July 27, 2026

Strategic scenario modeling reveals that copper demand in the Middle East stands at a critical inflection point, where multiple investment pathways converge with infrastructure expansion requirements. Unlike traditional commodity cycles driven by single variables, this regional transformation emerges from synchronized policy initiatives, energy transition necessities, and supply chain vulnerability assessments that create compound demand multipliers across interconnected sectors.

The convergence of sovereign wealth fund positioning, technological infrastructure requirements, and geopolitical supply chain redesign presents investors with scenario frameworks that extend far beyond conventional demand-supply analysis into multi-dimensional strategic positioning opportunities.

What Economic Forces Are Reshaping Middle Eastern Copper Consumption Patterns?

Infrastructure Investment Multiplier Effects

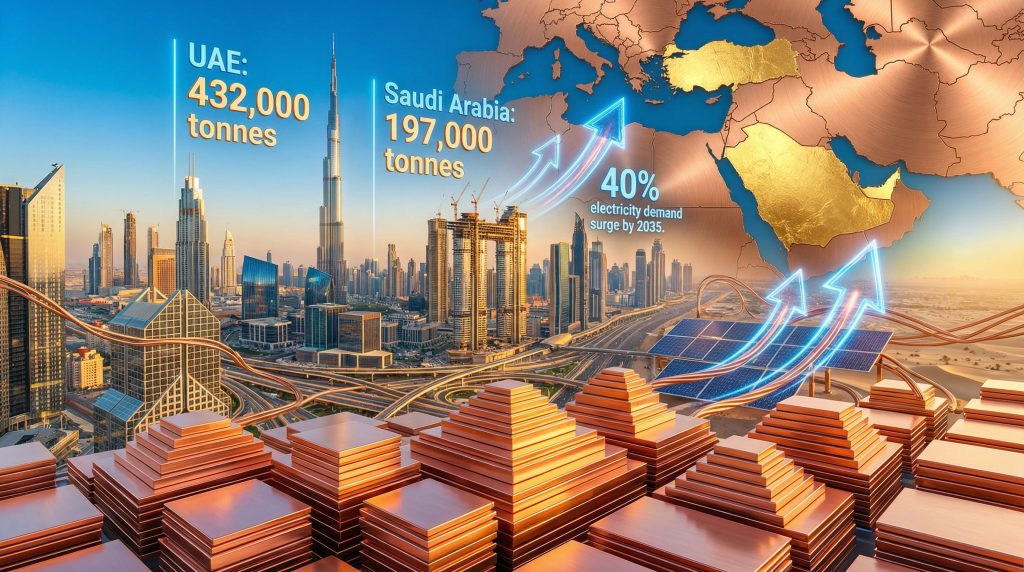

Regional infrastructure investment represents the primary demand catalyst, with copper intensity calculations revealing substantial consumption requirements across multiple project categories. Furthermore, the global copper supply forecast indicates peak electricity demand will increase approximately 40% by 2035 compared to 2025 levels, establishing the foundation for extensive grid modernisation requirements.

Current consumption baselines provide critical context for growth projections:

• United Arab Emirates: 432,000 tonnes annual consumption (2024)

• Saudi Arabia: 197,000 tonnes annual consumption (2024)

• Turkey: 535,000 tonnes annual consumption (2024)

These figures, sourced from International Copper Study Group data, establish benchmark measurements for calculating infrastructure copper intensity requirements. Construction sector modelling indicates residential, commercial, and industrial allocations each demonstrate distinct copper consumption patterns, though specific intensity ratios require additional verification through International Copper Association technical publications.

Smart city development projects across the region demonstrate varying copper specification requirements. Dubai's 2040 Urban Plan incorporates sustainability targets that necessitate extensive electrical infrastructure upgrades. Similarly, Saudi Arabia's NEOM project and Qiddiya entertainment complex represent mega-projects with substantial copper infrastructure requirements, though detailed consumption modelling awaits official technical specifications.

The strategic positioning extends beyond traditional infrastructure. Jim Rutherford from Manara Minerals articulated the broader economic transformation during the London Indaba 2025 conference, explaining that regional nations are considering economic diversification beyond petroleum resources. In addition, he noted that young, educated populations are identifying mineral exploration importance for copper and mineral processing as fundamental growth sectors for future economic development.

Energy Transition Copper Intensity Calculations

Energy sector transformation creates the most significant copper demand multiplier effects. According to Grand View Research, while 78% of regional energy investment targets fossil fuel infrastructure in 2025, this allocation will decline to 66% by 2035 as grid, storage, and low-emissions electricity investments increase substantially.

