May 20, 2026

Why the Commodity Cycle Is Deeper Than Most Investors Realise

Commodity markets move in long, slow arcs that most investors only recognise in hindsight. The conditions that produce the most powerful bull markets, including the Jordan Roo commodities bull market and nickel sulfide deposits thesis, rarely announce themselves clearly. Instead, they build quietly beneath the surface, driven by the convergence of demographic shifts, technological disruption, and geopolitical realignment. Understanding why certain commodities are poised for structural re-rating requires a framework that goes well beyond headline price movements.

The current commodity cycle is unusual in its breadth. It is not a single-factor trade. It is the simultaneous operation of at least three distinct structural forces, each of which would be sufficient to sustain a multi-year commodity cycle on its own. Together, they represent one of the more compelling macro setups in recent decades.

When big ASX news breaks, our subscribers know first

The Three Structural Pillars of the Current Commodities Bull Market

Pillar One: The Poverty Transition and Its Commodity Intensity

Over one billion people globally are currently transitioning from extreme poverty to low-income status. This demographic shift is profoundly commodity-intensive in a way that high-income consumption patterns simply are not. At low income levels, every incremental dollar of purchasing power gets channelled into physical goods — a bicycle, a motorcycle, and eventually a small car.

This dynamic is visible across emerging markets in Latin America, Southeast Asia, and Sub-Saharan Africa. When a young professional in a developing economy secures their first stable job, their single highest-impact lifestyle improvement is often the purchase of a small automobile. That vehicle requires enormous quantities of steel, aluminium, rubber, copper wiring, and energy to manufacture and operate. A private car consumes dramatically more energy per passenger kilometre than a shared bus, compounding the resource intensity of this transition at a civilisational scale.

Unlike wealthy-economy consumption, which is increasingly weighted toward services, software, and experiences, this demographic wave creates direct, durable demand for physical commodities. Furthermore, the scale of critical minerals demand underpinning this transition is only beginning to be understood by mainstream investors.

Pillar Two: AI Infrastructure and the Physical Demands of the Digital Economy

The artificial intelligence infrastructure build-out is rapidly emerging as a secondary commodity catalyst of significant scale. Data centre construction, semiconductor fabrication facilities, and power grid expansion to support AI workloads all require large quantities of copper, aluminium, steel, and critical minerals. AI-driven energy demand is expected to add substantial new load to power grids globally, reinforcing demand for both conventional energy sources and the critical minerals required for electrification infrastructure.

Importantly, this is a complementary driver to the poverty-transition thesis, not a replacement for it. These forces operate in parallel across different commodity types and geographies.

Pillar Three: Electrification and the Resource Sovereignty Imperative

The electrification of transport and industrial processes creates sustained long-run demand for lithium, cobalt, nickel, and copper. Compounding this demand signal is the accelerating policy imperative among major economies to reshore critical mineral supply chains. Following the supply disruptions exposed between 2020 and 2022, "resource sovereignty" has become a formal industrial policy objective across the United States, the European Union, and Australia. This reshoring drive is reshaping capital allocation in the mining sector.

The current commodities bull market is not driven by a single catalyst. It is the convergence of demographic, technological, and geopolitical forces operating simultaneously — a structural setup that historically produces multi-year commodity cycles.

How to Identify a Commodity That Is Genuinely "Cheap"

Within any broad commodity bull market, selectivity matters enormously. Not every commodity benefits equally from every structural trend. Identifying which commodities are genuinely cheap, and therefore positioned for the most powerful price recovery, requires a combination of technical and fundamental analysis.

Reading the Long-Term Price Chart

When analysts examine multi-decade price charts, the pattern to identify is a sharp post-boom decline followed by an extended price plateau. That flat base, persisting for months or years after the initial collapse, is a technical signal that supply destruction and demand stabilisation are setting the stage for a new cycle. Thermal coal post-2022 offers a clear contemporary example: a steep decline from the elevated 2022 spike, followed by persistent stabilisation in the approximately $100 to $130 per tonne range through 2023 and 2024.

Cost-of-Production as the Fundamental Floor

A commodity can be considered fundamentally cheap when its market price approaches or falls below the all-in sustaining cost (AISC) of production for the majority of active producers. At this level, a self-correcting mechanism begins to operate:

- Marginal producers exit the market or suspend operations

- New mine development stalls due to insufficient economic incentive

- Grades at existing mines naturally decline over time without reinvestment

- Supply begins to contract organically even without any formal production cuts

The principle that underpins contrarian commodity investing is straightforward: low prices are the cure for low prices. Supply shrinks, demand grows as users substitute toward the cheaper input, and the conditions for the next price cycle are quietly assembled.

