May 17, 2026

The Strategic Context Behind Major Copper Consolidation

The mining industry is experiencing a fundamental shift as established players aggressively pursue copper assets to secure future production streams. Fortescue lifts global copper exposure with Alta takeover, demonstrating how major miners are positioning themselves for unprecedented copper demand driven by electrification mandates, renewable energy deployment, and data infrastructure expansion. This structural transformation differs markedly from historical commodity cycles, creating sustained supply-demand imbalances that mining executives cannot ignore.

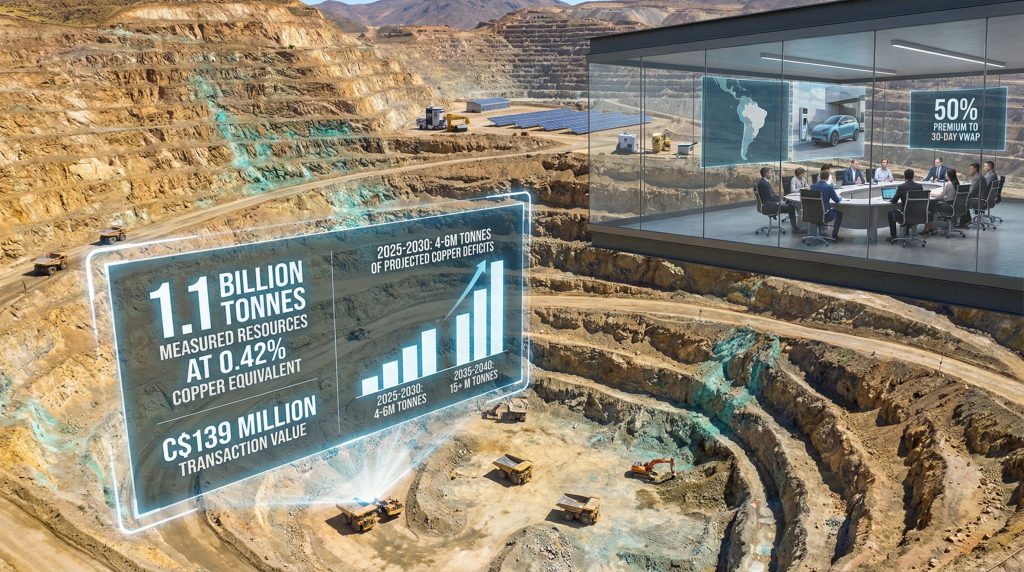

Furthermore, this mining consolidation trends reflects broader market forces reshaping the industry. Fortescue's strategic pivot represents a calculated response to these dynamics, with the company's acquisition of Alta Copper's remaining 64% stake for C$139 million signalling management confidence in long-term copper valuations.

This transaction, structured at C$1.40 per share with a 50% premium to Alta's 30-day volume-weighted average price, demonstrates the premium investors are willing to pay for quality copper development assets. Major mining companies are fundamentally rebalancing their portfolios as they recognise that critical minerals will drive future value creation.

The energy transition requires massive copper infrastructure investment, with electric vehicles demanding 3-4 times more copper than conventional vehicles and renewable energy systems requiring 2-5 times more copper per megawatt than fossil fuel alternatives.

When big ASX news breaks, our subscribers know first

What Makes the Cañariaco Project a Critical Copper Asset?

The Cañariaco project's strategic value lies in its exceptional scale and established location advantages rather than premium ore grades. With 1.1 billion tonnes of measured and indicated resources at 0.42% copper equivalent and an additional 0.9 billion tonnes of inferred resources at 0.29% grade, this asset offers the massive production capacity required to address projected supply deficits.

Resource Scale and Geographic Advantages

The project's 91 square kilometre tenure package encompasses three distinct areas: Cañariaco Norte, Cañariaco Sur, and the Quebrada Verde exploration target. This configuration provides operational flexibility and mine-life extension opportunities that smaller deposits cannot offer. The dual deposit structure enables staged development, reducing execution risk whilst maintaining long-term production optionality.

Northern Peru's established mining corridor provides significant infrastructure advantages that reduce development capital requirements. The Cajamarca region hosts several operating copper mines, including major copper system Argentina developments and regional facilities that have created robust supply chains, skilled workforce availability, and regulatory familiarity.

This existing infrastructure network substantially de-risks project development compared to greenfield locations. Additionally, the region's proven track record provides operational precedents that reduce technical uncertainty.

Technical Development Readiness Assessment

The preliminary economic assessment released in June 2024 validated the project's commercial viability under current market conditions. While specific financial metrics remain proprietary, the board's unanimous recommendation and Fortescue's acquisition premium indicate positive project economics. The PEA completion demonstrates advanced technical understanding and reduces execution uncertainty for the new owner.

