May 13, 2026

When Grade Becomes the Only Argument That Matters

Junior mining companies have historically fallen into a predictable trap: chasing portfolio breadth as a proxy for stability, only to discover that spreading thin capital across multiple low-grade operations amplifies risk rather than containing it. The economics of copper processing are unforgiving in this regard. When feed grades drop, recoveries deteriorate, processing costs per unit of output climb, and the margin between revenue and breakeven narrows to a point where no amount of throughput volume can rescue the business model.

This is the precise dynamic that makes the Copper 360 restructure to focus on Rietberg mine such a strategically significant event, not just for shareholders in a single JSE-listed small-cap, but for anyone watching the slow reawakening of South African copper production after four decades of dormancy. The decision to abandon surface and waste resource operations entirely in favour of a single underground asset is a grade-driven confession: that in copper mining, quality ultimately defeats quantity every time. Understanding the broader copper supply crunch helps contextualise why this pivot carries such weight at this particular moment in the commodity cycle.

When big ASX news breaks, our subscribers know first

South Africa's Copper Sector: A 42-Year Production Gap and Why It Ends Here

The O'Kiep Copper District: Historical Scale, Forgotten Potential

Few mineral districts in Southern Africa carry the historical weight of the O'Kiep Copper District in the Northern Cape. Copper extraction here stretches back to the 1930s, and at its peak the district supported a network of 12 separate mining operations spread across a 19,000-hectare land package. Then, progressively through the 1970s and into the early 1980s, production wound down. By 1983, the last underground operations had gone silent.

What followed was approximately 42 years during which one of Africa's most historically productive copper districts contributed nothing to global supply. The reasons were primarily economic: copper prices through much of the late 20th century did not justify the capital required to sustain or expand operations in a geologically complex, labour-intensive underground environment.

The transformation in copper's demand fundamentals over the past decade has, however, changed that calculus entirely. The metal sits at the intersection of almost every major infrastructure buildout currently underway globally:

- Electric vehicle manufacturing requires roughly three to four times more copper per vehicle than a conventional internal combustion engine car

- Renewable energy infrastructure, including wind turbines and solar installations, is copper-intensive at both the generation and transmission stages

- Data centre expansion linked to artificial intelligence computing demands has emerged as a newer, rapidly growing source of copper consumption

- Grid modernisation programmes across developed and developing markets require extensive copper wiring upgrades

Against this backdrop, BHP has publicly identified copper's AI-linked demand profile as a primary driver attracting new institutional investors to the sector, according to reporting by MiningMX in May 2026. That macro signal matters for a district like O'Kiep, where historical resource estimates suggest contained copper of between 140,000 and 750,000 tonnes across the broader land package. For investors assessing these dynamics, the copper price growth drivers underpinning the sector shift are worth examining carefully.

Copper 360's Position as South Africa's Sole Listed Copper Producer

Copper 360 (JSE AltX: CPR) holds a genuinely unique position in the South African mining investment landscape. It is the only listed copper producer on the JSE, making it the singular investable vehicle for domestic and international investors seeking pure-play exposure to South African copper production. The company was founded by the late Jan Nelson to unlock value from the Northern Cape assets, and at the time of its listing, Coronation Asset Management participated as an anchor institutional investor, lending early-stage credibility to the investment thesis.

That thesis was compelling on paper: a decades-long production vacuum, a large historical resource base, rising global copper demand, and a company with the rights to one of Africa's most historically significant copper districts. Converting that thesis into operational reality proved considerably harder.

The Anatomy of Operational Failure: What Went Wrong Before the Restructure

A Pattern of Underdelivery From the Start

From its first full financial year of operations, Copper 360 failed to meet the production targets it had outlined ahead of its market listing, according to reporting by David McKay in MiningMX, published May 11, 2026. The shortfall was not marginal. The gap between projected and delivered output created compounding pressure on cash reserves and eroded investor confidence at a rate that the company's geological assets alone could not offset.

The fundamental problem with surface and waste resource processing, which formed the operational backbone of Copper 360's early activities, is one of grade economics. Lower-grade material demands higher throughput volumes to generate equivalent copper output. Higher throughput demands more energy, more reagents, more labour, and more processing time. When those inputs are being funded from a constrained cash base in a company still proving its operational model, the arithmetic becomes unworkable quickly.

Leadership Instability and the Board Intervention

Copper 360's operational difficulties were compounded by significant leadership instability. CEO Graham Briggs, who was appointed specifically in 2025 to stabilise and revitalise the business, departed in February of that year alongside CFO Stephan Du Plessis, a former Deutsche Bank executive. Both were described by the company as taking a leave of absence with immediate effect, an unusual characterisation that MiningMX, citing its sister publication Currency, reported as reflecting a boardroom coup rather than a routine management transition.

