July 7, 2026

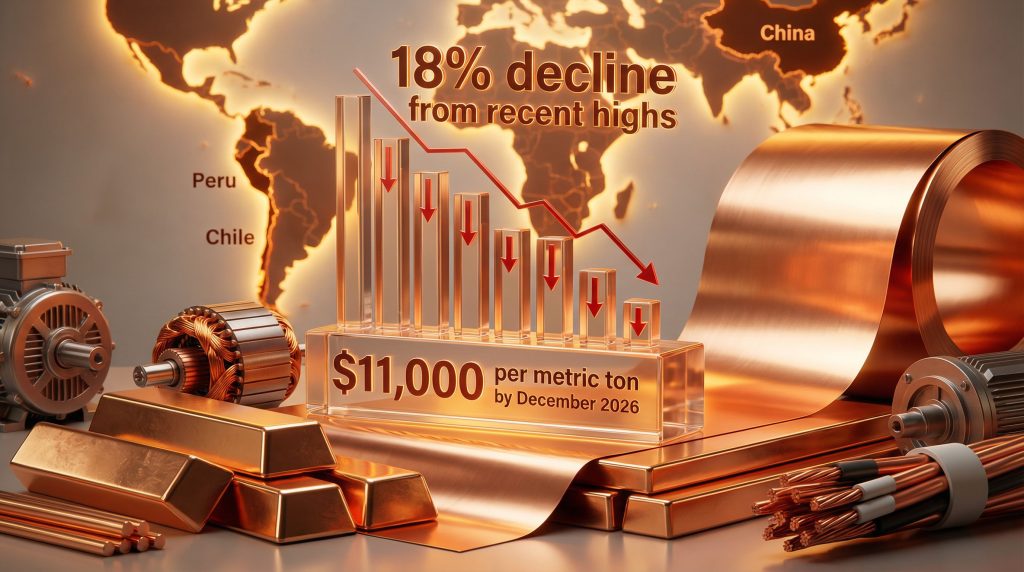

The copper market landscape has undergone significant structural changes, with analysts now predicting a potential copper price correction 2026 as speculative positioning unwinds and fundamental supply-demand dynamics reassert their influence. Goldman Sachs projects an 18% decline from recent highs, targeting approximately $11,000 per metric tonne by December 2026, compared to levels above $13,000 reached in early 2026. This shift reflects a broader recalibration where market forces move beyond momentum-driven pricing toward fundamentals-based valuation.

Understanding Market Cycles: Why Copper Experiences Price Volatility

Global copper markets operate through intricate cycles that reflect the intersection of industrial consumption patterns, macroeconomic conditions, and financial capital flows. Unlike precious metals that function primarily as stores of value, copper pricing mechanisms directly mirror real-time manufacturing activity and forward-looking infrastructure investment decisions. When financial positioning diverges significantly from these underlying consumption indicators, market corrections become inevitable as price discovery mechanisms seek equilibrium.

Industrial copper consumption occurs across measurable end-use categories: electrical construction and installation accounts for approximately 45% of global consumption, power generation and transmission represents 15%, industrial machinery and equipment comprises 15%, transportation accounts for 10%, and consumer goods represent the remaining 15%. This disaggregated demand structure creates identifiable growth drivers that operate independently from financial market positioning.

The Anatomy of Speculative-Driven Price Movements

Copper markets have become increasingly financialized since the early 2000s introduction of commodity index funds. Goldman Sachs Commodity Index (GSCI) and similar investment vehicles created passive allocation mechanisms that direct capital toward commodities based on macroeconomic narratives rather than physical supply-demand fundamentals. This structural evolution can amplify both rallies and corrections by concentrating capital flows into narrow time windows.

Historical data demonstrates copper's vulnerability to sentiment-driven volatility. During the 2008 global financial crisis, copper prices collapsed from $4.04 per pound in July 2008 to $1.38 per pound by December 2008, representing a 66% decline despite relatively stable underlying industrial consumption patterns. Similarly, the ny copper price records experienced a 65% rally from approximately $7,700 per tonne in March 2020 to $12,700 per tonne by May 2021, followed by normalized trading ranges as speculative positioning unwound.

Managed funds and hedge funds have constituted between 25-35% of LME copper positioning during recent bull markets, compared to 10-15% during normalized periods. Furthermore, this concentration of speculative capital creates conditions where flow reversals can generate price volatility that operates independently of physical market conditions.

