July 16, 2026

When Geology Meets Geopolitics: The Real Story Behind Salar de Maricunga

Global lithium supply chains are not built on announcements alone. They are built on brine chemistry, aquifer hydrology, regulatory frameworks, and the patience of sovereign entities willing to play a decades-long development game. The Codelco delays lithium from Salar de Maricunga with Rio Tinto in Chile narrative that has circulated in industry media since mid-2026 tells only part of the story. The fuller picture involves a sophisticated public-private partnership architecture, a technically justified exploration extension, and a production timeline that was always designed for the long game rather than the fast trade.

Understanding what is actually happening at Maricunga requires separating legitimate timeline adjustments from market noise, and distinguishing between project-level progress and company-wide strategic recalibration.

When big ASX news breaks, our subscribers know first

Salar de Maricunga: The Resource Context That Makes This Partnership Strategically Significant

Salar de Maricunga sits at approximately 3,700 metres above sea level in Chile's Atacama Region III, making it one of the highest-altitude lithium-bearing salars under active development anywhere in the world. Its elevation and remoteness create both geological advantages and logistical challenges that fundamentally shape the project's development pathway.

Unlike Salar de Atacama, which has been commercially exploited by SQM and Albemarle for decades, Maricunga represents largely uncaptured lithium endowment. Its brine lithium concentrations are competitive with other Andean salars, though the specific hydrogeological characteristics of the Maricunga aquifer system differ meaningfully from Atacama's more thoroughly mapped subsurface geology.

This distinction matters enormously when designing extraction systems, which is precisely why additional hydrogeological characterisation has been prioritised before committing to full-scale capital deployment. Furthermore, understanding Chile lithium reserves helps contextualise why Maricunga occupies such a pivotal position in the country's long-term resource strategy.

Key Project Snapshot:

| Metric | Detail |

|---|---|

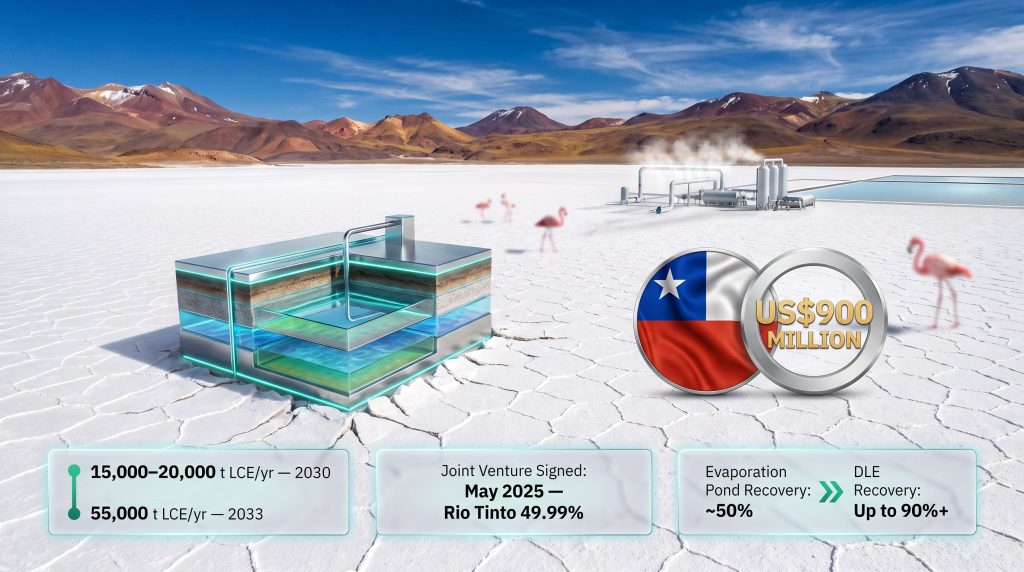

| Joint venture binding agreement | May 2025 |

| Rio Tinto equity stake | 49.99% |

| Total committed investment | Up to US$900 million |

| Phase I production target | 15,000 to 20,000 tonnes LCE/year by 2030 |

| Full-scale capacity target | 55,000 tonnes LCE/year by 2033 |

| CEOL exploration extension approved | February 2026 |

How the US$900 Million Investment Is Actually Structured

The financial architecture of the Codelco-Rio Tinto joint venture is a masterclass in staged risk allocation between a state-owned enterprise and a publicly listed private-sector major. Rather than front-loading capital into a project still requiring regulatory and technical maturation, both parties negotiated a three-tranche commitment structure that ties cash deployment directly to de-risking milestones.

The structure breaks down as follows:

- Tranche 1 – US$350 million: Payable at transaction closing, anticipated during Q1 2026, subject to regulatory clearance from Chilean and international authorities

- Tranche 2 – US$500 million: Contingent on the partners reaching a formal Final Investment Decision (FID), which will only occur once permitting, engineering, and commercial conditions are sufficiently advanced

- Performance incentive – US$50 million: A bonus payment triggered exclusively if first lithium production is achieved by the end of 2030, creating a tangible financial incentive for on-time execution

This staged model reflects a broader trend in large-scale mining project finance where sovereign partners retain resource control while private partners carry disproportionate early-stage capital risk. Rio Tinto's lithium strategy across multiple jurisdictions signals genuine commercial confidence in long-horizon lithium development, not merely aspirational project marketing.

