August 9, 2026

The United States demonstrates a complex relationship with copper resources that extends beyond simple mining capacity to encompass sophisticated processing infrastructure requirements. Current copper investment trends reflect increasing recognition that copper refining capacity in the US represents a critical bottleneck in transforming raw materials into market-ready products.

Complex metallurgical supply chains require precise coordination between extraction, processing, and refining operations to deliver market-ready products. In copper markets, this coordination becomes particularly challenging when mining capacity exceeds downstream processing infrastructure, creating bottlenecks that force raw materials through extended international supply chains before reaching end users.

The copper industry demonstrates how resource abundance alone cannot guarantee supply security. Nations with substantial mining operations may paradoxically depend on foreign processing facilities to convert their raw materials into usable formats, highlighting the critical importance of integrated industrial infrastructure in mineral value chains.

Analyzing America's Processing Infrastructure Against Global Benchmarks

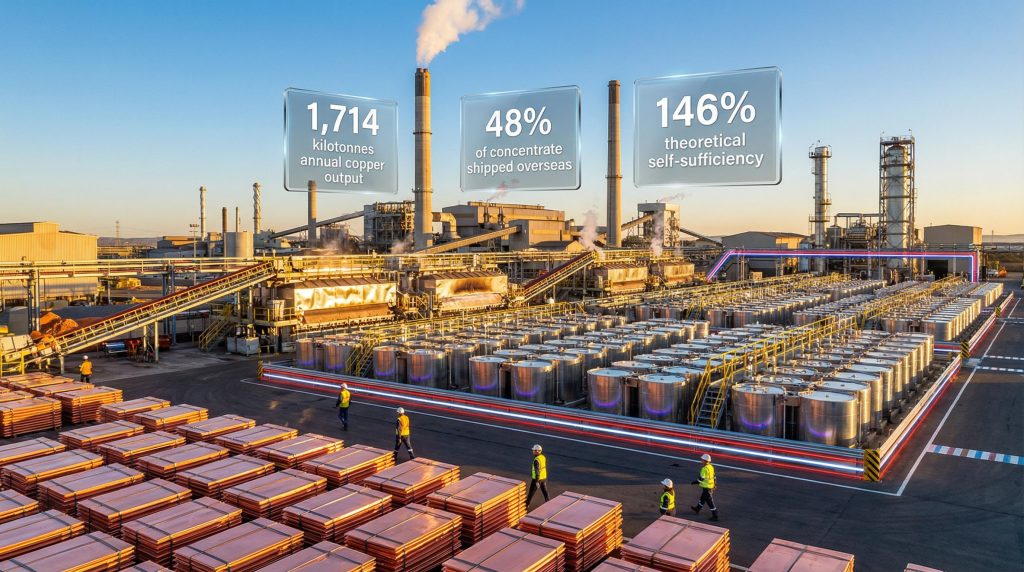

The United States operates within a unique position in global copper markets, producing 1.714 kilotonnes of copper annually while maintaining theoretical self-sufficiency at 146 percent of domestic demand when combining mining output with scrap recovery resources. This metric substantially exceeds China's 40 percent self-sufficiency rate, positioning America as a potentially independent copper producer.

However, this theoretical advantage dissolves when examining actual market flows. Despite producing sufficient raw copper materials to exceed domestic consumption, the United States imports significant volumes of refined copper cathode to supply manufacturing sectors. This disconnect reveals the fundamental challenge: resource availability without corresponding processing capacity creates supply chain vulnerabilities rather than advantages.

Processing Capacity Utilization Metrics

| Processing Stage | US Capacity | Utilization Challenge | Market Impact |

|---|---|---|---|

| Primary Mining Output | 1,714 kilotonnes annually | Exceeds domestic demand | Raw material surplus |

| Concentrate Processing | Limited smelting facilities | 48% exported for processing | Foreign dependency |

| Refined Cathode Production | Insufficient refining capacity | Import requirements despite surplus | Supply chain inefficiency |

| Scrap Recovery Integration | Substantial secondary sources | Processing bottlenecks | Underutilized resources |

The processing constraint fundamentally transforms copper market dynamics. While copper mining operations generate substantial concentrate volumes, the nation's limited smelting and refining infrastructure cannot convert these materials into the refined cathode format required by manufacturers. This creates the paradoxical situation where a copper-surplus nation depends on imports of refined copper products.