How Industrial Demand Patterns Signal Market Tops

Real copper consumption occurs through manufacturing processes, construction activity, and infrastructure development projects. When price appreciation significantly outpaces these end-use demand indicators, it suggests that financial positioning rather than industrial necessity is driving valuations. Consequently, this creates vulnerability to rapid reversals when speculative capital seeks alternative investment opportunities.

The 2016 Chinese devaluation cycle provides instructive precedent. In August 2015, China unexpectedly devalued the yuan, triggering a commodity sell-off driven by concerns about demand destruction and capital outflows. Copper prices declined from $2.75 per pound to approximately $2.05 per pound (a 25% correction) within three months, despite Chinese industrial production remaining relatively stable. This demonstrated how currency and policy uncertainty can override fundamental demand indicators.

The 2021-2022 inflation transition cycle further illustrates this dynamic. Copper rose from $3.25 per pound in March 2021 to $5.01 per pound by May 2021 as inflation expectations surged, but then declined to $3.50 per pound by September 2022 as real interest rates increased and recessionary concerns emerged. The cycle was driven primarily by macroeconomic positioning rather than changes in underlying copper consumption patterns.

When big ASX news breaks, our subscribers know first

Is a Major Copper Correction Coming in 2026?

Current market conditions suggest copper may face significant downward pressure as multiple converging factors reshape the fundamental supply-demand equation. Goldman Sachs' revised commodities outlook projects an 18% decline from recent highs, targeting approximately $11,000 per metric tonne by December 2026, compared to levels above $13,000 reached in early 2026. This global copper supply forecast revision reflects changing market dynamics that could trigger meaningful price adjustments.

The $30 Billion Capital Flow Reversal Risk

Goldman Sachs' commodities research team identified over $30 billion in speculative inflows into base metals during 2025, representing the largest annual speculative positioning on record. Copper absorbed more than 50% of this capital allocation, creating conditions where flow reversals could generate substantial price volatility independent of physical market fundamentals.

This unprecedented capital concentration creates asymmetric risk profiles. Positioning-led rallies tend to unwind faster than they develop because exit decisions occur simultaneously across similar investor cohorts. When macroeconomic narratives shift—whether through geopolitical tension resolution, policy uncertainty reduction, or improved returns from alternative assets—capital reallocation becomes concentrated within specific time windows, amplifying downward price pressure.

Key Flow Reversal Indicators and Price Impact Potential:

| Factor | Impact on Copper Prices |

|---|---|

| Speculative Position Unwinding | Potential 15-20% correction |

| Policy Premium Reduction | 5-8% normalisation |

| Inventory Accumulation | 3-5% supply pressure |

| Demand Substitution | 2-4% consumption decline |

Surplus Projections Replace Deficit Narratives

Market analysts have fundamentally revised their 2026 balance forecasts. Goldman Sachs increased surplus projections from 160,000 tonnes to 300,000 tonnes, representing an 88% increase in expected market surplus. In addition, this shift from deficit expectations to surplus reality removes a key pillar supporting elevated pricing levels and suggests that supply responses are beginning to exceed demand growth expectations.

This surplus projection reflects multiple supply-side adjustments: increased scrap recovery incentivised by high prices, inventory rebuilding across global exchanges, and production optimisation at existing operations. For instance, the transition from deficit psychology to surplus fundamentals typically triggers investor reassessment of long-term price assumptions and risk-adjusted return expectations.

What Factors Could Trigger a Copper Price Correction?

Several interconnected developments are creating conditions conducive to price normalisation rather than continued appreciation. These factors operate across different time horizons and market segments, but collectively suggest that current pricing may exceed sustainable equilibrium levels. However, the tariff impact on asx copper stocks demonstrates how policy uncertainty can amplify these correction risks.

Declining Electric Vehicle Copper Intensity

Early electric vehicle designs incorporated approximately 83-90 kg of copper per vehicle, whilst current generation EVs (2024-2026 models) incorporate approximately 50-65 kg of copper per unit. This represents a 30-40% reduction in copper content per vehicle, fundamentally altering demand projections from the automotive electrification trend.

Automotive manufacturers are redesigning electrical architectures to reduce material costs and vehicle weight. Battery management systems, motor windings, and charging circuits are optimised for minimal copper usage whilst maintaining performance and safety standards. Furthermore, this optimisation trend operates independently of copper price levels, as manufacturers pursue efficiency gains to reduce overall vehicle costs and improve energy density regardless of commodity pricing.