What a 49.99% Stake Actually Means in Practice

Codelco's retention of a 50.01% majority is not an arbitrary rounding decision. Under Chile's constitutional framework and the National Lithium Strategy, state majority ownership over strategic mineral resources carries both legal and political significance. It ensures that lithium extraction decisions remain subject to sovereign oversight, that revenue flows partially to the Chilean state, and that technology transfer obligations remain enforceable under domestic law.

| Ownership Dimension | Codelco (50.01%) | Rio Tinto (49.99%) |

|---|---|---|

| Strategic control | State-retained | Private operational input |

| Capital commitment | Resource and licence holder | Up to US$900M cash |

| Technology contribution | Brine extraction knowledge | Proprietary DLE technology |

| Governance role | Majority decision authority | Near-parity operational influence |

This structure contrasts sharply with Bolivia's more centralised model under Yacimientos de Litio Bolivianos, where state control has historically been absolute but operational execution has lagged significantly. Chile's hybrid approach, as outlined in the country's Chile lithium strategy, attempts to capture the commercial efficiency of a private-sector partner while preserving national resource sovereignty.

The CEOL Modification: What the Technical Reality Actually Shows

The term that has generated the most market confusion is the CEOL modification approved in February 2026. A CEOL, or Concesión de Explotación de Obras de Litio, is a Chilean regulatory instrument governing the rights to extract and process lithium from specific salar resources. It is distinct from a standard mining concession and carries specific obligations around environmental management, water use, and production reporting.

The February 2026 CEOL modification extended Maricunga's exploration characterisation phase by four additional years. This is not a production delay in any conventional sense. It is a regulatory optimisation that allows the joint venture to improve the resolution of its hydrogeological models before committing to the irreversible physical infrastructure of a full-scale extraction operation.

Why does this matter technically? Brine aquifer systems in high-altitude salars behave differently from lowland water tables. Extraction rates that exceed natural brine recharge can create subsidence, reduce long-term yield, and trigger regulatory intervention after production has commenced. Getting the subsurface modelling right before construction protects both the project's long-term economics and its environmental licence to operate.

Codelco's leadership has publicly confirmed that both partners remain aligned on the project timeline and strategic intent, with first production still targeted for end of 2030 under the base-case development schedule.

Phase I vs Phase II: Two Different Technologies, Two Different Production Realities

One of the most technically underappreciated aspects of the Maricunga development plan is that Phase I and Phase II are not simply scaled-up versions of the same process. They represent fundamentally different technological approaches to lithium extraction.

Phase I (targeting end of 2030) will rely on conventional lithium brine extraction combined with evaporation pond processing, targeting an initial output range of 15,000 to 20,000 tonnes LCE per year. This method is proven, bankable, and understood by engineering, procurement, and construction contractors with Latin American salar experience.

Phase II (targeting 2033) will integrate Rio Tinto's proprietary direct lithium extraction technology to scale total output to 55,000 tonnes LCE per year. DLE is a selective adsorption or ion-exchange process that pulls lithium directly from brine without requiring the 12 to 18-month evaporation cycle that conventional ponds demand.

| Production Method | Evaporation Ponds (Phase I) | DLE Technology (Phase II) |

|---|---|---|

| Recovery rate | ~50% | Up to 90%+ |

| Water consumption | High | Significantly lower |

| Land footprint | Large | Compact |

| Processing time | 12 to 18 months | Days to weeks |

| Output scalability | Limited | High |

| Environmental risk profile | Elevated in water-stressed salars | Substantially reduced |

The environmental sensitivity of Maricunga makes DLE's water efficiency particularly important. High-altitude salars in northern Chile support fragile flamingo breeding habitats and are subject to indigenous community consultation requirements under both Chilean environmental law and international frameworks. The transition to DLE in Phase II directly addresses these concerns by dramatically reducing the brine volume that must be extracted and processed per tonne of lithium carbonate produced.

Three Scenarios for Maricunga Through 2033: A Risk Framework

Any rigorous assessment of the Maricunga project requires acknowledging that multiple development pathways remain plausible. The following scenario framework is presented for analytical context and does not constitute financial advice or a production forecast.

Scenario A: Base Case – On-Schedule Delivery

Transaction closes Q1 2026, environmental permits secured by 2028 to 2029, construction commences 2029, Phase I first production achieved by end of 2030, Phase II DLE commissioned by 2033.

Key dependency: Regulatory continuity, stable lithium prices above the economic threshold for FID, and maintained partner alignment.

