July 13, 2026

The Copper Market's Structural Paradox: Abundance, Disruption, and the China Demand Equation

Commodity markets occasionally produce conditions that expose the limits of conventional price theory. The current copper market is one such moment. Textbook economics holds that rising inventories and expanding surpluses compress prices toward marginal cost. Yet copper prices and China's demand growth have together created a market where that logic breaks down entirely. In mid-2026, refined copper sits at nearly $13,484 per tonne on the LME, roughly 32% above its 2025 annual average, while exchange inventories have simultaneously reached their highest point in more than two decades. Understanding this contradiction requires moving beyond short-term supply-demand accounting and into the structural forces reshaping the global copper industry.

When big ASX news breaks, our subscribers know first

Two Opposing Forces Are Pulling the Copper Market Apart

The most important data point in the copper market right now is not the price itself, but the gap between what is happening at the mine level versus what is happening at the refinery level. These two segments of the copper supply chain are moving in opposite directions, and that divergence explains almost everything about current pricing behaviour.

World copper mine production contracted by 1.4% in the first four months of 2026, driven by a cluster of simultaneous disruptions at major operations:

- Grasberg, Indonesia: Concentrate production plunged 40% following a severe mud rush that forced significant disruptions to underground operations, representing one of the most consequential single-asset supply shocks in recent memory.

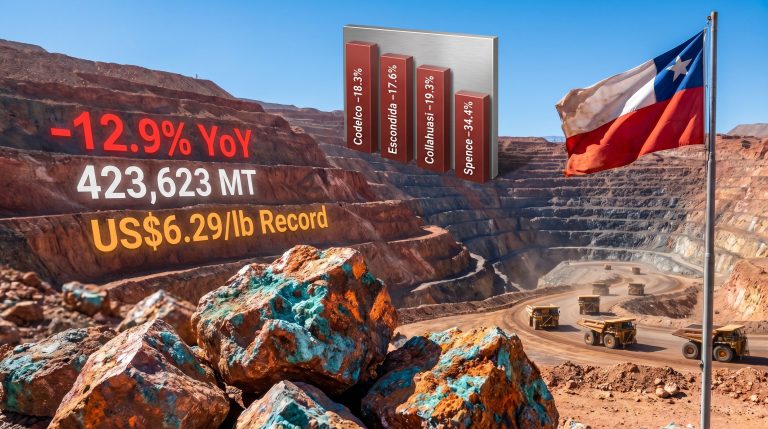

- Chile (five major operations): National mine output declined 7.9%, with shortfalls recorded at Escondida, El Teniente, Los Pelambres, Candelaria, and Spence. Chile's electrolytic refined copper production separately fell 26%, while SX-EW output declined 3.4%, removing a significant volume of lower-cost refined product from global markets.

- Democratic Republic of Congo: Concentrate production fell 33%, tightening the global feedstock pipeline available to smelters outside China.

In any prior copper cycle, this combination of disruptions would have translated directly into a tighter refined market. However, global refined copper output rose 4% to 9.711 million tonnes over the same period, while refined consumption increased only 2% to 9.471 million tonnes, producing a 239,000-tonne surplus approximately five times larger than the 47,000-tonne surplus recorded in the same period of 2025.

| Supply and Demand Metric | Jan-Apr 2026 Result |

|---|---|

| Global mine production change | -1.4% |

| Global refined copper production | +4.0% (9.711 million tonnes) |

| Global refined copper consumption | +2.0% (9.471 million tonnes) |

| Refined market surplus | 239,000 tonnes |

| Prior year surplus (Jan-Apr 2025) | 47,000 tonnes |

| Year-on-year surplus expansion | approximately 5x |

The mechanism connecting these two opposing realities is China's refining sector. Furthermore, this growing imbalance has significant implications for those tracking the copper supply crunch that defined market thinking just twelve months ago.

China's Refinery Expansion: The Hidden Engine of the Global Surplus

China and the DRC together account for roughly 60% of global refined copper production. In the first four months of 2026, China's domestic refined copper output grew 7.4%, a rate sufficient to more than replace the combined volume lost through disruptions at Grasberg and across Chilean operations. This is the structural insight that most observers miss when attempting to reconcile elevated prices with rising inventories.