Global EV production reached approximately 14 million units in 2024 compared to 5.7 million in 2020. However, this production acceleration has occurred simultaneously with declining copper intensity per unit, partially offsetting volume growth's demand benefits. Even with 25% EV production growth projected for 2025-2026, reduced copper requirements per vehicle could result in flat or declining copper demand from this sector.

Secondary Supply Response to High Prices

Elevated copper prices throughout 2024-2025 have incentivised increased scrap recovery and recycling facility expansion. Secondary copper supplies approximately 40-45% of global copper consumption annually, and collection rates have improved significantly in response to pricing incentives. According to Forbes analysis of copper market dynamics, this supply response represents a fundamental shift in market structure.

Recycling infrastructure expansion, particularly in Southeast Asia and Africa where copper-containing waste streams were previously underutilised, has created additional supply capacity estimated at 50,000-100,000 tonnes annually by 2026-2027. Consequently, this supply response persists because recycling infrastructure, once established, remains economically viable at copper prices above $8,000 per tonne.

Higher collection rates, improved processing technologies, and expanded geographic coverage of recycling networks contribute additional supply that wasn't incorporated into earlier market balance calculations. This represents structural supply addition rather than cyclical inventory management.

Geographic Arbitrage Normalisation

Throughout 2025, tariff concerns created premium pricing for COMEX-deliverable copper relative to London Metal Exchange contracts. This geographic arbitrage reflected expectations that tariffs would become the primary policy tool for addressing supply security concerns, leading to defensive stockpiling by US buyers.

COMEX-deliverable copper traded at a $200-400 per tonne premium to LME pricing during peak concern periods, but this premium has compressed to approximately $100-150 per tonne as of January 2026. Further normalisation toward $0-50 per tonne premium levels could represent an additional 1-3% price correction independent of fundamental supply-demand shifts.

As policy approaches shift away from tariff-based trade measures, the urgency for defensive inventory accumulation diminishes. Existing stockpiles begin normalising distribution through physical markets, reducing artificial demand premiums in specific geographic regions.

How Supply-Side Dynamics Support Correction Scenarios

Inventory Rebuilding Across Global Exchanges

Warehouse stocks across major exchanges have begun accumulating after extended periods of drawdowns. This inventory rebuilding reflects both increased supply availability and reduced urgent industrial demand, creating buffer capacity that wasn't present during the tightest market conditions. Exchange-monitored inventories provide transparency into this rebalancing process and serve as leading indicators for supply-demand equilibrium shifts.

Production Response to Incentive Pricing

Current copper prices provide strong economic incentives for producers to maximise output from existing operations whilst accelerating development timelines for advanced projects. This production response typically lags price increases by 12-18 months, suggesting supply additions may coincide with any demand moderation during 2026. The us copper production overview highlights how domestic producers are responding to these price signals.

Mining companies have utilised elevated cash flow generation to optimise existing operations, advance development projects, and improve processing efficiency. These operational improvements represent structural capacity additions that persist even if copper prices moderate from current levels.

What Economic Conditions Could Accelerate Price Declines?

Chinese Industrial Activity Patterns

China's refined copper consumption growth has remained subdued despite elevated global prices, suggesting that demand elasticity is beginning to influence purchasing decisions. If Chinese infrastructure spending or manufacturing activity fails to accelerate beyond current modest growth rates, it could remove a key demand pillar supporting current valuations.

The disconnect between Chinese industrial activity and copper price appreciation indicates that domestic consumption is price-sensitive at current levels. Alternative materials, efficiency improvements, and project deferrals become economically attractive when copper prices significantly exceed historical ranges relative to other input costs.

Interest Rate and Dollar Strength Impacts

Rising real interest rates increase the opportunity cost of holding physical commodities whilst simultaneously strengthening the US dollar, making dollar-denominated metals more expensive for international buyers. These macroeconomic headwinds can amplify commodity price corrections beyond what supply-demand fundamentals alone would justify.

Higher interest rates also affect commodity markets through credit availability channels, reducing financing for inventory accumulation and increasing costs for trade finance activities. These financial constraints can accelerate price corrections by limiting capital available to support elevated price levels.

