July 11, 2026

The Geology of Scarcity: Understanding Why Copper Supply Is Tightening From the Ground Up

Every commodity cycle eventually confronts a geological truth: the easy ore has already been mined. For copper, that reckoning is arriving faster than most market participants anticipated. The world's richest copper deposits were discovered and developed across the twentieth century, and the mines built on those discoveries are now ageing into their most challenging operational chapters. Declining ore grades, deepening extraction zones, and the compounding cost of maintaining ageing infrastructure are not temporary inconveniences. They are the physical reality of mineral depletion playing out in real time across the Andes.

When Chile May copper output falls sharply across top miners, as Cochilco's official data confirmed for May 2026, the numbers are striking. However, behind those numbers lies a more complex story about what it actually costs to extract copper from deposits that are becoming progressively less cooperative. Understanding the copper supply crunch requires looking beyond the headline figures to the geological and operational realities underneath them.

When big ASX news breaks, our subscribers know first

Chile May Copper Output Falls Sharply: The Raw Numbers

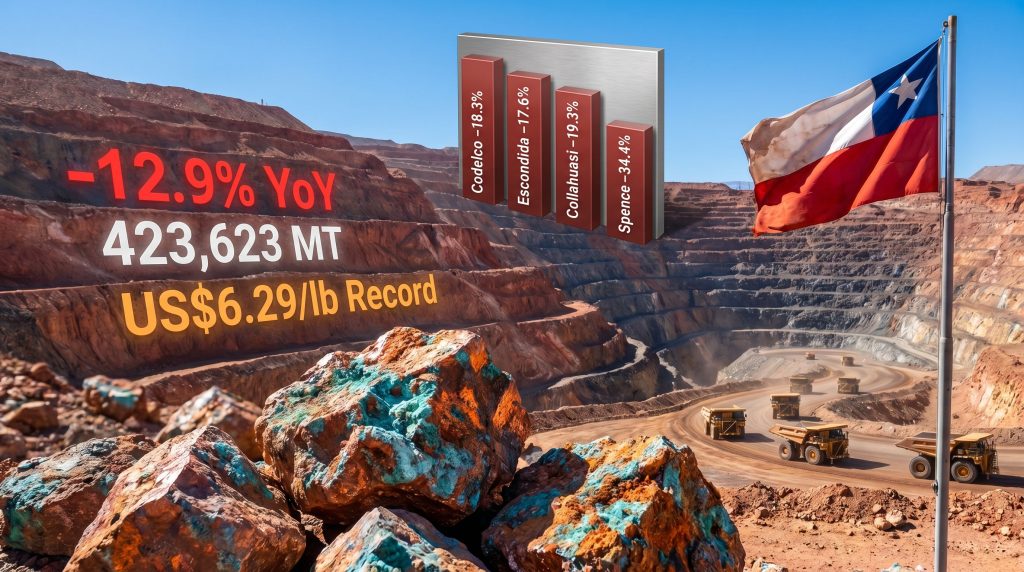

Chile's total copper production for May 2026 reached 423,623 metric tons, representing a 12.9% contraction compared to the same month in 2025. According to Chile's State Copper Commission, Cochilco, the decline was not concentrated at a single asset. It was broad-based, cutting across both state-owned operations and privately managed mines simultaneously.

That simultaneous, multi-site deterioration is the detail that transforms a monthly production report into a structural signal. Furthermore, Chile's copper supply gap has been widening for some time, making these figures consistent with a longer-term trend rather than an isolated anomaly.

