June 11, 2026

The Electrification Imperative and Why One Metal Sits at Its Centre

Every major energy transition in history has been defined by a bottleneck material. The industrial revolution ran on steel. The petrochemical age ran on oil. The transition now underway, spanning electric vehicles, utility-scale solar and wind, and the wholesale rewiring of national electricity grids, runs on copper. No other conductor combines the electrical performance, thermal tolerance, mechanical workability, and cost profile that copper delivers at industrial scale. Aluminium substitutes in some overhead line applications, but for motors, inverters, transformers, and charging infrastructure, copper remains the engineering default. This physical reality sits beneath every investment thesis, every geopolitical manoeuvre, and every permitting battle currently unfolding across Latin America — the region that holds the world's densest concentration of copper in the ground, making the race for copper in Latin America one of the defining resource contests of this decade.

When big ASX news breaks, our subscribers know first

A Supply-Demand Imbalance That Cannot Be Papered Over

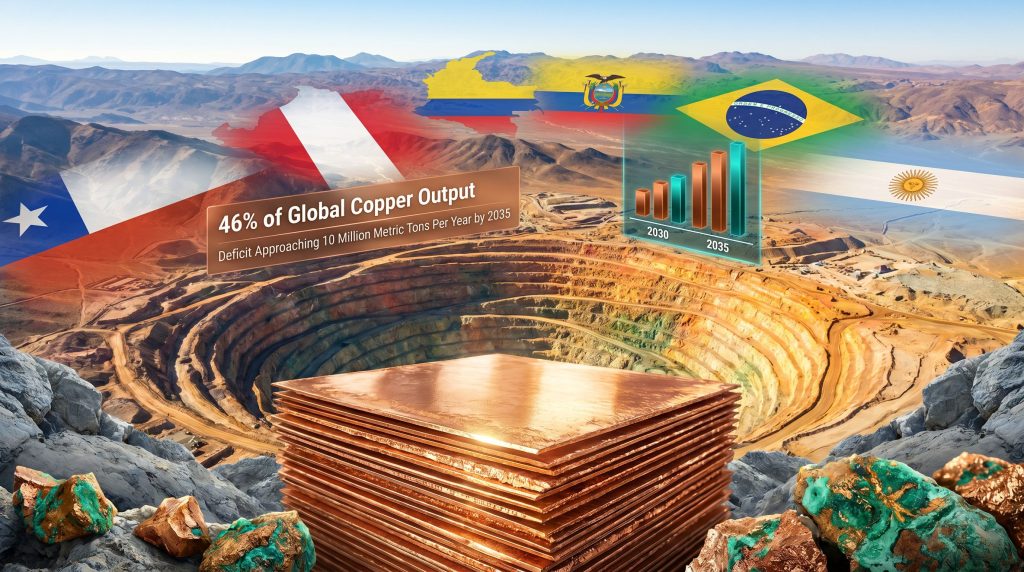

The numbers describing the coming copper shortfall are stark enough to command serious attention. Analysts tracking the intersection of energy transition demand and mine supply project that the global copper deficit could approach 10 million metric tons per year by 2035, with demand beginning to outpace available supply as early as 2030. To contextualise that figure: total global refined copper consumption currently sits at roughly 26 to 28 million metric tons annually. A deficit of the magnitude projected would therefore represent something approaching one-third of current total output — an extraordinary structural gap by any historical standard.

What makes this shortage different from previous commodity cycles is that demand is not being driven by a single geography or industry segment. A single electric vehicle contains roughly four times more copper than a conventional internal combustion engine vehicle. Offshore wind installations require approximately ten times more copper per megawatt than gas-fired power plants. Furthermore, grid modernisation programmes across Europe, North America, and Asia are committing to infrastructure replacement cycles that will sustain elevated copper demand for decades, not years.

The supply side faces an equally structural problem. Average copper ore grades at operating mines have declined consistently over several decades. Where mines once processed ore grading above 1% copper, many large-scale operations today work material at 0.5% or below. This grade decline means operators must move and process progressively larger volumes of rock to produce the same quantity of metal, compounding capital intensity, water consumption, and energy costs simultaneously.

New discoveries capable of replacing depleted reserves are taking longer to find, longer to permit, and longer to build than at any previous point in the industry's history. Lead times from discovery to first production now routinely exceed 15 to 20 years. The copper supply crunch is, consequently, a structural rather than cyclical phenomenon.