Credit Availability for Commodity Financing

Tightening credit conditions affect commodity markets through multiple transmission mechanisms:

• Reduced financing availability for inventory accumulation

• Higher costs for trade finance and hedging activities

• Decreased speculative position sizing due to margin requirements

• Limited working capital for commodity trading operations

These financial constraints become particularly acute during periods of monetary policy tightening or banking sector stress, when credit availability contracts regardless of underlying commodity fundamentals.

Which Copper Companies Could Weather a Price Correction?

Cost Curve Positioning Becomes Critical

Companies operating in the lower quartiles of the industry cost curve retain substantial margin protection even under stressed price scenarios. All-in sustaining costs below $3.50 per pound provide significant buffer against potential price declines whilst maintaining positive cash flow generation capabilities.

Cost Curve Analysis Framework:

| Cost Quartile | AISC Range ($/lb) | Margin Protection at $4.00/lb |

|---|---|---|

| First Quartile | $2.00-$2.75 | High (45%+ margins) |

| Second Quartile | $2.75-$3.25 | Moderate (23%+ margins) |

| Third Quartile | $3.25-$3.75 | Limited (7%+ margins) |

| Fourth Quartile | $3.75+ | At Risk (Negative margins) |

Cost positioning analysis must incorporate transportation costs, concentrate treatment charges, and regional smelting availability to provide accurate assessments of delivered costs to end markets.

Balance Sheet Strength and Capital Discipline

Companies with strong balance sheets, limited debt burdens, and disciplined capital allocation policies demonstrate superior positioning to navigate commodity price volatility. Access to credit facilities, cash reserves, and the ability to adjust capital expenditure provide operational flexibility during correction periods.

Financial metrics that indicate resilience include:

• Debt-to-EBITDA ratios below 1.5x at normalised copper prices

• Cash reserves exceeding 12 months of operating expenses

• Undrawn credit facilities providing additional liquidity

• History of maintaining dividends through previous cycles

Operational Flexibility and Production Optionality

Mining operations with the ability to adjust production rates, defer non-essential capital expenditure, or temporarily suspend higher-cost production centres can preserve cash flow during price downturns. This operational flexibility becomes particularly valuable during extended correction periods when maintaining positive operating margins becomes challenging.

Companies with multiple operating assets can optimise their production portfolio by prioritising lower-cost operations whilst reducing output from higher-cost centres. This flexibility provides competitive advantages during stressed market conditions.

The next major ASX story will hit our subscribers first

How Should Investors Position for Potential Copper Volatility?

Development-Stage Projects with Defensive Characteristics

Late-stage development projects with favourable economics may offer better risk-adjusted returns than high-cost producers during correction periods. Projects with oxide metallurgy, heap-leach processing capabilities, and clear permitting pathways provide lower technical risk profiles with accelerated payback periods. However, understanding the copper–uranium investment outlook is essential for diversification strategies.

Oxide heap-leach operations typically demonstrate:

• Lower capital intensity per tonne of annual production

• Reduced metallurgical complexity and processing risk

• Faster construction timelines and capital payback

• Lower operating costs compared to flotation and smelting alternatives

Geographic and Jurisdictional Considerations

Political stability, transparent regulatory frameworks, and established mining jurisdictions provide risk premiums that become more valuable during periods of heightened market volatility. Projects in jurisdictions with predictable permitting processes and stable fiscal regimes may attract capital that avoids higher-risk regions during uncertain market conditions.

Jurisdictional factors that support investment resilience include:

• Established mining codes with transparent permitting processes

• Political stability and respect for property rights

• Existing infrastructure reducing development capital requirements

• Access to skilled labour and technical services

Joint Venture and Partnership Models

Exploration and development companies with strategic partnerships can preserve upside exposure whilst sharing development risks and capital requirements. Joint venture structures with established operators provide technical expertise and financial backing that individual companies might lack during challenging market conditions.

Partnership advantages during volatile periods include:

• Shared capital requirements reducing financing risk

• Access to established operator expertise and infrastructure

• Risk diversification across multiple projects or partners

• Potential for accelerated development through partner resources

What Long-Term Trends Support Copper Despite Near-Term Correction Risk?

Infrastructure Investment Cycles

Global infrastructure investment requirements, particularly in electrical grid modernisation and renewable energy integration, provide structural demand support that transcends short-term price volatility. These multi-decade investment cycles create sustained copper consumption patterns that financial positioning cannot replicate or replace.

