July 16, 2026

When Copper Started Behaving Like a Technology Stock

There is a peculiar phenomenon unfolding across global commodity markets that would have seemed implausible to most industrial metal analysts just a decade ago. Copper demand from AI data centers is fundamentally reshaping how institutional money managers think about metal allocation. No longer moving primarily in response to Chinese construction data or global manufacturing PMIs, copper is tracking the fortunes of Nvidia, reacting to AI earnings calls, and correlating with the Nasdaq-100.

This is not a short-term aberration. It represents a structural repricing of copper's role in the global economy, driven by the convergence of two of the most capital-intensive megatrends in modern history: the electrification of everything and the explosive buildout of artificial intelligence infrastructure. Understanding the mechanics of this shift — its scale, timing uncertainties, and genuine risks — is increasingly essential for anyone seeking to understand where commodity markets are heading over the next two decades.

When big ASX news breaks, our subscribers know first

Why Copper Has Become the Defining Infrastructure Metal of the AI Era

The Convergence of Electrification and AI Infrastructure

For most of the 20th century, copper demand was a reliable proxy for industrial activity. The metal tracked steel, tracked construction, and tracked automotive output. Its nickname as "Dr. Copper," earned for its supposed ability to diagnose the health of the global economy, reflected its role as a lagging indicator of real economic conditions.

That relationship has not disappeared, but it has been joined by something far more forward-looking. Copper is now being priced on the basis of what it will be needed for, not just what it is currently being consumed in. The AI infrastructure buildout — spanning data centres, grid upgrades, substation construction, and transmission line expansion — has transformed copper from a cyclical industrial input into what analysts are increasingly calling a strategic infrastructure asset.

The historical parallel most frequently cited is China's industrial expansion in the early 2000s, which produced a commodity supercycle that reshaped global copper production for the better part of a decade. Mercuria's head of metals research, Nicholas Snowdon, has publicly drawn a direct comparison between the trajectory of AI-driven copper demand and the growth arc of China's electric vehicle and renewables sectors. The implication is significant: if AI infrastructure follows a similar adoption curve, copper markets could be at the beginning of a multi-year structural demand event rather than a speculative rally.

How Does an AI Data Centre Actually Use Copper?

Copper demand from AI data centers operates across multiple layers simultaneously, which is why the aggregate figures can appear surprisingly large relative to the visible footprint of individual facilities.

| Application Layer | Copper Use Case | Relative Intensity vs. Traditional DC |

|---|---|---|

| Power delivery systems | Busbars, cables, switchgear | 3–5× higher |

| Cooling infrastructure | Liquid cooling loops, heat exchangers | Significantly elevated |

| Network connectivity | High-speed data cabling, patch panels | Moderate increase |

| Grounding and safety systems | Earthing conductors, bonding | Proportional to scale |

| Grid connection infrastructure | Substations, transformers, transmission lines | Major new demand vector |

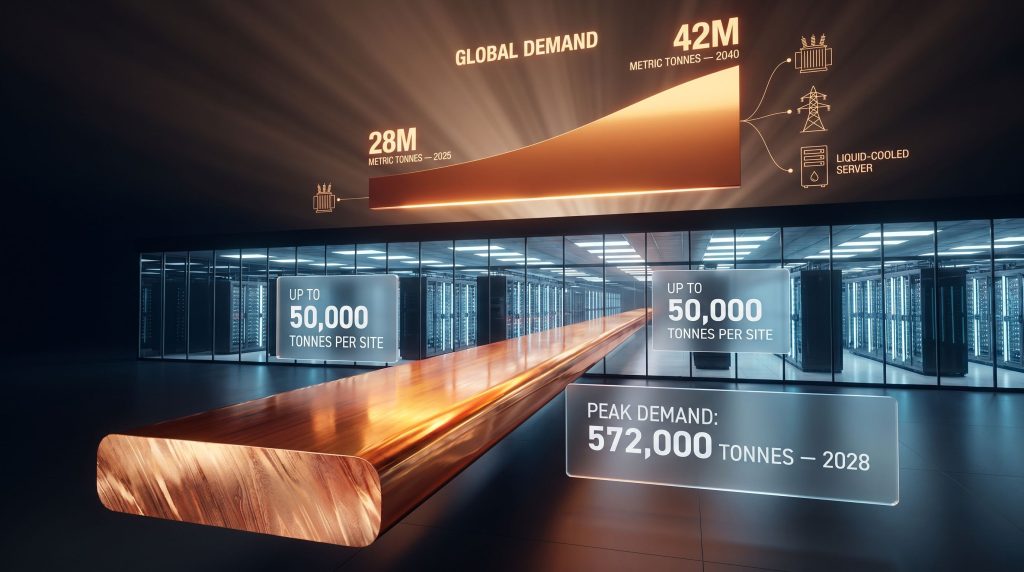

According to figures from the Copper Development Association, conventional data centres typically require between 5,000 and 15,000 tonnes of copper per facility. Hyperscale AI facilities, however, can require up to 50,000 tonnes per site, reflecting the dramatically higher power density, more intensive cooling requirements, and far more substantial grid connection infrastructure that AI workloads demand.

