May 17, 2026

What Drives Multi-Decade Commodity Supercycles?

The architecture of commodity markets operates on geological timescales that clash violently with financial market expectations. When demand surges meet supply constraints forged decades earlier, the resulting price dynamics can sustain themselves for periods that confound traditional economic modeling. Understanding these extended cycles requires examining the fundamental mechanics that separate commodity markets from other asset classes.

Historical Pattern Analysis of 20+ Year Commodity Booms

The 1970s energy crisis represents perhaps the most documented commodity supercycle in modern economic history. Oil prices escalated from approximately $3 per barrel in 1970 to peak at $38 per barrel by 1980, driven initially by OPEC embargo actions but sustained by structural supply-demand imbalances that persisted well beyond geopolitical triggers. This surge in commodities lasting for years extended through the early 1980s as stagflation gripped developed economies, demonstrating how commodity cycles operate independently of their initial catalysts.

The post-World War II reconstruction cycle from 1945 to 1965 showcased the power of synchronized global demand growth. Copper prices more than tripled over this two-decade period as industrial production ramped across Europe and Japan. Steel consumption in OECD countries grew at compound annual rates exceeding 4-5% during reconstruction phases, compared to historical averages of 1-2% in mature economies.

More recently, the emerging market industrialization wave from 1990 to 2010 produced commodity price movements of unprecedented scale. Copper rose from approximately $0.80 per pound in 2001 to exceed $4.00 per pound by 2008, while iron ore price trends increased roughly 2,000% over the same period. Global commodity indices gained approximately 350-400% from 1999 to 2008, illustrating how sustained demand growth from large economies can drive multi-year price appreciation.

Supply-Demand Imbalance Mechanics

The commodity production pipeline operates on substantially extended timeframes that create structural supply inflexibility during demand upswings. This temporal mismatch between market signals and supply response forms the foundation of extended commodity cycles.

Average Lead Times for New Commodity Production:

| Commodity | Development Timeline | Key Constraints |

|---|---|---|

| Copper mines | 7-15 years | Exploration, permitting, construction |

| Oil fields (offshore) | 5-10 years | Subsea infrastructure, regulatory approval |

| Lithium operations | 3-8 years | Environmental permits, processing capacity |

| Rare earth processing | 3-5 years | Technical complexity, waste management |

These lead times create critical market dynamics where price signals today cannot generate supply responses for years. When copper prices rose dramatically during 2008, producers could not rapidly expand output due to multi-year development requirements. This lag structure sustains price elevation as markets must wait for capacity decisions made years prior to come online.

The 2008 financial crisis demonstrated this lag effect clearly. Copper declined from $4.00 per pound to under $1.25 by early 2009, prompting mining companies to cancel or defer numerous projects during 2009-2012. The result was constrained copper supply growth through the mid-2010s, providing underlying support for prices during subsequent recovery phases.

Monetary Policy Amplification Effects

Real interest rate environments create the macroeconomic backdrop that either supports or undermines commodity valuations over multi-year periods. When central bank policies maintain real rates below historical norms, hard assets benefit from both reduced opportunity costs and increased inflation hedging demand.

Currency debasement pressures, whether from fiscal excess or accommodative monetary policy, drive commodity re-pricing as assets denominated in weakening currencies require higher nominal prices to maintain purchasing power parity. This dynamic becomes self-reinforcing when multiple major economies pursue similar policies simultaneously.

Institutional portfolio allocation shifts toward inflation hedges amplify these monetary policy effects. When traditional bond markets face sustained bear conditions, institutional investors increase commodity allocations from typical 2-5% weightings toward 10-15% or higher, creating sustained buying pressure independent of industrial demand fundamentals.

When big ASX news breaks, our subscribers know first

How Geopolitical Fragmentation Reshapes Resource Markets

The globalised commodity trading system that dominated from 1990 to 2020 is fragmenting into competing resource blocs as governments prioritise supply security over economic efficiency. This structural shift creates new price dynamics and supply constraints that traditional economic models struggle to capture.