A Framework for Identifying Supply-Demand Inflection Points

| Signal | Implication |

|---|---|

| Price below AISC for marginal producers | Supply destruction begins |

| No new mine development | Future supply pipeline shrinks |

| Grade decline at existing mines | Output falls even without closures |

| Demand substitution toward cheaper commodity | Demand increases as price falls |

| Inventories declining | Physical tightness emerging |

Why Nickel Sits Near the Top of the Opportunity List Right Now

Nickel's Post-Boom Suppression Pattern

Nickel prices surged dramatically in 2022 following a historic short-squeeze on the London Metal Exchange (LME), then collapsed as Indonesian laterite supply flooded global markets. As of 2024 and into 2025, nickel prices remain deeply suppressed relative to historical averages. For many Western and Australian producers, the nickel price has been trading near or below their cost of production, forcing project suspensions, mine closures, and the deferral of new development capital.

However, identifying the right type of nickel exposure is critical. Not all nickel is equal.

The Indonesian Laterite Problem: Environmental and Geopolitical Risk

Indonesia now accounts for over 50% of global nickel production, primarily from laterite deposits processed via High-Pressure Acid Leach (HPAL) or rotary kiln electric furnace (RKEF) methods. The Indonesian nickel supply dominance has structurally suppressed nickel prices globally, but it comes with a series of risks that are inadequately priced by most investors:

- Documented environmental damage at scale, including the generation of approximately 100 tonnes of toxic residual material per tonne of nickel laterite produced

- Historical use of deep-sea tailings disposal, where toxic material was pumped directly into marine environments, destroying surrounding ecosystems

- Transition to terrestrial tailings storage facilities located in high-rainfall, tectonically active jungle environments, creating long-term structural instability

- Human rights concerns associated with rapid industrial expansion in remote Indonesian provinces

The environmental and governance risks embedded in Indonesian laterite nickel production represent a systemic vulnerability in the global nickel supply chain. A single regulatory intervention, tailings failure, or ESG-driven procurement shift could materially tighten the supply of battery-grade nickel available to Western manufacturers.

Western automakers and battery manufacturers have consequently demanded sourcing transparency and "clean nickel" credentials, creating a growing bifurcation between Indonesian laterite supply and the nickel that can actually be accepted into Western battery supply chains without reputational or regulatory risk.

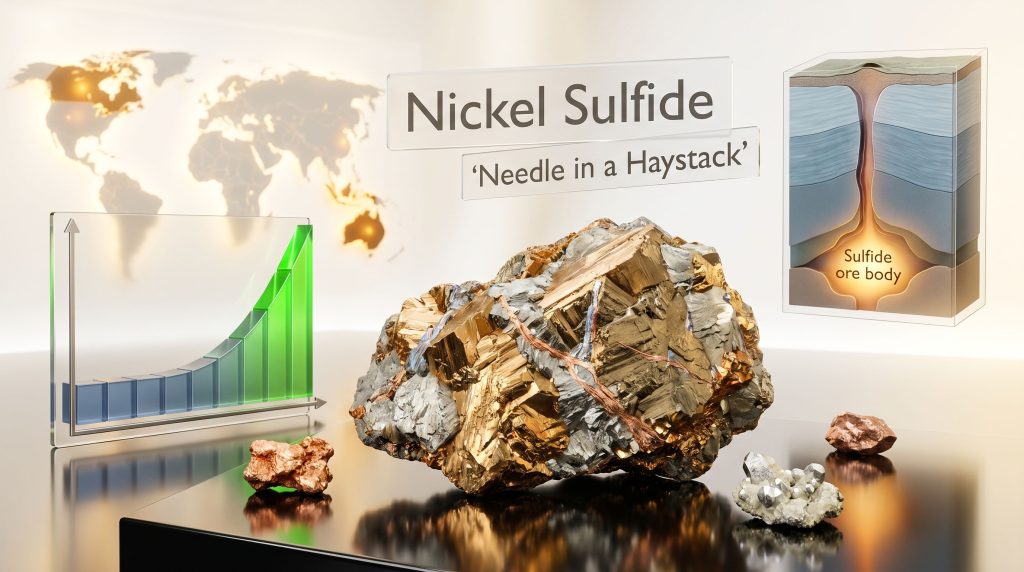

What Makes Nickel Sulfide Deposits Among the Most Coveted Assets in Mining

The Geological Distinction: Sulfide vs. Laterite

Magmatic nickel deposits form through intrusion processes deep within the Earth's crust — a fundamentally different geological origin from laterite deposits, which form through the surface weathering of ultramafic rock. This difference in origin translates into dramatically different deposit characteristics across every dimension that matters to investors and developers.

