July 7, 2026

The Copper Market's Most Reliable Signal Is Flashing Red

For most of the past century, commodity markets have moved in cycles driven by price, speculation, and macroeconomic momentum. Investors trained on these cycles instinctively reach for copper price charts when assessing the health of the sector. Yet one of the most analytically powerful signals in the entire copper supply chain receives a fraction of the attention it deserves: the treatment and refining charge benchmark. When that benchmark reaches zero-dollar copper treatment charges, as it did in 2026, the market is not simply communicating a smelter profitability problem. It is broadcasting a structural mine supply crisis that no amount of capital, policy, or price momentum can resolve quickly.

Understanding why requires stepping back from the copper price itself and examining the mechanics of how raw mine output is converted into refined metal.

When big ASX news breaks, our subscribers know first

What Treatment and Refining Charges Actually Measure

Treatment charges (TCs) and refining charges (RCs) are the fees that copper smelters levy on mining companies to process copper concentrate into refined cathode copper. They are deducted from the price a miner receives for its concentrate. When concentrate is abundant and smelters are competing for feedstock, miners can negotiate lower charges. When concentrate is scarce and miners hold the leverage, TCs rise. The directional logic is inverse to most commodity pricing intuitions: falling TCs signal tightening mine supply, not falling demand.

This makes TC/RC data one of the few genuinely real-time indicators of physical copper concentrate availability, operating independently of financial market sentiment. Furthermore, the copper supply crunch currently unfolding is reflected nowhere more clearly than in these benchmark figures.

The 2026 annual benchmark settlement between a major Chilean producer and a leading Chinese smelter set treatment charges at US$0 per tonne and refining charges at 0 cents per pound, the lowest benchmark on record. The year prior, the equivalent benchmark stood at US$21.25 per tonne and 2.125 cents per pound. The year before that, US$80 per tonne. The collapse has been swift, structural, and unambiguous.

| Year | Benchmark TC (US$/tonne) | Benchmark RC (US¢/lb) |

|---|---|---|

| 2021 | ~$59.50 | ~5.95¢ |

| 2022 | ~$65.00 | ~6.50¢ |

| 2023 | ~$80.00 | ~8.00¢ |

| 2024 | ~$80.00 | ~8.00¢ |

| 2025 | $21.25 | 2.125¢ |

| 2026 | $0.00 | 0.00¢ |

Sources: Fastmarkets; Reuters; industry benchmark settlements

How a Decade of Asymmetric Investment Created This Crisis

The zero-dollar benchmark did not emerge from a single disruption or a short-term demand shock. It is the product of a decade-long structural divergence between smelting capacity expansion and mine supply growth.

China expanded its copper smelting capacity at approximately four times the rate of global concentrate supply growth over the past decade. The economics of smelter construction are fundamentally different from those of mine development. A smelter can be permitted, financed, and commissioned within two to four years. A copper mine, from initial discovery through resource definition, feasibility studies, environmental permitting, financing, engineering, and construction, typically requires ten years or more before producing its first tonne of refined copper.

This asymmetric development timeline created a structural feedstock deficit that was partially concealed during periods when strong mine output growth kept pace with smelting expansion. As that mine output growth stalled, the mismatch became impossible to ignore.

Spot Markets: When Zero Became the Ceiling, Not the Floor

While the annual benchmark provides the headline figure, spot TC/RC markets reveal the true severity of the imbalance in real time. Spot rates entered negative territory during 2025, reaching approximately -$40 per tonne at mid-year. By early 2026, spot rates had deteriorated further to approximately -$90 per tonne, meaning smelters were effectively subsidising miners to secure access to feedstock at all.

Fastmarkets projected the 2025 average TC at approximately $10.70 per tonne, one of the lowest annual averages ever recorded. At a spot rate of -$90 per tonne, smelters were absorbing estimated losses of up to $415 per tonne of copper processed. That figure is not a rounding error. It is a financially unsustainable position that directly triggered coordinated output reductions across China's largest custom smelting operations. Antofagasta's agreement to zero processing charges for 2026 with a leading Chinese smelter underscores precisely how extreme this imbalance has become.