Chief Operations Officer Gordon Thompson stepped into an acting CEO capacity following the departures. The subsequent appointment of CEO Shirley Hayes refocused the executive team on the Rietberg ramp-up and cost reduction as the twin priorities for stabilisation.

The board's response to this accumulated pressure was a holistic review conducted in conjunction with external mining and technical advisers. Chairman Rupert Smith described the conclusion of that review as determining that restructuring was a necessary and decisive step to preserve capital and reposition the company toward a sustainable operating model, as reported by Mining Weekly on May 12, 2026. The announcement arrived just as the Johannesburg market closed, with shares falling approximately 1.7% on the day and sitting roughly 15% lower year-to-date at the time of the announcement.

The timing of the announcement, released as markets closed rather than during active trading hours, is a common practice for potentially market-sensitive corporate actions. It allows institutional investors to assess the implications before the next open rather than reacting in real time with incomplete information.

Rietberg Underground Mine: The Geological Case for a Company-Wide Pivot

A Resource That Transformed Between 2022 and 2024

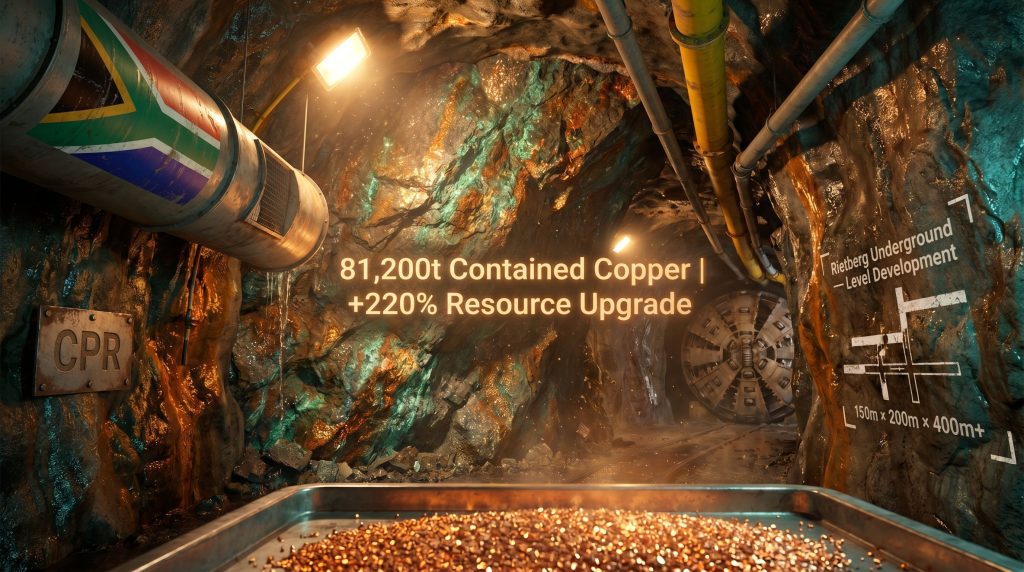

The most important single development underpinning the Copper 360 restructure to focus on Rietberg mine is a resource upgrade that fundamentally changed the deposit's investment profile. The mineral resource estimate increased by 220% between the 2022 baseline and the 2024 upgraded estimate, as detailed in the company's technical disclosures.

| Metric | 2022 Baseline | 2024 Upgraded Estimate | Change |

|---|---|---|---|

| Total Contained Copper (Mineral Resource) | 25,275 tonnes | 81,200 tonnes | +220% |

| Measured and Indicated Category | Not reported | 60,800 tonnes | n/a |

| Average Grade (Measured/Indicated) | Not reported | 1.27% Cu across 4.78 Mt | n/a |

| High-Grade Zone Grades | Not reported | 2.5% to 3.5% Cu | n/a |

| High-Grade Zone Dimensions | Not reported | 150m x 200m x 400m+ | Open at depth |

A resource upgrade of this magnitude carries significant implications that extend beyond simple headline numbers. The reclassification of 60,800 tonnes into the measured and indicated categories, the two highest-confidence resource classifications under standard reporting frameworks, means that a substantial portion of the total resource has been defined with sufficient geological data density to support preliminary economic analysis. Furthermore, understanding the nuances of interpreting drill results is essential for investors seeking to evaluate what these figures truly represent.

Understanding What "Open at Depth" Means for Investors

The deposit's description as remaining open at depth is a technical statement with meaningful investor implications that are not always well understood outside specialist geological circles.

When a mineral resource is described as open at depth, it means that drilling has not encountered the geological boundary that terminates the mineralised zone downward. In practical terms, this means the 81,200 tonne total resource figure is a floor estimate rather than a ceiling. Each additional underground development level drilled and sampled has the potential to extend the resource further.