| Feature | Nickel Sulfide | Nickel Laterite |

|---|---|---|

| Formation process | Magmatic intrusion (deep crustal) | Surface weathering of ultramafic rock |

| Typical grade | High, often above 1% Ni | Lower, typically 0.8 to 1.5% Ni |

| Co-products | Copper, platinum group metals (PGMs) | Cobalt in some deposits |

| Processing complexity | Lower, conventional flotation | High, HPAL or RKEF required |

| Environmental footprint | Smaller physical footprint | Large footprint, significant waste volumes |

| Permitting difficulty | Generally more straightforward | Complex due to scale and waste management |

| Discovery difficulty | Extremely rare, limited surface expression | More common, surface-exposed |

Why Nickel Sulfide Commands an Investment Premium

The investment appeal of nickel sulfide deposits extends well beyond simple grade comparisons. Several attributes work together to make these deposits disproportionately attractive relative to their laterite counterparts:

- Co-product economics: The presence of platinum group metals and copper alongside nickel meaningfully improves overall project economics and reduces single-commodity price risk

- Processing cost advantage: Conventional flotation is far less energy-intensive than HPAL or RKEF processing, a critical advantage in an elevated energy price environment

- Smaller physical footprint: Translates directly into faster permitting timelines and lower community opposition risk compared to large-scale laterite operations

- Capital payback speed: High-grade sulfide deposits typically deliver rapid capital payback periods and strong internal rates of return (IRRs)

- ESG positioning: The absence of the tailings controversies associated with Indonesian laterite production makes sulfide deposits significantly more acceptable to Western automakers and institutional investors with ESG mandates

According to research on nickel sulfide deposits in Australia, these assets exhibit characteristics and resource potential that place them among the most strategically valuable in the global mining landscape. The Voisey's Bay deposit in Labrador, Canada, is frequently cited as the archetype of a world-class discovery, demonstrating the exceptional investor returns possible when a high-grade magmatic sulfide deposit is located in a Tier 1 jurisdiction.

Why Discovery Remains a Multi-Year or Multi-Decade Challenge

Nickel sulfide bodies are often small in physical extent, with limited or no surface expression. They do not announce themselves through obvious surface mineralisation the way some laterite systems do. Discovery depends heavily on geophysical methods, particularly electromagnetic (EM) surveys and gravity anomaly mapping, rather than surface sampling or visual inspection.

The geological conditions required for magmatic sulfide formation are specific and relatively rare globally. Exploration teams with strong track records in this space may spend years searching for a single quality target. According to United States Geological Survey data, magmatic nickel-copper sulfide deposits account for a substantial share of global nickel production despite representing a small fraction of known nickel occurrences worldwide.

The combination of small footprint, geophysical detectability, and high grade means that nickel sulfide discovery is fundamentally a needle-in-a-haystack exercise. When a quality deposit is found, however, the economic and investment rewards are disproportionately large relative to the exploration capital deployed.

This dynamic is central to the Jordan Roo commodities bull market and nickel sulfide deposits framework — the scarcity of high-quality sulfide assets amplifies their value at precisely the moment when ESG pressure on laterite supply is intensifying.

Potash: The Overlooked Food Security Commodity

Why Potash Fits the Cheap Commodity Framework

Potash prices remain historically depressed relative to the 2021–2022 fertiliser price spike, yet the structural demand case is as robust as any commodity in the complex. Global food demand is structurally growing as world population expands, and potash is a non-substitutable input in agricultural production. There is no meaningful alternative to it.

New mine development is extraordinarily capital-intensive and time-consuming. BHP's Jansen Mine in Saskatchewan, Canada, has experienced significant cost overruns and schedule delays, signalling to other potential developers that bringing new potash supply to market is far more difficult and expensive than initial project economics suggest. The perverse effect is that supply may remain more constrained for longer than the futures market currently anticipates.

Once built, however, potash mines carry reserve lives almost without parallel in the mining industry. Reserve lives measured in hundreds of years are common, with some resource estimates extending beyond one thousand years.