Latin America's Irreplaceable Position in Global Copper Supply

Against this backdrop, the race for copper in Latin America takes on a significance that extends well beyond regional investment dynamics. Latin America accounts for approximately 46% of global raw copper mining output, a concentration with no parallel in any other critical mineral. Chile alone produces roughly 27% of the world's mined copper and hosts the largest known copper reserves of any nation. Peru contributes approximately 10% of global supply and holds the second-largest reserve base. Together, these two countries account for close to 35% of global production and roughly 30% of the world's identified copper reserves.

Chile's dependence on the metal is equally striking from an economic governance perspective. Copper contributes approximately half of Chile's total national export revenue, making it not merely an industrial commodity but a foundational pillar of sovereign fiscal capacity. The state-owned enterprise Codelco remains the world's largest single copper producer, though its output has declined from peak levels as its flagship deposits at Chuquicamata, El Teniente, and Escondida age and require increasingly expensive underground development.

Country-by-Country Production Snapshot

| Country | Global Production Share | Reserve Significance | Investment Status |

|---|---|---|---|

| Chile | ~27% | Largest global reserves | Established, expanding |

| Peru | ~10% | Second-largest reserves | Active, social complexity |

| Colombia | Emerging | Underexplored porphyry belts | Early-stage attraction |

| Ecuador | Emerging | Active project pipeline | Regulatory transition |

| Brazil | Growing | Significant underdeveloped deposits | Increasing foreign interest |

| Argentina | Growing | Copper-gold porphyry belt | Rising exploration activity |

The Geopolitical Contest Reshaping the Region

Understanding the race for copper in Latin America requires acknowledging that the competition is not merely commercial. It is geopolitical in its structure and strategic in its consequences. China currently purchases a disproportionately large share of Latin American copper exports and controls an estimated 40% or more of global copper refining capacity. Beijing's vertical integration across the copper value chain — from ore procurement through smelting, refining, and downstream manufacturing into cables, motors, and electronics — gives it a structural advantage that purely market-driven Western competitors have struggled to replicate.

The United States has recognised this asymmetry and is actively working to build stronger mineral supply relationships across the Western Hemisphere. Geographic proximity, existing trade frameworks, and shared infrastructure corridors make Latin America a natural partner in efforts to reduce dependence on Chinese-controlled mineral processing. Bilateral resource diplomacy has accelerated across the region, with Washington increasingly framing copper access as a matter of industrial security rather than simply commodity procurement. For a broader view of Latin America's mineral boom, the scale of this contest is difficult to overstate.

The Value Chain Problem: Who Captures the Wealth?

Latin America overwhelmingly exports raw copper ore and concentrate rather than refined cathode or fabricated copper products. The highest-margin processing stages occur primarily in China, meaning the region generates the physical extraction risk and environmental footprint while a disproportionate share of economic value is captured elsewhere in the supply chain.

This value chain asymmetry is increasingly a subject of industrial policy debate across Chile, Peru, and Ecuador. Domestic refining capacity, copper wire manufacturing, and export tariff structures on unprocessed ore are all being discussed as mechanisms for retaining more economic value within producing countries. Whether these discussions translate into implemented policy — and how quickly — will significantly influence the investment calculus for multinational mining companies operating in the region.

Beyond Chile and Peru: The Emerging Copper Frontier

As established deposits in Chile and Peru face declining ore grades, extended permitting timelines, and intensifying social opposition, exploration capital is diversifying toward less-developed jurisdictions across the continent. Each emerging producer presents a distinct combination of geological promise and investment risk.

-

Colombia hosts largely underexplored copper-gold porphyry belts with geological characteristics comparable to productive systems in Peru and Chile. The country's regulatory environment, however, has historically been less predictable for large-scale mining investment, creating uncertainty around project advancement timelines.

-

Ecuador has developed a more active project pipeline in recent years, though tension between resource development objectives and environmental governance frameworks continues to shape investor confidence. The Mirador and Fruta del Norte projects have demonstrated that large-scale mining is achievable in the country, while also illustrating the complexity of the social licence process.

-

Brazil holds significant copper deposits in the Amazon corridor, but remote location, limited transport infrastructure, and water management challenges in environmentally sensitive zones compress project economics meaningfully. The scale of potential endowment nonetheless sustains foreign investment interest.

