June 25, 2026

The Circular Metal That Cannot Close Its Own Loop

Copper has been recycled continuously for thousands of years. The Romans melted down worn coins, the Victorians stripped telegraph lines, and modern refiners process millions of tonnes of scrap annually. Yet despite this centuries-long tradition, the world is approaching a copper supply challenge so large that even the most aggressive recycling optimisation cannot fully resolve it. Understanding why recycling metals could supply a quarter of the copper the world will need by 2040 requires confronting an uncomfortable arithmetic reality: the denominator is growing faster than the numerator.

When big ASX news breaks, our subscribers know first

Why Primary Mining Cannot Carry the Load Alone

The forces reshaping copper demand are not cyclical. They are structural, multi-decade, and converging simultaneously. Battery electric vehicles contain roughly 2.5 to 4 times more copper than conventional internal combustion engine vehicles. Offshore wind installations require approximately 9.5 tonnes of copper per megawatt of installed capacity. Grid modernisation projects, AI data centre expansion, and industrial electrification are layering additional demand on top of these already copper-intensive transitions.

Under the International Energy Agency's Net Zero Emissions Scenario, global copper demand is projected to increase by approximately 50% by 2040, with total consumption potentially exceeding 40 million tonnes per year by mid-century. The challenge is that the primary mining pipeline is structurally ill-equipped to absorb this volume spike alone. Average copper ore grades have fallen from roughly 1.8% copper in the 1990s to below 0.6% at many major deposits today, meaning miners must process significantly more rock per tonne of refined metal.

Furthermore, combined with project development timelines that routinely span 10 to 20 years from discovery to first production, and permitting environments that have grown increasingly complex across key jurisdictions, primary supply expansion faces compounding friction. The copper supply crunch is therefore not a temporary dislocation but a deepening structural condition.

This is the structural opening through which secondary copper must step. Not as a replacement, but as an essential complement.

Understanding Secondary Copper: Categories, Sources, and Characteristics

Secondary copper originates from two distinct streams, each with different economics and availability timelines:

- New scrap refers to offcuts, turnings, and waste generated during manufacturing processes. This material is typically high-purity, quickly returns to the supply chain, and is generally easier to recycle efficiently.

- Old scrap encompasses copper recovered from end-of-life products including power cables, transformers, electric motors, plumbing systems, electronics, and end-of-life vehicles. This stream is larger in total volume but subject to long collection lags determined by product lifespans.

The physical property that makes copper uniquely suited to circular supply models is its 100% recyclability without metallurgical degradation. Unlike many materials that lose quality through recycling cycles, copper refined from scrap is chemically indistinguishable from copper refined from ore. This characteristic is commercially significant: secondary copper is not a lower-grade substitute but a genuine equivalent capable of meeting the stringent specifications demanded by EV motor windings, high-voltage transmission cables, and precision electronics.

How Much Recycling Can Realistically Deliver by 2040

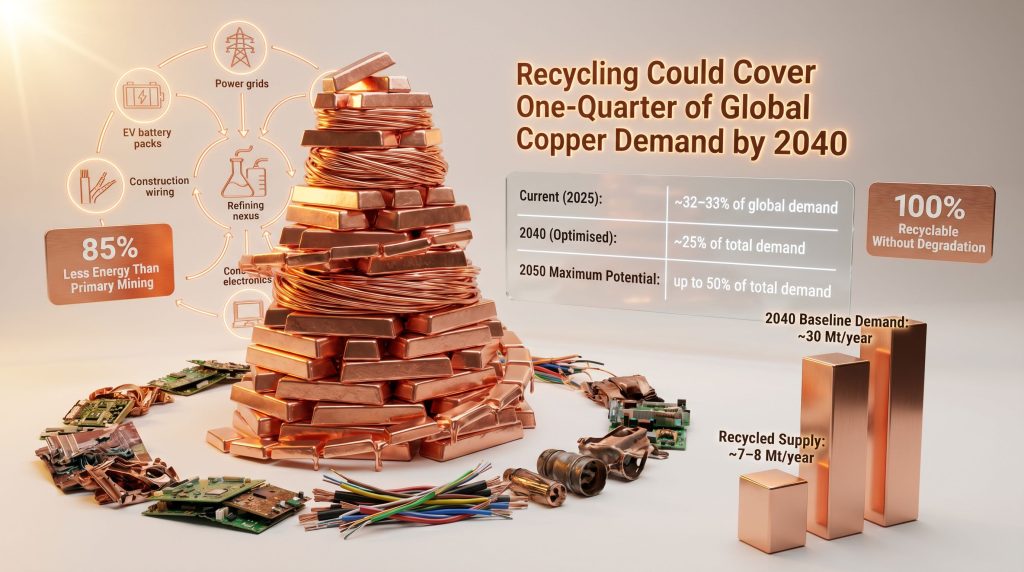

Currently, recycled copper accounts for approximately 32 to 33% of global copper supply, a proportion that represents decades of infrastructure investment in scrap collection, secondary smelting, and refining capacity. This figure, however, masks a critical dynamic that will define the metal's supply outlook over the coming two decades.