Project Development Timeline:

- Environmental permitting: 12-24 months concurrent with feasibility studies

- Final feasibility study: 18-36 months from PEA completion

- Construction phase: 3-4 years under accelerated development scenario

- First production target: 2029-2031 timeframe

Why Are Major Miners Accelerating Copper Acquisition Strategies?

The copper market confronts a structural supply deficit that distinguishes current conditions from typical commodity cycles. Global mine production of approximately 21 million tonnes annually faces demand growth of 4-6% per year, whilst supply capacity increases only 2-3% annually. This fundamental imbalance creates cumulative shortfalls projected to reach 4-6 million tonnes by 2030.

Global Supply Deficit Projections

Moreover, analysts examining the global copper supply forecast suggest these deficits could intensify if new projects face delays. The following table illustrates projected shortage scenarios:

| Timeframe | Projected Deficit | Key Drivers |

|---|---|---|

| 2025-2030 | 4-6 million tonnes | Electrification demand surge |

| 2030-2035 | 8-12 million tonnes | Grid infrastructure expansion |

| 2035-2040 | 15+ million tonnes | Full energy transition impact |

Supply-Side Constraints Analysis:

- Grade decline: Global copper ore grades declining 0.3-0.4% annually

- Development timelines: New mines requiring 10-15 years from discovery to production

- Project deferrals: 25+ significant copper projects cancelled or delayed due to permitting challenges

- Capital intensity: Rising development costs per tonne of production capacity

Critical Minerals Portfolio Diversification

Major miners face strategic imperatives to reduce commodity concentration risk as traditional revenue sources encounter long-term headwinds. Iron ore and coal markets face uncertain demand trajectories due to decarbonisation policies, whilst copper exhibits rising marginal utility in electrified economies.

Consequently, strategic copper-uranium investment trends are reshaping portfolio allocation strategies across the sector. These investment patterns reflect recognition that critical minerals will dominate future value creation.

Copper Demand Acceleration by Sector:

- Electric vehicles: Current demand ~0.5-0.7 million tonnes annually; growth rate 25-30%

- Renewable energy: ~3.5-4.0 million tonnes annually; expansion rate 15-20%

- Grid modernisation: Global investment requirement exceeding $2 trillion through 2050

- Data centres: AI-driven expansion requiring 10-15% additional power infrastructure annually

Strategic buyers recognise that securing tier-one copper assets today positions them to capture significant value appreciation as supply constraints intensify. Unlike cyclical price movements, the current demand acceleration reflects permanent structural changes in global energy systems.

How Does This Transaction Compare to Recent Copper M&A Activity?

Fortescue's acquisition premium of 50% to Alta's trading price aligns with recent industry benchmarks for strategic copper asset acquisitions. Development-stage copper projects typically command premiums of 30-50% depending on resource quality, jurisdiction, and study advancement, whilst tier-one deposits can attract strategic premiums of 45-65%.

Premium Analysis Framework

Transaction Structure Comparison:

- Fortescue-Alta premium: 50% to 30-day VWAP

- Industry development-stage average: 30-50%

- Strategic asset premiums: 45-65% for tier-one deposits

- Geographic premium factors: Peru jurisdiction adds 5-10% valuation benefit

The C$139 million total transaction value represents strategic positioning rather than opportunistic acquisition. Major miners increasingly view copper asset acquisition as portfolio insurance against supply shortages rather than traditional return-maximisation investments. This shift explains willingness to pay elevated premiums for quality development projects.

Comparative M&A Premium Benchmarks

Recent copper M&A activity demonstrates consistent premium compression as strategic buyers compete for limited tier-one assets. Early-stage copper projects with completed preliminary economic assessments command higher multiples than historically observed, reflecting supply scarcity concerns among major miners.

However, copper price collapse risks from geopolitical tensions could temporarily affect acquisition pricing, though structural demand fundamentals remain supportive.

Strategic Acquisition Rationale:

- Supply security: Guaranteed future production streams

- Development acceleration: Major miners' capital resources enable faster project advancement

- Operational synergies: Technical expertise and infrastructure integration

- Market positioning: Enhanced copper portfolio credentials for ESG-focused investors

What Are the Key Risk Mitigation Strategies in Peruvian Copper Development?

Peru's mining jurisdiction offers established regulatory frameworks alongside specific challenges requiring sophisticated risk management approaches. The country's long history of large-scale copper production creates institutional knowledge and workforce expertise, whilst political stability and community relations require ongoing attention.

