June 16, 2026

The Quiet Shift Reshaping Junior Mining Speculation

Every few years, the junior mining market experiences a fundamental realignment between geological discovery and financial reward. For most of the past two decades, the prevailing logic was straightforward: a high-quality drill hole generated an immediate and often violent upward price movement, frequently pricing the information into the stock before most investors could establish a meaningful position. The Rick Rule junior mining drill hole market reaction framework challenges this assumption directly, and for disciplined speculators who understand what this means structurally, the current environment may represent one of the most compelling asymmetric setups in the modern exploration cycle.

Understanding why this shift has occurred, and what it means for portfolio positioning, requires looking beyond the drill hole itself and examining the broader forces shaping capital flows, investor behaviour, and geological interpretation in today's junior resource market.

When big ASX news breaks, our subscribers know first

The Rick Rule Junior Mining Drill Hole Market Reaction Framework

Why Discovery Premiums Have Compressed in the Current Cycle

The compression of market reactions to drill results is not a random phenomenon. It reflects a convergence of factors: elevated capital allocation to exploration over the past two and a half years is finally generating meaningful geological results, but the investment community has not yet entered what experienced resource speculators would classify as a true discovery market. The distinction matters enormously.

In an exploration market, capital is deployed, holes are drilled, and results arrive. In a discovery market, the broader investment community recognises the commercial significance of those results and aggressively re-rates stocks accordingly. The current phase appears to occupy the transitional space between these two states, with high-quality drill results beginning to emerge but market re-rating remaining subdued relative to the geological significance of the data.

Rick Rule, the veteran resource speculator and founder of Rule Investment Media, has identified this dynamic directly. His commentary on junior market dynamics notes that in prior cycles, a successful drill result was effectively monetised by the market before investors could accumulate a sufficient position to benefit. That is no longer the case. According to Rule, several truly exceptional drill holes have emerged in recent weeks, and while the market has taken notice, his assessment is that substantial value remains unrecognised by the broader investing public.

This lagged recognition is not a flaw in the market system. It is a feature of cycle timing, and historically, the investors who identify commercially significant results before consensus forms capture the most substantial gains. Furthermore, interpreting drill results correctly remains one of the most critical skills any junior mining investor can develop.

The Historical Baseline: How Markets Once Responded to High-Grade Intercepts

In previous bull market cycles, particularly the 2005 to 2008 and 2009 to 2011 periods, a single high-grade intercept from a junior explorer with the right geophysical context could double or triple a stock's market capitalisation within days. Retail momentum capital flooded into these situations rapidly, often before institutional analysis had been completed. The discovery premium was priced in almost instantaneously.

That dynamic created a paradox: the more visually spectacular the drill result, the more difficult it became for even sophisticated investors to build a meaningful position at rational prices. Today, that urgency has dissipated. Market reactions are more measured, more delayed, and in some cases, almost entirely absent relative to the quality of the underlying geological data.

What a Muted Drill Hole Reaction Actually Signals

Grade, Width, Context, and the Third Dimension

A muted market reaction to a junior mining drill hole occurs when the share price response is disproportionately small relative to the geological significance of the result. This can happen when investors fail to contextualise the hole within the broader geophysical signature of the target, when market liquidity is thin, or when speculative capital has rotated toward other areas of the resource sector.

There was a period, not too long ago, when junior mining stocks would react sharply to any drill hole featuring impressive headline grades, regardless of whether the result indicated commercial scale. The market was, in Rule's framing, reacting stupidly to nice grades. A flashy intercept with no supporting geophysical context, no depth continuity, and no indication of a larger mineralising system was being treated as equivalent to a genuinely transformational discovery.

Today's more discerning, though arguably still incomplete, market response has corrected for this excess but may have overcorrected in the opposite direction. Genuinely significant results are now being undervalued precisely because the speculative reflexes that would once have driven immediate re-rating have been conditioned out of the market by prior disappointments. Understanding true vs apparent widths is essential here, as misinterpreting these figures is a common source of investor confusion.

The Third Dimension: Why Depth Confirmation Changes Everything

One of the most technically important, yet widely misunderstood, concepts in junior mining speculation is the establishment of what practitioners call the third dimension. A single drill hole provides a two-dimensional data point: it confirms mineralisation exists at a given location and depth. What it cannot confirm, in isolation, is whether that mineralisation extends laterally and at depth in a way that constitutes a commercially significant deposit.

