July 11, 2026

The Hidden Fee That's Reshaping Global Copper Markets

Most commodity market discussions focus on the LME copper price, but the economics underpinning how raw copper actually becomes usable refined metal are governed by a far less visible mechanism. Treatment and refining charges, universally abbreviated as TC/RCs in the industry, represent the fees miners pay to smelters for converting copper concentrate into cathode copper. For decades, these fees operated as a quiet but essential balancing mechanism between miners and processors. Today, that balance has fractured in ways that carry profound implications for global copper supply chains.

Understanding this shift requires looking beyond headline copper prices and into the structural dynamics of smelting economics, where Sumitomo Metal copper treatment charges have become a focal point for how the industry is navigating one of its most challenging pricing environments in recent memory.

When big ASX news breaks, our subscribers know first

Understanding TC/RCs: How Copper Processing Fees Actually Work

Copper concentrate, the product that emerges from mining operations after ore is crushed and processed, cannot be used directly in industrial applications. It must be smelted and refined into cathode copper before it enters manufacturing supply chains. Treatment Charges (TC) are the fees, expressed in US dollars per metric ton of concentrate, that miners pay smelters to perform this conversion. Refining Charges (RC) represent an additional fee expressed in cents per pound of copper recovered from that concentrate.

Together, TC/RCs constitute the primary revenue stream for copper smelters. They are typically negotiated annually through bilateral contracts, with a landmark deal between a major miner and a leading smelter establishing a benchmark rate that other market participants use as a reference. This system has functioned as a pricing anchor for the global copper processing industry for decades.

A key characteristic of TC/RCs that is often misunderstood outside the industry is their directional relationship to market power. When concentrate is abundant relative to smelting capacity, smelters can demand higher fees. When concentrate is scarce relative to processing capacity, miners gain leverage and fees compress. The current environment represents the latter scenario at an extreme, contributing directly to the broader copper supply crunch that has been building across global markets.

"When processing fees fall toward zero, the question is no longer about margin compression. It becomes a fundamental question about whether smelting capacity outside China's cost structure can remain economically viable at all."

