June 11, 2026

Global economic turbulence has reshaped commodity markets throughout 2026, with inflationary pressures from geopolitical conflicts creating complex dynamics across industrial metals. The intersection of monetary policy uncertainty, supply chain disruptions, and shifting industrial demand patterns has fundamentally altered how market participants assess risk and value in base metals markets. Understanding these macroeconomic forces becomes essential for analyzing price movements in copper markets, particularly within China's dominant consumption framework where copper prices in China serve as critical indicators for global economic health.

China's Copper Market Structure and Economic Indicators

China's position as the world's largest copper consumer creates unique pricing dynamics that extend far beyond simple supply-demand calculations. The nation's 745,283 tonnes of combined LME and SHFE copper inventories as of March 2026 represents a 56% increase from the previous month, illustrating how rapidly market conditions can shift based on production cycles and demand patterns.

Key Market Metrics:

- SHFE April contract prices declined from Yn103,920/t ($15,104/t) to Yn95,400/t ($14,082/t)

- LME three-month copper fell from $13,296/t to $12,340.50/t

- Combined price decline over three weeks: 8.3% (SHFE) and 7.2% (LME)

The relationship between Chinese copper consumption and broader economic health operates through multiple transmission mechanisms. Manufacturing activity, infrastructure development, and industrial capacity utilisation all influence copper market trends, creating price signals that often precede major economic shifts.

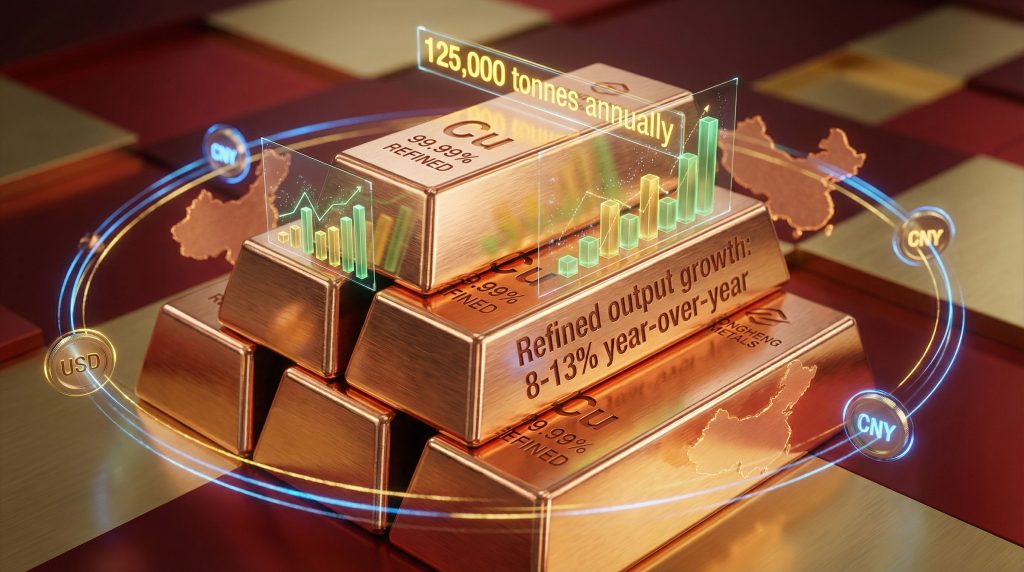

China's refined copper output demonstrated remarkable resilience in early 2026, with year-over-year growth ranging from 8-13% during January-February despite tightening concentrate markets. This expansion reflects strategic investments in processing capacity that continue even amid supply chain constraints, contributing to the copper supply forecast for the region.

Industrial Demand Evolution Across Sectors

The transformation of China's copper demand profile has accelerated with the transition toward electrification and renewable energy infrastructure. However, recent policy adjustments affecting purchase incentives have created notable shifts in growth expectations across key consumption sectors.

| Sector | 2025 Performance | 2026 Forecast | Primary Growth Drivers |

|---|---|---|---|

| New Energy Vehicles | +27% growth | +2% growth | Reduced purchase incentives |

| Power Grid Infrastructure | Stable demand | Moderate expansion | Ongoing grid modernisation |

| Construction | Declining activity | Continued weakness | Property sector challenges |

| Export Manufacturing | Mixed performance | Cautious recovery | Global trade conditions |

The new energy vehicle sector exemplifies these demand shifts. China's NEV output and sales declined 8.8% and 6.9% respectively to 1.735 million and 1.71 million units during January-February 2026, following policy changes that reduced purchase incentives.

