July 7, 2026

The Hidden Economics of Copper Concentrate Scarcity: Why Trading Houses Are Moving Upstream

Copper concentrate markets are undergoing a quiet but consequential transformation. For decades, the relationship between miners, traders, and smelters operated on relatively predictable terms: mines produced, smelters refined, and trading houses facilitated the movement of material between them. Treatment and refining charges (TC/RCs) served as the financial barometer of this relationship, with positive TC values indicating adequate concentrate supply and smelter leverage over pricing. That equilibrium has now inverted dramatically.

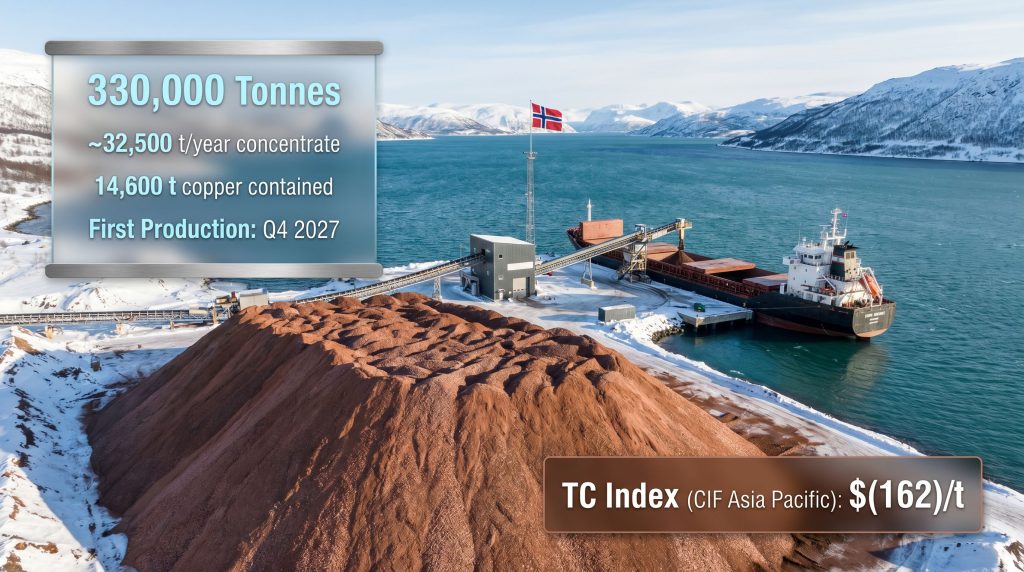

The Fastmarkets copper concentrates TC index, assessed on a cost-insurance-freight (CIF) Asia Pacific basis, stood at $(162) per tonne as of July 3, 2026, deteriorating a further $2.50 per tonne from the prior week's reading of $(159.50) per tonne. Negative TC/RC territory means smelters are not merely accepting lower refining fees — they are effectively paying a premium to secure concentrate feed. This structural inversion is the market backdrop against which the Hartree offtake Nussir copper concentrate agreement must be understood.

For market participants, this price signal communicates something fundamental: clean, high-grade, pre-contracted copper concentrate has become one of the most strategically valuable commodities in the global metals supply chain. Furthermore, the copper supply crunch unfolding across global markets has accelerated this dynamic considerably.

When big ASX news breaks, our subscribers know first

Understanding TC/RC Mechanics: What Negative Treatment Charges Actually Mean

To fully appreciate why the Hartree-Nussir arrangement is commercially significant, it helps to understand what treatment and refining charges represent in practice.

When a mining company sells copper concentrate to a smelter, it does not receive the full value of the contained metal. Instead, the smelter charges a treatment fee (TC, expressed in dollars per dry metric tonne of concentrate) and a refining charge (RC, expressed in cents per pound of contained copper) to compensate for the cost of converting concentrate into refined cathode. Historically, TC/RCs served as a proxy for the balance of power between miners and smelters.

- Positive TC/RCs: Concentrate supply exceeds smelter capacity; smelters have negotiating leverage

- TC/RCs near zero: Market is broadly balanced

- Negative TC/RCs: Smelter capacity exceeds available concentrate; miners gain leverage, and in extreme cases, smelters pay above-market terms to secure feed material

The current deeply negative environment reflects a structural mismatch: significant smelter capacity expansion, particularly in China, has outpaced the growth of new concentrate supply. Major copper ore grades at established mines have declined over decades, and new permitted projects of meaningful scale are rare. This is precisely why a project like Nussir, with its confirmed reserves, completed feasibility study, and clean concentrate profile, attracts serious pre-production capital commitments. Understanding these copper price growth drivers is essential for contextualising just how commercially significant this deal is.

