June 24, 2026

The Hidden Fault Line Running Through the Global Copper Market

Every major commodity cycle in history has been shaped not just by what the ground holds, but by whether the infrastructure, chemicals, and geopolitical stability required to extract it remain intact. Copper supply disruptions and Africa opportunity define the central tension of the 2026 commodity landscape — a moment when multiple layers of that support system are fracturing simultaneously. What makes the current situation analytically interesting is not simply that supply is disrupted — it is that disruption is occurring across three separate continents, through three entirely different mechanisms, at precisely the moment when demand-side confidence has softened enough to prevent the price response that basic supply-demand logic would predict.

Understanding this paradox requires stepping back from the price ticker and examining the structural architecture of the global copper supply chain — where it was fragile, where it has broken, and why Africa now sits at the centre of a long-term strategic reorientation in how the world sources one of its most essential industrial metals.

When big ASX news breaks, our subscribers know first

When Supply Tightens But Prices Don't Follow

The Mechanics Behind the 2026 Copper Pricing Paradox

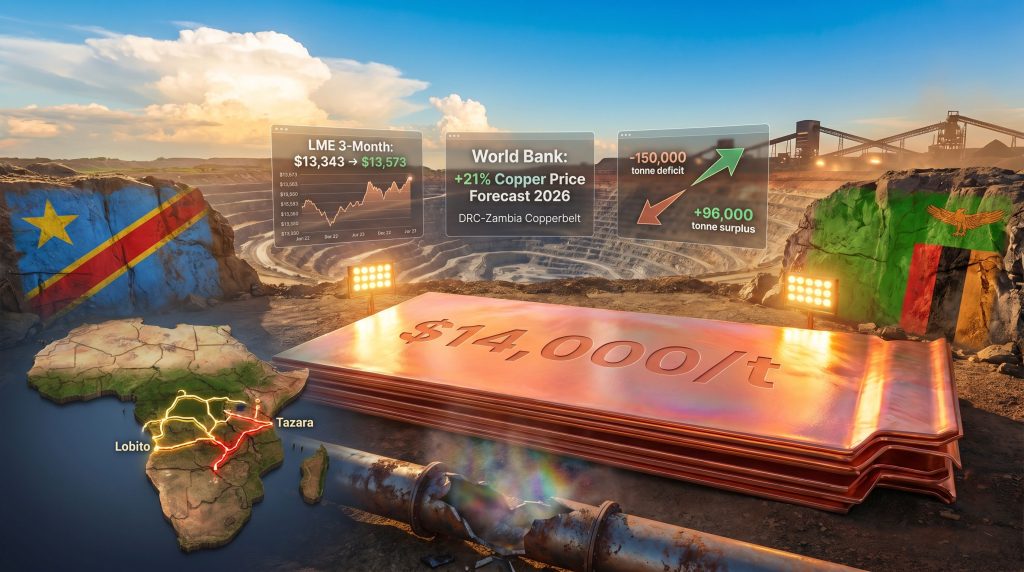

Copper briefly surpassed $14,000 per tonne in January 2026, a level representing a 40% increase since 2025 and a figure driven not by demand euphoria or speculative excess alone, but by a collision of simultaneous production failures. The rally was underpinned by stoppages at major producing operations including the Grasberg mine in Indonesia and the Kamoa-Kakula complex in the Democratic Republic of Congo. Furthermore, a pre-emptive purchasing surge by US buyers seeking to lock in refined copper inventory ahead of anticipated tariff changes amplified speculative trading activity in derivatives markets.

Yet by early May 2026, the three-month copper contract on the London Metal Exchange had risen only from $13,343 per tonne in late February to $13,573 per tonne — a gain so modest it barely registers as directional momentum. The fundamental question this raises is not why copper prices rose in January, but why they have struggled to hold and extend those gains despite a worsening supply picture.

The answer lies in the demand-side counterweight. The International Copper Study Group (ICSG) revised its global demand growth forecast downward from 2.1% to 1.6% for 2026, while simultaneously cutting its global mine production growth projection from 2.3% to 1.6%. The geopolitical instability driving supply disruptions is producing the same economic uncertainty that is suppressing industrial activity, investment confidence, and downstream copper consumption. These two forces are cancelling each other out.