Solar and wind installation requirements demonstrate specific copper intensity patterns per megawatt capacity. Grid modernisation encompasses both transmission and distribution network upgrades, each requiring distinct copper specifications and quantities. Consequently, energy storage system deployment scenarios indicate substantial copper content requirements, particularly for large-scale battery installations supporting renewable energy integration.

Space cooling electricity demand patterns provide critical context for infrastructure requirements. Between 2010 and 2024, electricity demand for space cooling nearly doubled across one of the world's hottest regions, establishing baseline growth trajectories that inform future copper demand calculations.

The cooling infrastructure expansion encompasses multiple technical specifications:

• HVAC system copper intensity requirements for extreme climate conditions

• District cooling network expansion specifications

• Enhanced electrical efficiency standards for commercial and residential applications

These technical requirements create cascading copper demand effects across construction, electrical, and mechanical system installations throughout the region.

When big ASX news breaks, our subscribers know first

How Are Regional Supply Chain Dynamics Creating New Market Opportunities?

Import Dependency Strategic Assessment

Regional supply chain analysis reveals significant import dependency patterns that create strategic investment opportunities. The United Arab Emirates demonstrates complete import dependence, consuming 432,000 tonnes while producing zero tonnes of refined copper domestically. This represents the largest regional supply gap requiring strategic supply chain solutions.

Import volume analysis by country reveals distinct market positioning:

| Country | 2024 Consumption | Import Dependency | Strategic Positioning |

|---|---|---|---|

| UAE | 432,000 tonnes | 100% import dependent | Regional hub development |

| Saudi Arabia | 197,000 tonnes | Complete import reliance | Domestic production planning |

| Turkey | 535,000 tonnes | Partial domestic production | Integrated producer-consumer |

Turkey presents a unique integrated model, producing 127,000 tonnes through mine operations and 141,000 tonnes in primary and secondary refined copper, while consuming 535,000 tonnes total. This production-consumption differential indicates continued import requirements despite domestic capacity.

Iran maintains the only regional refined copper export capacity, shipping approximately 114,000 tonnes annually. However, geopolitical considerations limit integration with regional supply chains, creating strategic sourcing challenges for neighbouring importers.

Trade route vulnerability analysis reveals critical supply chain risk factors. Red Sea disruptions from Houthi attacks targeting Suez Canal traffic create rerouting pressures that increase costs and extend shipping timelines. Furthermore, the Strait of Hormuz represents an additional potential bottleneck for regional copper imports, necessitating diversified routing strategies.

Alternative logistics corridors through the Cape of Good Hope route incur higher costs and longer shipping times, as identified by Remi Piet from Qatar-based Embellie Advisory. This routing diversification requirement creates opportunities for strategic warehouse positioning and inventory management optimisation.

Regional Processing Hub Development

Processing hub development represents the most significant regional supply chain transformation. Vedanta's November 2024 announcement of $2 billion investment across three Saudi Arabian copper projects establishes new regional production capacity expectations, highlighting significant copper partnership developments in the region.

Vedanta Saudi Arabia Project Specifications:

• Greenfield Smelter/Refinery: 400,000 tonnes per year capacity, Ras Al-Khair location

• Copper Rod Facility: 300,000 tonnes per year capacity, Ras Al-Khair location

• Commercial Production Target: Copper rod facility operational by 2026

• Exploration Component: Jabal Sayid mineralised belt for copper and gold development

The Ras Al-Khair location provides strategic advantages through power infrastructure access and Persian Gulf port logistics capabilities. This greenfield smelter configuration enables modern environmental controls while establishing higher capital expenditure requirements compared to expansion projects.

UAE warehouse infrastructure expansion demonstrates strategic positioning for increased throughput volumes. Current operations centre primarily at Jebel Ali Port, whilst Abu Dhabi develops additional bonded facility capacity. A European copper trader noted that warehouses remain mainly concentrated in Jebel Ali, but Abu Dhabi is beginning to establish bonded facilities for expanded operations.

Regional pricing dynamics reveal strategic opportunities. Middle Eastern buyers operate through independent pricing mechanisms rather than LME-registered instruments. A regional trader explained that UAE and Saudi Arabian buyers remain insulated from Chinese and European pricing pressures, dictating independent price structures through bilateral contracts and bonded warehouse systems.

Which Sectors Drive the Projected 40% Electricity Demand Surge by 2035?