China's refining expansion manifested across two distinct supply channels:

Primary Smelting Growth

Chinese smelters processed feedstock from alternative concentrate sources, expanding primary refined output at a pace that more than compensated for the feedstock losses from Grasberg and the DRC. Consequently, the copper trade war impact has also redirected trade flows, further amplifying China's domestic processing incentives.

Secondary Refined Copper Production

Global scrap-based refined copper output grew 6.8% in the first four months of 2026, with the majority of that increase originating in China. Secondary production carries structurally lower capital requirements than primary smelting, making it highly responsive to elevated price environments. When copper prices rise sharply, scrap collection economics improve, more material enters processing pipelines, and secondary output expands. This creates a self-reinforcing cycle that adds supply precisely when prices might otherwise remain elevated.

The practical consequence of this refining expansion is visible in China's import behaviour. Despite apparent domestic copper demand growing 2.4% over the period, China's net refined copper imports fell 25%. This import substitution effect is analytically critical: as Chinese smelters supply a larger share of domestic demand from domestically produced refined copper, the portion of globally produced refined copper that would otherwise flow into China as imports effectively becomes available to international markets instead, compounding the global surplus.

A market where the world's largest consumer simultaneously expands domestic production, reduces imports, and grows demand at a below-trend rate is structurally different from any prior copper cycle. The supply-demand imbalance is being manufactured internally by China's own refining capacity growth.

Exchange Inventories at a 23-Year High: What the Numbers Reveal

The inventory picture confirms the magnitude of the current imbalance. Combined copper stocks across the LME, COMEX, and SHFE reached 1,144,966 tonnes at the end of May 2026, an increase of 400,851 tonnes (54%) from end-2025 levels and the highest aggregate reading since January 2003.

| Exchange | Function in Global Copper Pricing |

|---|---|

| LME (London Metal Exchange) | Global benchmark; three-month copper at $13,484.50/t |

| COMEX (New York) | US futures market; key indicator of tariff-driven arbitrage and physical flows |

| SHFE (Shanghai Futures Exchange) | China's domestic benchmark; reflects onshore supply-demand conditions |

The LME forward curve structure reinforces the inventory signal. The curve sits in mild contango, ranging from approximately $13,453 to $13,494 per tonne through December 2026. Contango in a commodity market carries a specific analytical message that is often overlooked in mainstream coverage:

- The futures price for future-month delivery exceeds the current spot price, indicating that physical supply is adequate and storage costs are being absorbed into the curve

- Contango discourages speculative long positioning because rolling forward a futures contract in a contango market generates a negative roll yield

- Producer hedging activity is typically concentrated in contango markets, as forward prices offer better realisation than spot

- A shift from contango to backwardation would be the most important early signal that the surplus is genuinely narrowing, as backwardation reflects physical scarcity and premiums for immediate delivery

The market is currently pricing in no near-term supply emergency, and the inventory data confirms that assessment.

Why Prices Haven't Collapsed: The Psychology of Structural Bull Narratives

If the data clearly shows a surplus of this magnitude, why does copper trade 32% above its 2025 annual average? The answer lies in how commodity markets price futures versus present conditions, and in the durability of the structural demand narrative that has dominated copper sentiment since 2022. In addition, the copper price drivers underpinning the long-term bull case remain firmly intact despite near-term oversupply signals.

Copper's long-term demand thesis rests on three technology transitions that consume the metal at rates far exceeding conventional industrial use:

1. Power grid modernisation and electrification: Grid investment programs across multiple major economies require substantial copper for transmission lines, distribution networks, and substation infrastructure. Rural electrification programs in developing economies add further volume.

2. Electric vehicle production: EVs require approximately two to three times more copper than equivalent internal combustion engine vehicles, with copper used in motors, wiring harnesses, charging infrastructure, and battery connections. China's position as the world's largest EV market creates a structurally expanding demand base regardless of short-term industrial softness.

