June 16, 2026

When Strong Prices Are Not Enough: The Financing Gap Reshaping Copper Development

There is a persistent assumption in commodity markets that high prices automatically unlock new supply. However, the copper market is challenging that idea. Prices are roughly 35% above year-ago levels, yet the project pipeline is tightening. The reason lies in the mechanics of mine finance and how higher financing costs for copper developers are reshaping development economics.

This shift is not just about geology or politics. Instead, it reflects a harsher funding environment in which debt is pricier, equity is more selective, and project hurdles are rising. Consequently, even strong copper prices are not enough to move every asset towards construction.

When big ASX news breaks, our subscribers know first

The Interest Rate Transmission Mechanism in Mining Finance

Understanding why elevated rates hurt copper developers requires understanding how mine finance works. Unlike a software firm or retailer, a copper mine often needs hundreds of millions, or even billions, of dollars before earning its first dollar of revenue. In addition, construction timelines can span three to seven years.

Permitting adds further delays. In jurisdictions such as the United States, approval timelines can stretch for a decade or more. As a result, projects with distant cash flows are highly vulnerable to changes in discount rates.

This matters because net present value, or NPV, discounts future cash flows into today’s dollars. The further out those cash flows sit, the more value is eroded when rates rise. Therefore, a long-dated mine project suffers far more than a short-cycle asset.

When the weighted average cost of capital rises from 7% to 10%, a project that once looked robust may no longer clear its internal hurdle rate. Debt becomes more expensive, while equity investors demand stronger returns. This is one reason why fewer projects are reaching final investment decisions.

Furthermore, the broader macro backdrop has worsened the pressure. Inflation driven by energy and supply-side constraints has limited the scope for rate cuts. A stronger US dollar adds another challenge, because copper is priced in dollars and development costs can rise sharply in local currency terms.

For broader context on this funding challenge, S&P Global has highlighted how capital demands for new copper supply are increasing even as the market needs more output.

Declining Ore Grades Are Amplifying the Capital Intensity Problem

Higher rates are not arriving in isolation. They are colliding with another structural trend: declining copper ore grades across the global mining sector.

| Factor | Direction | Development Cost Impact |

|---|---|---|

| Average copper ore grade | Declining | More ore required per tonne of copper produced |

| Mine depth | Increasing | Higher extraction and infrastructure costs |

| Processing complexity | Rising | Greater capital expenditure per unit of output |

| Financing rates | Elevated | Higher discount rates compress NPV and extend payback periods |

| USD strength | Elevated | Raises effective project costs in non-dollar economies |

As grades fall, miners must move and process more material to produce each tonne of copper. That means larger plants, higher energy use, greater water demand, and more equipment. In turn, these factors raise upfront capital needs.

Chile’s Cochilco has projected that billions of dollars of investment will generate only modest production growth through the next decade. Meanwhile, BHP has flagged declining production at several major operations. That underlines a difficult truth: more capital is increasingly needed just to maintain output.

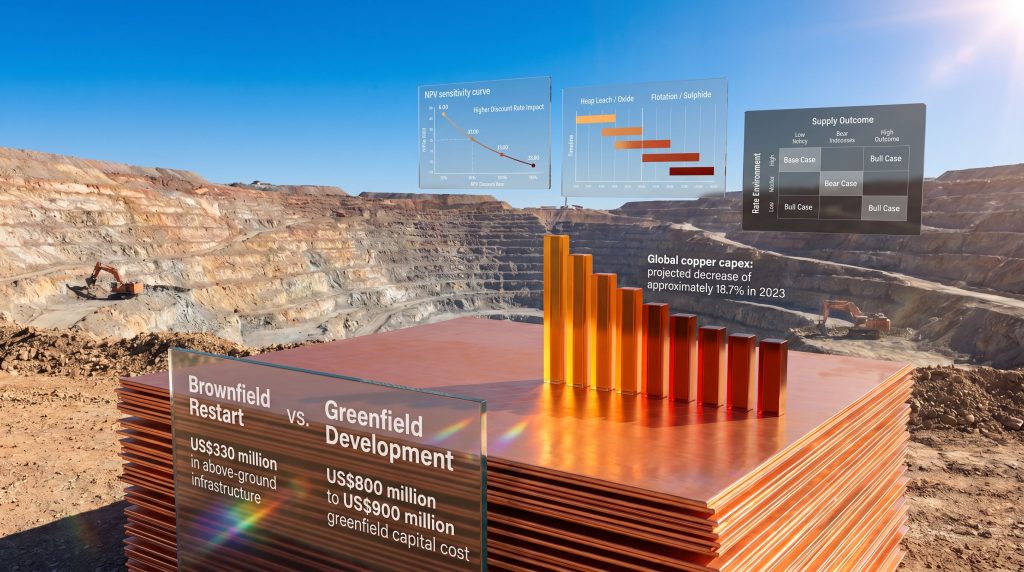

Global copper capital expenditure fell 0.1% in 2022, followed by a projected decline of around 18.7% in 2023. Accordingly, the industry has been retreating from investment even as long-term demand remains supportive. This is where higher financing costs for copper developers become especially damaging.

How Developers Are Responding: Four Capital Efficiency Strategies

Faced with these conditions, developers are adapting. Several approaches are emerging to reduce upfront capital requirements and preserve shareholder value.

1. Low-capital-intensity processing routes

Heap leaching, SX-EW, and in-situ leaching can require much less upfront capital than conventional flotation circuits. In addition, they may allow staged development and earlier revenue generation.

