July 22, 2026

Copper market trends 2026 reflect a fundamental shift in global industrial architecture. Unlike cyclical commodity rallies driven by speculative positioning, copper's ascension stems from structural demand transformation across digital infrastructure and energy transition sectors. The metal has evolved beyond its traditional industrial applications to become a critical input for technologies that define modern economic competitiveness.

What Makes Copper the Strategic Metal of 2026?

The simultaneous expansion of artificial intelligence infrastructure and renewable energy systems creates unprecedented copper demand intensity. Modern data centers require sophisticated electrical architectures that consume substantially more copper per unit of computing capacity than traditional facilities. This demand intersects with grid modernization requirements as utilities upgrade transmission networks to accommodate distributed renewable energy sources.

The electrification of transportation systems further amplifies copper requirements through charging infrastructure development. Each electric vehicle charging station incorporates copper-intensive transformers, cabling, and grid connection equipment. Market analysis indicates that charging network buildout represents a multiplier effect beyond the copper content within vehicles themselves.

Furthermore, the copper-uranium investment outlook demonstrates how strategic metals are becoming interconnected in portfolio strategies. Investors are recognising the correlation between critical materials needed for energy transition.

Key demand multipliers include:

• Hyperscale data center deployment across multiple geographic regions

• Edge computing infrastructure requiring distributed electrical systems

• Smart grid integration demanding enhanced transmission capacity

• Renewable energy interconnection infrastructure

• Industrial process electrification across manufacturing sectors

Supply Chain Vulnerabilities Reshaping Market Dynamics

Copper supply chains exhibit structural imbalances between mining capacity and downstream processing capabilities. While mine production faces geological and regulatory constraints, the refinement and smelting infrastructure presents an even tighter bottleneck. This creates a scenario where raw copper concentrate availability may exceed the industry's ability to convert it into finished metal products.

Geographic concentration in copper processing creates additional supply vulnerabilities. The specialised knowledge and capital requirements for modern smelting operations limit the number of facilities capable of meeting refined copper specifications. Environmental regulations further constrain expansion of processing capacity in developed markets, while emerging market facilities face technology transfer limitations.

Critical infrastructure constraints:

• Processing capacity lagging behind mine development timelines

• Environmental permitting delays for new smelting facilities

• Skilled workforce shortages in specialised metallurgical operations

• Energy-intensive processing requirements during grid transition periods

• Transportation infrastructure limitations for copper concentrate movement

When big ASX news breaks, our subscribers know first

How Are Global Supply Deficits Reshaping Price Discovery?

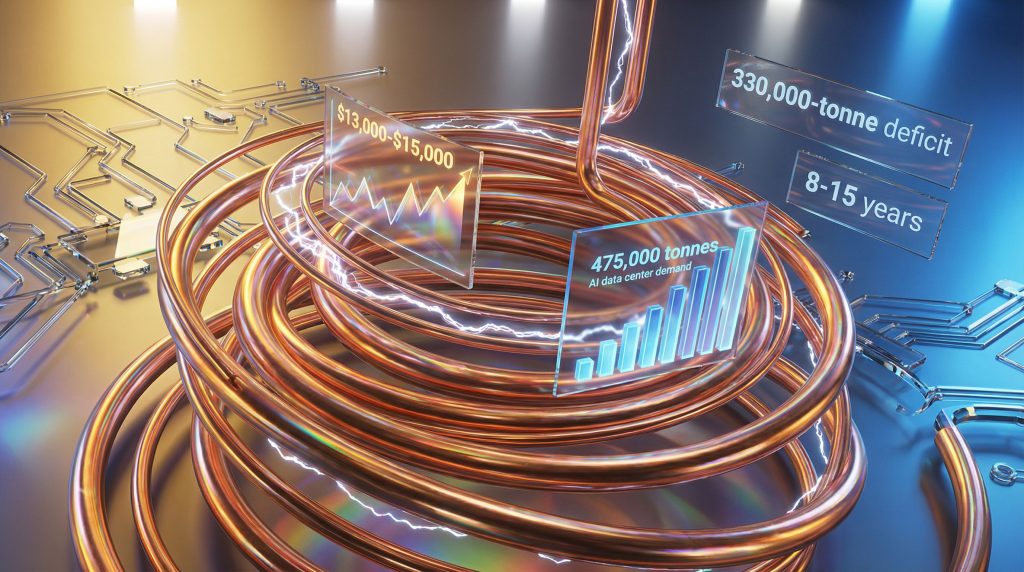

Supply deficit projections for 2026 vary significantly across forecasting institutions, reflecting uncertainty about both demand acceleration and supply response mechanisms. The divergence in deficit estimates suggests that traditional supply-demand modelling struggles to capture the complexity of structural demand shifts occurring simultaneously across multiple sectors.

