May 21, 2026

Copper's Coming Supply Crisis and Why Junior Explorers Are Moving Fast

The global mining industry is staring down a structural problem that no amount of recycling or demand management can fully resolve: the world needs significantly more copper than existing mines can produce, and the pipeline of new projects capable of filling that gap is alarmingly thin. Grades at legacy operations across Chile and Peru have been declining for decades. The average copper grade mined globally has fallen from around 1.6% in 2000 to below 0.6% today, according to data widely cited across industry research. New large-scale discoveries have become genuinely rare events, and the lead time from discovery to production at a greenfield copper mine now averages between 16 and 20 years.

Against that backdrop, the attention being directed toward the Midas Minerals Otavi Copper Project in Namibia becomes easier to understand. This is not simply a story about one junior miner reporting promising drill results in southern Africa. It is, furthermore, a window into how the global copper supply system is being forced to look further afield, at earlier-stage assets, in jurisdictions that were previously considered peripheral to the mainstream conversation. The copper supply crunch currently reshaping global commodity markets is making projects like this one increasingly difficult to ignore.

When big ASX news breaks, our subscribers know first

What Makes the Otavi Mountain Land Geologically Distinct

The Otavi Mountain Land in northern Namibia occupies a very specific position in the global sediment-hosted copper spectrum. The stratigraphy of the region belongs to the Damara Sequence, a Neoproterozoic-age rock package that has long been associated with some of southern Africa's highest-grade carbonate-hosted copper and lead-zinc mineralisation. What distinguishes the Otavi terrane from more commonly cited copper districts such as the Central African Copperbelt is the style of mineralisation.

Copper here is typically hosted within dolomitic carbonate units, creating a geochemical environment where high-grade, structurally controlled ore bodies can form within relatively compact footprints. This carbonate-hosted style carries specific economic implications. Dolomite-hosted copper mineralisation tends to respond well to conventional flotation processing, and the rock competency often supports cost-effective underground mining geometries.

The region has a documented history of high-grade copper production dating back to colonial-era mining activity, and remnant infrastructure, including sealed road access and proximity to power corridors, substantially reduces the greenfield capital burden for modern explorers.

How the Otavi Region Compares to Other African Copper Districts

Sediment-hosted copper systems exist across a wide geographic arc in Africa, from the Copperbelt straddling the DRC-Zambia border to emerging districts in Botswana and Namibia. However, not all of these systems carry the same risk-adjusted appeal for international capital.

| Jurisdiction | Political Risk | Infrastructure Quality | Royalty Rate | Foreign Ownership | Typical Grade Range |

|---|---|---|---|---|---|

| Namibia | Low | High | Competitive | Permitted | 1.0% to 4%+ Cu |

| DRC | High | Low | Variable | Restricted | 1.5% to 6%+ Cu |

| Zambia | Medium | Medium | Moderate | Permitted | 1.0% to 3.0% Cu |

| Botswana | Low | Medium | Competitive | Permitted | 0.8% to 2.5% Cu |

Namibia's combination of low political risk, established rule of law, and existing mining sector infrastructure positions it as arguably the most accessible of Africa's copper-prospective jurisdictions for foreign-listed junior miners. The country has a mining code that is transparent by regional standards, a stable currency arrangement through its link to the South African rand, and a track record of respecting property rights and investment agreements. Consequently, these factors underpin long-term capital commitment decisions. The mineral exploration importance of politically stable environments like Namibia cannot be overstated when evaluating junior project risk.