Where suitable, developers can also benefit from existing facilities. For instance, the appeal of simpler flowsheets is closely tied to the copper leaching benefits that help lower initial build costs.

2. Warrant-free equity financings

Warrant-free raises help avoid future dilution overhang. Although warrants can help secure a financing, they also create the risk of extra shares entering the market later.

Abitibi Metals demonstrated this strategy with a $31 million warrant-free financing at its B26 deposit in Quebec. The asset hosts 25.3 million tonnes grading above 2.1% copper equivalent across indicated and inferred resources. Moreover, Discovery Silver emerged as a 9.9% strategic shareholder.

3. Ring-fenced project financing

Where a company owns multiple assets, ring-fenced financing can protect exposure to higher-upside projects. Marimaca Copper is applying this approach in Chile, aiming to finance its oxide project without excessively diluting exposure to the Pampa Medina sulphide discovery.

4. Brownfield redevelopment

Past-producing assets with existing infrastructure offer a major embedded capital advantage. Selkirk Copper’s redevelopment of the Minto mine in Yukon illustrates this well.

The site retains more than US$330 million in above-ground infrastructure. By comparison, the greenfield equivalent cost is estimated at US$800 million to US$900 million. Furthermore, the existing resource stands at 12.6 million indicated tonnes at 1.20% copper and 23.7 million inferred tonnes at 1.05% copper.

Brownfield vs. Greenfield: A Structural Comparison in a High-Rate World

Brownfield advantages are not limited to lower headline capital costs. In a high-rate environment, anything that shortens payback or lowers financing risk can improve the odds of reaching a final investment decision.

| Attribute | Brownfield Restart | Greenfield Development |

|---|---|---|

| Upfront capital requirement | Lower | Higher |

| Construction timeline | Shorter | Longer |

| Payback period | Shorter | Longer |

| NPV sensitivity to discount rate | Lower | Higher |

| Permitting complexity | Mixed | High |

| Legacy closure liability | Must be assessed | Lower |

| Financing accessibility | Generally improved | More constrained |

That said, brownfield assets still carry risks. Existing infrastructure may require more refurbishment than expected. In addition, inherited environmental liabilities, closure obligations, and community issues can be expensive to resolve.

Processing Route Selection as a Financing Risk Variable

Processing technology is no longer just a metallurgical choice. It is also a financing decision. Heap leaching generally requires less capital than flotation and can often be expanded in stages.

Flotation remains essential for many sulphide deposits and can deliver higher recoveries. However, it usually comes with a bigger capital bill. Therefore, some developers are pursuing staged pathways, beginning with oxide material before committing to a larger sulphide circuit.

This staged logic connects closely with a definitive feasibility study or earlier technical work, because investors increasingly want proof that processing and financing plans are aligned from the outset.

The next major ASX story will hit our subscribers first

The Investor Screening Framework: Seven Variables That Now Matter More Than Grade

In prior cycles, grade often dominated investor attention. Today, funding structure matters just as much. Investors should now focus on a broader checklist:

- Funded status: Can the company reach its next catalyst without another raise?

- Warrant overhang: How much future dilution could outstanding warrants create?

- Capital intensity: What is the capital cost per annual tonne of copper output?

- Infrastructure advantages: Does the project benefit from roads, water, power, or existing plants?

- Cost curve position: Can the mine remain viable if copper falls 20% to 30%?

- Balance sheet strength: Is the company debt-free, and how long is its cash runway?

- Execution track record: Has management advanced similar projects before?

These factors matter because higher financing costs for copper developers can wipe out value even when the resource itself looks attractive.

Why Per-Share Value Is the Only Metric That Matters

A company can report drilling success, expand its resource, and generate positive headlines while still destroying shareholder value. The critical distinction is between enterprise-level growth and per-share value delivery.

If a company raises capital repeatedly at weak prices, existing shareholders are diluted. Consequently, a bigger asset does not necessarily mean a better investment. This is why financing discipline has become a central evaluation criterion.

For investors weighing the sector more broadly, articles on copper investment strategies and whether copper is a good investment provide useful context on how project economics feed into market opportunity.

Long-Term Demand vs. Near-Term Supply: The Structural Gap That Persists

Long-term copper demand is projected to roughly double by 2040, driven by electric vehicles, renewables, grid expansion, and data centres. These trends are structural rather than cyclical, so they are unlikely to disappear quickly.

Against that backdrop, supply remains constrained by declining grades, rising capital intensity, and higher financing costs for copper developers. The danger is not merely a temporary shortfall. Rather, the risk is that the supply response remains delayed for years.

This is the paradox of the current market: strong prices and tight supply can coexist with weak development activity. In other words, price alone is no longer enough to unlock production on historical timelines.

Investors should therefore pay close attention to the emerging copper supply crunch and the companies best positioned to finance projects efficiently. As one core lesson of this cycle shows, balance sheet discipline now matters almost as much as the metal itself.

Key risks still include:

- Execution risk from overruns and delays

- Single-asset concentration

- Interest rate sensitivity

- Dilution risk

- Permanent capital loss if financing fails

The copper market is not broken. Demand remains compelling. However, the route from discovery to production is far more complex and capital-intensive than it was five years ago. Therefore, the best-positioned developers are those treating finance, efficiency, and dilution control as central parts of strategy rather than secondary concerns.

Want To Capitalise On The Next Major Copper Discovery Before The Broader Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly converting complex mineral data into actionable investment insights — a critical edge in today's capital-constrained copper development environment. Explore historic examples of major mineral discoveries and their returns, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.