The market balance consequence is striking. The ICSG now projects a refined copper surplus of approximately 96,000 tonnes for 2026 — a dramatic reversal from the 150,000 tonne deficit that was forecast as recently as October 2025.

| Metric | Previous Forecast (Oct 2025) | Revised Forecast (2026) |

|---|---|---|

| Global Mine Production Growth | 2.3% | 1.6% |

| Global Demand Growth | 2.1% | 1.6% |

| Refined Copper Market Balance | -150,000 tonne deficit | +96,000 tonne surplus |

| LME 3-Month Contract (Feb vs. May 2026) | $13,343/tonne | $13,573/tonne |

"The copper market's current configuration illustrates a principle that commodity investors often underestimate: supply disruptions only translate into sustained price rallies when demand remains strong enough to absorb the shock. When both supply and demand weaken simultaneously, the market finds a fragile equilibrium that can persist for months before one variable dominates."

Understanding the copper supply crunch is therefore essential for any investor or analyst seeking to navigate this environment with confidence.

What Is Actually Driving the Copper Supply Disruptions?

A Sulphur Famine Born From Geopolitical Conflict

The single most technically underappreciated disruption in the current copper supply crisis is not a mine collapse or a port closure — it is a chemical shortage. Approximately 20% of global copper output is produced through hydrometallurgical leaching, a process that requires sulphuric acid to dissolve copper from oxide ore deposits. Unlike sulphide ores, which can be processed through smelting, oxide ores have no viable alternative processing pathway at industrial scale.

Sulphuric acid is manufactured from elemental sulphur, a byproduct of oil and gas refining that has historically flowed in large volumes from Gulf-region producers. The military closure of the Strait of Hormuz in early 2026, triggered by strikes on Iran, severed these export routes almost immediately. For the African Copperbelt, where leaching-based operations represent a substantial share of total production capacity, the consequences were direct and severe.

A significant proportion of the DRC and Zambia's sulphuric acid supply was historically sourced through Gulf sulphur imports, and the disruption cascaded rapidly into reduced processing volumes at multiple mine sites. The Zambia copper outlook for 2026 reflects this reality acutely, as the country's production ambitions are increasingly vulnerable to chemical supply chain fragility.

What makes this situation analytically distinct from a standard supply shock is the chemical supply chain's rigidity. Sulphuric acid cannot be rapidly substituted from alternative sources without significant cost increases, logistics reconfigurations, and contract renegotiations. European and Asian sulphur sources exist but are more expensive, involve longer shipping routes to central African landlocked operations, and lack the established infrastructure for bulk delivery that Gulf routes had developed over decades.

This vulnerability is compounded by a separate development: China has implemented export restrictions on sulphur chemicals that are tightening availability not just in Africa but in Chile, the world's largest copper-producing nation. A single policy decision in Beijing is reverberating across three continents simultaneously, driving up processing costs for leaching-dependent operations regardless of their geographic location. Chile's copper supply gap is consequently widening in ways that add further pressure to an already strained global balance.

Grasberg's Production Collapse and the Indonesia Factor

Indonesia's contribution to the current supply squeeze arrives through an entirely different mechanism. PT Freeport Indonesia, operator of the Grasberg complex — one of the world's largest copper and gold deposits — has revised its 2026 production target to 700 million pounds, down from an earlier goal of 1 billion pounds. This represents a reduction of approximately 30% from initial guidance.

The root cause was a deadly mudslide at the Grasberg site in September 2025 that forced an immediate halt to extraction activities. The mine has operated below capacity since that event, with full operational restoration now not anticipated until early 2028, pushed back from the previously expected end of 2027. The extended timeline reflects the complexity of geotechnical remediation at high-altitude open-pit operations, where slope stability assessment, waste repositioning, and structural reinforcement must satisfy both engineering and regulatory standards before normal extraction can resume.