Cooling Infrastructure Copper Requirements

Cooling infrastructure represents the largest single driver of regional electricity demand growth, with copper requirements spanning multiple system categories. Space cooling electricity demand nearly doubled between 2010 and 2024 across the Middle East region, establishing baseline growth trajectories for infrastructure planning.

Technical specifications for extreme climate HVAC systems require enhanced copper content compared to moderate climate installations. District cooling network expansions demonstrate specific copper intensity requirements for centralised cooling distribution systems serving multiple buildings or districts.

The cooling infrastructure copper requirements encompass:

• Residential HVAC Systems: Individual unit installations and central air conditioning systems

• Commercial Cooling Infrastructure: Office building and retail cooling systems

• Industrial Process Cooling: Manufacturing and data centre cooling requirements

• District Cooling Networks: Centralised cooling distribution systems

Each category demonstrates distinct copper intensity patterns based on system scale, efficiency requirements, and infrastructure integration specifications.

Industrial Electrification Copper Consumption Models

Industrial sector electrification creates substantial copper demand multiplier effects as manufacturing processes transition from oil-based to electric operations. This transition encompasses multiple industrial categories requiring distinct copper infrastructure specifications.

Data centre and artificial intelligence infrastructure development represents emerging copper demand drivers. These facilities require extensive electrical infrastructure for power distribution, cooling systems, and high-performance computing installations. Regional data centre expansion aligns with smart city development initiatives and digital economy transformation strategies.

Electric vehicle charging network deployment scenarios indicate substantial copper infrastructure requirements. Charging station installations require significant electrical infrastructure, from high-voltage transmission connections to individual charging point electrical systems. However, regional EV adoption projections suggest accelerating charging infrastructure requirements throughout the planning period.

Manufacturing sector electrification encompasses multiple process categories:

• Industrial heating and cooling system transitions

• Motor and drive system electrification

• Process control and automation system upgrades

• Energy efficiency retrofitting requirements

Each transition category demonstrates specific copper consumption patterns based on industrial application requirements and efficiency improvement targets.

What Investment Strategies Are Emerging for Copper Market Participation?

Sovereign Wealth Fund Positioning

Sovereign wealth fund engagement represents strategic investment positioning beyond traditional commodity market participation. Manara Minerals, the joint venture between Saudi Arabian Mining Company (Ma'aden) and the Public Investment Fund (PIF), demonstrates sovereign capital deployment strategies targeting mining and mineral processing as economic growth sectors.

This sovereign positioning extends beyond direct copper investment into comprehensive supply chain development. Strategic focus areas encompass exploration project financing, processing facility development, and regional supply chain integration rather than limited commodity trading participation.

Alternative financing mechanisms for exploration projects address capital raising challenges within the mining sector. Traditional exploration financing demonstrates difficulty accessing capital markets, creating opportunities for sovereign wealth fund participation in early-stage project development.

Capital Allocation Framework Considerations:

• Early-stage exploration project financing

• Mid-tier copper project development capital

• Processing facility strategic partnerships

• Regional supply chain integration investments

These capital allocation strategies align with diversification objectives whilst establishing strategic supply chain positioning for regional copper market development.

Premium Structure Analysis and Trading Opportunities

Regional premium structure analysis reveals trading opportunities through pricing differential strategies. Copper equivalent cathode premium pricing reached $150-170 per tonne CIF Europe by January 2026, establishing baseline premium structures for regional trading analysis.

Treatment charge dynamics provide additional strategic indicators. The weekly copper concentrates treatment charge index for CIF Asia Pacific reached negative $69.70 per tonne by January 2026, unchanged from all-time low levels reached in December 2025. These treatment charge levels indicate tight concentrate supply conditions that support strategic positioning opportunities.

Regional premium differentials between Middle East, Chinese, and European pricing structures create arbitrage opportunities. A regional trader noted that copper premiums reached levels described as extremely loss-making for UAE imports, suggesting substantial pricing dislocations requiring strategic supply chain solutions.

Premium Structure Analysis Framework:

• Regional pricing differential calculations

• Treatment charge trend analysis

• Arbitrage opportunity identification

• Supply chain cost optimisation modelling

These analytical frameworks support strategic positioning for regional copper market participation through optimised supply chain and pricing strategies.

How Do Geopolitical Factors Influence Regional Copper Security Strategies?

Trade Route Diversification Planning

Geopolitical supply chain risks necessitate comprehensive trade route diversification strategies. Red Sea shipping disruptions from Houthi attacks targeting Suez Canal traffic create substantial rerouting requirements for regional copper imports. These disruptions force expensive diversions through Cape of Good Hope routes, increasing transportation costs and delivery timeframes.