Structural Deficit Analysis Across Major Forecasting Houses

Investment bank copper market trends 2026 forecasts demonstrate considerable variation in deficit magnitude expectations. This dispersion reflects different assumptions about the pace of infrastructure deployment, the responsiveness of mining operations to higher prices, and the effectiveness of demand destruction mechanisms at elevated price levels.

Market analysts emphasise that unlike purely financial assets, copper markets remain anchored to industrial consumption patterns. This fundamental characteristic limits the sustainability of price levels that disconnect significantly from underlying physical demand, even when supply constraints provide theoretical justification for higher valuations.

In addition, the global copper supply forecast indicates significant regional variations in production capabilities and constraints.

Deficit projection framework:

• Mine production growth constrained by development lead times

• Processing bottlenecks creating refined copper shortages

• Inventory drawdowns across major trading exchanges

• Regional supply-demand imbalances affecting price discovery

• Speculative positioning amplifying fundamental supply tensions

The Scrap Supply Ceiling and Recycling Constraints

Copper recycling faces technological and economic limitations that prevent scrap supply from substantially alleviating primary supply deficits. The complexity of modern electronic devices complicates copper recovery, while the energy intensity of recycling operations creates cost thresholds that must be overcome for economic viability.

Secondary copper supply exhibits price elasticity, with higher prices encouraging increased scrap mobilisation. However, this response mechanism operates with significant lag times and faces diminishing returns as easily accessible scrap sources become exhausted. The quality differential between recycled and primary copper also limits substitutability in certain applications.

Recycling market dynamics:

• Maximum theoretical scrap contribution rates plateau below 25% of total supply

• Technology limitations in complex electronic waste processing

• Economic thresholds for scrap mobilisation at different price levels

• Quality specifications limiting recycled copper applications

• Infrastructure constraints for scrap collection and processing

Why Are Investment Banks Split on 2026 Price Targets?

Investment bank price forecasts for copper market trends 2026 exhibit substantial variation, reflecting fundamental disagreements about demand sustainability and supply response capabilities. The January 2026 price spike created a benchmark that challenges traditional forecasting methodologies, as spot prices exceeded even the most optimistic analyst projections.

The Bull Case: Structural Supply Constraints Meet Demand Acceleration

Bullish copper forecasts centre on the convergence of multiple demand drivers occurring simultaneously with constrained supply response capabilities. Energy transition requirements, digital infrastructure expansion, and traditional industrial demand combine to create unprecedented consumption growth trajectories that existing mining operations cannot accommodate.

The bull case emphasises that copper's role in electrification makes it irreplaceable in many applications, limiting substitution possibilities even at elevated price levels. Grid modernisation and renewable energy integration require copper-intensive infrastructure that cannot be economically redesigned to use alternative materials.

However, record-high copper prices have already prompted some industrial adaptation responses across certain sectors.

Bullish scenario foundations:

• Persistent supply bottlenecks across the processing chain

• Infrastructure investment acceleration in developed markets

• Limited substitution possibilities in critical applications

• Mine development timelines unable to match demand growth

• Strategic stockpiling by governments and major consumers

The Bear Case: Demand Destruction and Industrial Adaptation

Bearish forecasts emphasise copper's vulnerability to demand destruction when prices reach levels that trigger industrial adaptation responses. Manufacturers facing elevated input costs implement strategies including deferred purchases, material substitution, design optimisation, and metal conservation measures that reduce per-unit copper consumption.

The bear case highlights historical precedents where high commodity prices accelerated technological innovation and process optimisation, ultimately reducing long-term demand intensity. Industrial buyers possess flexibility to modify production schedules and design specifications when input costs exceed acceptable thresholds.

Market participants recognise that explosive price movements beyond fundamental justification typically trigger corrective mechanisms that restore supply-demand equilibrium through demand adjustment rather than supply expansion.