Supply Chain Nationalisation Trends

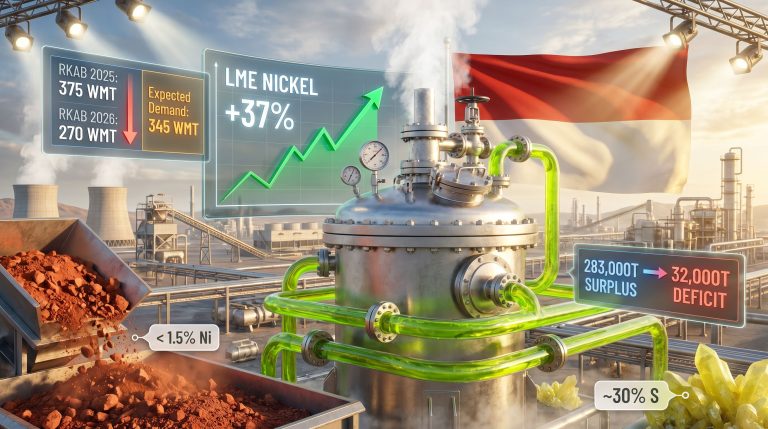

Resource sovereignty has replaced free trade optimisation as the dominant policy paradigm across major economies. Countries implementing active export controls or export restrictions on key commodities during 2024-2026 span the globe, including Indonesia's nickel ore export bans, China's rare earth element restrictions, and multiple African nations implementing cobalt and copper export taxes.

Critical mineral stockpiling by major economies has accelerated dramatically. The US Defense Logistics Agency expanded strategic stockpile targets for materials including cobalt, nickel, and lithium. China continues expanding rare earth strategic reserves, particularly for heavy rare earths like dysprosium and terbium. The European Union allocated over €1 billion toward domestic processing capacity development by 2030 through the Critical Raw Materials Act.

Key Export Restriction Categories (2024-2026):

• Raw material export bans: Indonesia (nickel ore), China (unprocessed rare earths)

• Export taxes and quotas: Multiple African nations (copper, cobalt)

• Processing requirements: Argentina (lithium), Chile (copper concentrate limits)

• Strategic material classifications: USA, EU, Australia (various critical minerals)

Infrastructure Weaponisation Impact

Iran's closure of the Strait of Hormuz in April 2026 following Middle East conflict escalation demonstrates how critical infrastructure becomes weaponised during geopolitical tensions. This closure affects approximately 20-30% of global seaborne oil trade, forcing cargo rerouting through longer routes around Africa or via pipeline alternatives where available.

The immediate effects include increased shipping costs and transit times extended by 2-4 weeks. While strategic petroleum reserve releases and increased production from non-OPEC sources like US shale and Brazil's pre-salt fields provide partial offsets, full replacement requires time given production ramp constraints.

Rare earth processing bottlenecks in Asia-Pacific create similar vulnerability points. China controls approximately 70-80% of global rare earth separation and refining capacity, creating dual bottlenecks where even Western mining production increases face processing limitations. However, Bank of America's analysis suggests the surge in commodities lasting for years will persist despite these constraints. Neo Performance Materials' production of heavy rare earths at their Estonia facility beginning in April 2026 represents incremental Western processing capacity expansion, but remains marginal relative to Chinese capacity.

Rail and port capacity constraints in major mining regions create additional supply bottlenecks independent of mine production capability. Peru's copper exports face port capacity limitations in northern regions, constraining throughput to approximately 1-1.5 million tonnes monthly despite higher mining capability. Similar infrastructure limitations affect Australia, Canada, and other major exporting regions.

Alliance-Based Trading Bloc Formation

The QUAD partnership between the USA, Japan, India, and Australia has formalised mineral security cooperation through initiatives like the Mineral Security Partnership announced in 2022. This framework focuses specifically on lithium, cobalt, and rare earth supply chain development outside Chinese control, with coordinated investment commitments toward developing alternative sources in partner countries.

EU-US critical materials cooperation has advanced significantly, with both regions finalising a minerals pact in April 2026 aimed at reducing China reliance and stabilising supply chains amid geopolitical mineral policies. The framework likely includes preferential trade terms, joint investment in processing infrastructure, and coordinated sourcing from aligned nations emphasising Australian, Canadian, and selected Latin American producers.

China's Belt and Road resource corridor strategy operates as the competing framework, targeting resource-producing nations in Africa and Southeast Asia. This approach often provides infrastructure financing in exchange for resource access commitments, creating long-term supply security for Chinese processors and refiners while potentially limiting Western access to key materials.

Which Commodities Lead the Current Supercycle Phase?

The composition of the current commodity surge reflects unique technological and geopolitical drivers that distinguish it from previous cycles. Unlike the broad-based demand growth of the 1970s or 2000s, today's surge in commodities lasting for years concentrates in materials essential for energy transition, strategic competition, and monetary uncertainty.

