August 5, 2026

Understanding Colombia's Energy Import Crisis

Global energy markets face unprecedented uncertainty as traditional supply-demand relationships undergo fundamental transformation. The intersection of geopolitical tensions, domestic policy shifts, and structural capacity constraints creates complex economic vulnerabilities that extend far beyond individual nations. These macro-economic forces particularly impact countries experiencing simultaneous production decline and import dependency growth, creating cascading effects throughout national economies. The Colombia energy crisis exemplifies these broader global dynamics where resource-abundant nations find themselves increasingly exposed to international price volatility.

Furthermore, Latin America's energy landscape reflects decades of infrastructure development decisions, regulatory policies, and fiscal strategies that now require urgent reassessment as external market conditions evolve rapidly. The regional energy security framework demonstrates how interconnected global markets can amplify local vulnerabilities.

When big ASX news breaks, our subscribers know first

How Fiscal Dependencies Create Economic Vulnerabilities

Colombia's economic structure demonstrates the inherent risks of concentrated revenue dependency on volatile commodity sectors. The hydrocarbon industry's contribution to national finances extends beyond direct export earnings, encompassing complex multiplier effects throughout the broader economy.

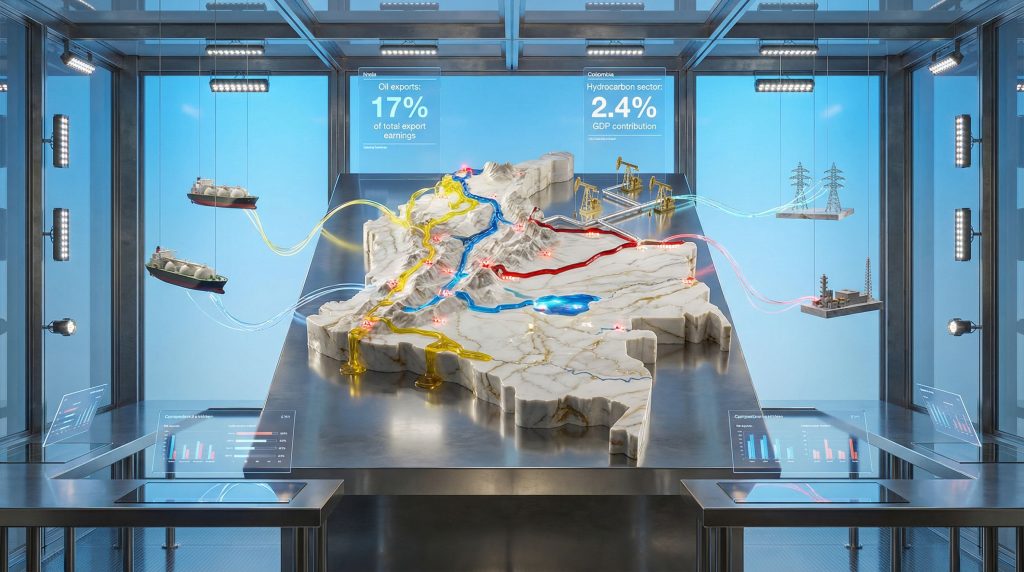

Current Economic Exposure Metrics:

- Oil export revenues constitute approximately 17% of total export earnings as of 2025

- The hydrocarbon sector contributes 2.4% directly to national GDP

- Government fiscal revenues remain heavily concentrated in petroleum-related taxation

- Historical production baselines of over 1 million barrels per day previously supported fiscal stability

The February 2026 production figures reveal concerning trends: daily output averaged 734,924 barrels, representing a 1.5% monthly decline and 2.7% year-over-year reduction. This output level marks the lowest monthly production since July 2021 and reflects a 23% decrease compared to production levels from a decade prior.

Economic Multiplier Effects Beyond Headline Numbers

The petroleum sector's relatively modest GDP contribution masks disproportionate economic impacts across multiple dimensions. Consequently, the Colombia energy crisis creates ripple effects that extend far beyond immediate energy markets.

Direct Fiscal Impact Areas:

- Government tax revenue concentration in energy taxation mechanisms

- Foreign exchange earnings critical for import financing capacity

- Regional employment concentrated in specific geographic zones

- Infrastructure investment dependencies in petroleum-producing regions

Indirect Economic Transmission Channels:

- Industrial competitiveness through energy cost pass-through effects

- Currency stability influenced by hydrocarbon export performance

- Credit market conditions affected by sovereign fiscal strength perceptions

- Investment climate assessments incorporating regulatory risk factors

The economic recovery trajectory following the COVID-19 pandemic remains structurally incomplete, creating additional fiscal pressure during this production decline period. Government budget baselines reflect weakened economic fundamentals that amplify the impact of reduced petroleum revenues.