Critically, as Guy Wolf, Marex Group's global head of market analytics, has noted, it is not really the data centres themselves that represent the largest copper demand driver. Furthermore, the power generation and transmission network required to support them is where the most significant metal volumes are embedded. Each new hyperscale AI facility effectively creates three distinct copper demand waves:

- Construction-phase demand for internal electrical, cooling, and connectivity systems

- Grid-connection demand for substations, transformers, and transmission upgrades to deliver the required power

- Ongoing operational demand for maintenance, capacity expansion, and efficiency retrofitting over the facility's operational life

This cascade effect means that announced data centre investment translates into copper demand that extends well beyond the construction window, creating a more durable demand signal than a single-event infrastructure spend would suggest.

What Does the Demand Curve Actually Look Like?

Scenario 1: Base Case — Steady AI Infrastructure Expansion

Under a base case assumption of measured but sustained AI infrastructure buildout, BloombergNEF-referenced projections model AI-powered facilities driving approximately 400,000 tonnes of copper demand annually over the coming decade. Peak AI-driven copper consumption under this scenario is estimated at approximately 572,000 tonnes in 2028, before efficiency gains in chip architecture and cooling technology begin moderating the per-unit copper intensity of AI compute.

To contextualise this figure: S&P Global estimates total global copper consumption at approximately 28 million metric tonnes annually as of 2025. The current AI data centre share, estimated by Mercuria at roughly 350,000 tonnes in 2026, represents approximately 2.5% of annual demand — a figure that sounds modest until mapped against its growth trajectory and the compounding effect of grid infrastructure investment.

Scenario 2: Accelerated Case — Hyperscale Buildout at Scale

BHP's long-range projections present a more striking picture. The mining giant models data centre copper consumption rising six-fold by 2050, from approximately 0.5 million tonnes annually to 3 million tonnes annually. In addition, S&P Global's structural forecast projects total global copper consumption rising from 28 million metric tonnes in 2025 to 42 million metric tonnes by 2040 — an increase of 50% over 15 years.

The supply deficit scenario that emerges from this demand trajectory is where analyst concern is most concentrated. If AI infrastructure buildout accelerates as projected while mining and refining capacity fails to scale commensurately, multiple forecasting bodies model a potential supply gap of up to 6 million tonnes by 2035. Understanding these dynamics is central to developing sound copper investment strategies for the years ahead.

Scenario 3: Constrained Case — Bottlenecks Delay Demand Materialisation

The constrained scenario is arguably the most intellectually honest of the three. Microsoft, Alphabet's Google, and Amazon have collectively committed approximately $580 billion to U.S. data centre projects in 2026 alone. Yet as research from Marex Group and Oxford University highlights, the industry is encountering formidable execution bottlenecks across labour availability, power procurement, equipment supply chains, and permitting timelines.

Guy Wolf, Marex Group's global head of market analytics, has noted publicly that while the AI narrative is genuinely bullish for copper, the actual metals demand is probably further into the future than many investors currently assume.

The distinction between committed capital and actual metal consumption is essential for investors assessing the near-term copper demand thesis. Announced investment is real; the copper required to build the infrastructure will materialise, but its timing is genuinely uncertain.

The Three-Pillar Framework Driving Copper's Structural Bull Case

Pillar 1: AI and Data Centre Infrastructure Demand

Matt Miskin, co-chief investment strategist at Manulife John Hancock Investments, has characterised the copper investment thesis as a three-legged stool: AI demand, inflation hedging, and a macro environment running structurally hot. The AI pillar is the most visible, but it is the interaction of all three that explains the scale and persistence of the current rally.

As data centre electricity consumption grows from approximately 2% of global electricity use today toward a projected 9% by 2050 (per BHP), the grid infrastructure investment required to support that growth creates a secondary and tertiary copper demand wave that compounds the direct facility construction demand.