-

Argentina is attracting renewed attention for its copper-gold porphyry systems in the Andean corridor, particularly as broader economic reforms have improved the country's perceived investment environment. Currency risk and historical sovereign policy volatility remain considerations for long-term capital allocation.

-

Panama offers a cautionary data point. The forced closure of the Cobre Panama mine in 2023 following large-scale public protests and a Supreme Court ruling illustrated how rapidly community opposition and legal risk can intersect to terminate even operating, world-class assets. The ongoing Panama copper mine dispute continues to serve as a reference point for investors assessing jurisdiction risk across the region.

What Makes a Jurisdiction Attractive for Copper Investment?

Mining capital allocators consistently weight several factors when evaluating Latin American copper opportunities:

-

Permitting timeline predictability — Projects in jurisdictions where environmental review processes are transparent and bounded by clear timelines attract premium valuations relative to those in systems prone to indefinite delay or political interference.

-

Water access and altitude — Many Andean copper deposits sit above 4,000 metres elevation in water-stressed catchment areas. Water rights, desalination logistics, and community water-sharing frameworks can be as determinative of project feasibility as ore grade.

-

Infrastructure proximity — Port access, road quality, and power grid connectivity are significant cost variables for remote deposits. Projects within reasonable distance of established infrastructure corridors carry materially lower development capital requirements.

-

Social licence durability — Indigenous consultation frameworks, community benefit-sharing structures, and environmental monitoring commitments are no longer peripheral considerations. They are central to whether a project advances or stalls at any stage of its development.

Structural Barriers That Cannot Be Ignored

The optimistic narrative around Latin American copper supply growth runs directly into a set of structural constraints that have proven durable across multiple commodity cycles. Community-led opposition to copper projects across Peru, Chile, Ecuador, and Panama has become more frequent and more sophisticated, not less. Civil society organisations now engage environmental impact assessment processes with technical expertise that was absent a decade ago, extending review timelines and raising the evidentiary bar for project approvals.

The capital intensity of new copper development has also increased dramatically. Large-scale greenfield projects in remote Andean or Amazonian environments now routinely require multi-billion dollar upfront investments before a single tonne of copper is produced. The shift toward lower-grade, higher-volume deposits amplifies this dynamic, as processing more rock per unit of metal requires proportionally larger mills, more water, more energy, and more tailings storage capacity.

Critical Consideration: Several Latin American governments simultaneously frame copper development as an economic priority while maintaining permitting environments that routinely extend project timelines by years beyond initial estimates. Resolving this contradiction between resource nationalism, environmental protection, and investment attraction is arguably the central policy challenge of the regional copper race.

The next major ASX story will hit our subscribers first

How Mining Companies Are Responding

The strategic response from the mining industry has been multidimensional. Mergers, acquisitions, and copper partnerships targeting Latin American copper assets have accelerated sharply as majors and mid-tier producers seek to replenish reserve bases depleted by years of underinvestment in exploration. Elevated copper prices have simultaneously improved project economics, unlocking previously marginal deposits that did not meet return thresholds at lower price points.

Streaming and royalty companies have expanded their financing role in early-stage Latin American copper exploration, providing capital to junior companies in exchange for long-term metal purchase agreements. This structure allows juniors to advance projects without immediate dilutive equity raises while giving royalty holders leveraged exposure to copper price upside. For context on the broader copper price drivers shaping these decisions, macroeconomic and energy transition forces remain the dominant tailwinds.

On the technology side, advances in geophysical survey methods, AI-assisted geological modelling, and deep drilling programmes are accelerating the identification of new copper systems in underexplored jurisdictions. Airborne electromagnetic and gravity surveys now allow geologists to develop detailed subsurface models of prospective porphyry targets before a single drill hole is completed, significantly reducing the cost and time associated with early-stage target generation. Some of the largest copper mines in operation today were identified using predecessor versions of these same technologies.

Three Scenarios for Latin American Copper Supply

Scenario 1: Accelerated Development

Regulatory reform, improved social licence frameworks, and sustained strong copper prices combine to unlock a meaningful pipeline of new project approvals across Chile, Peru, Ecuador, and Colombia. Latin America increases its share of global refined copper output, capturing progressively more value domestically and reducing the region's dependence on Chinese processing infrastructure.