Natural Gas Import Dependency Transformation

Colombia's energy security profile has undergone dramatic transformation as domestic natural gas production capacity fails to meet consumption requirements. The import substitution reversal represents one of the most rapid energy dependency shifts documented in recent Latin American energy history.

Production Decline Analysis:

Table: Colombia Natural Gas Production Trends

| Period | Daily Production (MMcf/d) | Year-over-Year Change | Import Dependency |

|---|---|---|---|

| 2016 (approx.) | 1,070 | Baseline | 0% |

| February 2025 | 828 | -23% vs 2016 | <4% |

| February 2026 | 695 | -16% vs 2025 | ~20% |

The February 2026 natural gas production averaged 695 million cubic feet per day, showing a 2% monthly increase but a 16% year-over-year decline. Most significantly, current production represents a 35% reduction compared to decade-prior baselines when Colombia maintained energy self-sufficiency.

Import Cost Structure and Economic Impact

The transition from energy self-sufficiency to import dependency creates multiple economic pressure points. Additionally, considering the broader US natural gas forecast, Colombia faces exposure to North American market volatility.

Current Account Balance Effects:

- Increased merchandise import costs affecting trade equilibrium

- Foreign exchange demand pressure from energy import payments

- Currency volatility exposure through international price transmission

- Strategic reserve inadequacy amplifying supply shock vulnerabilities

Price Transmission Mechanisms:

Colombia's growing reliance on liquefied petroleum gas (LPG) imports exposes the economy to global spot market pricing volatility. Industry analysis indicates that natural gas serves as a transitional energy source during renewable energy development, but this transition function becomes compromised when domestic production collapses.

The rapid scaling of costly LPG imports creates multiple economic vulnerabilities: higher landed energy costs, increased currency exposure, supply chain dependency on international shipping networks, and direct transmission of global energy price volatility to domestic markets.

Global Energy Disruption Spillover Analysis

The Strait of Hormuz closure represents the largest global oil market disruption in recorded history, according to International Energy Agency assessments. This event demonstrates how regional conflicts create worldwide economic impacts that particularly affect import-dependent economies.

Disruption Scale Quantification:

Table: Hormuz Closure Global Impact Assessment

| Impact Category | Magnitude | Duration | Economic Effect |

|---|---|---|---|

| Global Oil Supply Blocked | 20% | Multiple weeks | Price spike to $144/barrel |

| Qatar LNG Capacity Loss | 17% of Qatar's output | Up to 5 years | 3.4% of global LNG capacity |

| Natural Gas Price Peak | $3.20/million BTU | Supply shock period | Regional price increases |

Qatar's position as approximately 20% of global LNG production means the 17% capacity damage effectively removes 3.4% of worldwide LNG capacity from international markets for extended periods. This capacity loss creates persistent upward pressure on natural gas prices globally.

Market Price Response Dynamics

Energy price volatility during the disruption period exceeded historical precedents. However, the OPEC production impact on global markets demonstrates how coordinated responses can influence price stability.

- Brent crude oil peaked above $144 per barrel during active closure

- Natural gas prices surged beyond $3.20 per million BTU

- Two-week ceasefire announcement triggered significant price reductions

- Residual risk premiums maintained elevated pricing despite ceasefire measures

Financial institution analysis projected continued market pressure scenarios. Investment bank forecasts suggested oil prices could reach $120 per barrel if disruptions extended into July, while other projections indicated sustained $100+ Brent pricing throughout 2026 under prolonged closure scenarios.

Colombia Energy Crisis Amplification

The global supply disruption particularly impacts Colombia through several transmission channels. Moreover, the oil price rally 2025 created additional cost pressures for import-dependent economies.

Vulnerability Factors:

- Limited strategic petroleum reserve capacity

- Constrained LNG import infrastructure creating supply bottlenecks

- Energy import concentration in spot market purchases (highest price exposure)

- Domestic production decline coinciding with global supply shocks

Industry association analysis indicates Colombian energy import costs increased 20-25% during global supply disruptions, demonstrating direct economic transmission of international energy market volatility.