3. AI data centre construction: This is perhaps the least appreciated copper demand driver in public analysis. Hyperscale AI data centres require up to 50,000 tonnes of copper per facility, compared with 5,000 to 15,000 tonnes for conventional data centres. The copper intensity of AI infrastructure arises from the density of power delivery systems, cooling infrastructure, and signal cabling required to support high-performance computing at scale. Globally, AI-driven copper demand could reach 4.3 million tonnes annually by 2035, representing a demand category that did not exist at meaningful scale in any prior commodity cycle.

Analysts project that by 2040, energy transition infrastructure and AI data centre construction combined could account for 45% of total global copper demand, up from approximately 32% in 2024. This structural shift progressively reduces the market's sensitivity to China's traditional construction and heavy manufacturing cycles.

These narratives are not wrong. They are simply not yet dominant enough in the near-term demand picture to absorb a 239,000-tonne four-month surplus. Price elevation reflects forward-looking confidence in these themes, not current physical tightness.

China's Demand Trajectory: The Only Variable That Matters Now

With mine supply disruptions failing to tighten the refined market, the future direction of copper prices and China's demand growth trajectory become almost entirely co-dependent. The data currently presents a mixed picture. Indeed, China commodity demand across multiple metals markets is showing signs of structural deceleration that extends well beyond copper alone.

| Chinese Demand Indicator | Current Reading | Analytical Implication |

|---|---|---|

| Global copper demand share | approximately 60% | Extreme price sensitivity to demand shifts |

| Apparent demand growth (Jan-Apr 2026) | +2.4% | Below the rate needed to absorb the surplus |

| Factory output growth (April 2026) | 4.1%, down from 5.7% | Near-term industrial demand softening |

| Manufacturing PMI | 49.8 (below 50 threshold) | Contractionary signal for copper-intensive activity |

| Net refined copper import change | -25% | Domestic smelter capacity displacing import reliance |

China's share of global copper demand is projected to ease from approximately 57% in 2026 toward 52% by 2031, as demand growth increasingly shifts toward the United States and India driven by electrification programs and infrastructure investment. According to Reuters analysis of new copper demand drivers, this geographic diversification reduces the copper market's dependence on Chinese industrial cycles over time, though in the current window, China remains overwhelmingly the dominant swing variable.

The next major ASX story will hit our subscribers first

Scenario Analysis: Bull and Bear Pathways for H2 2026

The price trajectory for the remainder of 2026 resolves around a single analytical question: will China's apparent copper demand growth rate cross above its refined copper production growth rate?

| Scenario | Core Assumption | Expected Inventory Trend | LME Copper Target |

|---|---|---|---|

| Base Case (Bullish) | Apparent demand accelerates to 5%+, driven by grid, EV, and AI spending | Surplus narrows over 2-3 quarters | Toward $14,097/t (2026 high) |

| Bear Case | Refined production maintains 7.4% growth while demand holds at 2.4% | Inventories push above 23-year highs | Toward $11,826/t (2026 low) |

Major institutional forecasters have staked out positions across this range. Bank of America projects potential peak copper prices reaching $15,000 per tonne under tight supply scenarios, while J.P. Morgan forecasts a medium-term average closer to $11,000 per tonne if macroeconomic risks deteriorate materially. The structural bull consensus for copper remains intact through 2027 in most institutional outlooks, anchored by electrification demand that is relatively insensitive to short-term Chinese industrial cycles.

For investors evaluating entry points, exploring robust copper investment strategies is essential before committing capital in this environment of elevated prices and expanding surpluses.

Disclaimer: Price forecasts from financial institutions represent analytical estimates and are subject to change. They do not constitute investment advice, and actual copper price outcomes may differ materially from projections based on shifts in macroeconomic conditions, geopolitical events, or supply-demand dynamics not captured in current models.

Producer Cost Structures: Who Survives a Prolonged Surplus

A surplus environment transforms operational cost efficiency from a secondary metric into the primary differentiator between producers that maintain margins and those that face compression. The current copper market makes this analysis more consequential than at any point since 2022.

The cost dynamics are asymmetric across the current production landscape:

- Chilean operations that reduced output in 2026 spread fixed costs across fewer tonnes, mechanically increasing unit production costs. Chile's 26% decline in electrolytic refined output left smelter fixed costs distributed over a materially smaller volume base, with Escondida, El Teniente, and their peers all absorbing this cost inflation.