Energy Transition Metal Requirements

Copper demand faces unprecedented growth requirements as electrical grid infrastructure expands globally to accommodate renewable energy integration and electric vehicle charging networks. Current projections indicate copper demand increasing 85% by 2035, driven primarily by grid infrastructure development rather than traditional construction applications.

Projected Demand Growth (2025-2035):

| Metal | Demand Increase | Primary Driver | Supply Constraint |

|---|---|---|---|

| Copper | 85% | Grid infrastructure, EVs | Mine development lead times |

| Lithium | 300% | EV battery scaling | Processing capacity limits |

| Nickel | 130% | Energy storage systems | Indonesia export restrictions |

| Silver | 60% | Solar panel production | Mine by-product dependency |

Lithium faces the most dramatic demand expansion, with 300% growth projected through 2035 as electric vehicle adoption accelerates and grid-scale energy storage deployment increases. Furthermore, lithium industry innovations are driving new processing techniques and extraction methods. However, supply response faces significant constraints from environmental permitting delays, particularly in South American brine operations where water usage concerns create political opposition.

Nickel demand growth of 130% over the next decade stems primarily from battery applications, with energy storage systems requiring high-grade nickel for cathode production. Indonesia's policy shifts from raw ore exports to processed products create near-term supply constraints while long-term capacity additions remain dependent on Chinese processing partnerships.

Traditional Energy Complex Dynamics

Natural gas maintains its position as a transition fuel, supporting higher floor prices as coal-to-gas switching continues in developing economies while renewable intermittency requires backup generation. The current supply-demand balance faces additional complexity from Russian pipeline disruptions and increased LNG export capacity competition between major producers.

Oil markets experience structural changes from reduced investment cycles during 2020-2022, creating supply constraints that persist despite demand normalisation. Crude oil prices at $104.40 per barrel for Brent crude in April 2026 reflect not just geopolitical risk premiums but underlying capacity constraints from years of deferred investment in new field development.

Coal demand demonstrates surprising persistence despite environmental pressures, with developing economy steel production maintaining consumption levels. Metallurgical coal faces particular supply constraints as environmental regulations limit new mine development in major producing regions including Australia and Canada.

Precious Metals in Portfolio Allocation Shifts

Central bank gold accumulation accelerated to approximately 1,200 tonnes annually as monetary authorities diversify reserves away from government bonds amid fiscal sustainability concerns. This institutional demand provides sustained buying pressure independent of traditional investment demand cycles.

In addition, gold as inflation hedge continues to drive institutional and retail investor interest. Gold futures at $4,713.30 per ounce in April 2026 reflect not just geopolitical risk but fundamental portfolio rebalancing as investors seek alternatives to government bonds facing bear market conditions. The metal's performance illustrates how monetary uncertainty creates sustained demand for traditional store-of-value assets.

Silver's dual industrial-monetary demand profile creates unique dynamics during the current cycle. Silver futures at $75.48 per ounce capture both solar panel production demand growth and monetary hedge demand, with the metal's smaller market size amplifying price movements relative to gold.

Platinum group metals benefit from hydrogen economy development, though demand growth remains more speculative than other precious metals. Palladium faces supply constraints from Russian export limitations while demand patterns shift between automotive catalysts and potential hydrogen applications.

What Investment Strategies Capitalise on Extended Commodity Cycles?

Participating in multi-year commodity cycles requires strategic frameworks that account for volatility, timing uncertainty, and the unique characteristics of different commodity exposure vehicles. Traditional asset allocation approaches often underestimate both the duration and magnitude of commodity supercycles.

Direct Commodity Exposure Vehicles

ETF selection requires careful analysis of structure differences that significantly impact returns during extended cycles:

• Physical-backed structures: Provide direct commodity exposure without roll costs but face storage limitations and fees

• Futures-based structures: Offer liquidity and diversification but suffer from contango costs during supply-abundant periods

• Equity-linked products: Capture operational leverage but introduce company-specific risks and management quality variables

Contango risk management becomes critical in energy products where futures curves often trade in contango during supply surplus periods. The United States Oil Fund (USO) lost substantial value during 2020-2022 despite oil price recovery due to persistent negative roll yields, illustrating how structure selection affects long-term returns.

Storage cost considerations vary dramatically across commodities. Gold ETFs face annual storage costs of approximately 0.4-0.6%, while industrial metals ETFs may face storage costs exceeding 1-2% annually, creating drag during sideways price periods but providing pure exposure during trending markets.