Policy Framework Economic Trade-offs

President Gustavo Petro's administration, as Colombia's first leftist government, has implemented comprehensive energy policy reforms designed to reduce hydrocarbon dependency. These policy choices create immediate economic tensions during transition periods when renewable capacity development has not yet offset declining fossil fuel production.

"President Petro is Killing Colombia's Oil Industry", according to industry analysts, who cite adverse regulatory changes as a primary driver of production decline.

Fiscal Position Deterioration:

Table: Colombia Budget Deficit Trends

| Year | Budget Deficit (% GDP) | Economic Context | Policy Drivers |

|---|---|---|---|

| 2020 | 8.0% (approx.) | COVID-19 pandemic impact | Emergency spending |

| 2025 | 7.5% | Second highest on record | Production decline + spending |

| 2026 (projected) | 8.1% | Predicted all-time high | Policy transition costs |

The 2025 budget deficit of 7.5% of GDP represents the second-highest deficit in Colombia's modern economic history, exceeded only during the 2020 pandemic crisis. Economic forecasts project the 2026 deficit will reach 8.1% of GDP, establishing a new historical record during a critical election year period.

Regulatory Impact on Production Capacity

Current administration policies reflect deliberate prioritisation of environmental objectives over immediate energy security considerations. The regulatory framework includes adverse industry reforms and frequent taxation increases that directly impact production economics.

Policy Trade-off Analysis Framework:

- Environmental sustainability versus immediate energy security

- Long-term renewable transition versus short-term fiscal stability

- Climate commitment compliance versus economic growth maintenance

- Energy independence goals versus production capacity preservation

The confluence of declining production revenues and increased government spending creates compounding fiscal pressure. International energy experts suggest the administration's fiscal position reflects both structural revenue decline and discretionary spending increases that exceed available resources.

Regional Energy Security Comparative Analysis

Colombia's energy challenges reflect broader Latin American patterns while demonstrating unique vulnerability characteristics. Regional comparison provides context for understanding the severity of the Colombia energy crisis. Furthermore, the Saudi exploration impact on global supply chains affects regional energy security calculations.

Table: Latin American Energy Security Assessment

| Country | Energy Self-Sufficiency | Import Risk Level | Fiscal Vulnerability | Strategic Response |

|---|---|---|---|---|

| Colombia | Rapidly declining | High and increasing | Very high | Import scaling |

| Ecuador | Relatively stable | Low to medium | Medium | Production maintenance |

| Peru | Mixed profile | Medium | Medium | Diversification |

| Chile | Import-dependent | High | Low | Regional integration |

Colombia's energy security deterioration appears more rapid and comprehensive compared to regional peers. The simultaneous occurrence of production decline, import dependency growth, and fiscal pressure creates a unique vulnerability profile within Latin America.

Regional Integration Opportunities

Cross-border energy cooperation mechanisms could provide partial mitigation of Colombia's energy security challenges. In addition, trade war oil impacts create additional incentives for regional cooperation mechanisms.

Potential Regional Solutions:

- Shared LNG terminal infrastructure to reduce import costs

- Cross-border pipeline development for supply diversification

- Coordinated strategic reserve policies among regional partners

- Joint renewable energy development initiatives

Regional energy market integration remains underdeveloped compared to other global regions, limiting Colombia's ability to leverage geographic diversification for energy security enhancement.

The next major ASX story will hit our subscribers first

Economic Sectoral Impact Distribution

Colombia's energy cost increases affect economic sectors disproportionately based on energy intensity and cost sensitivity profiles. The manufacturing and agricultural sectors face particularly acute challenges from natural gas price increases.

Table: Sectoral Energy Exposure Analysis

| Economic Sector | Energy Intensity | Price Sensitivity | GDP Contribution | Export Share |

|---|---|---|---|---|

| Manufacturing | Very high | Critical | 11% | 22% |

| Agriculture | High | Significant | 6% | 30% |

| Mining | High | Moderate | 2% | Variable |

| Services | Low | Limited | 65% | Limited |

Industry association projections indicate natural gas prices will increase 20-25% in major economic regions, particularly affecting Antioquia department where Medellín, Colombia's second-largest city, operates significant industrial capacity.