The Otavi Project Structure: Scale, Licences, and Strategic Logic

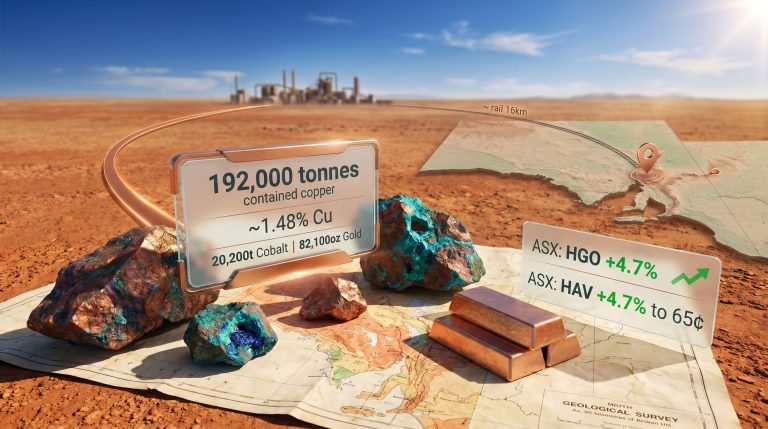

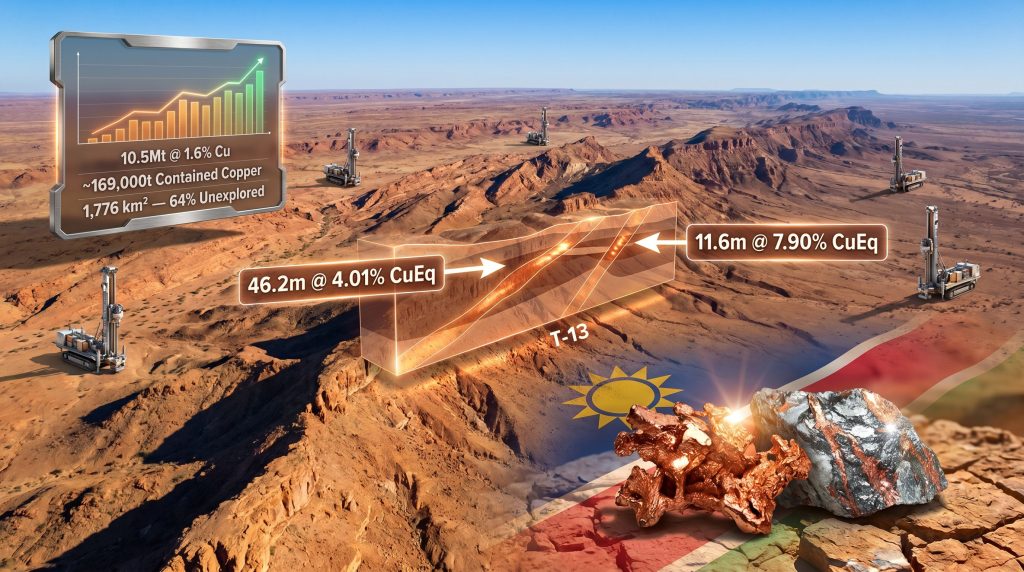

The Midas Minerals Otavi Copper Project in Namibia spans approximately 1,776 km² across ten exclusive prospecting licences, a footprint large enough to contain multiple deposit-scale targets at various stages of exploration maturity. The project's principal asset is the T-13 Copper-Silver Deposit, but the licence package also includes the Deblin Copper-Gold-Silver Deposit and the Spaatzu prospect, creating a genuinely multi-target exploration platform rather than a single-hole story.

Critically, modern systematic exploration has tested only around 36% of the total licence area. That figure carries significant weight in exploration circles: a district where nearly two-thirds of the ground remains undrilled by contemporary methods, after already delivering a multi-million-tonne resource, is statistically unusual. It represents a meaningful discovery pipeline that is difficult to replicate through asset acquisition at more mature projects.

How the Acquisition Was Structured

The project was acquired from Nexa Resources, a significant Latin American copper and zinc producer that had conducted historical work across the Otavi licences but had not advanced them to resource stage under modern exploration frameworks. The deal structure is an important detail for investors evaluating capital efficiency. Rather than paying a large upfront sum, the acquisition was designed around milestone-linked deferred payments, with payment triggers tied to the completion of a pre-feasibility study, a mine construction decision, and the commencement of commercial production.

Total consideration is reported at approximately N$126.4 million (approximately US$7 million), a relatively modest sum for a district-scale copper-silver asset in a stable jurisdiction. This type of milestone-deferred deal architecture is increasingly used in majors and junior partnerships across the exploration sector. It aligns the financial interests of vendor and acquirer across the development curve, ensures the explorer is not front-loading capital into payment obligations before the asset has been sufficiently derisked, and preserves drilling capital for the activities that actually create value.