Furthermore, market analysts project copper demand from China's new-energy sectors to grow by approximately 2% to exceed 3.3 million tonnes in 2026, substantially lower than the estimated 27% increase recorded in 2025.

When big ASX news breaks, our subscribers know first

Inventory Dynamics and Price Formation Mechanisms

Copper inventory management in China operates through sophisticated cycles that influence pricing across multiple timeframes. The rapid accumulation to 745,283 tonnes in combined exchange inventories during March 2026 demonstrates how quickly supply-demand imbalances can emerge.

The inventory build reflected several converging factors:

- Higher refined output exceeding immediate consumption needs

- Slower-than-expected demand recovery following the February lunar new year holiday

- Limited downstream restocking activity amid price uncertainty

- Weak industrial buyer confidence affecting procurement strategies

When combined inventories exceed normal consumption ratios, downward pricing pressure typically emerges as industrial buyers adjust procurement strategies to reflect abundant near-term supply availability.

Treatment Charge Indicators:

The Argus weekly TC index deteriorated significantly from -$44.60/t and -4.46¢/lb on December 31, 2025, to -$60.20/t and -6.02¢/lb on March 13, 2026. This 36% deterioration over 2.5 months indicates acute tightening in concentrate markets, creating the paradox of expanding refined output amid supply constraints.

Chinese smelters maintained operations by accepting increasingly negative treatment and refining charges, suggesting confidence in future demand recovery or financial incentives to sustain production volumes. This willingness to absorb higher effective costs for concentrate demonstrates the strategic importance Chinese refiners place on maintaining market share and operational continuity.

Currency Relationships and Dollar Strength Impact

The inverse relationship between USD strength and commodity prices created particular challenges for Chinese copper buyers throughout March 2026. The dollar index reached a four-month high of 100.54 on March 13, representing a 1.73% appreciation from 98.826 just three days earlier.

This currency movement coincided with copper prices in China experiencing significant declines, creating a dual headwind effect:

- Direct Cost Impact: Copper priced in USD becomes more expensive for Chinese buyers when the dollar strengthens

- Financing Costs: Higher USD funding costs increase the effective price of copper purchases

- Hedging Expenses: Currency volatility raises the cost of FX risk management

- Opportunity Costs: Stronger dollar often coincides with higher real interest rates, increasing the carrying cost of commodity inventories

Geopolitical Risk Premium

The strengthening dollar was partly driven by oil price volatility, with ICE front-month May Brent crude increasing from $91.40/bbl to $109.65/bbl between March 10-18, 2026. Market participants expressed concerns that sharply higher oil prices driven by Middle East conflict could delay US monetary easing, thus prolonging USD strength.

In addition, the Federal Reserve's decision to maintain target rates at 3.5-3.75% on March 18, while continuing to project only one quarter-point cut in 2026, reinforced expectations of sustained interest rate differentials between the US and other major economies.

Production Capacity Expansion Despite Supply Constraints

China's refined copper production growth demonstrates the complexity of global supply chain dynamics. Despite concentrate availability constraints indicated by deteriorating treatment charges, Chinese refiners expanded output by 8-13% year-over-year in early 2026.

New Capacity Additions:

Liangshan Copper's new 125,000 tonnes per year nameplate capacity refinery planned to begin trial operations in March 2026, representing approximately 1-2% of China's total refined capacity. This facility addition exemplifies continued strategic investment in processing capability despite challenging input costs.

However, for context on international production, US copper production faces different challenges compared to China's expansion-focused approach.

Import Dependency Metrics:

China imported 4.934 million tonnes of copper concentrate in the first two months of 2026, reflecting a 5% year-over-year increase. This growth in concentrate imports, despite tightening availability and deteriorating treatment charges, indicates sustained commitment to maintaining production volumes.

The concentrate import data suggests annual consumption approaching 29.6 million tonnes if the early-year pace continues, highlighting China's critical dependence on global mining operations for raw material supply. This dependency becomes particularly relevant when considering developments in regions such as Argentina's major copper system.