Research projections indicate that even under optimised recycling conditions, secondary copper recovery is expected to supply approximately one-quarter of total global copper demand by 2040 — a meaningful but structurally bounded contribution given the extraordinary scale of demand growth ahead.

The apparent contradiction between today's 32% share and tomorrow's projected 25% share is not evidence of recycling failure. It reflects the mathematics of a rapidly expanding denominator. Absolute recycled volumes will grow, but the pace of new copper demand from electrification and digital infrastructure is expected to outrun the growth in scrap supply during the 2025 to 2040 window.

| Timeframe | Recycled Copper's Share of Supply | End-of-Life Recovery Rate Required | Key Condition |

|---|---|---|---|

| Current (2025) | ~32-33% of global demand | ~32% of end-of-life scrap recovered | Baseline scenario |

| 2040 (Optimised) | ~25% of total demand | Significant improvement needed | Demand surge compresses share |

| 2050 (Maximum Potential) | Up to 50% of total demand | Recovery rate must reach ~66% | Requires policy, infrastructure, behavioural change |

Reaching 50% secondary supply by 2050 would require doubling the current end-of-life copper recovery rate from approximately 32% to 66%. That is not a technical impossibility, but it demands sustained policy intervention, infrastructure investment, and behavioural change across every major economy simultaneously.

The Energy and Carbon Case for Scaling Recycled Copper

Beyond supply arithmetic, the economic and environmental arguments for expanding secondary copper capacity are compelling. Recycling copper consumes up to 85% less energy than extracting and processing copper from primary ore. This energy intensity advantage translates directly into lower production costs when energy prices are elevated, and into substantially reduced lifecycle carbon emissions per tonne of refined output.

For manufacturers with Scope 3 emissions reduction commitments, the carbon accounting case for preferring certified secondary copper is becoming increasingly material. EV producers, grid operators, and electronics manufacturers are beginning to incorporate recycled content requirements into procurement frameworks, creating demand-pull incentives for copper recycling expansion across secondary refining capacity.

From a regulatory standpoint, frameworks such as the EU Critical Raw Materials Act and emerging Asian recycling standards are building the policy architecture that could gradually shift economics in favour of secondary production, though these represent broader market conditions rather than targeted support for individual projects.

Three Structural Barriers Limiting Secondary Copper Expansion

Is the Collection Infrastructure Keeping Pace?

Despite the compelling economics and environmental profile, three deep structural constraints limit how quickly secondary copper can scale:

-

Collection Infrastructure Fragmentation

Scrap collection networks in high-growth emerging markets are predominantly informal, fragmented, and poorly integrated with industrial refining capacity. Recovering copper from complex multi-material products such as printed circuit boards, hybrid vehicle components, and smart grid equipment requires sorting sophistication that many developing economy collection systems currently lack. The geographic mismatch between where copper is increasingly being consumed (Asia, Africa, Southeast Asia) and where secondary refining capacity is concentrated (China, Europe, North America) compounds this challenge. -

Product Lifecycle Lags

Copper embedded in power grid infrastructure, commercial buildings, and industrial machinery has an average service life of 25 to 40 years. The massive copper deployment currently underway in EV charging networks, offshore wind installations, and grid expansion will not begin generating significant old scrap volumes until the 2050s and beyond. Near-term scrap availability is therefore shaped by the comparatively modest copper deployment of previous decades, creating a structural supply lag that no policy intervention can fully accelerate. -

Processing Technology and Capacity Bottlenecks

Secondary refining of complex, contaminated scrap streams requires sophisticated hydrometallurgical and pyrometallurgical separation technology. Upgrading secondary smelting infrastructure to handle higher volumes of mixed-metal scrap requires substantial capital investment. Contamination remains a persistent quality challenge: copper recovered from electronics scrap often contains trace elements including tin, lead, and antimony that require additional processing steps to remove.

The next major ASX story will hit our subscribers first

Primary vs. Secondary Copper: A Comparative Framework

| Dimension | Primary (Mined) Copper | Secondary (Recycled) Copper |

|---|---|---|

| Energy Intensity | High | Up to 85% lower |

| Carbon Footprint | Significant | Substantially reduced |

| Supply Scalability | Constrained by ore grade and timelines | Limited by scrap availability |

| Quality Consistency | Highly consistent | Variable by scrap purity |

| Geographic Flexibility | Concentrated (Chile, Peru, DRC, Australia) | Distributed globally |

| Lead Time to Market | 10-20 years | Months from collection to output |

| Price Sensitivity | Driven by ore grade and energy costs | Correlated with primary copper prices |

A less widely appreciated dynamic within this comparison is the price linkage between primary and secondary copper markets. Secondary copper scrap prices are not independently set; they trade at a discount to primary copper cathode prices that reflects processing costs and quality adjustments. When primary copper prices rise, scrap economics improve simultaneously, creating a self-reinforcing incentive to increase collection and processing activity.