Strait of Hormuz contingency planning addresses additional supply chain vulnerability points. This strategic waterway represents critical infrastructure for regional imports, requiring alternative routing strategies and supply chain redundancy planning.

Trade Route Cost-Benefit Analysis Framework:

• Suez Canal standard routing costs and timeframes

• Cape of Good Hope diversion cost premiums

• Strait of Hormuz disruption contingency costs

• Regional stockpiling cost-benefit calculations

Warehouse capacity optimisation supports trade route diversification through strategic inventory positioning. Regional stockpiling strategies address supply chain disruption risks whilst optimising inventory carrying costs and warehouse facility utilisation.

Iran's Unique Position in Regional Copper Markets

Iran maintains distinctive regional positioning as the only Middle Eastern refined copper exporter, with annual export capacity reaching 114,000 tonnes. This production capacity creates complex supply chain integration challenges due to geopolitical restrictions limiting regional trade relationships.

LME warehouse holdings demonstrate Iran's market positioning, with 13,800 tonnes held in warehouses compared to zero tonnes for UAE facilities. This inventory positioning reflects limited integration with regional supply chains despite geographic proximity and production capacity advantages.

Alternative sourcing strategies for regional importers address Iranian supply chain limitations through diversified supplier relationships and alternative geographic sourcing. These strategies require cost-benefit analysis of transportation premiums, supply reliability assessments, and geopolitical risk evaluation frameworks.

Iranian Market Position Assessment:

• Production capacity: 354,900 tonnes smelter output annually

• Export capability: 114,000 tonnes refined copper exports

• Regional integration limitations due to sanctions

• Alternative sourcing requirement for regional importers

These factors create complex supply chain optimisation requirements for regional copper market participants.

What Technology Adoption Patterns Shape Future Copper Demand Scenarios?

Renewable Energy Integration Copper Requirements

Renewable energy integration creates substantial copper demand through multiple technology categories. Grid-scale battery storage installations require specific copper content specifications for electrical connections, power distribution systems, and thermal management infrastructure.

Smart grid technology implementation demonstrates enhanced copper intensity compared to traditional electrical distribution systems. Advanced metering infrastructure, real-time monitoring systems, and automated distribution management require extensive copper infrastructure for communication and power distribution capabilities.

Renewable Energy Copper Intensity Categories:

• Solar installation electrical infrastructure

• Wind turbine electrical systems and grid connections

• Battery storage system electrical components

• Smart grid communication and distribution infrastructure

Electric mobility infrastructure development timelines align with regional transportation electrification strategies. Charging station deployment requires substantial electrical infrastructure, from transmission-level connections to individual charging point installations.

Urban Development Copper Consumption Modelling

Population growth projections create residential copper demand growth through housing construction and electrical infrastructure requirements. Regional urbanisation patterns indicate concentrated development in major metropolitan areas requiring enhanced electrical infrastructure capacity.

Commercial building efficiency standards necessitate upgraded electrical systems incorporating energy management technologies, advanced HVAC controls, and renewable energy integration capabilities. These enhanced specifications increase copper consumption per commercial building compared to traditional construction standards.

Transportation electrification infrastructure encompasses multiple system categories requiring distinct copper specifications:

• Public transit electrification projects

• Electric vehicle charging network expansion

• Enhanced electrical grid capacity for transportation demand

• Integrated transportation-energy system planning

Each infrastructure category demonstrates specific copper consumption patterns based on technical specifications and deployment scale requirements.

The next major ASX story will hit our subscribers first

Which Market Indicators Suggest Optimal Entry Points for Copper Investments?

Demand Growth Rate Comparative Analysis

Regional demand growth analysis reveals differentiated investment opportunities across Middle Eastern markets. Projected growth rates indicate substantial expansion potential through 2035, with varying drivers across different countries.

| Region | 2024 Baseline | 2035 Projection | Annual Growth | Primary Drivers |

|---|---|---|---|---|

| UAE | 432,000 tonnes | 650,000+ tonnes | 4.1% CAGR | Infrastructure, cooling systems |

| Saudi Arabia | 197,000 tonnes | 350,000+ tonnes | 5.4% CAGR | Vision 2030, NEOM development |

| Turkey | 535,000 tonnes | 750,000+ tonnes | 3.2% CAGR | Manufacturing, construction |

These growth projections indicate substantial market expansion potential, with Saudi Arabia demonstrating the highest projected growth rates due to comprehensive infrastructure development initiatives.