Demand destruction mechanisms:

• Manufacturer purchase deferrals during price spikes

• Accelerated substitution research and implementation

• Design modifications reducing copper content per unit

• Inventory optimisation strategies minimising copper holdings

• Process innovations improving copper utilisation efficiency

Which Sectors Will Drive Copper Demand Growth Through 2026?

Copper demand growth across 2026 demonstrates sector-specific intensity variations that reflect different stages of technological deployment and infrastructure development. Understanding these sectoral dynamics provides insight into demand sustainability and potential volatility sources as economic conditions evolve.

AI and Data Center Infrastructure Expansion

Artificial intelligence infrastructure development creates copper demand through multiple channels beyond traditional data center requirements. Advanced AI processing systems generate substantial heat loads that require sophisticated cooling infrastructure, incorporating copper-intensive heat exchange systems and thermal management solutions.

The distributed nature of edge computing deployment multiplies infrastructure requirements across numerous smaller facilities rather than concentrating demand in hyperscale data centers. This geographic distribution creates copper demand in locations previously unserved by major data center development, expanding the total addressable market for electrical infrastructure.

AI infrastructure copper requirements:

• Enhanced cooling systems for high-performance computing environments

• Power distribution networks supporting increased electrical loads

• Backup power systems ensuring operational continuity

• Network connectivity infrastructure for data transmission

• Specialised electrical grounding systems for sensitive equipment

Grid Modernisation and Renewable Energy Integration

Smart grid development requires substantially higher copper intensity than traditional electrical distribution systems. Advanced grid technologies incorporate real-time monitoring, automated switching, and bidirectional power flows that demand sophisticated electrical architectures with enhanced conductor requirements.

Renewable energy integration creates copper demand through multiple infrastructure layers including generation equipment, transmission systems, and grid balancing technologies. Offshore wind development particularly drives copper consumption through submarine cable systems that connect remote generation sites to onshore transmission networks.

Grid infrastructure copper applications:

• Smart metering and distribution automation systems

• Enhanced transmission capacity for renewable energy transport

• Energy storage system interconnection requirements

• Grid stabilisation and power quality management equipment

• Microinverter and power electronics deployment

Electric Vehicle Ecosystem Beyond the Vehicle

Electric vehicle adoption creates copper demand multiplier effects through charging infrastructure deployment and grid reinforcement requirements. Public charging networks require substantial electrical infrastructure including transformers, distribution panels, and high-capacity conductors capable of supporting rapid charging protocols.

Residential charging infrastructure drives copper consumption through home electrical system upgrades and utility distribution network enhancements. The concentration of EV charging in specific geographic areas creates localised grid stress that requires targeted infrastructure investment to maintain service reliability.

EV ecosystem copper intensity:

• Fast-charging station electrical infrastructure

• Residential electrical panel and wiring upgrades

• Utility distribution network reinforcement

• Battery manufacturing facility electrical systems

• Vehicle-to-grid interconnection technologies

What Supply-Side Catalysts Could Reshape Market Balance?

Supply-side developments in copper markets face longer implementation timelines than demand-side changes, creating structural imbalances that persist across multiple market cycles. Understanding potential supply catalysts helps evaluate the sustainability of current market conditions and the likelihood of eventual supply-demand rebalancing.

Mine Development Pipeline Reality Check

Copper mine development faces increasingly complex permitting environments and community engagement requirements that extend project timelines beyond traditional expectations. Environmental impact assessments, indigenous consultation processes, and regulatory compliance create development phases that can span decades from initial discovery to commercial production.

Capital allocation within major mining companies reflects shareholder pressure for disciplined investment and sustainable returns rather than aggressive capacity expansion. This constraint limits the industry's ability to respond rapidly to price signals through accelerated development of marginal projects.

Consequently, gold-copper exploration trends are increasingly focusing on multi-commodity deposits to maximise development economics.

Mine development constraints:

• Environmental permitting requiring comprehensive impact studies

• Community consultation processes extending approval timelines

• Infrastructure development needs for remote deposit locations

• Skilled workforce availability for construction and operations

• Capital market conditions affecting project financing

Technological Breakthroughs in Extraction and Processing

Advanced extraction technologies offer potential solutions for previously uneconomic copper deposits, particularly lower-grade resources that conventional mining methods cannot profitably develop. In-situ recovery techniques and bioleaching applications demonstrate progress in accessing copper resources without traditional mining infrastructure.