The third dimension, established through follow-up drilling that confirms vertical and lateral continuity, fundamentally transforms the investment thesis. A discovery with confirmed depth continuity, sitting within a large geophysical anomaly, is an entirely different asset from a single impressive intercept with no supporting context. Rule explicitly identifies this distinction as a key factor in his current approach to open-market accumulation, noting that paying up once depth continuity has been confirmed, within a target carrying a sufficiently large geophysical footprint, represents a structurally sound entry point.

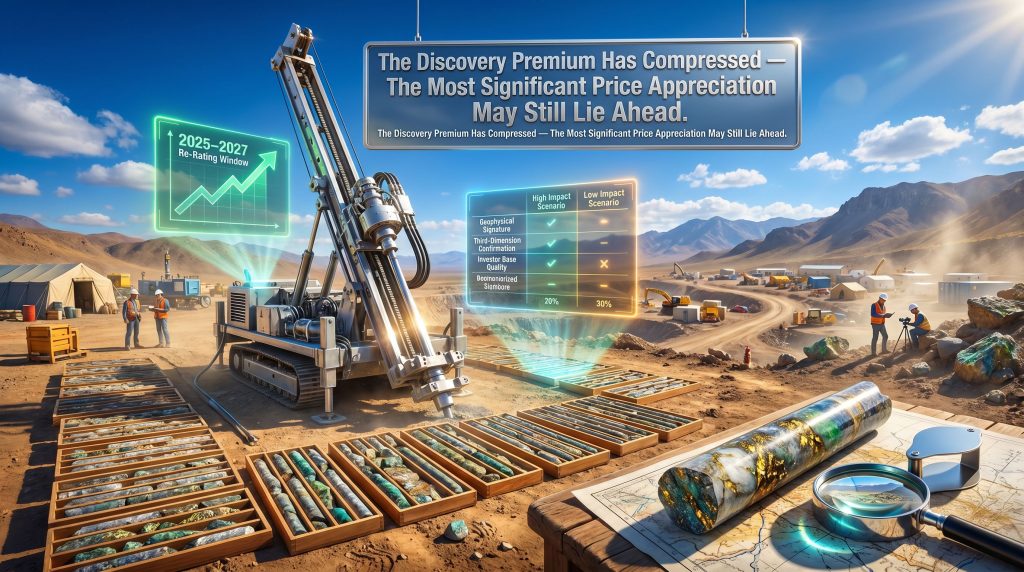

Five Factors That Drive Junior Mining Drill Hole Market Reactions

Understanding why some drill results generate explosive re-ratings while others produce muted responses requires a multi-variable analytical framework. The following factors, drawn from both the current market environment and long-cycle historical patterns, capture the primary drivers of market reaction intensity.

| Reaction Driver | High Impact Scenario | Low Impact Scenario |

|---|---|---|

| Geophysical signature | Large anomaly confirms deposit scale | Isolated intercept, no broader geological context |

| Third-dimension confirmation | Depth and lateral continuity established | Single-hole result, no follow-up data available |

| Investor base quality | Informed, long-term resource specialists | Broker-led retail momentum capital |

| Market cycle timing | Early-to-mid exploration bull market | Late-cycle fatigue or seasonal summer lows |

| Capital structure | Open market liquidity, no share overhang | Restricted placements, no warrant incentive for holders |

Each of these variables interacts with the others. A spectacular geophysical signature combined with confirmed depth continuity will still produce a muted reaction if the company's investor base consists primarily of broker-led retail capital that lacks the geological literacy to assess the significance of the data. Conversely, an informed, specialist investor base can re-rate a stock meaningfully even on a relatively modest intercept if the broader geological context supports a large-scale discovery thesis.

Are We Approaching a True Discovery Market?

The 12 to 24 Month Lag Between Capital and Recognition

One of the more instructive patterns in junior mining cycles is the consistent lag between elevated exploration expenditure and meaningful market re-rating of discovery-stage companies. Exploration capital deployed today generates drill results six to eighteen months later. Those results then require a further period of follow-up drilling before the third dimension is established and the commercial significance of the discovery becomes defensible to outside investors.