Market specialists emphasise that this constraint represents an industrial infrastructure problem rather than a resource scarcity issue. Furthermore, understanding the global copper supply forecast reveals how processing limitations affect broader market dynamics. The solution involves expanding downstream processing capabilities rather than acquiring additional mining assets, as unprocessed materials cannot directly serve manufacturing requirements regardless of their availability.

When big ASX news breaks, our subscribers know first

Identifying Critical Processing Bottlenecks

The American copper processing system operates through severely constrained infrastructure that creates systematic bottlenecks throughout the value chain. Current processing facilities include only 2 active primary electrolytic refineries, 14 electrowinning operations with variable utilisation rates, and 3 operational secondary fire refineries dedicated to scrap processing.

This limited infrastructure forces approximately 48 percent of American copper concentrate into export markets for foreign processing, primarily to Chinese refineries. The exported concentrate undergoes smelting and refining abroad before potentially returning as refined cathode, creating multiple transportation cycles and extended supply chains.

Infrastructure Capacity Analysis

Smelting Bottlenecks:

- Flash furnace capacity insufficient for domestic concentrate volumes

- Pyrometallurgical processing requires specialised high-temperature equipment

- Environmental compliance systems limit expansion of existing facilities

- Geographic concentration creates regional processing constraints

Refining Limitations:

- Electrolytic refining facilities operate below optimal throughput

- Electrowinning circuits distributed across limited locations

- Quality control systems require substantial technical expertise

- Power infrastructure demands exceed regional electrical capacity

The fundamental diagnosis identifies refining capacity as the critical constraint throughout the American copper value chain. Raw material availability significantly exceeds processing capacity, creating accumulation of intermediate products that require foreign processing to reach market-ready specifications.

Technical Processing Requirements

Modern copper smelting employs flash furnace technology operating at temperatures exceeding 1,200°C with oxygen-enriched air injection systems. These installations require sophisticated refractory materials, automated process control, and comprehensive off-gas handling systems that capture sulfur dioxide for sulfuric acid production.

Electrorefining installations utilise large tank houses containing multiple electrolytic cells, specialised power rectification equipment, and electrolyte circulation systems. The process dissolves impure copper anodes through electrical current, depositing 99.99 percent pure copper cathodes suitable for electrical and electronic applications.

Electrowinning directly produces refined cathode from heap-leached or vat-leached copper solutions, bypassing smelting requirements. This process works effectively with lower-grade ore deposits but demands substantial electrical infrastructure comparable to electrorefining operations.

Regional Distribution of Processing Centres

American copper processing infrastructure concentrates primarily in the Southwest region, creating both operational efficiencies and systemic vulnerabilities. The Kennecott Utah Copper integrated complex, operated by Rio Tinto, produces 169,300 tonnes of annual copper output with integrated smelting and refining capacity, representing one of the few vertically integrated operations in North America.

Arizona operations by Freeport-McMoRan include multiple processing facilities, with the Sierrita electrowinning plant maintaining 22,680 tonnes of annual cathode capacity. The Sierrita concentrator processes 100,000 metric tons of ore daily, representing world-class concentrator efficiency through sophisticated grinding, flotation, and concentrate thickening systems.

Major Processing Facilities

Integrated Operations:

- Kennecott Utah Copper: Mining-smelting-refining integration minimises concentrate exports

- Morenci Complex: 399,100 tonnes annual production requiring external refining

- Twin Buttes Facility: 50 million pounds refined cathode annually

- Sierrita Operations: Concentrator and electrowinning integrated processing

Geographic Concentration Implications:

- Supply chain integration reduces transportation between mining and refining

- Regional clustering enables shared infrastructure and technical expertise

- Concentration creates vulnerability to regional disruptions

- Limited geographic redundancy constrains system resilience

The Kennecott operation demonstrates the operational advantages of vertical integration, processing virtually all produced concentrate domestically rather than exporting for foreign refining. This integrated model reduces dependence on external refiners while maintaining control over quality specifications and delivery schedules.