How the 2025 and 2026 Benchmarks Reveal a Two-Tier Market

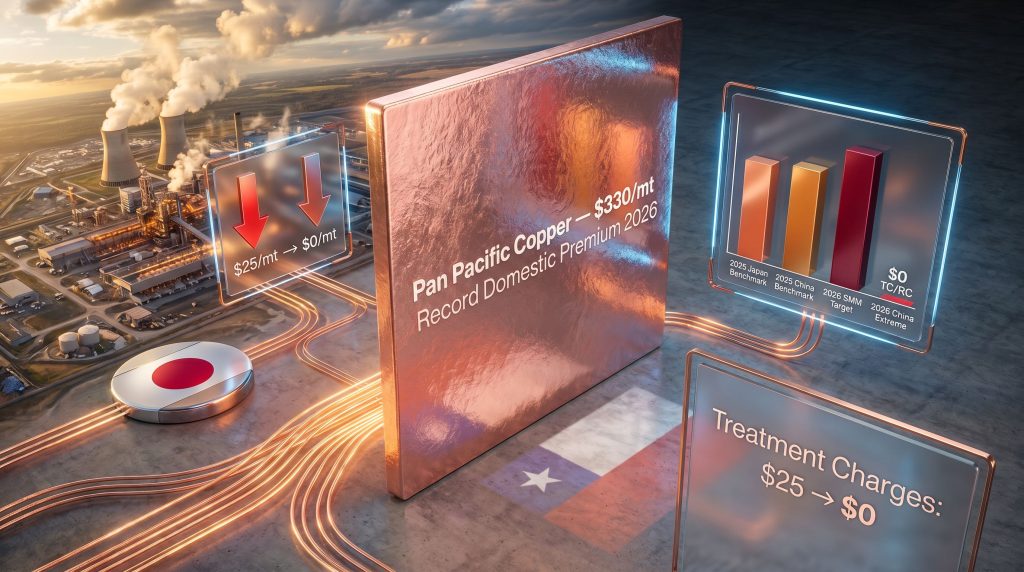

The divergence between Japanese and Chinese TC/RC benchmarks that emerged in 2025 was an early warning signal that the traditional unified pricing model was fragmenting. Japanese smelters, including Sumitomo Metal Mining, secured treatment charges of $25 per metric ton and refining charges of 2.5 cents per pound for 2025, according to Reuters reporting from May 11, 2026. A separate agreement struck between a Chilean miner and a Chinese smelter established a lower reference point of $21.25 per metric ton and 2.125 cents per pound.

That $3.75 per metric ton gap between Japanese and Chinese benchmarks was not merely a negotiating anomaly. It reflected a structural divergence in how different smelter cohorts interact with the concentrate market, with Chinese processors operating under different cost constraints and capacity utilisation pressures than their Japanese counterparts. Furthermore, Chile's copper supply gap has played a meaningful role in shaping the dynamics of these bilateral negotiations.

For 2026, the trajectory has deteriorated further across both regions. Sumitomo Metal copper treatment charges are expected to be finalised at double-digit levels per metric ton, representing a meaningful decline from the 2025 Japanese benchmark. The company has not disclosed a specific numerical target beyond characterising the anticipated outcome as double-digit, reflecting the commercial sensitivity of ongoing negotiations as of mid-May 2026.

At the most extreme end of the spectrum, Chinese smelters have reportedly accepted processing deals at effectively negligible fee levels as smelting overcapacity forces processors to compete aggressively for limited concentrate supply. Reports indicate that China's top copper smelters have been compelled to address negative processing economics, a condition where smelters are essentially paying to process concentrate rather than earning a margin from it. Copper smelting expansion across the region has been a central factor accelerating this race to the bottom on fees.

Year-on-Year TC/RC Benchmark Comparison

| Metric | 2025 Japan Benchmark | 2025 China Benchmark | 2026 SMM Guidance |

|---|---|---|---|

| Treatment Charge (TC) | $25/mt | $21.25/mt | Double-digit (<$25/mt) |

| Refining Charge (RC) | 2.5¢/lb | 2.125¢/lb | Double-digit (<2.5¢/lb) |

| Negotiating Driver | Side deal leverage | Capacity surplus | Supply tightness |

| Margin Pressure Level | Moderate | Elevated | Severe |

The Structural Forces Behind the TC/RC Collapse

Copper processing fees do not move in isolation. Their compression in 2026 reflects the convergence of several structural forces that have been building across the global copper supply chain for years.

Force 1: China's Smelting Buildout Has Outpaced Concentrate Supply

China's expansion of domestic copper smelting infrastructure has been substantial, creating a structural overhang of processing capacity relative to the global concentrate pool. With more smelters competing for a finite supply of copper concentrate, miners hold disproportionate negotiating leverage. This dynamic is the single most important driver of TC/RC compression, with global smelting capacity, led by China, expanding faster than mined supply.

The overcapacity problem is compounded by the incentive structure facing Chinese smelters. Maintaining throughput, even at near-zero or negative processing margins, can be economically rational for operators who need to cover fixed costs, retain workforce capacity, and maintain supplier relationships. This dynamic creates a floor-less pricing environment where traditional cost-based negotiating floors lose their anchoring function.

Force 2: Mine Supply Disruptions Have Tightened the Concentrate Pool

On the supply side, the concentrate market has faced headwinds from operational disruptions at major copper mining assets. The Freeport-McMoRan Grasberg complex in Indonesia, one of the world's largest copper producers, has faced delays in returning to full operational capacity, with a full restart now targeted for early 2028. This represents a meaningful reduction in globally available concentrate at a time when smelting capacity continues to grow.

Additional supply disruptions, including flooding-related shutdowns at other operations, have further tightened the concentrate balance. The net effect is a pronounced gap between installed smelting capacity and available feed material, which structurally advantages miners in pricing negotiations and reinforces the underlying copper price drivers that analysts have been tracking closely.