What the Nussir Project Brings to a Concentrate-Starved Market

Resource Characteristics and Metallurgical Quality

The Nussir copper project deposit sits in northern Norway and represents one of the more advanced undeveloped copper projects in the European Arctic. Its resource characteristics place it in a commercially attractive tier for concentrate buyers.

| Attribute | Detail |

|---|---|

| Mining jurisdiction | Northern Norway |

| Average ore grade | 0.81% copper (0.99% copper-equivalent) |

| Reserve classification | Proven and probable |

| Annual concentrate output (full rate) | ~32,500 tonnes at 45% copper grade |

| Contained copper per year | ~14,600 tonnes |

| Life of mine | 13 years |

| Mill throughput | 6,000 tonnes per day (nominal) |

| Gold by-product | ~3,600 oz/year (life-of-mine average) |

| Silver by-product | ~546,000 oz/year (life-of-mine average) |

| Life-of-mine copper equivalent | ~19,000 tonnes per annum |

| Metallurgical recoveries | 96% copper, 84% gold, 95% silver |

The concentrate grade of 45% copper positions Nussir's output at the upper end of typical specifications, where most concentrates globally grade between 25% and 35% copper. Higher-grade concentrates are commercially preferable because they reduce the volume of material that must be physically transported, loaded, and processed per unit of contained metal, thereby lowering logistics costs and smelter handling fees.

Why Concentrate Cleanliness Is a Commercial Differentiator

Beyond grade, the single most commercially sensitive characteristic of copper concentrate in today's smelter market is elemental cleanliness. Penalty elements — including arsenic, bismuth, antimony, lead, mercury, and fluorine — trigger financial deductions that can substantially erode the economics of an otherwise high-grade concentrate parcel.

Industry context: Global smelter penalty thresholds have tightened over the past decade as environmental regulations governing smelter emissions have become stricter, particularly in China and Europe. Concentrates containing arsenic above 0.5% increasingly face outright rejection from certain smelters or punitive deductions that can render the material uneconomic to process.

The Nussir concentrate has been characterised as containing negligible levels of deleterious elements. This is a commercially meaningful claim, though it is worth noting that detailed independent assay verification of specific elemental concentrations — including arsenic, lead, zinc, mercury, bismuth, and antimony — has not been publicly released. Smelter acceptance and final commercial terms will ultimately depend on independently verified parcel specifications when production commences.

The Architecture of the Hartree-Blue Moon Partnership

More Than a Trading Agreement

The Hartree offtake Nussir copper concentrate arrangement is not a conventional arm's-length trading contract. It sits within a multi-layered financial and commercial relationship between Hartree Partners LP and Blue Moon Metals that integrates equity ownership, debt financing, and commodity offtake into a single structure. Blue Moon Metals secured up to US$140 million in project finance through this partnership, underscoring the scale of commitment involved.

| Financial Instrument | Terms |

|---|---|

| Equity investment | C$12.5 million (~8% of Blue Moon Metals) |

| Project finance commitment | Up to US$140 million |

| Bridge loan (in place) | US$25 million |

| Additional bridge financing (MOU) | Up to US$20 million |

| Base metals offtake | 330,000 tonnes of copper concentrate (fixed volume) |

| Precious metals stream | Separate arrangement, also held by Hartree |

| Right of last offer | Applies to a portion of offtake from related Blue Moon projects |

| Technical committee seat | Hartree holds representation on technical advisory body |

This structure reflects a broader strategic shift among major commodity trading firms. Rather than waiting for projects to reach production and then competing for spot or short-term contract volumes in a tight market, trading houses are now deploying capital at the development stage to secure long-dated supply pipelines. The equity co-investment component is particularly significant: it aligns Hartree's financial interests directly with project delivery, creating an incentive for the trader to support rather than merely observe the development process.

The Fixed-Volume Offtake Structure Explained

One technically nuanced aspect of this agreement is that it is structured around a fixed total volume of 330,000 tonnes rather than a fixed multi-year term. This distinction matters more than it might initially appear.

At the planned production rate of approximately 32,500 tonnes of concentrate per year, the offtake volume represents roughly 10 years of full-rate output. However, Blue Moon Metals has indicated an ambition to eventually double annual production at Nussir. If that expansion is realised, the offtake delivery period would compress to approximately five years, substantially accelerating the timeline over which Hartree recovers its capital.

This creates an embedded incentive mechanism: the developer benefits from higher throughput through faster capital recovery and operational leverage, while the offtake partner benefits from earlier fulfilment of its contractual volume. It is a structurally elegant alignment of interests that differs from traditional fixed-term agreements, where a trader might have less incentive to support production acceleration.

Production Timeline: From Permits to Commercial Output

The Nussir project has completed a significant sequence of regulatory and engineering milestones that reduce development risk considerably relative to earlier-stage projects.