Scenario B: Moderate Delay of 12 to 24 Months

Environmental permitting complexity at the high-altitude salar, including indigenous consultation timelines and water rights adjudication, introduces construction lags. Phase I first production shifts to 2031 to 2032, Phase II delayed to 2034 to 2035.

Key dependency: The pace of Chile's environmental impact assessment process for large-scale salar operations.

Scenario C: Strategic Restructure

Sustained lithium carbonate prices below US$10,000 per tonne reduce Rio Tinto's commercial incentive to commit the US$500 million FID tranche. Project scope is renegotiated or alternative financing partners are sought by Codelco.

Key dependency: Global EV demand trajectory and Chinese lithium oversupply conditions persisting beyond 2027.

| Scenario | First Production | Full Capacity | Primary Risk |

|---|---|---|---|

| A – Base Case | End of 2030 | 2033 | Regulatory continuity |

| B – Moderate Delay | 2031 to 2032 | 2034 to 2035 | Permitting complexity |

| C – Strategic Restructure | Uncertain | Uncertain | Lithium price and FID commitment |

Disclaimer: The scenarios above are analytical projections based on publicly available information and are not investment advice. Actual project outcomes may differ materially from any scenario described.

The next major ASX story will hit our subscribers first

Chile's Broader Strategic Position and What Maricunga Changes

Chile currently holds approximately 35 to 37% of global identified lithium reserves, according to the US Geological Survey's most recent mineral commodity summaries. The Atacama basin, operated primarily by SQM and Albemarle under long-term concession agreements, currently dominates Chilean lithium output. Maricunga's development introduces a structurally distinct third production centre, one operated under a different ownership model, different technology pathway, and different regulatory instrument.

If Maricunga reaches its full-scale 55,000 tonnes LCE per year capacity, it would represent a meaningful increment to Chile's national lithium output at a time when global demand forecasts continue to project compound annual growth rates of 20% or higher through the early 2030s. According to Benchmark Minerals, Rio Tinto could become the second-largest lithium miner globally by 2035, underscoring just how consequential the Maricunga partnership is to the company's long-term supply positioning.

The product mix decisions at Maricunga, specifically whether output will be sold as battery-grade lithium carbonate, lithium hydroxide, or further upgraded for downstream battery precursor chemistries, will determine how the project integrates into existing supply chains serving Asian, European, and North American battery manufacturers.

For battery supply chain planners seeking non-Chinese lithium sourcing, Chile's investment-grade sovereign environment and the Codelco-Rio Tinto partnership's institutional credibility offer a degree of supply security that newer, less-established lithium jurisdictions cannot yet match.

Frequently Asked Questions

When is first lithium production expected from Salar de Maricunga?

First production is targeted for the end of 2030, contingent on environmental permitting and construction progress across the 2027 to 2030 development window.

Does Codelco delays lithium from Salar de Maricunga with Rio Tinto in Chile mean the project has been cancelled or significantly scaled back?

No. The CEOL exploration extension and updated timeline adjustments reflect proactive technical and regulatory management, not a fundamental change to the project's scope or strategic rationale.

What is the maximum annual production capacity at Salar de Maricunga?

The project targets 55,000 tonnes of lithium carbonate equivalent per year at full Phase II capacity, expected by 2033 under the base-case schedule.

Why is DLE technology critical to Maricunga's Phase II?

DLE enables significantly higher lithium recovery rates of up to 90% or more compared to evaporation pond recoveries of around 50%, while consuming substantially less water. In a sensitive high-altitude ecosystem with flamingo habitat and indigenous community interests, this distinction is both commercially and environmentally material.

Who controls the joint venture?

Codelco holds a 50.01% majority stake, preserving Chilean state control. Rio Tinto holds 49.99% and contributes staged capital of up to US$900 million alongside its proprietary DLE technology platform.

Key Takeaways for Supply Chain Watchers and Industry Analysts

The Maricunga project's strategic significance extends well beyond its nameplate production capacity. Five dimensions define its importance:

- Ownership architecture: The 50.01% state retention model may become a template for future Chilean lithium development under the National Lithium Strategy framework

- Technology sequencing: The Phase I conventional to Phase II DLE transition de-risks capital deployment while building toward a higher-efficiency, lower-impact long-term operation

- Regulatory management: The CEOL modification reflects sophisticated pre-construction risk management rather than project failure

- Timeline realism: The 2030 to 2033 production window was always a long-horizon target, and modest adjustments within that range do not alter the project's fundamental investment thesis

- Global supply chain positioning: Chile's combination of resource scale, institutional stability, and now DLE-enabled production efficiency makes Maricunga a meaningful piece of the non-Chinese lithium supply mosaic that battery manufacturers are actively seeking to build

The story of Codelco delaying lithium from Salar de Maricunga with Rio Tinto in Chile is, on closer examination, a story of deliberate, technically-grounded project stewardship — not a cautionary tale of strategic failure.

Want to Track the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, transforming complex commodity data into actionable investment insights across lithium and more than 30 other resources — explore historic discoveries and their returns to understand the scale of opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.