Regulatory Navigation Framework

Permitting Process Requirements:

- Environmental impact assessment: Comprehensive ecological and social evaluation

- Community consultation: Mandatory stakeholder engagement with indigenous populations

- Water rights acquisition: Critical resource allocation in arid regions

- Infrastructure approvals: Transportation and power supply authorisations

Fortescue's seven years of Latin American operational experience since 2018 provides significant advantages in regulatory navigation. The company has established relationships with government agencies, understanding of permitting timelines, and familiarity with community consultation protocols essential for project advancement.

Political Stability Considerations

Peru's mining-friendly regulatory environment has attracted substantial foreign investment over decades, creating stable institutional frameworks for large-scale development projects. However, periodic political transitions and evolving environmental regulations require continuous monitoring and adaptive management strategies.

Risk Mitigation Strategies:

- Community engagement protocols: Early and transparent stakeholder consultation

- Environmental compliance excellence: Exceeding minimum regulatory requirements

- Local economic development: Job creation and infrastructure investment in regional communities

- Political relationship management: Engagement with multiple government levels

How Will This Acquisition Impact Fortescue's Portfolio Balance?

The Alta Copper acquisition significantly advances Fortescue's strategic diversification beyond iron ore dependency. Currently, iron ore comprises approximately 85-90% of revenue exposure, creating cyclicality and price volatility that management seeks to reduce through critical minerals investment.

Commodity Diversification Strategy

Current Portfolio Analysis:

- Iron ore operations: 85-90% of revenue contribution

- Copper development projects: 5-10% through various investments

- Other critical minerals: 5% development pipeline

Target Portfolio Optimisation Benefits:

- Reduced iron ore concentration: Strategic commodity risk distribution across multiple assets

- Enhanced copper exposure: Cañariaco adds significant future production capacity

- Critical minerals integration: Alignment with global decarbonisation investment themes

- Geographic diversification: Expanded operational footprint beyond Australian iron ore

Strategic Value Creation Framework

The acquisition positions Fortescue to capture copper price appreciation as supply constraints intensify throughout the 2025-2040 period. Unlike iron ore markets facing potential demand headwinds from steel industry decarbonisation, copper demand exhibits secular growth driven by energy transition requirements.

In addition, Fortescue lifts global copper exposure with Alta takeover through this strategic transaction that enhances the company's critical minerals portfolio. This move aligns with broader industry trends towards sustainable commodity exposure.

Long-Term Value Drivers:

- Structural supply deficits: Copper market fundamentals support sustained price appreciation

- ESG investment flows: Critical minerals attract institutional capital focused on energy transition

- Portfolio revaluation: Reduced commodity concentration risk may command valuation premiums

- Development optionality: Future expansion opportunities within 91km² tenure package

The next major ASX story will hit our subscribers first

What Market Dynamics Drive Copper Asset Valuations?

Copper asset valuations reflect fundamental shifts in supply-demand balance rather than temporary market conditions. The structural nature of current demand acceleration creates sustained pricing support that mining companies are positioning to capture through strategic asset accumulation.

Supply-Side Constraint Analysis

Global Production Challenges:

- Mine depletion rates: Existing operations experiencing declining ore grades

- Development complexity: New projects requiring longer lead times and higher capital intensity

- ESG compliance costs: Environmental and social requirements adding operational complexity

- Geopolitical concentration: Quality deposits concentrated in politically sensitive jurisdictions

Demand Acceleration Framework:

| Sector | Copper Intensity | Growth Projection |

|---|---|---|

| Electric vehicles | 3-4x traditional vehicles | 25-30% annual growth |

| Renewable energy | 5x fossil fuel systems | 15-20% capacity additions |

| Grid infrastructure | Massive modernisation needs | $2+ trillion investment |

| Data centres | AI-driven expansion | 20% annual power demand growth |

Market Psychology and Investment Flows

Institutional investors increasingly recognise copper as essential infrastructure for decarbonisation goals, driving capital allocation toward copper-exposed mining companies. This investment theme creates sustained demand for copper equity exposure that extends beyond traditional commodity investing.

According to recent analysis, fund managers are increasingly allocating capital to copper-exposed assets, recognising the structural demand transformation ahead.

Valuation Support Mechanisms:

- ESG mandate compliance: Institutional investors requiring critical minerals exposure

- Supply security premiums: Guaranteed future production streams commanding higher multiples

- Development acceleration value: Major miners' ability to advance projects faster than junior companies

- Long-term price appreciation bets: Structural supply shortage expectations

How Does the Transaction Structure Optimise Stakeholder Outcomes?