Strategic Implications of Capacity Expansion

Chinese smelters' willingness to accept increasingly negative treatment charges while expanding capacity reflects several strategic considerations:

- Market Share Protection: Maintaining production volumes to preserve competitive positioning

- Long-term Demand Confidence: Investment decisions based on multi-year electrification trends

- Operational Efficiency: Leveraging scale economies to offset input cost pressures

- Financial Incentives: Possible policy support or financing advantages for domestic production

Demand Sector Analysis and Policy Implications

The moderation in China's new energy vehicle sector growth illustrates how policy adjustments can rapidly alter industrial commodity demand patterns. The reduction in NEV purchase incentives created immediate impacts on copper consumption forecasts, demonstrating the sensitivity of industrial metals to government policy decisions.

Downstream Market Indicators:

Domestic spot premiums assessed by market analysts have traded at discounts to SHFE futures since mid-January 2026, indicating limited restocking interest among downstream fabricators. This pricing relationship suggests weak immediate demand relative to available supply, contributing to inventory accumulation.

Consequently, China's imports of unwrought copper and semi-finished products declined 16% year-over-year to 700,000 tonnes during January-February, reflecting reduced import appetite as arbitrage opportunities remained closed due to pricing dynamics.

Construction Sector Challenges

The ongoing weakness in China's property and infrastructure development sectors continues to weigh on copper demand. Construction-related copper consumption faces headwinds from:

- Reduced residential development activity

- Cautious infrastructure investment amid fiscal constraints

- Slower urbanisation growth rates

- Regulatory restrictions on property sector financing

Medium-Term Supply-Demand Balance Considerations

Despite near-term pricing weakness, structural factors suggest potential tightening in copper markets over multi-year horizons. Global supply constraints combined with long-term electrification trends support expectations of higher price levels, though timing remains uncertain given current inventory levels.

Supply-Side Risk Factors:

- African copper belt production vulnerabilities due to regional conflicts

- Concentrate availability constraints affecting global refining operations

- Mining project development delays amid capital allocation challenges

- Environmental and regulatory pressures on existing operations

For instance, investors seeking to understand broader market dynamics often examine copper investment insights to gauge future supply-demand balance considerations.

Demand Growth Projections:

While immediate growth has moderated, longer-term copper demand drivers remain intact:

- Electric vehicle adoption continuing despite policy adjustments

- Power grid modernisation requirements for renewable energy integration

- Industrial automation and digitalisation trends

- Export manufacturing recovery as global trade conditions stabilise

The next major ASX story will hit our subscribers first

Risk Management and Trading Strategy Adaptations

Market participants have adapted their approaches based on the complex interplay of inventory levels, currency movements, and demand forecasts. The relationship between spot premiums and futures prices provides crucial signals for trading decisions and risk management strategies.

Key Monitoring Indicators:

- Combined exchange inventory levels relative to historical consumption patterns

- Treatment charge trends indicating concentrate market tightness

- New energy sector policy developments affecting demand growth

- USD/CNY exchange rate stability and central bank intervention signals

- Downstream sector restocking activity and fabricator sentiment

Chinese copper consumers increasingly employ sophisticated hedging strategies to manage price volatility, including currency hedging to protect against yuan depreciation and supply contract diversification to reduce dependence on spot market purchases. Moreover, tracking real-time copper prices helps inform these strategic decisions.

Market Psychology and Sentiment Factors

The copper market's response to inventory builds and currency movements reflects broader sentiment regarding China's economic recovery trajectory. Market participants weigh immediate supply-demand imbalances against longer-term structural growth drivers, creating volatility as expectations shift.

Investor Positioning Considerations:

Professional investors monitor copper prices in China as a leading indicator for:

- Global economic growth momentum

- Industrial commodity sector performance

- Currency policy effectiveness

- Geopolitical risk premium adjustments

- Central bank monetary policy coordination

The complexity of factors influencing copper prices in China makes the market a sophisticated gauge of both domestic economic health and international commodity market conditions. Understanding these interconnected dynamics requires continuous analysis of production data, inventory levels, policy developments, and macroeconomic trends.

Disclaimer: This analysis is based on market data and industry reports current as of March 2026. Commodity prices and market conditions are subject to rapid change based on economic, political, and supply chain developments. Investors should conduct independent research and consider professional advice before making investment decisions.

Looking for the Next Copper Market Breakthrough?

Understanding copper price dynamics in China provides valuable insights, but savvy investors know that individual discovery announcements can drive exceptional returns within hours. Discovery Alert's proprietary Discovery IQ model delivers instant notifications when significant ASX copper discoveries are announced, transforming complex mineral data into actionable trading opportunities that position you ahead of broader market movements.