Given that the high-grade zone already extends over 400 metres in its known dimension, and that underground copper deposits in similar geological settings have been mined to depths exceeding 1,000 metres at other operations globally, the depth extension potential is a legitimate value optionality rather than speculative noise. The role of well-structured drilling programmes guide the process of unlocking this potential systematically.

Grade Economics: Why 2.5% to 3.5% Changes Everything

The distinction between the grades achievable at Rietberg's high-grade zone and the grades being processed through surface and waste operations is not merely academic. It directly determines whether a copper mining operation can survive at prevailing copper prices.

Consider the processing economics in simplified terms:

- At 1.0% copper feed grade, a processing plant must move 100 tonnes of ore to produce one tonne of copper content

- At 2.5% copper feed grade, the same plant needs only 40 tonnes of ore to produce the same copper content

- At 3.5% copper feed grade, that figure drops to approximately 28.5 tonnes

This means that at Rietberg's high-grade zone grades, the plant is handling between 60% and 70% less material per unit of copper produced compared to a 1.0% operation. That reduction flows directly into lower energy costs, lower reagent consumption, lower wear on processing equipment, and lower waste management costs. The operating margin improvement is structural, not cyclical.

The Modular Flotation Plant Advantage

Ore from Rietberg is processed through the Nama Copper Modular Flotation Plant, referred to internally as MFP 2. This processing facility was purpose-designed for the ore characteristics of the O'Kiep district, and its modular architecture carries a strategic advantage that is frequently underappreciated in junior mining company analysis.

Modular flotation plants can be expanded incrementally by adding processing modules rather than requiring entirely new plant construction. This means that as underground development at Rietberg expands accessible ore tonnages, processing capacity can scale in proportion without requiring disproportionate capital commitment. The plant's existence also eliminates the construction timeline risk that typically adds 12 to 36 months and significant capital uncertainty to new mining projects.

The company is also transitioning its product specification from copper plate to copper concentrate. Copper concentrate, a partially processed product containing copper sulphides alongside other minerals, is the standard product form accepted by copper smelters globally. It consequently commands broader market access and pricing transparency than copper plate, which is a less common intermediate product form.

The first underground blast at Rietberg occurred in January 2025, marking the reactivation of a mine that had been silent since 1983. That single event represented a 42-year gap in underground copper production from one of South Africa's most historically significant mining districts.

Three Scenarios for Copper 360 After the Restructure

Scenario 1: Successful Ramp-Up (Base Case)

The company reaches its stated steady-state target of 40,000 to 45,000 tonnes of ore per month at a 1.6% average feed grade through MFP 2 within the four to five month transition window. Cost base aligns with the single-asset operating model. Cash preservation through the transition is sufficient without emergency capital market access.

Under this scenario, Rietberg establishes break-even or positive operating cash flow, which then creates the financial platform from which adjacent prospects, Jubilee and Homeep-East, can be progressively activated. The restructure is validated and the investment case for South Africa's only listed copper producer strengthens considerably.

Scenario 2: Extended Transition Under Capital Pressure (Bear Case)

Underground development encounters geological or infrastructure challenges that extend the ramp-up timeline beyond the stated window. Workforce restructuring costs and statutory consultation obligations consume more available cash than modelled. The company approaches capital markets from a weakened negotiating position, resulting in dilutive equity issuance.

This scenario does not necessarily threaten the viability of Rietberg as a geological asset, but it materially extends the timeline for value realisation and imposes additional shareholder dilution risk. The 15% year-to-date share price decline already partially prices this possibility.

Scenario 3: Resource Growth Accelerates Value Creation (Bull Case)

Continued underground development drilling confirms resource extensions at depth, triggering further mineral resource upgrades beyond the already significant 220% increase achieved in 2024. Copper price strength, driven by sustained AI infrastructure investment, energy transition spending, or supply disruptions elsewhere, improves the revenue outlook materially. Strategic interest from larger producers or royalty finance providers may, furthermore, emerge under these conditions.

Under this scenario, the Copper 360 restructure to focus on Rietberg mine becomes retrospectively recognised as the inflection point at which a distressed small-cap was repositioned as a genuine acquisition or partnership candidate. Investors exploring broader copper investment strategies will find this bull case scenario particularly instructive when benchmarking junior mining pivots of this type.

Disclaimer: The above scenarios are illustrative frameworks for analytical purposes only and do not constitute financial advice or a forecast of future performance. Investors should conduct independent due diligence and consult a licensed financial adviser before making investment decisions.

The Operational Transition: A Phased Execution Framework

Phase 1: Winding Down Surface and Waste Operations

The first phase of the restructure involves the cessation of processing activities across Copper 360's surface and waste resource operations in the Northern Cape. This triggers two parallel processes:

- Statutory labour consultation under South Africa's Labour Relations Act, specifically the provisions governing large-scale retrenchments under Sections 189 and 189A

- Redeployment assessment for operational personnel whose skills are transferable to underground support functions at Rietberg

South African labour law imposes meaningful procedural obligations on employers conducting large-scale restructurings. The consultation process requires genuine engagement with affected employees, recognised trade unions, and workplace forums before any final retrenchment decisions are implemented. Failure to follow this process creates legal exposure that can extend timelines and impose financial costs beyond those modelled in initial restructuring plans.