The elevated exploration budgets deployed across multiple jurisdictions over the past two and a half years are now beginning to produce results. The geological pipeline is filling. However, the investment community's re-rating mechanism remains muted, suggesting that the most significant price appreciation for discovery-stage juniors may still lie ahead. This aligns with the broader mineral discovery curve, which shows how value creation in exploration is rarely linear.

Rule has expressed confidence that high-quality projects will continue to benefit from improving market conditions over the next two to three years, with the current period of subdued reactions potentially representing the most attractive accumulation window in the cycle.

This view implies that the current junior mining market is best characterised as a late exploration, pre-discovery phase. The results are arriving. The commercial significance is emerging. But the capital has not yet followed at the scale required to price these discoveries appropriately.

How Sophisticated Speculators Are Positioning Around Muted Reactions

Open-Market Accumulation as the Dominant Strategy

The shift away from private placement participation toward open-market accumulation represents one of the most significant behavioural changes among experienced resource investors in the current cycle. Rule's explanation for this shift is pragmatic: the private placement market has become crowded, deal terms have deteriorated significantly, and the absence of warrant coverage in many current transactions has eliminated the structural advantage that sophisticated investors once enjoyed.

Where Rule previously allocated approximately 90 percent of his capital through private placement markets during bearish phases, the current competitive environment has changed that calculus dramatically. With hundreds of capital allocators competing for the same placement opportunities, warrants have been largely negotiated away, and restricted shares without warrant coverage offer no compelling advantage over open-market purchases.

The strategic implication is significant. For investors willing to conduct independent geological analysis, the open market now offers access to high-quality discovery situations at prices that reflect the market's muted reaction rather than the geological significance of the underlying data.

A Step-by-Step Framework for Approaching High-Quality Drill Results

Rule's current approach to capitalising on muted drill hole reactions can be distilled into a disciplined, information-driven accumulation process:

-

Assess the geophysical context — Determine whether the drill hole sits within a large coincident anomaly or represents an isolated intercept with limited broader significance.

-

Evaluate the third dimension — Has depth continuity been confirmed through follow-up drilling, or does this remain a single-point data result?

-

Monitor the price reaction — Is the market's response proportionate to the geological significance of the result, or does a meaningful disconnect exist?

-

Identify the fear window — If initial excitement fades and the share price retreats, assess whether the underlying geological thesis has changed or whether the decline reflects sentiment rather than fundamentals.

-

Accumulate on weakness — If the geological case remains intact, a declining share price following an initially positive drill result represents a potential entry point of structural advantage.

-

Scale with information — Add to the position incrementally as subsequent drill results confirm, expand, or modify the discovery thesis.

The next major ASX story will hit our subscribers first

The Private Placement Market and What Its Deterioration Means

Warrant Coverage, Deal Terms, and the Erosion of Sophisticated Investor Advantage

The private placement market in junior mining has historically served as the primary vehicle through which informed, specialist investors gained asymmetric exposure to early-stage discoveries. The standard structure — a discounted share price combined with a full warrant providing leveraged upside — effectively compensated sophisticated investors for taking liquidity risk and for providing capital in environments where broker-led retail money was absent.

That structure has eroded materially. The entry of hedge funds and corporate strategic investors into the junior financing market has increased competition for placement allocations to the point where deal terms have normalised toward broker-led marketed deals without warrants. When an investor receives restricted shares at a modest discount with no warrant coverage, the placement offers no structural advantage over simply buying stock on the open market.

Rule identifies an interesting alternative strategy for investors who prefer a cooperative approach with management: approaching companies before they announce a financing, purchasing shares on the open market to tighten the market, and then facilitating a subsequent financing at a higher price. This approach aligns investor and management incentives while avoiding the fee-extraction dynamic that characterises broker-dependent capital raising strategies.

CEO Capital-Raising Competency: The Underrated Variable in Junior Mining Valuations

Why Management's Investor Acquisition Strategy Matters as Much as the Geology

Among the variables that experienced resource investors assess when evaluating junior mining companies, CEO capital-raising competency remains one of the most consequential and least systematically evaluated. Rule describes a specific line of questioning designed to distinguish between CEOs who have a genuine investor acquisition strategy and those whose approach begins and ends with calling a broker.