Force 3: The Annual Benchmark System Is Fragmenting

Perhaps the most consequential structural shift is the erosion of the annual benchmark system itself. Historically, a single landmark deal set a reference rate that anchored secondary contracts across the market. As bilateral agreements at widely varying fee levels proliferate, including deals struck at effectively zero processing fees, the shared reference rate loses its stabilising function.

This transition toward spot-like bilateral pricing introduces significantly greater uncertainty for smelters operating outside China's cost structure. Industry analysts covering copper smelter fee negotiations have noted that each contract negotiation now reflects real-time supply and demand conditions rather than a shared market convention.

How Sumitomo Metal Mining Is Responding

Despite the challenging fee environment, Sumitomo Metal Mining has adopted a notably measured strategic posture. The company has confirmed it has no plans to curtail primary copper metal production volumes, a stance that diverges from responses seen among some Chinese smelters that have announced output reductions to address negative processing economics.

This decision to maintain production reflects two key considerations. First, Sumitomo Metal Mining's executive leadership has indicated that elevated physical copper premiums will partially compensate for the decline in TC/RC income. Physical copper premiums are charges applied above the LME price for the delivery of refined copper in specific markets. When refined copper availability tightens in regional markets, these premiums can rise substantially, providing an alternative revenue stream that partially offsets processing fee losses.

Second, maintaining production preserves Sumitomo's market position and supplier relationships during what management expects to be a transitional period. The company's finance and accounting executive stated publicly that the supply and demand balance in the copper concentrate market is expected to normalise as miner output recovers, though no specific timeframe was provided. This cautious optimism suggests the production maintenance decision is premised on a belief that current fee compression represents a cycle trough rather than a permanent structural floor.

The critical caveat here is that the pace of concentrate supply recovery remains genuinely uncertain. Grasberg's delayed restart, flooding disruptions at other operations, and the structural nature of Chinese smelting overcapacity mean that normalisation timelines are subject to significant revision.

Broader Implications for the Global Copper Supply Chain

The compression of Sumitomo Metal copper treatment charges is not merely a firm-specific story. It is a symptom of structural shifts that carry implications across the entire copper value chain.

The Viability Question for Non-Chinese Smelters

Japanese, South Korean, and European copper smelters operate at materially higher cost structures than their Chinese counterparts. They face labour costs, environmental compliance expenses, and energy costs that cannot be compressed in the same way as some Chinese facilities. For these operators, prolonged periods of near-zero processing fees create an existential margin problem that cannot be fully resolved through premium offsets alone.

If TC/RCs remain structurally depressed over a multi-year horizon, the economic case for maintaining primary copper smelting capacity outside China weakens considerably. Capacity rationalisation, whether through outright closures, production curtailments, or consolidation, becomes a realistic medium-term scenario. This would paradoxically tighten refined copper availability in key consumption markets even as smelting overcapacity persists globally.

The Geopolitical Dimension

A less discussed but critically important implication of sustained TC/RC compression is the geographic concentration of copper refining capacity it could accelerate. If non-Chinese smelters cannot operate viably at current processing fee levels, the share of global refined copper production occurring within China would increase. For Western industrial economies that rely on copper for electrification infrastructure, electric vehicles, and defence manufacturing, this concentration creates supply chain vulnerability that extends well beyond commercial economics.

This risk is not hypothetical. The iron ore and rare earth industries provide historical precedents where geographic concentration of processing capacity created leverage asymmetries that proved difficult and expensive to reverse. Indeed, the top copper producer rankings globally are already shifting in ways that reflect these deepening structural pressures.

What Investors and Analysts Should Watch

For those monitoring the copper sector, several indicators deserve close attention:

- Concentrate supply recovery pace: The speed at which major mining assets like Grasberg return to full production will be the primary determinant of whether TC/RCs recover meaningfully from current levels.

