potential within existing mine infrastructure.

Advanced Geological Modelling and Resource Optimisation

Modern mining operations employ sophisticated geological modelling systems that continuously update resource estimates and optimise extraction sequences. These systems integrate real-time drilling data, grade analysis, and processing feedback to maximise copper recovery from increasingly complex ore bodies.

At operations like Chuquicamata and El Teniente, geological modelling improvements enable extraction planning adjustments that extend asset lifecycles beyond original engineering estimates. The implementation of automated drilling systems and real-time data analytics represents technological infrastructure investment that compounds operational benefits over extended periods.

Beneficiation process optimisation becomes critical as ore grades decline naturally at aging deposits. Advanced flotation technologies, grinding optimisation, and metallurgical process improvements enable economic copper extraction from ore bodies previously considered below economic cutoff grades.

Declining Ore Grade Challenges and Processing Solutions

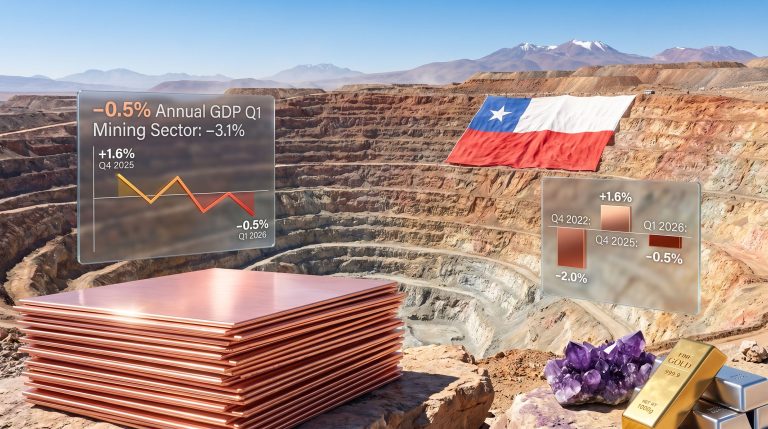

Q1 2026 production of 271,300 tonnes represented an 8% year-over-year decline, illustrating ongoing operational challenges despite technological improvements. This performance gap demonstrates the magnitude of geological headwinds that technology must overcome to maintain production levels.

Ore grade decline affects production economics through multiple mechanisms:

- Processing volume increases: Lower-grade ore requires processing larger tonnages to extract equivalent copper content

- Energy consumption scaling: Additional crushing, grinding, and flotation processes increase electricity requirements

- Reagent consumption expansion: Chemical processing inputs scale with ore volume rather than copper content

- Waste management complexity: Larger tailings volumes require expanded storage and environmental management

Cost optimisation strategies focus on process efficiency improvements that reduce per-tonne processing expenses. Automation technologies enable consistent processing parameters that maximise copper recovery while minimising reagent waste and energy consumption.

Operational Decentralisation and Management Efficiency

Codelco recover global copper leader through implementing management restructuring with emphasis on operational decentralisation, delegating execution authority to mine-level leadership. This organisational change addresses project delivery delays and cost overruns that historically constrained production recovery.

Decentralised decision-making reduces bureaucratic delays in operational adjustments, equipment procurement, and maintenance scheduling. Mine-level managers gain authority to implement process improvements without extensive corporate approval processes, accelerating operational optimisation cycles.

Project management improvements specifically target cost control and timeline adherence for major infrastructure developments. Previous cost overruns and structural project delays created production capacity constraints that operational restructuring aims to eliminate.

Global Copper Demand Dynamics Through 2030

Industrial electrification trends create structural copper demand growth independent of traditional economic cycles. Electric vehicle manufacturing requires approximately 183 pounds of copper per vehicle compared to 50 pounds in conventional automobiles, representing a 266% copper intensity increase per unit produced.

Furthermore, the copper supply forecast suggests significant challenges ahead as demand continues outpacing production capacity growth across major producing regions.

Energy Transition Infrastructure Requirements

Renewable energy deployment drives copper consumption through multiple infrastructure components:

- Transmission line expansion: Grid modernisation for renewable energy integration requires extensive copper wiring

- Substation construction: Electrical infrastructure expansion for distributed energy resources

- Inverter and control systems: Electronic components supporting renewable energy conversion

- Energy storage systems: Battery technologies and grid-scale storage facilities

Grid infrastructure expansion represents multiyear demand cycles that sustain copper consumption regardless of short-term economic fluctuations. These infrastructure projects exhibit extended planning and construction timelines that create predictable demand patterns.

Industrial electrification across manufacturing sectors continues driving baseline copper consumption growth. Motor replacements, power system upgrades, and control system modernisation create consistent demand from existing industrial facilities beyond new construction.

Strategic Reserve Policies and Market Dynamics

Global copper inventories at 15-year lows reflect supply-demand imbalances that strategic reserve policies could amplify. Major consuming nations increasingly consider copper stockpiling for economic security, similar to petroleum strategic reserves.

China's electric vehicle production exceeding 13 million units annually concentrates demand growth in specific geographic regions. This production concentration creates supply chain vulnerabilities that strategic stockpiling aims to address.