However, the geographic concentration of processing facilities in specific regions means that mining operations in other areas cannot access nearby refining infrastructure, necessitating long-distance concentrate transportation or export to foreign facilities.

Economic Drivers of Concentrate Export Patterns

The substantial export of American copper concentrate reflects structural capacity limitations rather than economic optimisation. The 48 percent export rate occurs by necessity, not choice, as domestic processing infrastructure cannot handle the full volume of concentrate production from mining operations.

This export pattern creates multiple inefficiencies throughout the supply chain. Concentrate travels overseas for processing, undergoes smelting and refining in foreign facilities, and potentially returns as refined cathode through separate transportation cycles. Each stage involves additional costs, currency exposure, and extended lead times compared to domestic processing.

Processing Economics Analysis

Cost Structure Components:

- Transportation expenses for concentrate export and cathode import

- Currency exchange exposure throughout multiple transaction cycles

- Extended inventory holding periods during international processing

- Quality control challenges with foreign processing specifications

Capital Investment Barriers:

- Smelter construction requires $800 million to $1.2 billion investment

- Development timelines extend 4-6 years for operational facilities

- Environmental compliance systems demand substantial additional capital

- Permitting and regulatory approval processes create timeline uncertainty

The decision to export concentrate rather than expand domestic processing reflects these substantial capital barriers combined with regulatory complexity. However, the economic analysis must consider long-term supply chain security and the strategic implications of foreign processing dependency.

China's dominance in copper refining creates asymmetric relationships where American producers depend on Chinese refiners for finished product conversion. This dependency means that refined cathode supply to North American manufacturers depends partly on Chinese refiner capacity allocation and processing priorities.

Infrastructure Expansion Requirements and Investment Analysis

Expanding American copper refining capacity in the US demands coordinated investment across multiple infrastructure categories, requiring $1.55 billion to $2.5 billion in total capital expenditure before considering financing costs and contingency expenses.

Investment Categories and Timelines

| Infrastructure Type | Capital Requirement | Development Timeline | Capacity Addition |

|---|---|---|---|

| Smelter Expansion | $800M – $1.2B | 4-6 years | 200,000-300,000 tonnes |

| Refinery Development | $400M – $600M | 3-4 years | 150,000-250,000 tonnes |

| Infrastructure Support | $200M – $400M | 2-3 years | Logistics and utilities |

| Environmental Systems | $150M – $300M | Concurrent | Compliance infrastructure |

These capital requirements contrast with current underutilisation challenges, where existing facilities operate below nameplate capacity due to various operational constraints. Adding substantial new capacity requires not merely financial commitment but sustained policy certainty supporting long-term operational economics.

Technical Specifications for Modern Facilities

Flash Furnace Smelting Technology:

- Oxygen-enriched air injection systems for rapid oxidation reactions

- Sophisticated refractory materials withstanding extreme temperatures

- Automated process control managing thermal profiles and feed rates

- Comprehensive off-gas handling capturing SO₂ for acid production

Electrorefining Infrastructure:

- Large tank houses containing multiple electrolytic refining cells

- Specialised power rectification converting AC to DC current

- Electrolyte circulation and purification maintaining solution quality

- Anode slime processing recovering precious metal byproducts

Modern installations achieve energy efficiency through optimised circuit design and voltage control, though electrorefining remains electrically intensive. Power infrastructure requirements often determine facility location and expansion feasibility.

Industry analysts emphasise that effective capacity expansion must address the constellation of constraints simultaneously: financing mechanisms, permitting acceleration, technological selection, environmental compliance frameworks, labour availability, and regional utility infrastructure. Addressing individual constraints without resolving systemic bottlenecks creates implementation challenges where some components remain limited.