- By contrast, Oyu Tolgoi in Mongolia increased underground production by 29% in the first four months of 2026. Higher output spreads fixed costs over more tonnes, reducing unit costs. With copper trading 32% above its 2025 average, Oyu Tolgoi's expanding production volume combined with its improving cost position creates meaningful downside protection relative to higher-cost peers.

Producers requiring LME copper above $12,500 per tonne to break even face materially greater exposure if the refined surplus continues to expand and prices trend toward the bear-case target of $11,826 per tonne. In a surplus market, cost position is not merely a performance metric. It is a survival threshold.

The Three Signals to Monitor for Copper's Next Directional Move

For investors tracking copper prices and China's demand growth in the second half of 2026, three observable data points provide the most reliable leading and coincident signals for price direction:

- ICSG Monthly Copper Bulletin: Published with a two-month reporting lag, this is the primary source for global refined production and consumption data. The critical ratio to track is the gap between Chinese refined production growth and apparent demand growth. Two consecutive reporting periods where demand growth exceeds production growth would signal a genuine surplus contraction.

- LME Forward Curve Structure: The transition from contango to backwardation is the most reliable physical market signal that near-term supply tightness is emerging. Monitor whether the spread between spot and three-month contracts narrows and eventually inverts.

- SHFE Inventory Levels and Spot Premiums: Rising SHFE inventories paired with negative spot premiums indicate that physical copper is accumulating in China and demand is not absorbing supply. Declining inventories paired with positive spot premiums indicate the opposite. This data is available on a weekly basis and provides a higher-frequency read on Chinese physical market conditions than monthly ICSG publications.

Threshold levels for surplus monitoring:

- A monthly world refined copper surplus below 40,000 tonnes for two consecutive periods would indicate the surplus is narrowing and would support a move toward the $14,097 bull case target.

- A monthly surplus above 100,000 tonnes for two consecutive periods would signal compounding excess supply and increase the probability of a move toward the $11,826 bear case level.

Frequently Asked Questions

Why do copper prices remain elevated when a large surplus exists?

Commodity price adjustment to surplus conditions typically lags inventory accumulation by several months. Copper's current elevation reflects the earlier supply disruption narrative from Grasberg and Chile, combined with durable long-term structural demand confidence from grid investment, EV growth, and AI infrastructure. Price discovery has partially decoupled from near-term physical balances, a condition that resolves once inventory accumulation becomes large enough to overwhelm forward-looking sentiment.

What would cause the copper surplus to narrow in 2026?

The most direct catalyst is an acceleration in Chinese apparent copper demand from its current 2.4% growth rate to approximately 5% or above, driven by grid spending, EV production ramp-up, and AI data centre construction. Simultaneously, a moderation in China's domestic refined copper production growth from 7.4% would reduce the supply-side pressure. Both conditions occurring together would rapidly shift the surplus trajectory.

How does AI infrastructure specifically affect copper demand?

Hyperscale AI data centres are copper-intensive at a scale that conventional facility benchmarks underrepresent. The power delivery density, thermal management systems, and signal infrastructure required to support high-performance AI computing clusters consume up to 50,000 tonnes of copper per major facility. As AI build-out accelerates globally, this demand category adds a structurally new and growing consumption floor that did not feature in copper demand models prior to approximately 2023.

What is the significance of the LME forward curve being in contango?

Contango means that future-dated copper contracts trade at higher prices than spot contracts. This structure signals adequate near-term physical supply, discourages speculative long positioning through negative roll yield, and reflects producer hedging activity. For investors, contango is a caution signal that the market does not currently anticipate a near-term supply squeeze. A shift to backwardation, where spot prices exceed futures prices, would represent a fundamentally different market signal and an early indicator that surplus conditions are reversing.

Want to Track the Next Major Copper Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly translating complex geological data into actionable investment insights — essential for navigating a copper market where structural forces are reshaping traditional price dynamics. Explore historic mineral discovery returns on Discovery Alert's dedicated discoveries page, or begin your 14-day free trial at discoveryalert.com.au to position yourself ahead of the next major copper find.