Government stockpiling decisions operate independently of commercial market signals, potentially creating additional demand pressure during periods when industrial consumption already strains supply capacity. These policy-driven purchases can amplify price volatility during supply constraints.

Competitive Positioning Analysis: Global Production Leaders

The global copper production landscape centres on three major entities competing for market leadership:

| Producer | 2027 Projected Output | Key Strategic Assets | Competitive Advantages |

|---|---|---|---|

| Codelco | 1.37 million tonnes (owned operations) | Chuquicamata, El Teniente, Andina | State ownership enables long-term planning |

| BHP | ~1.43 million tonnes | Escondida (world's largest individual mine), Olympic Dam | Diversified commodity portfolio, capital market access |

| Freeport-McMoRan | ~1.3 million tonnes | Grasberg (Indonesia), Americas portfolio | Geographic diversification, high-grade reserves |

Production Cost Architecture and Operational Efficiency

All-in sustaining costs (AISC) determine true competitive positioning beyond production volume metrics. These costs encompass:

- Energy expenses: Regional electricity pricing variations create substantial cost differences

- Labour productivity: Jurisdictional wage levels and operational efficiency variations

- Ore characteristics: Grade, metallurgy, and processing requirements affect unit economics

- Capital intensity: Infrastructure age and modernisation requirements

Middle East geopolitical tensions have increased Codelco's production costs by approximately 10 cents per pound, demonstrating vulnerability to global supply chain disruptions. These external cost pressures affect all producers but impact operations differently based on supply chain dependencies.

Energy cost advantages emerge from renewable energy adoption in mining regions. Chile's northern solar and wind resources create potential electricity cost reductions that improve long-term competitive positioning relative to operations dependent on conventional energy sources.

Reserve Life and Resource Replacement Strategies

According to Reuters, Escondida's planned ore grade decline according to its mine plan creates competitive opportunities for producers capable of maintaining or increasing output. As the world's largest individual copper mine experiences natural grade degradation, market share redistribution becomes possible.

Reserve replacement through exploration and acquisition determines long-term competitive sustainability. Producers must continuously identify and develop new ore bodies to offset depletion at existing operations.

Codelco's exploration investment during commodity downturns reflects state ownership advantages in maintaining reserve replacement activities. Private corporations often reduce exploration budgets during low-price periods, potentially constraining future production capacity.

Financial Performance Indicators and Capital Allocation

Codelco's 35% EBITDA growth in 2024 combined with $5.5 billion in cash generation demonstrates operational leverage to commodity price improvements. This financial performance provides capital for strategic investments without external financing requirements.

Cash Flow Generation and Reinvestment Capacity

The combination of elevated copper prices and operational efficiency improvements has generated substantial cash flow growth. This financial strength enables simultaneous debt reduction, exploration funding, and major capital project advancement.

Production levels exceeding 1.3 million tonnes create significant leverage to copper price movements. Each USD per pound price increase translates to substantial annual cash flow improvements, while price declines create proportional financial pressure.

State ownership structure enables countercyclical investment strategies that maintain capital deployment during market stress periods. This financial flexibility differentiates Codelco from competitors facing shareholder return pressures during commodity downturns.

Capital Project Economics and Return Analysis

Major capital projects require multiyear development timelines with substantial upfront investment before production benefits materialise. Codelco's strategic capital commitment to production recovery reflects confidence in long-term copper market fundamentals.

Return on invested capital (ROIC) evaluation becomes critical for project prioritisation across exploration, processing upgrades, and infrastructure modernisation initiatives. Capital allocation decisions weight production recovery potential against alternative investment opportunities.

Technology investments often exhibit delayed returns that compound over extended operational periods. Automated systems and processing optimisation generate cost savings and productivity improvements that justify initial capital requirements through cumulative benefits.

Regional Mining Sector Competitiveness and Strategic Advantages

Chile's mining competitiveness extends beyond individual company operations to encompass regulatory framework stability, infrastructure quality, and skilled workforce availability. These systemic advantages create sustained competitive positioning for Chilean copper producers.

Regulatory Environment and Operational Certainty

Political stability and regulatory predictability enable long-term investment planning with reduced policy risk. Mining companies require multidecade operational certainty to justify major capital investments in exploration and infrastructure development.

Environmental regulation compliance creates operational costs but also establishes consistent standards that enable planning and budgeting. Clear regulatory frameworks reduce uncertainty and legal risks that can disrupt operations in other jurisdictions.

Water management regulations in arid mining regions require technological solutions that become competitive advantages. Companies developing efficient water recycling and conservation technologies reduce operational risks and regulatory compliance costs.

Workforce Development and Technical Expertise

Specialised mining workforce concentration in established production regions creates human capital advantages that new mining jurisdictions struggle to replicate. Technical expertise in ore processing, equipment maintenance, and geological analysis represents accumulated knowledge that supports operational efficiency.

Training programmes and educational infrastructure specifically supporting mining sector needs ensure continued workforce quality. University mining engineering programmes and technical training facilities maintain the skilled labour supply essential for complex operations.