Equity Positioning Across Market Capitalisations

Large-cap miners offer dividend sustainability and operational stability but typically provide limited leverage to commodity price movements. Companies like BHP and Rio Tinto maintain dividend policies through commodity cycles, but their diversified operations and large asset bases limit upside participation during price booms.

Mid-cap developers present project financing risk assessment challenges but offer significant leverage to commodity prices once projects reach production. These companies face binary outcomes where successful project completion generates substantial returns, but financing failures or development delays create total loss risks.

Equity Strategy Framework by Market Cap:

• Large-cap miners (>$20B market cap): Core holdings for dividend income and stability

• Mid-cap developers ($1-20B market cap): Growth positions with defined project catalysts

• Small-cap explorers (<$1B market cap): Speculative allocations with discovery potential

Small-cap explorers require discovery premium valuation models that account for geological risk, permitting uncertainty, and financing capability. Historical data indicates that fewer than 5-10% of exploration companies successfully advance projects from discovery through production, requiring portfolio approaches with numerous positions to capture occasional outsized winners.

Geographic Diversification Frameworks

Jurisdiction risk weighting has become increasingly critical as resource nationalism intensifies globally. Political stability scoring systems help assess long-term operational risks that can dramatically impact investment returns regardless of commodity price performance.

Jurisdiction Risk Assessment Matrix:

| Jurisdiction | Political Stability | Regulatory Environment | Currency Risk |

|---|---|---|---|

| Australia | AAA | Stable, established | Low (AUD hedging available) |

| Canada | AA+ | Stable, provincial variations | Low (CAD correlation) |

| Chile | BB+ | Moderate, election sensitivity | Medium (CLP volatility) |

| Peru | B+ | High, frequent policy changes | High (PEN instability) |

Currency hedging requirements by region create additional complexity for international commodity investments. Chilean peso exposure affects copper investments, while South African rand volatility impacts platinum group metals investments. Effective hedging strategies must balance currency risk reduction against hedging costs that can exceed 2-3% annually in volatile currency pairs.

How Do Macroeconomic Cycles Interact with Resource Pricing?

Commodity markets operate within broader macroeconomic cycles that either amplify or dampen fundamental supply-demand dynamics. Understanding these interactions provides critical context for timing and positioning decisions during extended commodity cycles.

Interest Rate Sensitivity Analysis

Real yield correlation with commodity performance demonstrates clear patterns across different rate environments. When real yields (nominal yields minus inflation expectations) remain below historical averages, commodities benefit from reduced opportunity costs and increased inflation hedging demand.

Fed policy transmission to emerging market currencies creates secondary effects on commodity demand. When the Federal Reserve maintains accommodative policies, emerging market currencies strengthen relative to the dollar, increasing local purchasing power for dollar-denominated commodities and supporting demand growth.

Historical Commodity Returns by Rate Environment (1970-2025):

| Real Yield Environment | Commodity Index Return | Duration (Years) | Leading Sectors |

|---|---|---|---|

| Negative real yields (<0%) | +15.2% annually | 8.3 average | Energy, precious metals |

| Low real yields (0-2%) | +8.7% annually | 5.1 average | Industrial metals, agriculture |

| High real yields (>2%) | -2.1% annually | 4.2 average | Minimal commodity outperformance |

Dollar Strength Impact Modelling

DXY level thresholds create identifiable breakpoints affecting commodity demand patterns. Historical analysis indicates that DXY levels above 105 typically constrain commodity demand from emerging markets, while levels below 95 generally support broad-based commodity strength.

Emerging market purchasing power dynamics explain much of this relationship. When the dollar strengthens significantly, countries with dollar-denominated debt face increased servicing costs, reducing available capital for commodity imports and infrastructure investment that drives industrial demand.

However, tariffs impact markets in complex ways that can offset traditional dollar strength effects. Trade-weighted currency basket considerations provide more nuanced analysis than DXY alone. The Chinese yuan, Euro, and Japanese yen weightings in global trade patterns affect commodity demand differently than DXY movements suggest, particularly for industrial metals where China represents 40-60% of global consumption.

Inflation Expectations and Asset Allocation

TIPS breakeven rates serve as forward-looking indicators of commodity demand from institutional investors. When 5-year TIPS breakevens exceed 3%, historical data suggests increased institutional allocation toward commodities as inflation hedges, creating sustained buying pressure independent of industrial demand.