Negative spot treatment charges represent something historically rare: smelters operating at a net loss on the processing function itself, sustained only by byproduct revenue from sulfuric acid sales and gold and silver credits recovered during refining. This revenue model shift is not a temporary patch. It reflects a fundamental restructuring of smelter economics under conditions of prolonged concentrate scarcity.

The Paradox of Rising Refined Output Amid Concentrate Scarcity

One of the more counterintuitive data points in the current cycle is that Chinese refined copper production grew approximately 7.4% year-over-year from January through April 2026, even as Chinese smelters had pledged collective output reductions exceeding 10% due to the concentrate shortage.

This apparent contradiction requires careful interpretation. Smelters drew down existing concentrate inventories and utilised operational flexibility to maintain throughput in the near term. Refined production figures therefore lagged the physical constraint rather than immediately reflecting it. The persistence of refined output growth does not disprove the supply thesis. It accelerates it, by depleting available feedstock inventories faster and pulling the production constraint forward in time.

The Chinese government's decision to halt new smelter approvals in response to the feedstock imbalance is itself a significant signal. It confirms that even policymakers have recognised that additional smelting capacity would only deepen the structural problem.

Why Higher Copper Prices Cannot Solve a Mine Supply Deficit

This is arguably the most important and least understood aspect of the current market dynamic. Conventional commodity cycle logic suggests that rising prices stimulate new supply. In copper mining, however, this mechanism is severely constrained by irreducible development timelines.

Consider the critical path required to bring a new copper mine into production:

- Initial discovery and target definition through regional exploration

- Resource definition drilling to establish an inferred mineral resource

- Economic scoping studies to assess preliminary viability

- Prefeasibility and feasibility studies incorporating engineering, metallurgy, and cost estimation

- Environmental and social impact assessments submitted for regulatory review

- Permitting and approvals across multiple jurisdictions and agencies

- Project financing secured from lenders and equity partners

- Engineering, procurement, and construction of all site infrastructure

- Commissioning and ramp-up to design capacity

In major copper jurisdictions including Chile, Peru, Canada, and the United States, this sequence routinely spans a decade or longer. Regulatory review timelines are largely insensitive to commodity price cycles. BHP has publicly projected zero mine output growth from Chile between 2031 and 2040, a statement that carries profound implications given Chile's status as the world's largest copper-producing nation, accounting for approximately 27% of global mine supply.

The Chile copper outlook reflects these structural constraints acutely: declining ore grades at mature operations, intensifying water scarcity in the Atacama and Antofagasta regions, and rising energy costs have collectively capped the country's ability to expand production. These are geological and environmental realities that copper prices alone cannot overcome.

How Zero-Dollar TCs Reshape Copper Project Valuation

For developers advancing copper projects through the feasibility and financing pipeline, the structural concentrate shortage has a direct and quantifiable impact on project economics. In addition, understanding the broader copper price drivers helps contextualise why these projects are attracting renewed investor interest.

Copper project feasibility studies use long-term price assumptions to calculate post-tax net present value (NPV) and internal rate of return (IRR). Sustained concentrate scarcity provides analytical justification for elevating those long-term price assumptions. Higher assumptions feed directly into NPV calculations, improving the metrics that lenders and equity partners evaluate when assessing project financing.

Consider how this plays out across different project archetypes:

| Project Archetype | Key Advantage | Primary Risk | Typical Timeline to Production |

|---|---|---|---|

| Reserve-backed developer (feasibility complete) | Higher NPV under elevated price assumptions; financing-ready | Execution risk; capex inflation | 3-5 years |

| Past-producing restart asset | Existing infrastructure; lower capex; shorter timeline | Resource confidence; rehabilitation costs | 2-4 years |

| Advanced explorer (resource defined, PEA-stage) | De-risked resource; M&A appeal | Permitting; financing; feasibility execution | 5-10 years |

| Greenfield early-stage discovery | High optionality; acquisition target potential | Long timeline; resource uncertainty | 8-15+ years |

Offtake partners and cathode buyers facing long-term supply uncertainty are increasingly motivated to secure future supply agreements ahead of final investment decisions. This commercial urgency provides development-stage companies with the kind of contractual validation that can unlock project financing in otherwise challenging capital markets.