Breaking Down the T-13 Drill Results: What the Numbers Actually Mean

The most recent drilling campaign at the T-13 Copper-Silver Deposit has delivered intercepts that, by the standards of sediment-hosted copper exploration globally, are genuinely notable for their combination of width and grade. Understanding why requires a brief detour into how the industry evaluates drill results.

Understanding Copper Equivalent and Why Grade-Width Combinations Matter

Copper equivalent (CuEq) is the standardised metric used across the industry to express the combined economic value of multiple metals as a single copper percentage. At T-13, the mineralisation carries both copper and silver credits, and in some zones, gold. The CuEq calculation incorporates prevailing metal prices, metallurgical recovery rates, and payability factors applied by smelters and refiners.

The distinction between narrow ultra-high-grade intercepts and wide moderate-grade intercepts matters enormously for project economics. A narrow high-grade zone may support a selective, low-tonnage, high-value underground operation. A wide, consistently mineralised zone at moderate-to-high grades, however, is the foundation of a bulk-tonnage resource that can underpin significantly larger production scenarios and attract institutional capital at pre-feasibility stage.

Interpreting drill results from the T-13 campaign reveals that the deposit is delivering both attributes simultaneously, which is what makes them technically interesting:

- Drill hole T13DD009: 46.2 metres at 4.01% CuEq from 193.2 metres depth, including a sub-interval of 9.7 metres at 6.55% CuEq and a second sub-interval of 10.6 metres at 7.45% CuEq

- Drill hole T13DD013: 41.9 metres at 3.70% CuEq, with a peak sub-interval of 11.6 metres at 7.90% CuEq

- Multiple intercepts across the campaign exceeding the 4% CuEq threshold across widths relevant to bulk underground mining scenarios

For context, a copper development project with consistent intercepts above 2% copper is generally considered high-grade in the current industry environment, where the global average mined grade sits well below 1%. Intercepts consistently exceeding 4% CuEq over widths above 40 metres represent a materially different proposition.

The T-13 Mineral Resource: Current Scale and 2026 Update Trajectory

The initial mineral resource estimate for the T-13 deposit, as detailed in the Otavi Project investor presentation, establishes a baseline from which the 2026 update will be measured.

| Metric | Reported Figure |

|---|---|

| Total Resource Tonnage | 10.5 million tonnes |

| Average Copper Grade | 1.6% Cu |

| Average Silver Grade | 21 grams per tonne |

| Contained Copper Metal | ~169,000 tonnes |

| Contained Silver | ~7.1 million ounces |

| T-13 Strike Length | ~1.4 kilometres |

An important nuance here is that the existing resource was established before the current high-intensity drilling campaign. Infill drilling is now returning grades that are, in the assessment of company management, exceeding internal modelling expectations. If those grades are consistent with the broader resource envelope, the updated estimate expected in 2026 could reflect both additional tonnage and a higher average grade profile, a double-positive outcome that would materially re-rate the deposit.

The Western Extension: A Second High-Grade Domain in Development

Approximately 600 metres west of the T-13 Main Zone, infill drilling has intersected 27 metres grading 1.46% CuEq from 286.8 metres depth, with a higher-grade sub-interval of 6 metres at 3.20% CuEq. While these grades are lower than the Main Zone intercepts, the geological significance lies in the spatial separation.

A mineralised corridor confirmed 600 metres along strike from an established high-grade zone, in a system that already extends 1.4 kilometres of strike, raises the possibility that the T-13 system is either a continuous mineralised body of greater total extent than the current resource reflects, or a series of structurally related but geometrically distinct ore shoots. Either interpretation carries positive implications for total resource scale.

Geologists working on carbonate-hosted copper systems understand that ore shoot geometry in these environments is frequently controlled by intersecting fold axes and fault corridors within the host dolomite. The 600-metre offset of the western extension intercept is consistent with structural repetition patterns observed in analogous systems, a speculative but geologically coherent framework for interpreting what may be a second high-grade domain.