Secondary Copper Processing and Scrap Integration

Secondary copper recovery through scrap processing represents a significant opportunity for expanding effective refining capacity without requiring new mining operations. The United States generates substantial copper scrap volumes from infrastructure replacement, electronic waste, and industrial processes that currently face processing limitations.

Current scrap processing infrastructure includes 3 operational secondary fire refineries that upgrade copper scrap through pyrometallurgical processes. These facilities sort, prepare, and process various scrap grades to produce refined copper suitable for manufacturing applications.

Scrap Processing Opportunities

Urban Mining Potential:

- Electronic waste containing high-grade copper components

- Infrastructure replacement generating substantial scrap volumes

- Industrial process waste requiring quality upgrading

- Construction and demolition copper recovery

Processing Technology Improvements:

- Advanced sorting systems separating copper from mixed materials

- Improved purification processes for secondary copper

- Enhanced collection and transportation logistics

- Quality control systems ensuring specification compliance

Scrap processing requires different technical approaches compared to concentrate processing, but offers shorter development timelines and lower capital requirements for capacity expansion. Secondary refineries can process materials that bypass smelting requirements, providing more direct pathways to refined copper production.

The integration of scrap processing with primary refining operations creates operational synergies through shared infrastructure, technical expertise, and distribution networks. This integration approach may provide more economically viable expansion pathways than developing entirely separate processing facilities.

The next major ASX story will hit our subscribers first

Strategic Supply Chain Security Implications

The structural mismatch between American copper mining capacity and refining infrastructure creates significant supply chain vulnerabilities despite apparent resource abundance. Current export patterns place refined copper supply partly under foreign control, creating dependencies that extend beyond simple market transactions.

Vulnerability Assessment Framework

Geopolitical Risk Factors:

- Concentration of refining capacity in specific countries

- Transportation costs for multiple international shipping cycles

- Quality control limitations with foreign processing operations

- Currency exposure throughout extended supply chains

Strategic Mitigation Approaches:

- Targeted domestic capacity expansion addressing specific bottlenecks

- Technology upgrading for existing processing equipment

- Geographic diversification of processing capabilities

- Public-private partnerships supporting infrastructure development

The experience of other major copper producers demonstrates alternative supply chain configurations. Chile and Peru maintain domestic refining capacity proportional to mining production, minimising concentrate exports while ensuring access to refined products for domestic industries.

However, the American situation requires different strategic approaches due to the established industrial base, existing infrastructure constraints, and regulatory environment. Effective mitigation strategies must work within these constraints while gradually expanding processing capabilities.

Investment Policy Considerations:

Specialists suggest that policy initiatives focused on acquiring foreign mining assets may provide less supply chain security than expanding domestic refining capacity. Mining asset ownership does not ensure that concentrate flows to American refiners unless corresponding processing infrastructure exists to handle the materials.

The strategic logic emphasises that controlling downstream processing capabilities provides greater supply chain security than controlling upstream mining operations, particularly when domestic mining already generates surplus concentrate volumes requiring foreign processing.

Future Capacity Planning and Market Dynamics

The global copper market faces substantial supply constraints that will intensify pressure on processing infrastructure worldwide. Industry projections indicate requirements for 61 new copper mines by 2030 with associated investment of approximately $285 billion to meet growing demand.

This supply pressure will likely increase competition for available refining capacity, potentially creating advantages for nations with integrated mining-refining operations. Countries dependent on foreign processing may face allocation challenges when global refining capacity becomes constrained.

Market Development Trends

Demand Growth Drivers:

- Electrification infrastructure requiring substantial copper inputs

- Data centres and 5G networks increasing industrial copper consumption

- Renewable energy systems demanding high-quality copper components

- Electric vehicle production scaling rapidly across multiple regions

Processing Technology Evolution:

- Energy-efficient smelting and refining technologies

- Automated process control reducing operational complexity

- Environmental compliance systems enabling expansion

- Modular facility designs reducing capital requirements

Recent market developments demonstrate the financial impact of supply constraints, with London copper prices increasing approximately 40 percent since October and reaching record levels exceeding $14,000 per tonne during periods of supply disruption.