The next major ASX story will hit our subscribers first

Future Production Scenarios and Market Implications

Codelco's ambitious target of 1.7 million tonnes by 2030 requires sustained operational improvements and potential asset expansion. This growth trajectory faces multiple execution challenges that could affect achievement timelines.

However, effective mineral exploration strategies become increasingly critical as easily accessible deposits become depleted. Codelco recover global copper leader status will depend significantly on identifying and developing new copper resources.

Project Pipeline Analysis and Capacity Expansion

Production growth to 1.7 million tonnes requires identifying and developing additional copper resources beyond current operational capacity. This expansion could involve:

- Existing mine life extensions through deeper mining or resource expansion

- New mine development from exploration discoveries within Chilean territory

- Strategic acquisitions of producing assets or advanced development projects

- Joint venture partnerships providing access to external copper resources

Resource depletion rates at existing operations must be offset by new capacity additions to achieve net production growth. Geological surveys and resource estimation updates determine feasible production expansion pathways.

External Risk Factors and Production Vulnerabilities

Multiple external factors could disrupt production projections and affect target achievement:

Geopolitical risks affecting Chilean mining operations include regulatory changes, taxation policies, and international trade restrictions. Political stability remains crucial for sustained investment and operational certainty.

Climate change impacts on water availability pose operational challenges for mining operations in arid regions. Water scarcity could constraint processing capacity and require significant technological adaptation.

Technology disruption in extraction and processing methods could alter competitive positioning rapidly. Companies failing to adopt new technologies risk operational obsolescence and cost disadvantages.

Labour market dynamics including wage inflation and skill availability affect operational costs and productivity. Workforce development must keep pace with technological advancement and production expansion.

Investment Considerations and Strategic Positioning

Copper market dynamics through 2030 require careful evaluation of production growth sustainability, cost competitiveness, and external risk factors. Investors must assess multiple scenarios affecting long-term competitive positioning.

In addition, copper investment strategies should consider the broader implications of Codelco's recovery for global supply dynamics and pricing mechanisms.

Production Growth Evaluation Criteria

Investment analysis should examine several key factors:

- Capital efficiency: Production growth relative to capital investment requirements

- Timeline realism: Achievement probability for stated production targets

- Cost trajectory: All-in sustaining cost trends and competitive positioning

- Reserve quality: Ore grade sustainability and resource replacement rates

ESG compliance and social licence considerations increasingly affect operational sustainability. Environmental performance and community relations determine long-term operational viability in many jurisdictions.

Geographic risk assessment across different mining jurisdictions helps evaluate relative investment attractiveness. Political stability, regulatory consistency, and infrastructure quality vary significantly between regions.

Supply Chain Strategic Implications

Concentrated copper production among major producers creates supply chain vulnerabilities for downstream industries. Manufacturing sectors must evaluate sourcing strategies and potential alternative suppliers.

Downstream processing capacity and geographic distribution affect value chain positioning. Copper refining and manufacturing capabilities determine regional industrial competitiveness beyond primary production.

Strategic stockpiling policies among major consuming nations could amplify demand volatility and price movements. Industrial companies should monitor government reserve policies that could affect market dynamics.

Long-Term Market Evolution and Strategic Outlook

The global copper market faces fundamental restructuring driven by energy transition demand, supply constraints, and technological advancement. Production leadership among major producers remains contested as operational challenges and market dynamics evolve.

Consequently, sustainable mining transformation initiatives become increasingly important for maintaining operational licences and community acceptance across global mining operations.

Technology Investment and Competitive Sustainability

Continuous technology investment becomes essential for maintaining cost competitiveness as ore grades decline and extraction complexity increases. Companies failing to modernise processing capabilities risk operational obsolescence.

Automation and data analytics provide operational advantages that compound over time. Early technology adoption creates competitive moats through improved efficiency and reduced operating costs.

Sustainability initiatives increasingly determine operational licensing and social acceptance. Environmental performance affects regulatory approval timelines and community relations essential for long-term operations.

Market Structure Considerations

Demand growth sustainability across key end-use sectors depends on energy transition advancement and industrial electrification rates. Policy support for renewable energy and electric vehicle adoption directly affects copper consumption patterns.

New mine development faces extended permitting timelines and increased capital requirements. Project development cycles often exceed a decade from discovery to production, creating supply inflexibility relative to demand changes.

Recycling technologies and circular economy initiatives could affect primary copper demand over extended periods. Secondary copper supply from recycling reduces pressure on primary production but requires technological advancement and collection infrastructure development.

Investment Disclaimer: This analysis is for educational purposes only and does not constitute investment advice. Copper market dynamics involve significant risks including commodity price volatility, operational challenges, geopolitical factors, and regulatory changes. Past performance does not guarantee future results. Investors should conduct thorough due diligence and consider professional financial advice before making investment decisions.

Ready to Capitalise on the Next Major Copper Discovery?

Discovery Alert's proprietary Discovery IQ model provides instant notifications when significant ASX copper and mineral discoveries are announced, transforming complex geological data into actionable trading insights for both new and experienced investors. Begin your 14-day free trial today and position yourself ahead of the market with real-time alerts that have historically identified major discoveries like those from De Grey Mining and WA1 Resources.