Processing technology improvements focus on energy efficiency and environmental impact reduction while maintaining production capacity. Automation in mining operations addresses workforce constraints while improving safety and operational consistency in challenging environments.

Technology advancement areas:

• In-situ recovery systems for low-grade deposit exploitation

• Bioleaching processes reducing environmental impact

• Automated mining systems improving operational efficiency

• Advanced metallurgy for complex ore processing

• Waste heat recovery systems in smelting operations

Geopolitical Supply Chain Diversification Efforts

Government policies promoting critical mineral supply chain resilience create incentives for copper production diversification away from geographically concentrated sources. Strategic partnerships and investment incentives aim to develop alternative supply sources that reduce dependence on dominant producing regions.

Trade policy developments affect copper flows through tariffs, export restrictions, and investment limitations that reshape global supply chain patterns. These policies influence long-term investment decisions and operational strategies across the copper value chain.

Supply diversification initiatives:

• Critical minerals partnerships between allied nations

• Investment incentives for domestic mining development

• Strategic stockpile programmes for supply security

• Technology transfer agreements for processing capacity

• Trade agreement provisions addressing mineral supply chains

How Should Investors Position for Copper Market Volatility?

Copper market trends 2026 present complex risk-reward scenarios requiring sophisticated positioning strategies that account for multiple volatility sources and time horizons. Investment approaches must balance exposure to structural demand growth against risks from price corrections and supply response developments.

Direct Exposure Strategies and Risk Management

Direct copper exposure through exchange-traded funds and futures contracts offers pure commodity exposure but requires careful attention to market structure dynamics. Contango and backwardation patterns provide signals about market stress levels and inventory conditions that influence optimal entry and exit timing.

Futures market positioning requires understanding the relationship between spot prices and forward curves, particularly during periods of supply disruption or demand surge. Roll yield considerations become significant during extended holding periods when futures curves exhibit persistent structural patterns.

For instance, copper investment strategies increasingly incorporate multiple exposure methods to optimise risk-adjusted returns.

Direct exposure considerations:

• ETF tracking efficiency and expense ratio analysis

• Futures contract selection and roll timing optimisation

• Margin requirements during high volatility periods

• Correlation patterns with broader commodity indices

• Liquidity considerations for position sizing and exit strategies

Equity Exposure Through Mining Company Analysis

Copper mining equity exposure provides leveraged participation in price movements while introducing company-specific operational and financial risks. Production growth profiles vary significantly across mining companies based on their development pipeline and operational optimisation capabilities.

Cost curve positioning determines mining company profitability across different price environments. Companies operating lower on the cost curve maintain profitability during price corrections while higher-cost producers face margin compression that affects equity valuations disproportionately.

Mining equity evaluation criteria:

• Production growth visibility and development pipeline quality

• Cost curve positioning relative to industry benchmarks

• Exploration success rates and reserve replacement capabilities

• Balance sheet strength and capital allocation discipline

• Operational efficiency improvements and automation deployment

Downstream Industrial Exposure Considerations

Companies with significant copper content in their products face input cost pressures during price increases but may benefit from inventory appreciation and demand growth in copper-intensive applications. Pricing power and contract structures determine ability to pass through cost increases to customers.

Infrastructure and technology companies with copper-intensive business models provide indirect exposure to structural demand growth while maintaining diversified revenue sources. These positions offer participation in copper demand themes without direct commodity price exposure.

Industrial exposure analysis:

• Copper content analysis across product portfolios

• Pricing power assessment and contract indexation mechanisms

• Inventory turnover patterns during price volatility periods

• Customer diversification and end-market exposure

• Substitution risk in copper-intensive applications

The next major ASX story will hit our subscribers first

What Are the Key Risk Factors That Could Derail Bull Scenarios?

Copper bull market sustainability faces multiple risk factors that could trigger significant price corrections regardless of underlying supply-demand fundamentals. These risks operate across different time horizons and require continuous monitoring to assess their probability and potential market impact.

Demand Destruction Thresholds and Substitution Acceleration

Industrial consumers demonstrate price sensitivity above certain threshold levels where copper costs become economically unsustainable for marginal applications. These thresholds vary by sector and application but create demand elasticity that limits sustained high pricing.

Substitution research accelerates when copper prices reach levels that justify investment in alternative materials and design modifications. While substitution takes time to implement, high prices provide economic incentives for technological innovation that reduces long-term copper demand intensity.