Grasberg's underperformance is particularly significant for global copper concentrate markets. Concentrate — the partially processed material shipped from mine sites to smelters — is already in tight supply globally, and Grasberg's contribution at full capacity is substantial. According to analysis from Mining Technology, when one of the world's premier producing assets runs at a fraction of its design output, the ripple effect on smelter feed availability extends to operations in Asia, Europe, and the Americas.

Infrastructure Failures Compounding Africa's Export Capacity

Even for African copper operations that have managed to maintain processing volumes despite the acid shortage, getting product to market has become dramatically more complicated. Two infrastructure failures have converged to create a logistics crisis of unusual severity.

The collapse of the Kasumbalesa Bridge, a critical DRC export corridor on the border with Zambia, blocked an estimated one-third of the DRC's refined copper exports from their primary overland route. Simultaneously, election-related unrest at the port of Dar es Salaam in Tanzania forced a closure that redirected approximately two-thirds of Africa-to-China copper flows through alternative ports including Durban in South Africa, Walvis Bay in Namibia, and Beira in Mozambique.

The rerouting adds cost, transit time, and port congestion to every tonne of copper that Chinese buyers — who account for more than 50% of global copper demand — are seeking to receive from African sources. Congestion at alternative ports creates cascading delays that extend well beyond the initial disruption event, as vessel scheduling, customs processing, and inland transport coordination all require reconfiguration.

Africa's Strategic Position in the Global Copper Supply Picture

The Scale of Africa's Copper Endowment

Despite the disruptions, the African Copperbelt's importance to global copper supply is not diminishing — it is growing. The DRC and Zambia together are projected to account for approximately 26% of global copper exports in 2026, representing roughly one-sixth of total global copper output. Zambia has set a national production target of 1 million tonnes for the year, while Ivanhoe Mines' Kamoa-Kakula complex in the DRC is guiding for 380,000 to 420,000 tonnes of production.

For Zambia specifically, the stakes extend beyond the mining sector. Copper accounts for approximately 70% of the country's total export revenues, meaning that the intersection of elevated prices and constrained production volumes creates macroeconomic volatility at the national level, not just operational challenges for mining companies.

The geological case for Africa's long-term copper significance is compelling and often underappreciated in Western investment analysis. The Central African Copperbelt hosts some of the highest-grade copper deposits in the world. While Chilean and Peruvian operations increasingly process lower-grade ores as their richest deposits mature, African operations such as Kamoa-Kakula benefit from ore grades that significantly reduce the cost per pound of recoverable copper.

The Sulphuric Acid Dependency: Africa's Structural Achilles Heel

The leaching process dependency creates an asymmetric risk profile for African copper producers that is not well understood outside specialist circles. Leaching-dependent mines account for approximately 20% of global copper output but are disproportionately concentrated in the African Copperbelt, meaning that a sulphur supply shock delivers a larger relative blow to African production than global output figures might suggest.

The cruel irony for African producers in the current environment is that elevated copper prices arrive precisely when the capacity to capitalise on them is most constrained. Higher prices improve revenue per tonne, but reduced processing volumes mean fewer tonnes are being produced. The financial benefit of a price rally is consequently neutralised by the volume loss caused by processing paralysis — a dynamic that standard commodity price analysis often fails to capture.

Until African producers diversify their sulphuric acid sourcing away from Gulf dependency — either through agreements with European or Asian sulphur suppliers, or through investment in alternative processing technologies — leaching-based operations will remain structurally exposed to geopolitical events in regions that have historically seemed distant from African mining concerns.

The Infrastructure Race: Who Controls African Copper Flows?

Competing Corridors and Geopolitical Bifurcation

The battle for control over African copper export infrastructure is intensifying in ways that will shape the geopolitical alignment of the continent's mining sector for decades. Two major corridor investments are currently in various stages of development, backed by competing geopolitical blocs.