Institutional portfolio rebalancing triggers typically activate when commodity allocations drift beyond target ranges of 5-15% of total portfolios. During the current cycle, many institutional investors have increased target allocations toward the upper end of this range, providing structural demand support.

The fundamental shift toward hard assets reflects recognition that traditional bond portfolios may face sustained bear market conditions rather than cyclical corrections.

Retail investor behaviour during inflationary periods shows distinct patterns where precious metals purchases accelerate when CPI prints exceed 4-5% annually. This retail demand, while smaller than institutional flows, can create significant price momentum in smaller markets like silver where industrial demand provides underlying support.

What Risk Management Approaches Address Commodity Volatility?

Commodity markets exhibit volatility patterns that exceed most other asset classes, requiring specialised risk management frameworks that account for both fundamental and technical factors driving price movements.

Position Sizing Methodologies

Portfolio allocation guidelines for commodity exposure must balance opportunity capture with volatility management:

-

Core commodity exposure: 5-15% of total portfolio provides meaningful participation while limiting overall portfolio volatility

-

Tactical overlay positions: 2-5% for momentum plays allow increased exposure during favourable technical or fundamental conditions

-

Hedge positions: 1-3% for downside protection using precious metals or volatility products during periods of elevated systematic risk

These allocation ranges reflect historical analysis showing that commodity weightings below 5% provide insufficient benefit capture during supercycles, while allocations above 20% create excessive portfolio volatility that triggers emotional selling during inevitable correction periods.

Position sizing within commodity allocations requires additional consideration of correlation patterns. Copper, aluminium, and zinc often move together due to industrial demand linkages, requiring diversification across sectors rather than just individual commodities.

Timing Strategy Frameworks

Technical analysis applications in commodity markets focus on longer-term trend identification rather than short-term trading signals. Moving average systems using 50-day and 200-day periods help identify trend changes that often persist for months or years in commodity markets.

Fundamental supply-demand indicator monitoring requires specialised data sources and analytical frameworks. Inventory-to-consumption ratios provide early warning signals when they drop below historical ranges, typically indicating tightening markets that support higher prices.

Key Monitoring Indicators for Cycle Timing:

• Global manufacturing PMI divergence patterns: Leading indicator for industrial metal demand

• Inventory-to-consumption ratios: Supply tightness measurement across major commodities

• Capex announcement trends: Forward-looking supply growth indicator in resource sectors

• Central bank policy divergence: Monetary policy impact on real yields and dollar strength

Seasonal pattern exploitation techniques work particularly well in agricultural commodities and natural gas, where weather and storage cycles create predictable price movements that can be captured through systematic approaches.

Correlation Risk Management

Cross-commodity relationship monitoring becomes critical during crisis periods when traditional diversification benefits erode. Historical analysis shows that commodity correlations can increase from typical ranges of 0.3-0.6 to above 0.8-0.9 during major market stress events.

Equity market spillover effects create additional correlation risks, particularly during liquidity crises when forced selling affects all risk assets simultaneously. The 2008 financial crisis and March 2020 COVID-19 panic demonstrated how commodity prices can decline alongside equities despite strong fundamental supply-demand characteristics.

Diversification benefits erode during crisis periods when correlations approach unity, requiring dynamic position management and liquidity reserves for opportunity capture.

This correlation breakdown emphasises the importance of maintaining adequate liquidity reserves during commodity cycles to take advantage of temporary dislocations that create exceptional opportunity.

The next major ASX story will hit our subscribers first

Why Traditional Economic Models Underestimate Commodity Duration?

Academic economic literature consistently underestimates commodity cycle duration and magnitude due to theoretical assumptions that diverge significantly from real-world market dynamics. Understanding these model limitations provides insight into why surges in commodities lasting for years often surprise conventional forecasts.

Substitution Effect Limitations

Physical constraints on alternative material adoption create multi-year lags that economic models typically underestimate. Aluminium conductor substitution for copper in electrical applications requires extensive engineering validation, testing, and regulatory approval processes that extend 3-5 years before widespread implementation becomes feasible.

Technology transition timelines exceed economic forecasts consistently. Electric vehicle adoption projections often assume smooth substitution curves, but battery chemistry changes, charging infrastructure deployment, and consumer behaviour modifications create discontinuous adoption patterns that sustain commodity demand longer than linear models predict.

Infrastructure lock-in effects extend demand profiles beyond substitution possibilities. Existing copper wiring in buildings, electrical grids, and industrial facilities cannot be replaced economically, creating sustained demand for maintenance and expansion that persists regardless of alternative material availability.