Demand destruction mechanisms:

• Price thresholds triggering industrial buyer behaviour changes

• Aluminium substitution in electrical applications

• Design optimisation reducing copper requirements per unit

• Manufacturing process modifications improving material efficiency

• End-user conservation measures during high-price periods

Supply Response Mechanisms and Market Corrections

High copper prices eventually stimulate supply responses through multiple channels including scrap mobilisation, operational optimisation, and capacity expansion. While supply response takes time, sustained high prices create powerful economic incentives for increased production.

Mine operators implement production optimisation strategies during high-price environments, including processing of stockpiled lower-grade materials and acceleration of development projects. These responses may not immediately affect supply but create conditions for eventual market rebalancing.

According to Goldman Sachs commodity analysts, supply response mechanisms typically gain traction 12-18 months after sustained price elevation periods.

Supply response factors:

• Scrap collection and processing acceleration at higher price levels

• Mine production optimisation and processing efficiency improvements

• Accelerated development of previously marginal projects

• Inventory destocking by consumers and intermediaries

• Technology deployment reducing production costs

Macroeconomic Headwinds and Policy Shifts

Economic slowdown scenarios reduce industrial copper demand across multiple sectors simultaneously, creating demand destruction that overwhelms supply constraints. Recession risks particularly affect infrastructure spending and manufacturing activity that drive copper consumption.

Interest rate changes influence infrastructure investment economics and commodity financing conditions. Higher rates reduce the economic viability of capital-intensive projects while affecting the cost of commodity inventory financing and trading positions.

Macroeconomic risk factors:

• Economic recession reducing industrial production and construction activity

• Interest rate increases affecting infrastructure investment economics

• Currency fluctuations impacting international trade flows

• Trade policy changes disrupting established supply chains

• Government spending reductions affecting infrastructure programmes

What Does the 2027 Outlook Signal for Long-Term Positioning?

Copper market trends 2026 establish conditions that will likely influence 2027 market dynamics through supply response developments and demand maturation processes. Understanding these longer-term trends provides context for investment positioning and risk management strategies extending beyond immediate market conditions.

Market Maturation and Price Stabilisation Expectations

Market consensus anticipates price stabilisation or correction during 2027 as supply responses begin affecting market balance and demand growth rates moderate from 2026 acceleration levels. This expectation reflects recognition that current supply-demand imbalances cannot persist indefinitely without triggering corrective mechanisms.

The timeline for market rebalancing depends on the pace of supply development and the sustainability of demand growth across key sectors. Infrastructure deployment cycles and mining project development schedules create predictable timeframes for supply-demand convergence.

Furthermore, research from Trading Economics suggests that historical copper cycles typically exhibit 18-24 month correction phases following periods of extreme supply tightness.

Stabilisation factors:

• Supply project commissioning schedules affecting production capacity

• Infrastructure deployment completion reducing peak demand growth

• Market maturation in key consuming sectors

• Inventory rebuilding cycles following deficit periods

• Price normalisation encouraging demand recovery

Strategic Metal Classification and Policy Implications

Government recognition of copper as a strategic material influences market dynamics through stockpiling programmes, investment incentives, and trade policies designed to ensure supply security. These policy interventions create additional demand sources while affecting international trade patterns.

Critical materials designation leads to increased government involvement in copper markets through strategic reserves, domestic production incentives, and supply chain security initiatives. These policies introduce non-market factors that influence pricing and availability patterns.

Policy development trends:

• Strategic stockpile programmes affecting demand patterns

• Investment incentives for domestic production capacity

• International cooperation frameworks for supply security

• Trade agreement provisions addressing critical materials

• Research and development funding for copper technologies

Disclaimer: This analysis contains forward-looking statements and projections based on current market conditions and available information. Copper prices are subject to significant volatility, and actual results may differ materially from forecasts. Investment decisions should be based on individual risk tolerance and comprehensive due diligence. Past performance does not guarantee future results.

Considering Your Copper Market Positioning for 2026?

Discovery Alert's proprietary Discovery IQ model delivers instant alerts on significant ASX mineral discoveries, including copper-rich deposits that could capitalise on the structural demand drivers reshaping the market. Explore Discovery Alert's dedicated discoveries page to understand how historic mineral discoveries have generated substantial returns, then begin your 14-day free trial to position yourself ahead of the market.