The US and EU-backed Lobito Corridor involves a $553 million investment in the Benguela railway system, designed to route Copperbelt output westward through Angola to Atlantic-facing ports, reducing dependence on Indian Ocean routes where Chinese infrastructure investments are dominant. The China-backed Tazara Railway involves approximately $1.4 billion in investment connecting Zambia to Tanzania's Indian Ocean coast, reinforcing Beijing's influence over the supply chains that feed Chinese smelters and manufacturing.

| Infrastructure Project | Backer | Investment | Route | Strategic Objective |

|---|---|---|---|---|

| Lobito Corridor (Benguela Railway) | US / EU | $553 million | DRC/Zambia to Angola (Atlantic) | Reduce Chinese logistical dominance |

| Tazara Railway | China | ~$1.4 billion | Zambia to Tanzania (Indian Ocean) | Reinforce Beijing supply chain influence |

The corridor that achieves operational reliability first will gain a structural pricing and ownership advantage over the other. Whichever route copper flows through consistently determines not just logistics costs but the commercial relationships, financing arrangements, and ultimately the geopolitical alignment of the producing nations involved.

Value-Chain Ambitions and the Revenue Mathematics

Both the DRC and Zambia have signalled at the government level a desire to develop domestic refining and downstream processing capacity, rather than continuing to export raw concentrate or cathode copper at prices that leave significant value on the table. The revenue mathematics are straightforward: refined copper commands a higher price per tonne than copper concentrate, and further processing into wire rod, sheet, or tube commands even more.

Export licensing frameworks and selective export restriction policies are already being used to signal this shift in orientation. The barriers are substantial — energy infrastructure gaps, capital constraints, technical workforce limitations, and the entrenched interests of existing processing capacity in China and elsewhere — but the direction of policy travel is clear.

Chinese operators currently dominate production volumes in the DRC. China Molybdenum reported approximately 650,000 tonnes of copper-equivalent output from DRC operations in 2024. Ivanhoe Mines' Kamoa-Kakula represents the flagship non-Chinese growth asset in the region. Meanwhile, US and European capital is increasingly being directed toward Copperbelt projects through development finance institutions as part of broader energy transition supply security strategies.

What Do Copper Prices Look Like Through 2027?

The World Bank's Outlook and Three Plausible Scenarios

The World Bank's commodity price projections indicate that copper prices are expected to rise by an average of 21% in 2026, which would represent a yearly record for the metal. This is followed by an anticipated correction of approximately 8% in 2027 as supply disruptions gradually ease and production capacity is restored. However, as market analysts have noted, the range of plausible outcomes is wide, and the key variables are highly sensitive to geopolitical developments that remain difficult to forecast with confidence.

| Scenario | Key Trigger | Estimated LME Price Range | Timeline |

|---|---|---|---|

| Base Case | Partial Hormuz reopening; moderate demand recovery | $13,000-$13,800/tonne | H2 2026 |

| Bull Case | Prolonged blockade and persistent infrastructure failures | $14,500-$15,000/tonne | Q2-Q3 2026 |

| Bear Case | Global recession accelerates; demand collapses | $11,500-$12,500/tonne | H1 2027 |

The bull case scenario hinges on the Strait of Hormuz remaining closed beyond 30 days, during which the full weight of African production losses would compound with Grasberg's underperformance to drive prices toward $15,000 per tonne. At that level, the critical question becomes demand destruction: the price point at which EV manufacturers, renewable energy developers, grid operators, and electronics producers begin substituting materials, deferring purchases, or redesigning products to reduce copper intensity.

The bear case requires a meaningful deterioration in global economic activity severe enough to suppress industrial demand despite the structural supply constraints already in place. Given that the energy transition continues to create copper demand that has no realistic substitution pathway in many applications, the bear case would require an unusually deep and broad recession to materialise.

Why the January 2026 Spike Was Structurally Distinct From Previous Rallies

Previous copper price spikes — including the 2007–2008 commodity supercycle peak and the 2021 post-pandemic rally — were primarily demand-driven events. The January 2026 move above $14,000 per tonne was different in character, driven by three simultaneous supply-side forces rather than a broad acceleration in consumption:

- Production stoppages at both Grasberg and Kamoa-Kakula within a short timeframe

- A concentrated pre-tariff purchasing rush by US buyers that front-loaded demand into a narrow window

- Speculative trading activity amplifying the fundamental signal in derivatives markets

When the pre-tariff buying frenzy subsided and speculative positioning normalised, the price could not sustain the momentum on fundamental grounds alone given the demand-side softness. This structural distinction matters for investors: a price spike driven by temporary purchasing acceleration is inherently more fragile than one driven by genuine structural demand growth. Understanding the underlying copper price drivers is therefore essential before drawing conclusions from short-term price movements.