May 2026 Production Summary: Chile's Major Copper Producers

| Mine / Operator | May 2026 Output | Year-on-Year Change | Key Context |

|---|---|---|---|

| Escondida (BHP) | 108,800 tonnes | -17.6% | World's largest copper mine by annual output |

| Codelco (Total) | 106,300 tonnes | -18.3% | El Teniente down ~29.5% vs. Jan 2025 levels |

| Collahuasi (Anglo American / Glencore) | 31,000 tonnes | -19.3% | Reversed a 16% surge recorded in March 2026 |

| BHP Spence | Not disclosed (May) | -34.4% (Q1 2026) | Steepest proportional decline among major Chilean assets |

What makes this table particularly significant is not any single figure, but the consistency of the declines. When three of the world's largest copper mines all post double-digit year-on-year contractions in the same month, the statistical probability of coincidental, unrelated operational issues becomes negligible.

Four Structural Forces Driving the Decline

Ore Grade Deterioration: The Invisible Headwind

Ore grade refers to the concentration of copper within the rock being mined, typically expressed as a percentage. A mine with an ore grade of 1.5% copper contains 15 kilograms of recoverable copper per tonne of processed rock. As grades decline toward 0.5% or lower, three things happen simultaneously: energy consumption per unit of copper output rises sharply, water requirements increase, and processing costs escalate.

Chile's copper deposits, many of which were world-class high-grade resources when first developed, are now being mined at grades significantly below their historical averages. This is not an operational failure. It is geology. The higher-grade ore near the surface and in accessible zones was extracted first. What remains is deeper, lower-grade, and more expensive to process.

"Ore grade decline is perhaps the most underappreciated driver of rising production costs in the copper sector. It is silent, gradual, and irreversible without new discovery or deposit expansion, yet it systematically erodes the economics of even the most efficiently managed mines."

El Teniente and the Underground Transition Challenge

Codelco's El Teniente operation, widely recognised as the largest underground copper mine in the world, is navigating a particularly demanding phase of its operational life. The mine is in the process of transitioning into deeper, lower-grade ore panels as shallower sections reach depletion. The Codelco production outlook remains uncertain as this transition unfolds over the coming years.

This kind of block cave mining transition involves years of development work before new ore production zones reach their designed extraction rates. During the transition, output suppression is essentially engineered into the schedule. El Teniente's output declined approximately 29.5% compared to January 2025 levels, a figure that reflects the scale of disruption associated with this process.

Codelco's broader portfolio faces the compounding challenge of chronic capital investment shortfalls accumulated over multiple years. Several of its major assets require simultaneous structural upgrades, creating competing demands on a capital budget that has historically been constrained by the financial pressures facing Chile's state-owned mining enterprise.

Expansion Projects Failing to Offset Mature Mine Losses

One of the critical assumptions underpinning optimistic copper supply forecasts was that new project ramp-ups would compensate for volume losses at ageing operations. May 2026's production data suggests that assumption is not holding.

Teck Resources' Quebrada Blanca operation, one of the more prominent recently developed large-scale Chilean copper projects, encountered waste-storage complications that forced a downward revision to its 2026 production guidance. Projects of this scale and complexity carry significant execution risk during their early operational years, and when they underperform, there is no easy substitute.

Sulfuric Acid Supply Constraints: A Processing Bottleneck

A less widely understood structural challenge facing Chilean copper producers is the availability and cost of sulfuric acid. Oxide copper ore, which is leached using sulfuric acid in a process known as heap leaching followed by solvent extraction and electrowinning (SX-EW), requires enormous volumes of acid. Chile has historically relied on sulfuric acid as a byproduct of smelting operations, but as global smelting capacity shifts and domestic supply tightens, acid procurement has become an increasingly significant operational constraint.

Tightening acid availability affects Codelco, BHP, and Anglo American across multiple Chilean assets simultaneously, compressing SX-EW output volumes and adding a further layer of pressure on top of ore grade and infrastructure challenges. In addition, copper price drivers such as these processing bottlenecks are increasingly influencing how analysts model future price trajectories.

Global Market Implications: Why Chile's Problem Is Everyone's Problem

Chile's position in global copper supply cannot be overstated. The country accounts for approximately 25 to 27% of global annual mine supply, making it the single most important national source of the metal. When Chile's output contracts at the pace observed in May 2026, the downstream effects ripple through copper markets worldwide.