Navigating the Potash Investment Landscape

| Company Type | Examples | Key Characteristics |

|---|---|---|

| Major producers | Nutrien, The Mosaic Company | Large-scale, diversified, but carry significant balance sheet leverage |

| Royalty exposure | Altius Minerals | Lower leverage, royalty-based exposure, less sensitive to capital cost overruns |

Investors who are sensitive to balance sheet leverage may find royalty-based potash exposure more attractive than direct producer equity, given the capital-intensive and often over-budget nature of new potash mine development.

The next major ASX story will hit our subscribers first

Gold at Cycle Maturity: Mapping the Risk-Reward Honestly

How Long Do Gold Bull Markets Actually Last?

Since the United States abandoned the gold standard in 1971, gold has experienced several distinct bull market cycles. Historical bull market durations have ranged from approximately three years to just over ten years. The current gold bull market, measured from the late-2015 price bottom, is now approximately a decade in duration, placing it among the longer cycles on historical record.

This does not mean the bull market is over. The structural case for continued gold appreciation remains credible: government expenditure persistently exceeds tax revenue across major economies. The US dollar has lost approximately 97% of its purchasing power over the past century, and the 2022 use of the dollar as a sanctions weapon against Russia has accelerated central bank gold accumulation globally.

The Asymmetric Risk of Major Gold Producers at Current Valuations

Despite the bullish structural narrative, the risk-reward profile of major gold producers at current valuations warrants careful scrutiny. A large-cap gold producer trading at approximately 12 times forward free cash flow after a five-fold increase in the gold price presents a specific asymmetry: a further $2,000 per ounce rise in gold might produce a doubling of the equity, while a $2,000 per ounce decline could produce a drawdown of 70 to 75%. That is not an attractive risk-reward ratio for new capital.

Why Royalty and Streaming Companies Offer a More Favourable Structure

The structural advantages of royalty and streaming companies become particularly relevant as the gold cycle matures:

| Metric | Major Producer | Royalty/Streaming Company |

|---|---|---|

| Gross margin | 40 to 60%, variable with gold price | 85 to 90%, largely stable |

| Leverage to gold price decline | High: margins compress and revenue falls simultaneously | Lower: margins stable, only revenue falls |

| Balance sheet risk | Often carries significant debt | Typically low debt |

| Growth profile | Dependent on ongoing capex deployment | Embedded in existing royalty portfolio |

| S&P 500 eligibility | Most are Canadian-domiciled | US-domiciled options exist |

A royalty company with approximately 86% gross margins does not see those margins collapse when the gold price falls. Revenue declines, but the business model remains intact. A conventional producer, by contrast, faces a double compression: falling revenue per ounce and simultaneously shrinking margins as fixed costs remain constant.

Silver: The Latent Supply Risk That Mainstream Narratives Are Ignoring

The Gold-to-Silver Ratio as a Diminishing Analytical Tool

Silver's demand profile has fundamentally shifted in recent decades. Industrial applications, including solar panels, electronics, and electric vehicles, now represent a growing and structurally significant share of total demand. This blurs the traditional gold-silver ratio framework, which was developed when both metals served primarily monetary functions. The ratio may be a less reliable valuation tool today than it was in prior cycles.

For perspective, platinum is significantly rarer than gold on a geological basis, yet gold trades at a substantial multiple to platinum prices. If the gold-to-platinum ratio is not considered a reliable valuation tool, the analytical basis for the gold-to-silver ratio deserves the same level of scrutiny.

The Rural Asian Silver Savers: A Supply Overhang No One Is Talking About

An estimated 1 to 1.5 billion people across rural Asia, particularly in India, China, and Southeast Asia, hold physical silver as their primary savings vehicle. In markets like India, silver jewellery and silverware trade at or near spot price, making it a highly liquid store of value that functions more like a bank account than a decorative purchase.

As silver prices have risen sharply, these holders are sitting on significant unrealised gains. Consider the mathematics:

- At 1 ounce of silver sold per person across 1.5 billion rural Asian savers, the implied supply release is approximately 1.5 billion ounces

- Annual global silver mine supply is estimated at approximately 800 to 900 million ounces per year

- That single-ounce-per-person scenario represents nearly two years of global mine production arriving on the market

- At 3 ounces per person, the implied supply release extends to multiple years of mine supply

Scenario Analysis: If even a small fraction of rural Asian silver savers choose to monetise holdings to fund a vehicle purchase, a move to the city, or a land acquisition, the volume of silver coming to market could be materially larger than current supply models anticipate. This latent supply overhang is largely absent from mainstream silver bull narratives.