Agricultural Sector Vulnerability

The agricultural sector's dual exposure to energy costs and export market competition creates particular vulnerability during price shock periods:

Agricultural Impact Channels:

- Direct energy costs for irrigation and processing operations

- Transportation cost increases affecting distribution networks

- Fertiliser price impacts from natural gas feedstock costs

- Export competitiveness erosion from increased production costs

Government data indicates agriculture generates 30% of export earnings while contributing 6% to national GDP, highlighting the sector's disproportionate economic importance during foreign exchange constraint periods.

Investment Climate and Capital Allocation Impacts

Colombia's energy policy transition creates complex investment climate challenges as foreign capital reassesses long-term project viability under evolving regulatory frameworks. Traditional energy sector investments face policy uncertainty while renewable energy development requires substantial infrastructure capital.

Foreign Investment Considerations:

- Regulatory stability concerns affecting long-term project planning

- Taxation policy unpredictability impacting investment returns

- Infrastructure requirements for renewable energy transition

- Technology transfer opportunities in clean energy sectors

Energy sector capital allocation decisions increasingly reflect policy risk assessments alongside traditional geological and market factors. International energy companies evaluate Colombian projects within broader regional portfolios that include more stable regulatory environments.

Clean Energy Investment Potential

The energy crisis accelerates opportunities in renewable energy infrastructure development:

Renewable Energy Investment Sectors:

- Solar photovoltaic systems in high-irradiation geographic regions

- Wind power development in coastal areas with favourable conditions

- Small-scale hydroelectric projects for distributed generation

- Energy storage system deployment to manage renewable intermittency

Economic multiplier effects from clean energy investments include job creation in manufacturing and installation, technology transfer with knowledge spillovers, export potential for renewable energy equipment, and industrial energy cost reduction for end users.

Strategic Economic Response Framework

Colombia's energy security challenges require coordinated policy responses that balance immediate crisis management with long-term structural transformation objectives. The economic response framework must address fiscal stability, energy security, and sustainable development simultaneously.

Short-term Stabilisation Measures:

- Strategic petroleum and natural gas reserve establishment

- Emergency import financing mechanisms to manage foreign exchange pressure

- Price stabilisation funds to buffer consumer impact

- Regional energy cooperation agreements for supply diversification

Medium-term Structural Adjustments:

- Revenue diversification strategies to reduce hydrocarbon fiscal dependency

- Energy subsidy reform programmes to improve economic efficiency

- Carbon pricing mechanism development to fund transition investments

- Alternative energy infrastructure acceleration through targeted incentives

Fiscal Framework Adaptation Requirements

Government fiscal policy needs fundamental adjustment to manage energy transition costs while maintaining economic stability:

Fiscal Policy Reform Areas:

- Tax base diversification beyond petroleum-dependent revenues

- Energy subsidy restructuring to reduce fiscal burden while protecting vulnerable populations

- Carbon taxation implementation with revenue recycling toward renewable infrastructure

- Public investment reallocation toward energy security and transition projects

The timing of fiscal reforms becomes critical as Colombia approaches the 2026 election cycle. Political economy constraints may limit policy flexibility during transition periods when economic adjustment costs are highest.

Colombia Energy Crisis Long-term Implications

Colombia's energy transformation represents both significant economic challenge and potential development opportunity. The convergence of declining domestic production, increased import dependency, and global market volatility creates immediate vulnerabilities requiring coordinated policy responses.

The macro-economic implications extend throughout the national economy, affecting fiscal stability, trade balance dynamics, industrial competitiveness, and currency stability. Success in managing this transition depends critically on balancing immediate energy security requirements with long-term sustainability objectives while maintaining economic growth trajectories and fiscal discipline.

Colombia's experience provides broader lessons for resource-dependent economies navigating energy transitions during periods of global market instability. The outcome will significantly influence regional energy security frameworks and Latin American approaches to sustainable development challenges.

Future Research Considerations:

Energy sector analysts and economic researchers continue developing frameworks for understanding energy transition economics in developing economies. Regional energy integration mechanisms and renewable energy deployment strategies remain active areas of academic and policy research with practical applications for energy security enhancement.

Ready to Capitalise on Critical Energy Transition Opportunities?

Colombia's energy crisis demonstrates how rapidly shifting global dynamics create both challenges and investment opportunities across resource-dependent economies. Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, helping investors identify actionable opportunities in energy transition commodities and traditional resources as markets respond to evolving supply-demand fundamentals. Explore historic examples of major mineral discoveries that generated substantial returns during periods of market uncertainty, and begin your 14-day free trial today to secure a market-leading advantage in navigating these complex global energy dynamics.