Pillar 2: Macro Inflation Hedging and Hard Asset Rotation

Commodities broadly, and copper specifically, have undergone a significant re-rating in institutional portfolio construction. Investors are no longer treating copper purely as an industrial exposure; it is increasingly being held as a hard asset hedge against persistent inflation and currency debasement.

The scale of this rotation is quantifiable. Money managers have added approximately $14 billion in net-long futures positions in London and New York copper markets within a single quarter. Over the same period, the combined market capitalisation of Nasdaq-100 companies rose by approximately $7.8 trillion, with copper prices moving in near-parallel — a behavioural correlation not seen in prior commodity cycles.

Pillar 3: Chronic Supply-Side Underinvestment

The supply-side story is where the structural bull case finds its most durable foundation. Matthew Fine, a portfolio manager who has focused on copper miners since 2017, has argued that even accounting for AI's contribution as a new demand vector, copper demand is only likely to grow at approximately 2.7% annually through to 2040.

That rate sounds manageable until mapped against a mine development pipeline that is increasingly unable to keep pace. Permitting timelines for new copper mines routinely run between 10 and 20 years from discovery to production. Furthermore, ore grades at existing mines are declining as the highest-quality deposits are progressively depleted. Fine has stated plainly that the world faces a genuine, structural copper supply crunch in the near to medium term, independent of whether AI demand materialises exactly as projected.

Comparative Demand Vector Analysis

| Demand Driver | Annual Copper Impact (Approx.) | Timeline to Peak | Structural or Cyclical? |

|---|---|---|---|

| AI data centers (current) | ~350,000–400,000 tonnes | 2028–2032 | Structural |

| EV manufacturing and charging | ~1.5–2 million tonnes | 2030–2035 | Structural |

| Renewable energy (solar/wind) | ~1–1.5 million tonnes | 2030–2040 | Structural |

| Grid modernisation (global) | ~2–3 million tonnes | 2030–2050 | Structural |

| Traditional industrial demand | ~20+ million tonnes baseline | Mature | Cyclical |

What distinguishes the current copper market from any prior cycle is the simultaneous activation of multiple structural demand drivers. AI data centre demand is not replacing EV demand or renewable energy demand; it is layering on top of them, compressing the timeline within which the global mining industry must respond.

Regional Demand Hotspots: Where AI Copper Demand Is Concentrating

North America: The Fastest-Growing Demand Centre

U.S. data centre electricity consumption is projected to grow from approximately 5% to 14% of national electricity demand by 2030, according to S&P Global. The copper demand embedded in the grid upgrades required to deliver that power growth may ultimately exceed the copper demand from the data centre construction itself.

A complicating factor is the tariff arbitrage dynamic currently distorting US-China copper prices and U.S. copper markets more broadly. Comex copper prices have been trading approximately $400 per tonne above LME prices, incentivising physical metal flows toward U.S. warehouses and creating supply tightness elsewhere.

Europe: Power Availability as the Binding Constraint

In Europe, AI infrastructure ambition is being moderated not by lack of investment appetite but by electricity availability. Data centre concentration in markets such as Ireland has already pushed national grid capacity toward its limits, forcing regulators to impose connection moratoriums in some jurisdictions. The grid upgrade investment required to overcome these constraints represents a secondary copper demand wave that operates independently of the facilities themselves.

Asia-Pacific: China's Shifting Role

China's domestic copper demand has undergone a structural shift. The property sector, which drove copper demand for much of the 21st century, has contracted significantly. Its place has been taken by power grid investment and the renewable energy and EV manufacturing sectors. China is consequently transitioning from price-setter to price-taker — a structural shift with significant implications for how global copper markets are balanced and who bears the cost of supply tightness.

The next major ASX story will hit our subscribers first

The Unicorn Mine Phenomenon: A Supply-Side Reality Check

One of the less widely understood dynamics currently reshaping the copper mining landscape is the emergence of what the industry is calling unicorn mines. The recent copper price surge has made approximately 75 previously uneconomic copper deposits financially viable, with 23 newly qualifying in the most recent price rally.

However, financial viability is not the same as production readiness. A deposit that crosses the economic threshold today still requires years of feasibility work, environmental permitting, infrastructure development, and capital raising before it contributes a single tonne of refined copper to global supply. Consequently, the unicorn mine phenomenon is a long-dated supply signal rather than a near-term relief valve.

The geographic concentration of copper refining capacity adds another layer of structural vulnerability. The majority of the world's copper refining capacity sits within China, creating a strategic bottleneck for Western AI infrastructure buildout that is receiving growing attention from policymakers. Advancing future copper mining capabilities outside Asia remains a critical long-term priority.