The distinction is fundamental. A broker-dependent CEO, when asked about their capital-raising strategy, will describe calling Haywood, Canaccord, or a similar firm. This is not a strategy. It is a fee-paying technique. The broker will market the deal, charge a commission, and move on to the next transaction with no lasting relationship with the investor base it assembled.

A CEO with genuine capital-raising competency can answer the following questions clearly:

- Who is the specific target investor audience for this company?

- What is the documented strategy for reaching that audience, independently of broker intermediation?

- How does the company convert investor interest into committed, long-term capital?

- Has the CEO previously built and retained a loyal shareholder base across multiple financing cycles?

Rule cites the example of specialist investor-relations practitioners who built deep relationships with specific investor constituencies, including wealthy family offices in the Middle East, as examples of effective audience-specific capital-raising that produced durable shareholder bases and lower costs of capital over time.

The ATM Facility Advantage in Junior Mining Capital Markets

How At-the-Market Programs Are Reshaping the Cost of Junior Mining Capital Raises

At-the-market equity programs represent one of the most structurally efficient capital-raising mechanisms available to publicly listed junior mining companies, yet they remain underutilised relative to their potential impact on cost of capital and shareholder value creation.

| Capital Raising Method | Typical Cost | Warrant Dilution | Speed | Investor Loyalty Built |

|---|---|---|---|---|

| Traditional brokered deal | 3–5% commission | Often included | Moderate | Low (transactional) |

| ATM (at-the-market) facility | ~0.5–1% | None | Continuous | High (if PR-supported) |

| Private placement (weak market) | Negotiable | High (warrants common) | Fast | Medium |

| Private placement (hot market) | Low discount | Low/none | Fast | Low |

Rule's experience with ATM programs at Sprott, where physical trust AUM grew from approximately $1.8 billion to approaching $80 billion, illustrates the transformational potential of this approach when combined with sustained investor relations and constituency-building programs. The cost reduction relative to traditional marketed deals is substantial, with Rule citing cost savings of approximately 80 percent compared to brokered transactions.

The critical prerequisite for ATM effectiveness is aftermarket trading volume. An ATM program requires an active secondary market in which the company can sell treasury shares incrementally at prevailing prices. Without the investor constituency and public relations infrastructure to generate sustained trading activity, the facility's utility is limited.

The Infrastructure Proximity Paradigm Shift in Established Mining Camps

Why Deposit Size Thresholds Have Changed in Infrastructure-Rich Jurisdictions

One of the most practically significant shifts in junior mining valuation frameworks over the past decade concerns the minimum viable deposit size in established mining districts. In greenfield jurisdictions where processing infrastructure does not exist, a deposit must be large enough to justify the capital cost of constructing a standalone processing facility. In many cases, this threshold has historically been set at several million ounces for gold or equivalent scale for other commodities.

In established mining camps where milling and processing infrastructure already exists, that calculus has changed fundamentally. A deposit that cannot justify its own mill construction may still represent a compelling acquisition target for an existing operator seeking to maximise throughput from sunk capital.

The insight, which Rule credits to a respected operator in the Abitibi Greenstone Belt, is that a small deposit within 45 to 50 kilometres of an existing mill can be built, mined, and trucked to that facility, eliminating the need to amortise a new processing plant and dramatically improving the deposit's economic viability.

This paradigm shift has practical consequences for junior explorer valuation. Deposits in the 800,000 to 1.2 million ounce range, which Rule had historically avoided due to their inability to support standalone processing economics, now warrant serious examination in established gold camps. Jonathan Goodman made a parallel observation about the Sudbury basin, noting that the district's existing mills and smelters are hungry for feed, fundamentally lowering the deposit-scale threshold for viable development.

Hypothetical scenario illustrating the model: A junior explorer delineates an 850,000-ounce gold deposit in an established mining camp. Under traditional standalone valuation assumptions, the deposit struggles to justify a $350 million processing facility. If an operating mill with spare capacity exists within 50 kilometres, the deposit's capital requirements drop dramatically, its path to production compresses, and its acquisition probability for a throughput-hungry operator increases substantially.