The next major ASX story will hit our subscribers first

Key Risks That Could Undermine Africa's Copper Opportunity

A Balanced Assessment of the Vulnerabilities

Africa's copper endowment is unambiguously significant, but the path from geological advantage to reliable, profitable production involves navigating a set of risks that are specific to the operating environment:

- Governance and regulatory risk: Shifting royalty regimes, export restriction policies, and political instability in key producing nations can rapidly alter the economics of project development. The DRC in particular has a history of regulatory changes that have surprised investors and altered fiscal terms.

- Logistics fragility: The Kasumbalesa Bridge collapse and Dar es Salaam port disruptions have illustrated in real time how single-point infrastructure failures can paralyse export capacity across an entire producing region.

- Sulphur dependency: Until alternative acid supply chains are established at competitive cost and reliable volume, leaching-dependent operations remain exposed to geopolitical events in the Gulf region that were previously considered irrelevant to African mining risk assessments.

- Currency and fiscal risk: Copper-dependent economies like Zambia face amplified macroeconomic volatility when production volumes and commodity prices move in opposite directions, as they are doing in mid-2026.

- Energy availability: Domestic refining ambitions require reliable industrial-scale electricity, which remains constrained in several Copperbelt producing regions. Power shortages can reduce processing efficiency and create operational uncertainty that international capital finds difficult to price.

The Strategic Outlook for Africa's Copper Sector

Converting Geological Advantage Into Structural Market Leadership

The longer-term structural argument for African copper is compelling precisely because of what is happening elsewhere in the global supply base. Latin American operations — particularly in Chile and Peru — are increasingly processing lower-grade ores as their highest-quality deposits are depleted. Indonesian operations face both geological transition and, now, significant operational disruption. Australian copper is geographically distant from the demand centres driving growth in the energy transition.

Africa, by contrast, holds high-grade deposits in the Copperbelt that remain among the most cost-competitive sources of new copper production available globally. As the world's electrification programmes expand — requiring copper for EV charging infrastructure, offshore wind cabling, solar interconnects, and grid modernisation — the strategic importance of navigating copper supply disruptions and Africa opportunity together will only grow.

The critical variable is timeline. Africa's ability to convert geological advantage into dependable production volumes hinges on three deliverables that are currently in process but not yet complete:

- Completion and operationalisation of reliable export corridors, whether via the Lobito Atlantic route or the Tazara Indian Ocean route

- Diversification of sulphuric acid supply chains away from Gulf dependence, through long-term agreements with alternative suppliers and investment in on-site acid generation capacity

- Stable and predictable regulatory frameworks that attract and retain the international mining capital required to develop the next generation of Copperbelt deposits

Consequently, those developing copper investment strategies for the years ahead would be well advised to weight African exposure carefully, balancing the exceptional geological upside against the infrastructure, chemical supply chain, and governance risks outlined above.

"The copper market's current state — tight supply, muted price response, geopolitical disruption, and chemical shortages — represents a transitional phase rather than a structural ceiling. For Africa, the fundamental question is not whether the opportunity exists. The geological, economic, and strategic case is well established. The question is whether the infrastructure, governance continuity, and supply chain resilience required to fully capitalise on that opportunity can be assembled before the investment window narrows or competitor regions recover their operational footing."

This article contains forward-looking statements and forecasts, including commodity price projections and production estimates. These represent analytical perspectives based on available data and are subject to material risks, uncertainties, and changes in market conditions. Nothing in this article constitutes financial or investment advice. Readers should conduct independent research and seek professional guidance before making investment decisions.

Want to Catch the Next Major Copper Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries — including copper — and delivering actionable alerts to subscribers before the broader market can react. Explore how historic discoveries have generated substantial returns on Discovery Alert's dedicated discoveries page, and begin your 14-day free trial today to position yourself ahead of the next major find.