Copper prices reached a record high of US$6.29 per pound during Q1 2026, reflecting market recognition that supply growth is structurally lagging behind accelerating demand. The price signal is not simply a trading artefact. It represents the market's honest assessment of the difficulty of replacing Chilean tonnes with supply from elsewhere. Analysts tracking the Chile copper price forecast have consequently revised their outlooks upward to account for sustained supply pressure.

Demand Acceleration Is Colliding With Supply Contraction

The timing of Chile's output decline is particularly challenging because it is occurring precisely as two powerful demand acceleration forces are intensifying:

-

Electrification infrastructure driven by electric vehicle adoption, grid modernisation, and renewable energy deployment. A single electric vehicle contains approximately three to four times more copper than a conventional internal combustion engine vehicle, and utility-scale wind and solar installations are among the most copper-intensive energy infrastructure categories.

-

Artificial intelligence and data centre buildout, where energy-intensive computing requires substantial copper for power distribution, cooling systems, and high-density wiring. The scale of planned AI infrastructure investment globally represents a copper demand category that barely existed a decade ago.

These are not short-cycle demand drivers that will normalise within a year or two. Both electrification and AI infrastructure are decade-long capital deployment programmes, meaning the copper demand they generate will compound over time rather than moderate.

Scenario Analysis: How Severe Could the Supply Gap Become?

"If Chilean copper output continues contracting at a rate of 10 to 15% annually, the global market faces a cumulative monthly supply shortfall from Chile alone of approximately 40,000 to 65,000 tonnes. No single alternative producing nation has the near-term capacity to bridge a gap of that magnitude."

The following comparison illustrates the volatility pattern that has characterised recent Chilean output:

| Period | Production Signal | Direction |

|---|---|---|

| March 2026 | Collahuasi +16% monthly surge | Temporary upswing |

| May 2026 | National output -12.9% year-on-year | Renewed contraction |

| Q1 2026 (BHP Spence) | -34.4% year-on-year | Sustained decline |

BHP Spence's 34.4% Q1 2026 decline is particularly notable because Spence was expected to function as a growth asset following its recent hypogene ore body expansion. The fact that it is instead recording one of the steepest proportional declines among major Chilean assets raises serious questions about whether even recently expanded operations can sustain forecast output rates in a lower-grade, higher-cost operating environment. Official data on Chile's copper output confirms the breadth of these contractions across multiple operators.

Who Bears the Corporate Exposure?

BHP: A Dual-Asset Vulnerability

BHP's Chilean portfolio spans Escondida and Spence, and both assets recorded severe production contractions in 2026. Escondida's 17.6% decline to 108,800 tonnes in May 2026 is particularly significant. As the single largest copper mine on earth by annual output capacity, Escondida carries considerable weight in BHP's overall copper division performance. FY2026 copper guidance for BHP's Chilean assets is attracting close scrutiny from analysts and investors alike.

Anglo American and Glencore: Collahuasi's Reversal

The Collahuasi joint venture's 19.3% year-on-year decline to 31,000 tonnes in May 2026 is especially noteworthy because it reversed a 16% production surge recorded as recently as March 2026. That kind of intra-year volatility suggests operational instability rather than a smooth production recovery curve. Both Anglo American and Glencore have strategically positioned copper as a core growth metal within their respective portfolio strategies, making Collahuasi's underperformance a direct challenge to their publicly stated production growth narratives.

Codelco: A Reform Imperative With No Easy Timeline

Codelco's 18.3% monthly decline represents its worst recent performance across a portfolio that includes some of the world's most significant copper assets. El Teniente's transition timeline is measured in years, not quarters, and the capital requirements to accelerate development across multiple ageing assets simultaneously are substantial. Chile's government has acknowledged the structural nature of Codelco's challenges, though the path to a sustained production recovery remains complex and contingent on successful project execution at scale.