Niche Metals vs. Major Commodities: Where the Risk-Reward Breaks Down

Why Supply Elasticity Makes Minor Metal Investments Structurally Challenging

Rule's approach to commodity selection in the junior mining space reflects a discipline refined through both success and painful experience with niche metals. The structural challenge with minor metals is supply elasticity: any marginal increase in production from a new discovery can materially oversupply the global market, collapsing the price thesis that originally justified the investment.

He applies a rigorous tier-one deposit test before considering any commodity-stage junior investment:

- Does the deposit rank in the lowest-cost quartile within its commodity peer group on a production cost basis?

- Would the deposit, if developed, generate a top-quartile return on invested capital relative to industry peers?

- Is the in-situ resource large enough to constitute a genuine tier-one asset by commodity-specific standards?

- Does marginal new supply from this deposit risk materially oversupplying the target commodity market?

Rule notes that when he applies these criteria to vanadium, titanium, and similar minor metals, he consistently fails to find junior companies that pass all four tests simultaneously. The exception he identifies is rare earths, where qualitative differentiation between deposits is sufficiently large that a small number of genuinely superior projects may justify the structural supply risk.

For most investors, gold, silver, copper, and uranium offer more predictable speculative frameworks precisely because their markets are deep, liquid, and capable of absorbing new supply from a single discovery without catastrophic price consequences. In addition, understanding junior mining risks and rewards at a commodity level is essential before committing capital to any speculative position.

Artificial Intelligence as a Geological Screening Tool

How AI Is Compressing Grassroots Exploration Timelines

The application of artificial intelligence to mineral exploration represents a genuine and near-term shift in discovery economics, though its implications are more nuanced than the headline applications typically suggest. Rule's current view is that AI's most immediate value is not in replacing geological expertise but in dramatically narrowing the search space before human teams deploy to the field.

The specific capability he identifies as transformative is AI's ability to synthesise large, heterogeneous datasets simultaneously: geochemical surveys, spectrally differentiated satellite imagery, historical drill records, and macro-structural geological data. Human geologists working sequentially through these data sources would require years to identify coincident anomalies across a large land package. AI systems can perform this analysis rapidly, identifying the subset of targets that warrant ground-level investigation.

As Rule frames it, AI can examine 1,000 square miles of terrain in Kazakhstan and effectively eliminate 998 square miles from consideration, directing human attention and capital toward the areas with the highest probability of hosting significant mineralisation. The human geologist still needs to walk the terrain, examine outcrops, and apply contextual judgment that no current AI system can replicate. However, the efficiency gain in the pre-field phase is substantial and likely to compress discovery timelines meaningfully. Accurate geological logging codes remain critical throughout this process, as AI tools are only as reliable as the underlying data they interpret.

Seasonal Patterns and Cycle Positioning in Junior Mining

The Summer Liquidity Trough as a Structural Entry Opportunity

Junior mining stocks exhibit well-documented seasonal patterns that create recurring entry opportunities for disciplined investors. The summer months, characterised by reduced institutional participation, lower trading volumes, and the absence of major catalysts, consistently produce price weakness across the sector that is frequently cyclical rather than fundamental in nature.

Rule is explicit about his expectation for a difficult summer for junior mining stocks, describing it as a period he is actively looking forward to from a buying perspective. His approach relies on a pre-built watchlist of companies with known quality at indicative prices, allowing him to respond quickly to price dislocations created by seasonal or geopolitical events rather than attempting to predict their timing.

The analytical challenge for investors is distinguishing between cyclical price weakness, which creates buying opportunities, and structural deterioration, which warrants position reassessment.

| Signal Type | Cyclical Weakness | Structural Deterioration |

|---|---|---|

| Share price decline | Broad sector selloff, no company-specific news | Project setback, management failure, or resource downgrade |

| Volume pattern | Low volume, seasonal | High volume, persistent selling pressure |

| Fundamental change | None, thesis remains intact | Disappointing drill results, capital structure worsens |

| Appropriate response | Accumulate at indicative price | Reassess position and exit thesis if confirmed |

Black swan events, including geopolitical shocks, serve a similar function: they create price dislocations that have no bearing on the underlying geological or commercial merit of quality junior mining companies. Rule's response to such events is not anticipatory positioning based on geopolitical forecasting. It is reactive accumulation based on pre-established watchlists and valuation targets, deployed when market fear drives prices to levels that offer compelling risk-reward relative to assessed fundamental value. According to Rule, the best junior mining companies will absolutely rip in this market once conditions fully align.