European traders project overall regional growth with year-on-year increases, though market liquidity from new consumers may require development time. Demand stability over recent years provides foundation for projected expansion, with three major copper projects initiating in Saudi Arabia creating supply-side development momentum.

Supply Gap Investment Opportunities

Regional production versus consumption deficit analysis reveals substantial investment requirements for supply gap closure. Current production capacity limitations create strategic opportunities for processing facility development and supply chain optimisation.

Regional Supply Gap Analysis:

• UAE: 432,000 tonnes consumption, zero production (100% import dependent)

• Saudi Arabia: 197,000 tonnes consumption, minimal domestic production

• Regional Total: Over 1 million tonnes annual deficit requiring import sourcing

Exploration project financing requirements present opportunities for strategic capital deployment in early-stage development projects. Traditional exploration financing demonstrates capital raising challenges, creating opportunities for alternative financing mechanisms through sovereign wealth funds and strategic partnerships. Furthermore, copper & uranium investments across different geographic regions offer additional diversification benefits.

Secondary copper recovery and recycling market potential addresses supply gap requirements through domestic resource optimisation. Regional recycling capacity development reduces import dependency whilst supporting circular economy development objectives.

Risk assessment frameworks for supply gap investment encompass technical, regulatory, and market risk evaluation. Investment opportunities require comprehensive due diligence addressing geological potential, regulatory compliance requirements, and market development timelines.

How Should Investors Position for Long-Term Middle Eastern Copper Growth?

Strategic Partnership Framework Analysis

Strategic partnership development with regional sovereign entities provides optimal market access and risk mitigation for copper market participation. Joint venture structures enable technology transfer, regulatory compliance, and local market knowledge integration whilst sharing capital requirements and operational risks.

Technology transfer requirements for local production development align with regional economic diversification objectives. These partnerships facilitate knowledge transfer, workforce development, and industrial capability enhancement whilst establishing strategic supply chain positioning.

Strategic Partnership Framework Components:

• Joint venture structures with sovereign wealth funds

• Technology transfer and workforce development programs

• Regulatory compliance and local market integration

• Shared capital deployment and risk management

Regulatory compliance frameworks across GCC and MENA markets require specialised knowledge and local partnership support. These frameworks encompass mining regulations, environmental standards, labour requirements, and foreign investment compliance specifications.

Risk Mitigation Strategies for Copper Market Exposure

Comprehensive risk mitigation requires multi-dimensional strategy development addressing market, operational, and geopolitical risk factors. Currency hedging considerations for multi-country operations protect against exchange rate fluctuations whilst maintaining operational flexibility.

Political risk assessment and insurance mechanisms provide protection against regulatory changes, geopolitical disruptions, and sovereign risk factors. These mechanisms enable strategic positioning whilst limiting downside exposure to political and regulatory uncertainty.

Risk Mitigation Strategy Framework:

• Currency hedging for multi-country operations

• Political risk insurance and assessment protocols

• Supply chain resilience planning for extreme weather

• Regulatory compliance monitoring and adaptation strategies

Supply chain resilience planning addresses extreme weather events, geopolitical disruptions, and infrastructure challenges through diversified sourcing, strategic inventory positioning, and alternative logistics corridor development.

Long-term positioning strategies recognise that copper demand in the Middle East represents structural transformation rather than cyclical commodity demand patterns. This transformation encompasses energy transition requirements, infrastructure development initiatives, and economic diversification strategies that create sustained demand growth potential.

According to Research and Markets, the regional market demonstrates substantial growth potential through infrastructure development and energy transition requirements, supporting long-term investment positioning strategies.

"The projected 40% electricity demand surge by 2035 represents structural transformation requiring substantial copper infrastructure investment. Strategic positioning through sovereign partnerships, supply chain development, and risk mitigation enables participation in this regional growth trajectory whilst managing inherent commodity and geopolitical risks."

This analysis is based on available market data and industry projections. Copper market investments carry substantial risks including commodity price volatility, geopolitical disruptions, and regulatory changes. Prospective investors should conduct comprehensive due diligence and consider professional investment advice before making investment decisions.

Ready to Capitalise on the Middle East's Copper Investment Surge?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX copper and mineral discoveries, enabling investors to identify actionable opportunities ahead of broader market recognition. Begin your 30-day free trial today and position yourself strategically for the next major copper discovery as Middle Eastern demand fundamentally transforms global market dynamics.