- Chinese smelter output decisions: Voluntary production curtailments by Chinese smelters could reduce the effective overcapacity and provide some floor under processing fees.

- Physical copper premium trajectories: Rising premiums in key regional markets like Japan signal tightening in refined copper availability and represent the primary offset mechanism for smelters absorbing lower processing fees.

- Bilateral contract disclosures: Individual deal announcements, particularly those involving major miners and Chinese processors, will reveal whether the floor in TC/RCs has been reached or whether further compression is possible.

- Non-Chinese smelter capacity announcements: Any announcements of curtailments, closures, or consolidation among Japanese, South Korean, or European smelters would signal that the current fee environment is proving unsustainable at the operational level.

Reporting on how the pricing system is cracking under these pressures has intensified in 2025 and 2026, reflecting growing concern among industry participants about the long-term viability of current negotiating frameworks.

The next major ASX story will hit our subscribers first

Frequently Asked Questions: Copper TC/RCs in 2026

What are copper treatment and refining charges?

TC/RCs are fees paid by copper miners to smelters for processing raw copper concentrate into refined cathode copper. Treatment Charges are denominated in US dollars per metric ton of concentrate processed. Refining Charges are expressed in cents per pound of copper metal recovered. Both fees are deducted from the LME copper price in supply contracts, making them a direct determinant of smelter profitability.

Why are TC/RCs falling so sharply in 2026?

The primary driver is a structural imbalance between smelting capacity and concentrate supply. China has significantly expanded its copper smelting infrastructure, creating excess processing capacity relative to the available concentrate pool. Simultaneously, mine supply has been constrained by operational disruptions at major producing assets, tightening concentrate availability and shifting negotiating leverage decisively toward miners.

What TC/RC level is Sumitomo Metal Mining targeting for 2026?

According to Reuters reporting from May 11, 2026, Sumitomo Metal Mining expects to secure double-digit treatment charges per metric ton for 2026, which would represent a decline from the 2025 Japanese benchmark of $25 per metric ton. Negotiations were still in final stages as of that date and no specific figure beyond the double-digit characterisation had been disclosed.

How do copper premiums offset lower processing fees?

Physical copper premiums are charges applied above the LME reference price for the delivery of refined copper in specific regional markets. When refined copper availability tightens, these premiums rise, providing smelters with additional revenue per unit of metal sold. Sumitomo Metal Mining's executive leadership has confirmed that elevated premiums are expected to partially compensate for weaker TC/RC income, though the offset is characterised as partial rather than complete.

Is TC/RC compression a temporary cyclical problem or a permanent structural shift?

Sumitomo Metal Mining's public commentary suggests management views current conditions as cyclical, with concentrate supply expected to normalise as miner output recovers. However, the structural overcapacity of Chinese smelting infrastructure is unlikely to resolve quickly, and the fragmentation of the annual benchmark system toward bilateral spot-like pricing introduces a longer-term structural dimension to the problem. Both cyclical and structural forces are present simultaneously, making the trajectory genuinely uncertain.

What happens to global copper supply if non-Chinese smelters become unviable?

If sustained fee compression forces capacity rationalisation outside China, the geographic concentration of copper refining would increase, tightening refined copper availability in Western markets and raising supply chain risks for industrial economies dependent on copper for electrification and manufacturing. This scenario would likely result in higher physical copper premiums in non-Chinese markets and potentially higher LME copper prices over the medium term.

This article is intended for informational purposes only and does not constitute financial or investment advice. Statements regarding future TC/RC rates, concentrate market normalisation, and smelter viability are inherently uncertain and subject to change based on market conditions, company decisions, and events that cannot be predicted with certainty. Readers should conduct their own independent research before making any investment decisions.

Want to Capitalise on Structural Shifts Driving the Next Major Copper Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant copper discoveries are announced on the ASX, turning complex mineral data into actionable investment insights — explore historic discovery returns on the Discovery Alert discoveries page to understand the scale of opportunity these structural supply pressures can create, and begin your 14-day free trial today to position yourself ahead of the broader market.