The transaction structure balances immediate liquidity for Alta Copper shareholders with strategic value realisation for Fortescue through comprehensive operational control. The Canadian plan of arrangement provides regulatory clarity and standardised approval processes that reduce execution risk.

Shareholder Value Maximisation

Immediate Benefits for Alta Copper Shareholders:

- 50% premium realisation: Significant uplift to recent trading levels

- Liquidity provision: Cash consideration eliminates development risk exposure

- Execution certainty: Fortescue's financial capacity ensures transaction completion

- Timeline clarity: Q1 FY2026 closing target with defined regulatory milestones

The board's unanimous recommendation alongside management support from officers holding 12.5% of shares demonstrates confidence in transaction terms and timing. This stakeholder alignment reduces approval risk and facilitates smooth transaction execution.

Strategic Buyer Advantages

Fortescue's Operational Control Benefits:

- Integrated decision-making: 100% ownership enables accelerated development decisions

- Capital deployment efficiency: Direct resource allocation without partner consultation

- Technical expertise application: Fortescue's mining methodology transfer to copper operations

- Synergy realisation: Operational efficiency gains through established Latin American infrastructure

Development Timeline Acceleration:

The acquisition enables Fortescue to leverage its established Peruvian operational infrastructure, regulatory relationships, and technical expertise to advance Cañariaco development faster than Alta Copper could achieve independently. This acceleration creates value through earlier cash flow generation and reduced project execution risk.

Furthermore, detailed reporting shows that the strategic partnership benefits both companies through enhanced operational capabilities and financial resources.

What Are the Broader Implications for Critical Minerals M&A?

The Fortescue lifts global copper exposure with Alta takeover transaction exemplifies broader consolidation trends in critical minerals as major miners secure strategic assets before supply constraints intensify. This acquisition pattern reflects fundamental shifts in mining industry strategy away from commodity diversification toward energy transition positioning.

Market Consolidation Trends

Strategic Acquisition Drivers:

- Tier-one asset scarcity: Limited number of quality development projects available

- Capital requirement barriers: Development costs exceeding junior company financing capacity

- Technical expertise gaps: Complex projects requiring major miner operational capabilities

- Time horizon misalignment: Long development timelines favouring established players

Investment Thesis Evolution:

Major mining companies are transitioning from cyclical commodity exposure toward structural energy transition positioning. This strategic shift creates sustained demand for copper assets regardless of short-term price movements, supporting elevated acquisition premiums.

Geographic Diversification Imperatives

Risk Distribution Requirements:

- Jurisdiction diversification: Reducing political and regulatory concentration risk

- Supply chain security: Geographic distribution of production sources

- Market access optimisation: Regional positioning for key demand centres

- ESG compliance standards: Operations in jurisdictions with established environmental frameworks

Long-Term Industry Structure:

The critical minerals sector is evolving toward greater concentration among major miners capable of financing large-scale development projects. This consolidation trend creates opportunities for strategic asset accumulation whilst quality deposits remain available at reasonable premiums.

Future M&A Implications:

- Premium compression expectations: Early-stage assets commanding higher multiples as supply tightens

- Accelerated acquisition timelines: Strategic buyers moving faster to secure assets before competition intensifies

- Enhanced due diligence requirements: Greater focus on ESG compliance and community relations

- Integrated development strategies: Buyers emphasising operational synergies and development acceleration

Conclusion: Strategic Positioning for the Energy Transition

As global copper markets face unprecedented supply challenges, strategic acquisitions like Fortescue lifts global copper exposure with Alta takeover represent proactive positioning for the structural demand growth ahead. Companies that secure quality copper assets today will benefit from sustained value appreciation as energy transition requirements drive consumption growth throughout the next decade.

The transaction demonstrates how established mining companies are leveraging their capital strength, technical expertise, and operational infrastructure to capture value in critical minerals markets. This strategic approach positions major miners to benefit from the energy transition whilst providing development-stage companies with attractive exit opportunities at significant premiums to market valuations.

Consequently, this acquisition sets a precedent for future critical minerals M&A activity, establishing premium benchmarks and highlighting the strategic value of quality copper development projects. As supply constraints intensify and demand acceleration continues, similar transactions will likely become increasingly common in the sector.

Ready to capitalise on the next major copper discovery?

Discovery Alert instantly identifies significant ASX mineral discoveries using its proprietary Discovery IQ model, transforming complex geological announcements into actionable investment insights for both short-term traders and long-term investors. Explore how major mineral discoveries can generate substantial returns by visiting Discovery Alert's dedicated discoveries page and begin your 30-day free trial today to position yourself ahead of the market.