Long-term Demand Projections:

Major mining companies project substantial demand growth, with BHP estimating 70 percent increased global copper demand by 2050 driven by electrification, emerging technologies, and decarbonisation initiatives. Digital sector expansion through artificial intelligence, expanded data processing, and advanced telecommunications will likely contribute additional demand growth.

These demand projections suggest that nations with integrated copper processing capabilities will maintain strategic advantages in supply security and industrial competitiveness. Countries dependent on foreign processing may face increasing challenges securing refined copper supplies during periods of global supply constraints.

The American copper industry faces a critical decision point: continue dependence on foreign processing with associated vulnerabilities, or invest in domestic refining capacity expansion that provides long-term supply security despite substantial capital requirements and extended development timelines. Consequently, implementing effective copper investment strategies becomes essential for navigating these complex market dynamics.

Furthermore, the broader mining industry evolution continues to reshape processing technologies and operational approaches. Additionally, potential policy changes could create global market impacts that affect copper processing economics and investment decisions.

How Does Processing Infrastructure Affect Supply Security?

Processing infrastructure fundamentally determines whether nations can transform their raw copper resources into usable industrial inputs. According to a comprehensive analysis by the World Resources Institute, the United States faces a strategic contradiction between abundant copper resources and insufficient processing capacity.

This mismatch creates supply chain vulnerabilities where resource-rich nations become dependent on foreign refiners. The structural challenge extends beyond simple economics to encompass strategic supply security and industrial competitiveness.

Processing capacity constraints limit the nation's ability to respond to supply disruptions or market volatility. When global refining capacity becomes constrained, nations without domestic processing capabilities face potential allocation challenges that could affect manufacturing sectors.

What Investment Approaches Support Capacity Expansion?

Expanding copper refining capacity in the US requires coordinated investment strategies addressing multiple infrastructure components simultaneously. The U.S. Geological Survey's mineral commodity summaries highlight the complex technical requirements for modern processing facilities.

Investment approaches must consider both primary processing expansion and secondary copper recovery enhancement. Scrap processing offers shorter development timelines and lower capital requirements compared to new smelter construction, potentially providing interim capacity increases while major facilities undergo development.

Public-private partnerships may provide mechanisms for sharing development costs and risks while ensuring long-term operational viability. These partnerships can combine private sector technical expertise with public sector strategic interests in supply security.

Conclusion: Transforming Raw Material Abundance Into Industrial Advantage

The United States possesses abundant copper resources through both mining operations and scrap recovery, yet cannot effectively utilise these materials due to insufficient processing infrastructure. This fundamental mismatch creates supply chain vulnerabilities and economic inefficiencies that prevent the nation from capturing the full value of its copper resources.

Addressing copper refining capacity in the US requires coordinated investment across smelting, refining, and supporting infrastructure, demanding $1.55 billion to $2.5 billion in capital expenditure with development timelines extending 4-6 years for major facilities. However, these investments would provide long-term supply security while reducing dependence on foreign processing operations.

The strategic importance of integrated processing capabilities will likely increase as global copper demand grows 70 percent by 2050 and supply constraints intensify worldwide. Nations with domestic processing capacity will maintain advantages in supply security, quality control, and industrial competitiveness that extend beyond simple resource ownership.

Success in expanding American copper processing infrastructure requires addressing multiple constraints simultaneously: financial mechanisms, regulatory frameworks, technological selection, environmental compliance, and utility infrastructure. Coordinated policy support and private investment can transform the nation's raw material abundance into sustained industrial advantage.

Investment Disclaimer: This analysis presents general market information and should not be considered investment advice. Copper markets involve substantial price volatility, regulatory uncertainty, and operational risks that may significantly impact investment returns. Readers should conduct independent research and consult qualified financial advisors before making investment decisions related to copper processing, mining operations, or related industrial sectors.

Looking to Capitalise on America's Copper Processing Revolution?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant copper and mineral discoveries across the ASX, empowering subscribers to identify actionable opportunities ahead of the broader market. Begin your 14-day free trial today and position yourself to profit from the next major discovery in copper and critical minerals sectors.