Scenario 2: Incremental Growth with Persistent Constraints

Existing operations expand modestly, a small number of new projects reach production over the forecast period, but structural barriers — including community opposition, permitting delays, and grade decline at mature mines — limit the pace of supply growth. The copper deficit widens gradually, sustaining elevated prices but falling short of meeting the full scale of energy transition demand.

Scenario 3: Supply Disruption

Escalating social conflicts, adverse regulatory rulings, or coordinated environmental enforcement actions curtail production across multiple jurisdictions simultaneously. The global copper deficit accelerates sharply, triggering a price spike and forcing downstream manufacturers to accelerate substitution research and secondary recovery programmes.

Disclaimer: The above scenarios represent analytical frameworks for thinking about supply risk and should not be construed as investment advice or precise forecasts. Copper markets are influenced by a wide range of variables, and actual outcomes may differ materially from any scenario described.

Frequently Asked Questions: The Race for Copper in Latin America

Why is Latin America so important to global copper supply?

Latin America mines approximately 46% of the world's copper, with Chile and Peru alone accounting for around 35% of global production and holding close to 30% of identified global reserves. No other region comes close to matching this concentration of copper endowment, making Latin American supply continuity a global economic variable.

Which countries are the top copper producers in Latin America?

Chile ranks first globally in copper production, Peru ranks second globally, followed by emerging producers including Brazil, Argentina, Ecuador, and Colombia — each at earlier stages of development but attracting increasing exploration and project capital.

What is causing the global copper deficit?

Demand acceleration from electric vehicles, renewable energy installations, and electricity grid expansion is outpacing the rate at which new mines can be discovered, permitted, financed, and built. Analysts project this gap could reach 10 million metric tons annually by 2035, compounded by declining ore grades at existing operations.

Why does China hold such a strong position in Latin American copper trade?

China controls a dominant share of global copper refining capacity and has built a vertically integrated supply chain spanning procurement, smelting, refining, and downstream manufacturing. Long-term offtake agreements, state-backed financing, and proximity to Asian processing infrastructure give Chinese buyers structural advantages that Western competitors are working to close. An in-depth analysis of copper in Latin America further illustrates how deeply embedded these trade relationships have become.

What risks do investors face in Latin American copper projects?

Key risk categories include social licence failures, permitting delays, resource nationalism, water scarcity at altitude, political instability driven by election cycle volatility, currency exposure, and the capital intensity of large-scale remote development.

How can Latin American countries capture more value from copper resources?

Policy pathways under active discussion include domestic refinery investment, downstream manufacturing incentives, export tariff structures applied to raw ore and concentrate, and the development of regional processing hubs that retain higher-margin production stages within producing economies.

Key Takeaways

-

Latin America holds an irreplaceable position in the global copper supply chain, but translating extraordinary geological endowment into sustained economic advantage requires resolving deep structural tensions between investment attraction, social equity, and environmental governance.

-

The race for copper in Latin America is simultaneously a contest for extraction volume, refining control, and long-term supply security — with China currently holding the strongest integrated position and the United States actively working to build alternative supply relationships.

-

Countries beyond Chile and Peru represent the next frontier of copper development, but each presents a distinct and meaningful combination of geological promise and investment risk that demands careful jurisdiction-level analysis.

-

Ore grade decline at mature operations is a systemic challenge that will only intensify over the coming decade, increasing the urgency of discovering and developing next-generation deposits.

-

The ultimate beneficiaries of the Latin American copper race will be those who solve the value chain problem — building the processing and manufacturing infrastructure that transforms producing nations from raw material exporters into integrated copper economies capable of capturing the full value embedded in their geological inheritance.

For ongoing coverage of Latin American mining investment, project pipelines, and industry developments, BNamericas provides detailed reporting and intelligence across the region's mining and metals sector at bnamericas.com.

Want to Know Which ASX Copper Stocks Could Benefit From the Global Supply Crunch?

Discovery Alert's proprietary Discovery IQ model instantly scans ASX announcements to identify significant mineral discoveries — including copper — delivering real-time alerts that allow investors to act ahead of the broader market. Explore historic discovery returns on Discovery Alert's dedicated discoveries page to understand the scale of opportunity, then begin your 14-day free trial to position yourself at the forefront of the next major find.