FAQ: Rick Rule Junior Mining Drill Hole Market Reaction

Why do junior mining stocks sometimes fall after a positive drill hole result?

A positive drill hole result can trigger a short-term price decline when the initial excitement fades and investors who bought in anticipation of the news sell into the announcement. This sell the news dynamic is common when the result, while geologically positive, does not contain the scale or third-dimension confirmation that institutional investors require to increase position sizes. Thin liquidity in junior markets amplifies these moves.

What is the third dimension in junior mining exploration, and why does it matter?

The third dimension refers to the confirmation of vertical and lateral continuity in a mineralised system through follow-up drilling. A single drill hole establishes that mineralisation exists at a point in space. Multiple holes that confirm depth continuity and lateral extent transform that point into a volumetric resource estimate, which is the foundation of any commercial valuation. Without the third dimension, even high-grade intercepts remain speculative.

What geophysical indicators suggest a drill hole is part of a larger discovery?

Key indicators include the size and intensity of coincident geophysical anomalies surrounding the drill hole, including magnetic, electromagnetic, and gravity signatures. A drill hole that intersects significant mineralisation within a large coincident anomaly suggests the mineralising system extends beyond the single intercept. In contrast, an isolated intercept with no supporting geophysical context offers limited evidence of deposit scale.

Is the current junior mining market in a discovery cycle or an exploration cycle?

Based on current market dynamics, the weight of evidence suggests the market remains in a late-stage exploration phase transitioning toward a discovery market. Elevated exploration budgets are generating high-quality results, but the market's re-rating mechanism has not yet responded at the scale historically associated with true discovery cycles. This transitional positioning is what creates the structural opportunity for informed speculators interested in the Rick Rule junior mining drill hole market reaction framework.

How do private placement terms signal the health of the junior mining capital market?

Generous placement terms, including significant discounts to market price and full warrant coverage, signal that capital is scarce and that promoters must offer substantial incentives to attract investors. Deteriorating terms, including minimal discounts and absent warrants, signal that capital is abundant and competition for placement allocations is intense. The latter environment, which characterises the current market, generally pushes experienced investors toward open-market accumulation strategies.

The Strategic Opportunity in a Market That Has Not Yet Priced the Geology

The current disconnect between geological quality and market price response in junior mining is a cyclical phenomenon with a historical resolution pattern. Discovery markets follow exploration markets with a lag that has typically ranged from one to three years across multiple resource cycles. The geological pipeline is now filling with results that, in a more mature discovery market, would generate substantially larger re-ratings than the market is currently delivering.

For speculators who develop the analytical capability to evaluate the Rick Rule junior mining drill hole market reaction in its proper geophysical context — to distinguish between flashy single-hole intercepts and commercially significant discovery-scale results — and to accumulate positions during the fear-induced pullbacks that follow even genuine discoveries, the current phase offers a structural advantage that is unlikely to persist indefinitely.

The combination of muted market reactions, deteriorating private placement terms driving sophisticated capital toward open-market purchases, a geological pipeline that is beginning to yield high-quality results, and a seasonal weakness period that is expected to offer lower entry prices creates a rare convergence of conditions. The investors who build analytical frameworks now, establish watchlists at disciplined indicative prices, and respond systematically to the opportunities that emerge over the coming months are likely to be well-positioned for the re-rating phase that history suggests follows the current period of underappreciated geological progress.

Disclaimer: This article is intended for educational and informational purposes only and does not constitute financial advice or an investment recommendation. Junior mining investments involve substantial risk, including the potential loss of the entire invested capital. Past performance of resource market cycles is not indicative of future results. Readers should conduct their own due diligence and consult a qualified financial advisor before making any investment decisions. Forward-looking statements and cycle projections referenced in this article are speculative in nature and involve significant uncertainty.

Want to Be First When the Next Major ASX Mineral Discovery Hits the Market?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries are announced on the ASX, transforming complex geological data into clear, actionable insights so investors can act before the broader market catches on — explore historic discovery returns to understand what early positioning in genuinely transformational finds has meant for informed speculators, and begin your 14-day free trial today to secure your edge in the next re-rating cycle.