Elasticity Assumptions in Academic Literature

Short-term versus long-term price responsiveness differences create modelling errors where academic literature applies inappropriate elasticity coefficients. Copper demand shows relatively inelastic response to price changes in the short term (6-24 months) due to project commitments and engineering specifications, but longer-term demand (5+ years) demonstrates greater price sensitivity as substitution and efficiency improvements become viable.

Behavioural economics factors in commodity consumption patterns deviate from rational economic assumptions. Industrial consumers often maintain supply relationships and inventory policies based on risk management rather than pure price optimisation, creating demand stability during price increases that exceeds model predictions.

Government intervention distorts market signals through subsidies, strategic stockpiling, and trade restrictions that traditional supply-demand models cannot capture effectively. China's rare earth export policies, for example, create artificial scarcity that sustains higher prices regardless of underlying production costs or traditional market forces.

Feedback Loop Complexity

Investment cycle amplification effects operate through multiple feedback mechanisms that linear economic models cannot capture. Higher commodity prices increase mining company cash flows, enabling expansion capital investment, but with multi-year development lags that create cyclical oversupply once projects reach production simultaneously.

Speculation versus fundamental demand interactions create price dynamics that diverge from pure supply-demand fundamentals. Financial investor participation in commodity markets through ETFs and futures contracts can amplify both upward and downward price movements beyond levels justified by physical market conditions.

Central bank policy response lag impacts create additional complexity. When commodity price increases contribute to inflation pressures, central bank responses through interest rate adjustments affect commodity demand with 12-24 month delays, creating policy feedback loops that extend cycle duration beyond initial fundamental drivers.

Positioning for the Remainder of the 2020s Supercycle

The current commodity cycle shows characteristics suggesting extended duration through the remainder of the decade, driven by structural factors that differ from previous cycles. Investment positioning requires understanding both the fundamental drivers and the potential catalysts that could alter cycle dynamics.

Key Monitoring Indicators

Global manufacturing PMI divergence patterns provide early insight into industrial metal demand shifts. When major economies show divergent manufacturing trends, commodity demand typically follows the strongest regions with 3-6 month lags. Current patterns indicate continued strength in emerging markets despite developed economy moderation.

Inventory-to-consumption ratios across major commodities currently sit at or below long-term averages for copper, aluminium, and zinc, indicating supply tightness that supports higher price floors. Historical analysis suggests that ratios below the 25th percentile of historical ranges typically sustain price strength for 12-24 months minimum.

Capex announcement trends in resource sectors remain below levels required to meet projected demand growth through 2030. Mining industry capital expenditure announcements during 2024-2026 total approximately 40% below levels required to meet consensus demand forecasts, suggesting supply constraints will persist.

Strategic Portfolio Implications

Overweight recommendations for resource-exposed assets reflect both fundamental supply-demand dynamics and macroeconomic positioning benefits. The World Bank's commodity markets outlook supports expectations that the Bloomberg Commodity Index climbing 35% since the start of 2025, more than double S&P 500 returns over the same period, validates the strategic thesis while suggesting further upside potential remains.

Currency hedging considerations for international exposure require careful analysis of correlation patterns during commodity cycles. Resource-producing currencies like the Canadian dollar, Australian dollar, and Chilean peso typically strengthen during commodity booms, providing natural hedging for commodity investments but creating currency risk for other portfolio components.

Timeline expectations for cycle maturation suggest the current supercycle could extend through 2028-2030 based on supply development lead times and sustained structural demand from energy transition requirements. However, investors should remain prepared for volatile correction periods that create reentry opportunities without signalling cycle termination.

The combination of geopolitical fragmentation, monetary policy constraints, and supply-demand fundamentals creates a framework supportive of sustained commodity strength. While short-term volatility remains inevitable, the structural drivers supporting this surge in commodities lasting for years appear likely to persist through the remainder of the decade.

Disclaimer: This analysis is for educational purposes only and does not constitute investment advice. Commodity investments carry substantial risks including price volatility, geopolitical factors, and regulatory changes. Past performance does not guarantee future results. Investors should conduct their own research and consider their risk tolerance before making investment decisions.

Ready to Capitalise on the Next Major Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities ahead of the broader market. Understand why historic discoveries can generate substantial returns by exploring major mineral finds that have transformed portfolios, then begin your 14-day free trial today to position yourself ahead of the market.