Five Rigs Running: The Operational Scale of the Current Campaign

The breadth of the current drilling programme reflects a deliberate multi-target strategy across the Otavi licence area.

| Rig Type | Location | Primary Objective |

|---|---|---|

| Diamond Rig 1 | T-13 Main Zone | High-grade infill and resource conversion |

| Diamond Rig 2 | T-13 Main Zone | Resource expansion along strike and at depth |

| Diamond Rig 3 | Deblin Deposit | Copper-gold-silver deposit delineation |

| Diamond Rig 4 | Deblin Deposit | Parallel delineation drilling |

| Reverse Circulation Rig | Spaatzu Prospect | Target testing and geochemical reconnaissance |

| Additional Core Rig | Mobilising | Imminent deployment across project area |

Running five rigs simultaneously across a project area of this scale is operationally significant for a company of Midas Minerals' size. It reflects confidence in the capital runway to sustain the programme and a deliberate decision to advance multiple targets in parallel rather than sequentially, which accelerates the timeline toward a multi-deposit resource base.

The Deblin Copper-Gold-Silver Deposit represents a strategically important parallel thread. If drilling at Deblin returns results of comparable grade and width to T-13, the Otavi project transitions from a single-deposit narrative into a district-scale story with multiple potential development centres. This is a transformation that typically triggers a meaningful re-rating in how institutional capital assigns enterprise value to junior exploration companies.

Managing Director Mark Calderwood has communicated that the latest drilling campaign is consistently delivering results that surpass the company's internal benchmarks. His assessment of the western drilling programme is that it is increasingly pointing toward a separate high-grade zone with the potential to materially expand the total mineralised system, a view that, if validated by ongoing results, would represent a significant positive development for the project's overall scale thesis.

The next major ASX story will hit our subscribers first

Copper Demand Fundamentals: Why the Timing of Otavi Matters

The structural case for copper demand growth over the coming two decades is among the most robustly documented in commodity markets. Electric vehicles require roughly three to four times more copper than internal combustion engine vehicles. Offshore wind installations use approximately 8 tonnes of copper per megawatt of installed capacity. Grid infrastructure upgrades required to accommodate renewable energy integration represent a demand source that is independent of, and additive to, the EV transition.

The Wood Mackenzie copper market analysis and similar industry research frameworks point consistently toward a supply deficit emerging through the late 2020s and deepening into the 2030s. This is driven by existing large-scale mines depleting their highest-grade ore zones and insufficient new capacity reaching production. In addition, the International Energy Agency's critical minerals assessments have identified copper as one of the minerals facing the most acute supply-demand imbalance under accelerated decarbonisation scenarios.

This creates a structural tailwind for exploration-stage projects in stable jurisdictions that are advancing toward resource definition. It is not a guarantee of project success, but it does mean that the external environment facing the Midas Minerals Otavi Copper Project in Namibia is materially more supportive than it was a decade ago. Exploring the right copper investment strategies for this environment requires careful attention to jurisdictional quality and project-level fundamentals alike.

Financial Position: Exploration Runway Through 2026

As of September 2025, Midas Minerals held approximately A$15.3 million in cash. Management has indicated this capital base is sufficient to fund the exploration programme through 2026, encompassing the completion of the current multi-rig drilling campaign and the delivery of the updated mineral resource estimate.

The milestone-deferred acquisition structure plays an important role here. By avoiding large upfront payments to Nexa Resources, the company has been able to direct exploration capital toward drilling rather than vendor obligations, a capital allocation discipline that is particularly important for junior explorers operating on a finite cash base.

Key Milestones and Their Investor Significance

| Milestone | Expected Timing | Why It Matters |

|---|---|---|

| Updated T-13 Mineral Resource Estimate | 2026 | Redefines deposit scale, grade, and classification |

| Deblin Drilling Results | Early to Mid 2026 | Potential second major deposit confirmation |

| Western Extension Confirmation | Ongoing | Could significantly expand T-13 system scale |

| Additional Rig Deployment | Imminent | Accelerates data generation across all targets |

Risks Every Investor Should Understand

A rigorous assessment of the Midas Minerals Otavi Copper Project in Namibia requires an honest accounting of the risks alongside the opportunities.