Combined with a price chart that exhibits the characteristics of a parabolic advance, the risk profile for silver warrants more caution than the gold-to-silver ratio narrative suggests.

Evaluating Junior Mining Companies: The Dollar-Per-Ounce Trap

Why Cheap Per-Ounce Metrics Are Often Misleading

One of the most common errors in junior mining investment is treating a low implied valuation on a per-ounce-in-the-ground basis as a proxy for value. This metric ignores the fundamental question of whether a deposit can ever be economically developed and permitted. Considerations around grade and permitting are therefore essential components of any rigorous junior mining assessment.

Real-world examples of permanently impermittable deposits include:

- A project requiring the drainage of a rare trout-bearing lake, where only approximately one in one hundred Ontario lakes qualifies as trout habitat

- A project that would require the relocation of a functioning cemetery, requiring consent from the families of all individuals interred there — a practical and legal impossibility in most jurisdictions

- Projects located adjacent to Indigenous land claims, protected water sources, or culturally protected sites

In each case, the low per-ounce trading price reflects a rational market assessment that the deposit is unlikely to be developed, not an overlooked value opportunity.

A Framework for Assessing Junior Mining Quality

| Quality Indicator | High-Quality Project | Red Flag Project |

|---|---|---|

| Jurisdiction | Tier 1 (Canada, Finland, Australia, Nevada) | High-risk or unstable jurisdiction |

| Permitting pathway | Clear, precedented, low community opposition | Requires unprecedented environmental approvals |

| Deposit consistency | Uniform mineralisation, easy to drill cheaply | Erratic grades, complex structural geology |

| Grade | High relative to sector peers | Below economic threshold for development |

| Capex-to-production ratio | Reasonable payback period | Excessive capital requirement relative to output |

| Exploration upside | Significant open extensions beyond current resource | Limited additional resource potential |

A high-quality junior mining investment combines consistent, high-grade mineralisation with a clear permitting pathway in a Tier 1 jurisdiction. These attributes are rare, but when they converge, the market tends to recognise them. Rupert Resources, located in Finland, traded at approximately $680 per ounce in the ground before being acquired, reflecting the premium that genuine quality commands in a market where truly developable deposits are uncommon.

Commodity Selectivity Within the Bull Market: A Decision Framework

Not all commodities benefit equally from the structural trends outlined above. A disciplined top-down selection process identifies the specific intersections of cheap pricing, supply destruction, and structural demand growth. The Jordan Roo commodities bull market and nickel sulfide deposits framework applies this logic systematically:

- Identify commodities trading at or below historical cost-of-production floors

- Assess the supply pipeline: are new mines being built or are they being deferred?

- Evaluate the demand trajectory: is structural demand growing, stable, or in decline?

- Confirm the price chart shows a post-boom plateau consistent with supply destruction and demand stabilisation

- Narrow focus to commodities where supply destruction and demand growth are converging simultaneously

Mapped across the four primary commodity beneficiary categories:

- Electrification beneficiaries: Nickel, lithium, cobalt, copper

- AI infrastructure beneficiaries: Copper, aluminium, silver (industrial component), rare earths

- Poverty-transition beneficiaries: Oil, steel, cement, potash

- Monetary debasement beneficiaries: Gold, silver (monetary component)

Within each category, the application of the cheap-commodity framework narrows the field considerably. Nickel, at current suppressed price levels, combined with the structural scarcity of high-quality sulfide deposits and the growing ESG liability of Indonesian laterite supply, sits at a particularly compelling intersection of these forces. Furthermore, the Jordan Roo commodities bull market and nickel sulfide deposits thesis reinforces why selective positioning — rather than broad commodity exposure — is the more disciplined approach for investors navigating this cycle.

Disclaimer: This article is for informational and educational purposes only. It does not constitute financial or investment advice. Commodity markets involve significant risk, and past performance is not indicative of future results. Investors should conduct their own research and consult a licensed financial adviser before making any investment decisions. Forward-looking statements and projections discussed in this article are speculative in nature and subject to material uncertainty.

Ready to Capitalise on the Next Major Mineral Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — transforming complex geological and commodity data into clear, actionable investment insights for both short-term traders and long-term investors. Explore historic examples of major mineral discoveries and their market returns, then start your 14-day free trial at Discovery Alert to position yourself ahead of the next major find.