April 2026 → Feasibility study published by Worley Europe Ltd

June 18, 2026 → Norwegian Directorate of Mines approves updated mine operating plan

June 25, 2026 → EPC contract awarded to MOMEK Services AS; environmental permits finalised

July 6, 2026 → Hartree offtake agreement publicly confirmed

Q4 2027 → First production targeted

Q2 2028 → Full commercial production expected

The award of the EPC contract to MOMEK Services AS, a subsidiary of Norway's MOMEK Group, is particularly significant from a risk management perspective. EPC contracts transfer a defined scope of construction responsibility to a contractor, with the developer bearing less direct exposure to cost overruns within the contracted scope. In the context of an Arctic operating environment, where weather, logistics, and labour constraints are meaningful variables, this risk allocation is commercially prudent.

The ramp-up window from first production in Q4 2027 to full commercial output in Q2 2028 is approximately two quarters. For an underground Arctic mining operation, this timeline is relatively tight and reflects the advanced state of engineering preparation rather than optimistic scheduling.

Risk Dimensions Investors and Market Participants Should Weigh

Execution and Logistics Risk

Arctic operating environments introduce complexity that temperate-climate mining projects do not face to the same degree. Year-round shipping from the mine-site port in Norway, whilst feasible given Norway's ice-free northern coastlines in many areas, requires logistical planning that accounts for seasonal conditions. Concentrate shipments in 5,000-tonne lots imply a vessel call frequency that needs reliable port access and scheduling coordination with smelter destinations.

Financial and Pricing Transparency

Several commercially material terms remain undisclosed:

- TC/RC terms negotiated with Hartree have not been made public

- The term versus spot pricing structure of the offtake has not been confirmed

- Detailed elemental assay data for the concentrate has not been independently verified

- The capital allocation pathway for any production doubling scenario has not been formally scoped

These gaps do not invalidate the strategic logic of the arrangement; however, they do limit the ability of external analysts and investors to model precise revenue economics on a per-tonne basis.

Production Doubling as Optionality, Not Certainty

The ambition to double Nussir's output is best understood as medium-to-long-term optionality rather than a near-term operational commitment. Achieving double the current planned throughput would require a separate feasibility process, additional capital investment beyond the current US$140 million project finance envelope, and new regulatory engagement. Investors should apply appropriate probability weighting to this scenario when assessing project economics.

The next major ASX story will hit our subscribers first

What the Nussir Deal Reveals About the Future of Copper Supply Chains

The convergence of three structural forces is reshaping how copper concentrate is sourced, financed, and contracted globally:

- Grade decline at major producing mines is reducing the volume of high-quality concentrate available per tonne of ore processed, tightening effective supply even where mine production volumes remain stable

- Smelter overcapacity relative to available concentrate, particularly driven by Chinese refinery expansion, is creating persistent downward pressure on TC/RCs and incentivising early-stage supply capture

- Geopolitical concentration risk in copper supply chains, with significant production concentrated in a small number of jurisdictions, is driving European and allied-nation buyers to prioritise politically stable, domestically accessible sources

The Nussir project sits at the intersection of all three dynamics. Its Norwegian jurisdiction offers political stability and established environmental governance. Its clean, high-grade concentrate profile commands genuine commercial differentiation in a penalty-heavy market. Consequently, its contracted offtake with a major global trading house reduces the financing and market access risk that typically constrains junior developers.

In addition, the copper supply gap that analysts have long anticipated is now manifesting in real pricing data, making pre-production offtake agreements of this nature increasingly strategic rather than merely procedural. Furthermore, considering the future of copper mining more broadly, the Nussir model may well serve as a template for how upstream capital is deployed across the sector.

Investor perspective: The Hartree offtake Nussir copper concentrate agreement is not simply a supply contract. It is a structural signal that sophisticated commodity capital is positioning for a prolonged period of concentrate scarcity, and doing so by moving further upstream in the value chain than has traditionally been the norm.

Whether the project delivers on its Q4 2027 first production target will depend on factors that no offtake agreement can fully insulate against: construction execution, underground development rates, and the operational realities of Arctic mining. Nevertheless, the financial architecture now in place — combining equity, bridge finance, project finance, and long-dated offtake within a single integrated partnership — represents one of the more sophisticated junior mining financing structures to emerge in the European copper space in recent years. For those evaluating copper investment strategies, this deal offers a compelling case study in how capital can be structured to capture long-term supply chain value.

This article contains forward-looking statements and references to production timelines, financial projections, and market forecasts. These involve inherent uncertainties and should not be interpreted as guarantees of future performance. Independent due diligence is recommended before making any investment decisions. TC/RC data sourced from Fastmarkets (July 3, 2026). All project data sourced from Blue Moon Metals public disclosures and Fastmarkets reporting.

Want to Capitalise on the Next Major Copper Discovery Before the Broader Market?

Discovery Alert's proprietary Discovery IQ model instantly scans ASX announcements to identify significant copper and base metals discoveries, delivering real-time alerts that give subscribers an actionable edge in a concentrate-scarce market — explore historic discoveries and their exceptional returns, then begin a 14-day free trial at Discovery Alert to position yourself ahead of the next major find.