Exploration-stage risks:

- Current drill results are exploratory and do not constitute a guarantee of mineable reserves at economic parameters

- Resource estimate upgrades rely on geological continuity assumptions that may not hold uniformly across the system

- The western extension and Deblin targets remain at early stages and could underperform historical results

Financial and market risks:

- Copper and silver price movements directly affect project economics; a sustained price decline would reduce resource value and project attractiveness

- Funding requirements for pre-feasibility and feasibility studies will likely require capital beyond current cash reserves, potentially involving equity dilution

- Junior copper explorers can experience significant share price volatility independent of project fundamentals

Operational and jurisdictional risks:

- Permitting timelines, even within a stable jurisdiction like Namibia, can introduce schedule variability

- Multi-rig drilling programmes carry execution risk, including equipment availability, geotechnical challenges, and assay laboratory turnaround times

This article contains forward-looking statements and projections based on publicly available information. It is not financial advice. Readers should conduct their own due diligence and consult a qualified financial adviser before making any investment decisions.

Frequently Asked Questions About the Midas Minerals Otavi Copper Project

What is the Otavi Copper Project in Namibia?

The Otavi Copper Project is a large-scale copper-silver exploration project covering approximately 1,776 km² across ten exclusive prospecting licences in northern Namibia's Otavi Mountain Land region. The project is operated by Australian mining company Midas Minerals and hosts multiple exploration targets including the T-13 Copper-Silver Deposit, the Deblin Copper-Gold-Silver Deposit, and the Spaatzu prospect.

What are the most significant drill results reported at T-13?

The latest campaign returned 46.2 metres at 4.01% CuEq and 41.9 metres at 3.70% CuEq, with peak sub-intervals reaching 7.90% CuEq over 11.6 metres, all of which exceed common industry benchmarks for high-grade sediment-hosted copper mineralisation.

How large is the current mineral resource at T-13?

The initial estimate stands at 10.5 million tonnes grading 1.6% copper and 21 grams per tonne silver, containing approximately 169,000 tonnes of copper and 7.1 million ounces of silver. An updated estimate incorporating the current drilling programme is expected in 2026.

Why is the 36% exploration coverage figure significant?

With only 36% of the total licence area tested by modern systematic exploration methods, the project retains a substantial undrilled discovery pipeline. For a project that has already defined a multi-million-tonne resource in the tested ground, the remaining 64% represents a genuine opportunity for additional target generation.

What is Midas Minerals' financial runway?

The company reported approximately A$15.3 million in cash as of September 2025, which management has indicated is sufficient to fund exploration through 2026, supported by the capital-efficient milestone-deferred structure of the Otavi acquisition.

What the Otavi Project Signals for African Copper Exploration

The Midas Minerals Otavi Copper Project in Namibia occupies an increasingly important position in the global conversation about critical mineral supply. Its combination of high-grade, wide drill intercepts at T-13, a district-scale licence area with substantial unexplored ground, a capital-efficient acquisition structure, and a stable, infrastructure-endowed jurisdiction makes it one of the more technically and commercially coherent junior copper stories currently active in sub-Saharan Africa.

The 2026 updated mineral resource estimate will be the most significant near-term catalyst. If infill drilling grades are incorporated at the widths and values now being reported, and if the western extension is confirmed as a structurally independent high-grade domain, the deposit's scale and grade profile could look materially different from the current baseline.

Furthermore, the parallel drilling campaigns at Deblin and Spaatzu provide multiple pathways through which the project could evolve from a single-deposit exploration story into a district-scale copper-silver development platform. In the context of tightening global copper supply, rising demand from electrification, and increasing investor focus on jurisdictional quality, that is a combination worth watching closely.

Further coverage of African critical minerals exploration and investment trends is available through Business Insider Africa.

Want to Be First When the Next Major Copper Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex data across 30+ commodities into clear, actionable insights for investors at every level. Explore how historic mineral discoveries have generated extraordinary returns, then start your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.