Supply Deficit Scenarios at a Glance

| Scenario | Projected Supply Gap by 2035 | Key Assumptions |

|---|---|---|

| Base case | ~3–4 million tonnes | Moderate AI buildout, incremental new mine development |

| Accelerated AI case | ~6 million tonnes | Rapid hyperscale expansion, limited new supply |

| Efficiency-adjusted case | ~1–2 million tonnes | Significant copper intensity reductions per AI workload |

What Are the Real Risks to the AI Copper Demand Thesis?

Not all observers are uniformly bullish, and the risks to the thesis deserve serious consideration rather than dismissal.

Demand timing miscalculation is the most frequently cited risk among experienced commodity analysts. The market may be pricing in copper demand that is genuinely years away from materialising in physical form. Commodity markets have a well-documented history of mispricing the timing of structural demand shifts, and the gap between announced data centre investment and actual metal consumption is currently wide.

Efficiency gains reducing copper intensity represent a technological wildcard. As chip architectures advance and alternative thermal management approaches mature, the copper required per unit of AI processing capacity could decline meaningfully. Liquid cooling innovations, in particular, are advancing rapidly and could moderate the per-facility copper intensity assumptions underpinning the more aggressive demand forecasts.

Geopolitical and trade disruption adds supply-side uncertainty that can amplify price volatility independently of AI demand fundamentals. The tariff-driven Comex premium is already distorting physical metal flows in ways that create artificial tightness in some markets while masking genuine demand weakness in others.

Investor sentiment reversal is perhaps the most underappreciated near-term risk. Copper's growing correlation with technology equity indices means a significant tech sector correction could trigger copper price weakness even if the underlying physical demand fundamentals remain structurally intact. The distinction between the long-term structural demand story and the near-term speculative positioning that has amplified the recent price rally is essential for investors managing position sizing and timing.

Key Data Summary: Copper Demand From AI Data Centers

| Metric | Data Point | Source |

|---|---|---|

| Copper per hyperscale AI facility | Up to 50,000 tonnes | Copper Development Association |

| Projected annual AI copper demand | ~400,000 tonnes/year average | BloombergNEF-referenced reporting |

| Peak AI copper demand year | ~2028 (572,000 tonnes) | BloombergNEF-referenced reporting |

| Projected supply gap by 2035 | Up to 6 million tonnes | Carbon Credits / BloombergNEF |

| BHP 2050 data center copper forecast | 3 million tonnes/year (6× current) | BHP Insights |

| S&P Global 2040 total demand forecast | 42 million metric tonnes | S&P Global |

| Data center share of global electricity (2050) | ~9% (up from ~2%) | BHP Insights |

| U.S. data center electricity share (2030) | ~14% (up from ~5%) | S&P Global |

| Institutional net-long copper positions (Q2 2026) | ~$14 billion added | Bloomberg |

| Committed U.S. data center investment (2026) | ~$580 billion | Marex / Bloomberg |

Strategic Implications for Investors and Industry

The AI-copper nexus creates a differentiated set of implications depending on the investor's time horizon and risk tolerance. For long-term allocators, the three-pillar framework of AI demand, inflation hedging, and supply scarcity provides a multi-dimensional thesis more durable than any single narrative. For shorter-term traders, the critical discipline is separating the structural demand signal from the speculative amplifier that institutional tech-correlated inflows have introduced into copper pricing.

For the mining industry itself, the AI buildout represents a generational investment case, but only for producers with long-dated, scalable assets capable of delivering supply into the 2035 to 2040 window when AI-driven copper demand is modelled to be approaching its structural peak. Decisions being made today about capital allocation, project development, and permitting strategy will ultimately determine whether the industry is positioned to meet that demand or whether the supply deficit scenarios currently modelled by BHP, S&P Global, and others become the defining market reality of the 2030s.

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Forward-looking projections and demand forecasts cited herein are drawn from third-party research sources and involve inherent uncertainty. Past commodity price performance is not indicative of future results. Readers should conduct independent research and consult qualified financial advisers before making investment decisions.

Want to Position Ahead of the Next Major Copper Discovery on the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries — including copper — are announced on the ASX, turning complex data into actionable insights for both short-term traders and long-term investors. Explore why major mineral discoveries have historically generated extraordinary returns and begin your 14-day free trial today to secure a market-leading edge as the AI-driven copper demand story continues to unfold.