The next major ASX story will hit our subscribers first

Downstream Exposure: Industrial Buyers and Supply Chain Strategy

The practical consequences of Chile's sustained output decline extend well beyond mining company balance sheets. Three categories of industrial copper consumer face particularly acute exposure:

-

Electric vehicle manufacturers for whom copper is an irreplaceable component in motors, battery packs, power electronics, and charging infrastructure. Rising spot prices translate directly into input cost pressure across vehicle production lines.

-

Renewable energy project developers relying on copper-intensive wind turbines, solar installations, and grid interconnection infrastructure. Sustained price volatility complicates project economics and long-term procurement planning.

-

Data centre operators scaling AI computing capacity, where copper is essential for power distribution systems, server connectivity, and thermal management infrastructure.

In response to tightening supply dynamics, sophisticated industrial buyers are increasingly shifting away from spot market procurement toward longer-term offtake agreements that lock in supply at more predictable pricing. This strategic behaviour itself reflects a market assessment that the current supply tightness is not a transient condition. Consequently, Q1 copper mine output data further validates the urgency with which buyers are rethinking their procurement strategies.

Frequently Asked Questions: Chile's Copper Production Decline

Why did Chile's copper production fall so sharply in May 2026?

The 12.9% year-on-year decline reflects the convergence of four structural factors: declining ore grades at ageing open-pit and underground operations, the complex transition at Codelco's El Teniente mine into deeper ore zones, expansion project underperformance at Quebrada Blanca, and tightening sulfuric acid availability for leaching operations.

Which mine recorded the steepest decline in the May 2026 data?

Among assets with disclosed monthly figures, Collahuasi posted the largest year-on-year contraction at 19.3%, falling to 31,000 tonnes. BHP Spence recorded the steepest quarterly decline at 34.4% during Q1 2026.

What is the significance of ore grade decline in copper mining?

Ore grade is the concentration of copper within processed rock. As grades fall, more rock must be handled per unit of copper produced, increasing energy, water, and reagent consumption simultaneously. This dynamic is geological in nature and cannot be resolved through operational efficiency measures alone.

Is Codelco's production decline reversible?

Over a sufficiently long time horizon, yes. However, recovery depends on successful execution of multi-year mine development programmes, sustained capital investment, and operational stabilisation at assets undergoing complex transitions. The timeline is measured in years rather than months.

How does Chile's output contraction affect copper prices?

Chile supplies roughly 25 to 27% of global copper mine output. Sustained contraction at this scale tightens global availability and supports elevated pricing. Copper reached a record US$6.29 per pound in Q1 2026, with Chilean supply constraints among the contributing factors.

Key Takeaways

-

Chile's May 2026 copper output fell 12.9% year-on-year to 423,623 metric tons, with declines recorded across every major producing asset

-

Codelco (-18.3%), BHP Escondida (-17.6%), Collahuasi (-19.3%), and BHP Spence (-34.4% in Q1) all recorded severe contractions simultaneously

-

The primary drivers are structural: ore grade depletion, ageing mine infrastructure, expansion project underperformance, and sulfuric acid supply constraints

-

Copper prices reached a record US$6.29/lb in Q1 2026 as markets priced in persistent supply tightness

-

The convergence of contracting Chilean supply with accelerating electrification and AI-driven copper demand creates a durable supply-demand imbalance with significant implications for industrial buyers, investors, and anyone with exposure to the copper supply chain

This article contains forward-looking scenario analysis and production trend assessments. These represent analytical projections based on available data and should not be construed as financial advice. Production forecasts, price projections, and supply-demand scenarios involve inherent uncertainty and may differ materially from actual outcomes. Readers should conduct independent research and consult qualified financial advisers before making investment decisions.

Want to Position Yourself Ahead of the Next Major Copper Discovery?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries — including copper — and delivering actionable insights before the broader market reacts. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin a 14-day free trial to secure a market-leading edge.