Electrical grid infrastructure requires substantial copper content for power transmission and distribution systems. Grid modernisation initiatives, renewable energy integration, and electrification trends represent demand drivers with 20-30 year implementation timelines that provide fundamental support for long-term copper consumption growth. According to S&P Global's assessment, these structural trends remain intact despite near-term correction risks.

Electrification Momentum Remains Intact

Despite optimisation in individual applications, the broader electrification trend across transportation, industrial processes, and energy systems continues to drive incremental copper demand. This structural shift provides a foundation for long-term price support even if near-term corrections occur due to financial positioning adjustments.

Electrification encompasses multiple sectors:

• Transportation: Electric vehicles, charging infrastructure, public transit

• Industrial: Motor efficiency improvements, automation systems

• Residential: Heat pumps, solar installations, energy storage

• Commercial: Building automation, efficiency upgrades

Supply Chain Security Considerations

Geopolitical tensions and supply chain diversification initiatives continue to influence copper market dynamics. Strategic stockpiling programmes, domestic production incentives, and supply security concerns create demand components that operate independently of traditional industrial consumption patterns.

Government policies increasingly recognise copper's strategic importance for energy transition and economic security objectives. These policy-driven demand sources provide additional support during periods when traditional industrial consumption may moderate.

Key Takeaways: Navigating Copper's Correction Potential

The copper market in 2026 faces a recalibration period where speculative positioning unwinds and fundamental supply-demand dynamics reassert their influence on pricing mechanisms. Whilst long-term structural trends remain supportive of copper demand, near-term copper price correction 2026 risk has increased substantially due to surplus projections, demand optimisation trends, and potential financial flow reversals.

Critical Success Factors for Copper Investments:

• Cost positioning: All-in sustaining costs below $3.50/lb provide substantial margin protection

• Balance sheet strength: Low debt levels and cash reserves enable operational flexibility

• Jurisdictional stability: Established mining regions offer regulatory predictability

• Technical risk management: Oxide projects with proven metallurgy reduce execution risk

• Strategic partnerships: Joint ventures share development costs and technical expertise

The investment opportunity lies not in avoiding copper exposure entirely, but in selecting companies and projects positioned to outperform during the market's transition from momentum-driven pricing to fundamentals-based valuation. This selectivity phase rewards thorough analysis of company-specific factors rather than broad commodity exposure strategies.

Market Timing and Entry Point Considerations

Goldman Sachs' copper price correction 2026 outlook targeting $11,000 per tonne reflects cooling excess optimism rather than collapse in copper's strategic relevance. The correction thesis is grounded in observable fundamentals: surplus projections increasing to 300,000 tonnes, demand substitution trends, and unwinding of speculative positioning that drove prices beyond levels justified by physical market conditions.

Historically, macro-driven corrections reset valuation frameworks and improve long-term entry points for investors with discipline to differentiate between price momentum and economic resilience. The anticipated selectivity phase will reward companies demonstrating margin protection, execution capability, and capital discipline under various price scenarios.

Investment Strategy Implications

The emphasis shifts from commodity exposure toward company-specific fundamentals. Successful navigation of the copper price correction 2026 environment requires focus on:

• Margin resilience: Companies maintaining profitability at $3.75-$4.25/lb copper prices

• Execution visibility: Projects with clear development timelines and permitting certainty

• Capital efficiency: Development projects with industry-leading returns on invested capital

• Operational flexibility: Ability to adjust production and costs during volatile periods

Those who distinguish between speculative market froth and structural value creation are positioned to outperform as copper markets recalibrate toward more sustainable equilibrium pricing. The copper price correction 2026 scenario presents both risks and opportunities for discerning investors focused on fundamental analysis rather than momentum-based strategies.

Forward-Looking Risk Assessment

Whilst near-term correction risks have increased, copper's role in global electrification and infrastructure modernisation remains structurally intact. The anticipated copper price correction 2026 represents market normalisation rather than demand destruction, creating opportunities for well-positioned companies to outperform during the transition period.

Market timing considerations suggest that correction periods often provide superior entry points for long-term investors willing to focus on operational excellence, cost competitiveness, and execution capability rather than short-term price momentum. The selectivity environment ahead will differentiate companies based on fundamental strength rather than broad commodity exposure.

Could Your Copper Investments Weather a Market Correction?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant copper discoveries and mining developments across the ASX, helping investors identify opportunities that remain resilient during market corrections. Start your 30-day free trial today to discover which copper companies maintain competitive advantages whilst market dynamics evolve beyond speculative positioning towards fundamentals-based valuations.