Phase 2: Accelerated Underground Development

With capital and personnel redirected, the priority becomes expanding underground development headings at Rietberg to increase the volume of accessible ore available for processing. The target is reaching 40,000 to 45,000 tonnes per month of ore delivery to MFP 2, a throughput rate that, at the stated average feed grade of 1.6% copper, would generate meaningful copper output on a monthly basis.

The transition from copper plate to copper concentrate production also occurs during this phase, requiring minor process adjustments and quality control protocols aligned with concentrate market specifications.

Phase 3: Cost Base Realignment and Adjacent Prospect Sequencing

Once Rietberg is operating as the sole production source, total group overhead is realigned to a single-asset model. Non-core expenditures, including exploration spending at the broader O'Kiep district, are suspended until Rietberg generates sufficient cash flow to fund incremental activity.

The adjacent prospects of Jubilee and Homeep-East represent what investors often call optionality value: the potential upside embedded in assets that are not currently contributing to cash flow but whose development becomes feasible once the primary asset is self-funding.

The next major ASX story will hit our subscribers first

Labour, Community, and the Long-Term Employment Argument

The O'Kiep Copper District communities in the Northern Cape have historically depended on copper mining as an economic anchor. Any reduction in employment at surface operations carries localised social consequences that extend well beyond the directly affected workforce, touching supplier businesses, local service economies, and community tax bases.

The strategic argument being made implicitly by the board is that sustainable employment at a viable underground mine is preferable to preserving marginal jobs at surface operations that are consuming capital without generating sufficient returns to ensure long-term survival. That argument is economically defensible but requires clear, genuine communication with affected stakeholders to maintain social licence in a region where mining employment has historical and cultural significance.

How This Restructure Compares With Other Junior Copper Pivots

| Factor | Copper 360 Rietberg Focus | Typical Junior Copper Restructure |

|---|---|---|

| Primary Trigger | Operational underperformance and leadership change | Commodity price downturn or capital exhaustion |

| Strategic Response | Single high-grade asset concentration | Asset sales or merger activity |

| Resource Quality | 220% upgrade; 2.5% to 3.5% Cu high-grade zone | Varies significantly by jurisdiction |

| Processing Infrastructure | Modular flotation plant operational | Often requires greenfield capital expenditure |

| Timeline to Steady State | 4 to 5 months stated target | Typically 12 to 36 months for new builds |

| Depth Extension Potential | Open at depth beyond 400 metres | Varies; often limited in near-surface deposits |

The most significant differentiator separating this restructure from the typical junior miner contraction story is the pre-existing processing infrastructure. Most junior mining companies facing capital pressure at an early production stage must simultaneously manage operational challenges and fund new infrastructure. Copper 360's possession of MFP 2 removes the construction phase entirely, compressing the timeline between strategic decision and production delivery in a way that most comparable situations cannot replicate.

Key Considerations for Investors Monitoring the Rietberg Ramp-Up

For investors following the Copper 360 restructure to focus on Rietberg mine, the following metrics represent the most meaningful indicators of whether the transition is proceeding as stated:

- Monthly ore delivery rate against the 40,000 to 45,000 tonne target is the primary leading indicator of operational progress

- Feed grade achieved at the plant versus the 1.6% average target will determine whether the high-grade zone is being accessed as planned

- Cash reserve levels at each quarterly reporting point will indicate whether the transition timeline is consuming capital at the modelled rate

- Any further resource updates from underground development drilling would signal continued geological delineation of the depth extensions

- Workforce restructuring completion and any associated legal proceedings will clarify the human capital cost of the transition

The 220% mineral resource upgrade from 2022 to 2024 represents a geological validation of Rietberg that the market has not yet fully rewarded, partly because operational delivery has not yet demonstrated that the resource can be extracted economically at scale. If the four to five month transition produces ore delivery rates approaching the stated targets, the geological merit of the deposit may begin to receive more appropriate commercial recognition.

The Copper 360 restructure to focus on Rietberg mine is, at its core, a bet on grade over breadth. Whether that bet pays off depends on execution in the next several months, making the upcoming operational reporting periods among the most consequential in the company's short listed history.

Want to Track the Next Major Copper Discovery Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly transforming complex geological data into actionable investment insights for traders and long-term investors alike. Explore historic mineral discovery returns on Discovery Alert's dedicated discoveries page to understand the scale of opportunity, then begin your 14-day free trial to position yourself ahead of the market.