Technologies Reshaping the Economics of Copper Recycling

What Innovations Are Closing the Recovery Gap?

The gap between current recovery rates and what is technically achievable is increasingly being targeted by a new generation of processing and sorting technologies. According to research on recycled copper's role in clean energy transitions, scaling these innovations is essential to meeting long-term supply targets:

- AI-assisted optical and sensor-based sorting systems are dramatically improving the speed and accuracy with which different metal streams can be separated at scrap processing facilities, reducing contamination and improving the value of sorted material.

- Advanced hydrometallurgical leaching processes are enabling economic recovery of copper from scrap streams that would previously have been unviable, including low-grade electronic waste and mixed alloy residues.

- Direct electrorefining of complex scrap reduces the number of processing steps required and lowers energy consumption relative to conventional pyrometallurgical routes.

- Digital material passports, which track the copper content and alloy composition of products through their entire lifecycle, are emerging as a tool for improving end-of-life recovery rates by giving recyclers precise advance knowledge of incoming scrap composition.

In addition, the battery recycling process being refined in China offers instructive parallels, demonstrating how industrial-scale secondary recovery systems can be built rapidly when policy and capital align effectively.

Policy Levers That Can Accelerate Secondary Copper Recovery

Technology alone will not close the recovery rate gap. Consequently, policy architecture is equally important:

- Extended Producer Responsibility frameworks that mandate take-back schemes for EVs, consumer electronics, and electrical equipment can significantly improve collection rates for complex copper-containing products.

- Minimum recycled content standards in government procurement specifications for infrastructure and vehicles create guaranteed demand signals for secondary copper.

- Scrap export controls and domestic processing incentives retain high-value material within national borders rather than exporting it for processing elsewhere.

- Carbon border adjustment mechanisms can create trade flow advantages for low-emission secondary copper over primary material produced with higher carbon intensity.

Scenario Analysis: Recycled Copper's Share Under Different Demand Trajectories

| Demand Scenario | Total Copper Demand by 2040 | Recycled Copper Supply | Recycled Share |

|---|---|---|---|

| Baseline (Moderate Transition) | ~30 Mt/year | ~7-8 Mt/year | ~25% |

| Accelerated Energy Transition | ~35-40 Mt/year | ~8-9 Mt/year | ~22-25% |

| Net Zero Emissions Pathway | ~40+ Mt/year | ~9-10 Mt/year | ~22-23% |

A counterintuitive insight embedded in this scenario analysis is that the more ambitious the energy transition, the lower the percentage share that recycling contributes to total supply, even as absolute recycled volumes increase. Faster electrification means faster copper consumption growth, and the scrap stream simply cannot keep pace with demand that is being created today but will not return to the recycling system for decades.

The broader critical minerals demand picture reinforces this point. Copper is not alone in facing this structural tension between accelerating consumption and constrained secondary supply, and policymakers are increasingly recognising that recycling and primary production must scale in parallel rather than in sequence.

The Strategic Conclusion: A Pillar, Not a Solution

The 25% figure is not a ceiling on ambition. It is an honest reflection of the extraordinary scale of copper demand growth being driven by electrification, clean energy deployment, and digital infrastructure expansion. Recycling metals could supply a quarter of the copper the world will need by 2040, while primary mining addresses the remaining three-quarters.

This framing dissolves the false binary between recycling and mining. Both are necessary. Neither is sufficient alone. Secondary copper reduces marginal pressure on primary producers, moderates price volatility during supply disruptions, and provides a geopolitically diversified supply source that is not concentrated in any single country or region.

For investors, the strategic implication is equally clear. Copper investment strategies must therefore span the full value chain simultaneously: primary exploration and development, secondary smelting infrastructure, advanced sorting technology, and scrap collection network expansion. The circular copper economy is not a threat to primary miners; it is a complementary layer that will deepen copper supply security across all scenarios.

The scrap wave generated by today's electrification build-out will eventually crest. However, between now and then, the world must mine its way through a supply gap that no amount of recycling optimisation can fully bridge. As industry analysis confirms, closing the mineral supply gap will require both technological advancement and sustained long-term investment across every recovery pathway available.

This article contains forward-looking projections and scenario analysis drawn from publicly available industry research. These projections involve assumptions about future demand, policy, and technology adoption that are inherently uncertain. Readers should not rely on this material as investment advice.

Want to Track the Next Major Copper Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including copper — instantly translating complex geological data into actionable investment insights for both short-term traders and long-term investors. Explore historic mineral discoveries and their extraordinary returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the market.