Real-World Project Examples Illustrating the Investment Thesis

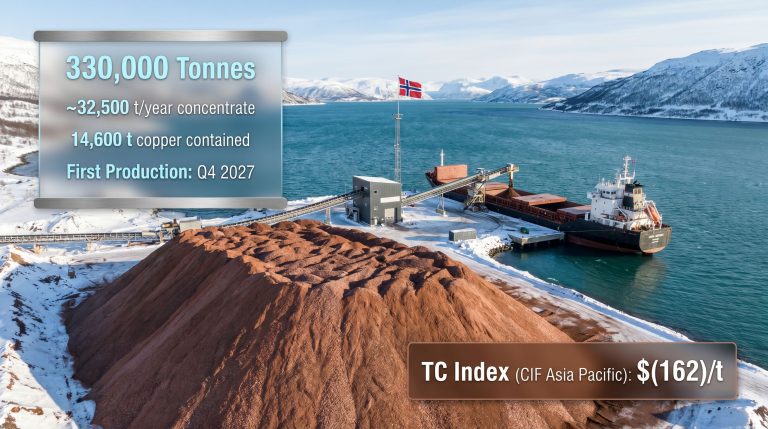

Marimaca Copper is advancing the Marimaca Oxide Deposit toward a final investment decision in Chile's Antofagasta region. The project holds Proven and Probable reserves of 748,000 tonnes of contained copper, supporting a post-tax NPV of approximately US$1.1 billion at an 8% discount rate. The company is also drilling the separate high-grade Pampa Medina target, adding exploration upside beyond the defined reserve base. Marimaca's chief executive has noted publicly that the project's operating cost structure is expected to remain well below US$300 per tonne, providing resilience across a range of copper price scenarios.

Selkirk Copper is advancing the past-producing Minto copper project in Yukon as a restart candidate. An existing mineral resource estimate supports an updated preliminary economic assessment, with a definitive feasibility study and targeted production restart by mid-2028. In a market that urgently needs new mine supply, a project capable of reaching production within two to three years carries a timing premium that greenfield developments simply cannot match.

Abitibi Metals is advancing the B26 polymetallic deposit in Quebec's Abitibi Greenstone Belt, where the combined resource has expanded to approximately 25.3 million tonnes grading 2.15% copper equivalent, representing a 124% increase since 2023. The company is targeting a preliminary economic assessment in the first quarter of 2027. Industry participants have noted that copper-gold deposits of this scale and grade have become among the most sought-after acquisition targets in the current market, with recent M&A activity confirming strong demand for large, long-life assets in proven jurisdictions.

Fitzroy Minerals is conducting an approximately 22,000-metre drill program at the Buen Retiro copper project in Chile's Atacama region, where recent drilling returned 59.0 metres grading 1.73% copper. Industry observers have highlighted that production growth in Chile and globally faces severe structural constraints, with the capital intensity of new projects rising and established mines struggling to maintain flat output.

Mogotes Metals is advancing the Albor discovery at its Filo Sur project in Argentina, where drilling returned 86 metres at 0.70% copper, including 43 metres at 1.1% copper. The project sits directly along strike from a major district-scale discovery. The rarity of large copper-gold finds of this kind has been openly acknowledged by industry executives, who note that such discoveries attract acquisition interest regardless of whether the company is actively seeking a transaction.

Cobra Resources is advancing the Manna Hill copper project in South Australia's proven porphyry and skarn province, a region that hosts several Tier-1 copper deposits exceeding one million tonnes of contained copper. Recent drilling at the Blue Rose prospect returned intercepts including 74 metres at 1.02% copper, illustrating the district's potential to yield additional large-scale mineralisation.

The next major ASX story will hit our subscribers first

Geopolitical Dimensions and Jurisdictional Value

The structural supply deficit has amplified the premium attached to copper projects located in stable, mining-friendly jurisdictions. Political and regulatory risk in several emerging copper regions has increased over recent years, making established provinces in Chile, Canada, Australia, and the United States relatively more attractive to project financiers and potential acquirers. Consequently, the copper project pipeline in these regions has become a focal point for strategic investment activity.

Argentina's copper endowment remains significantly underexplored relative to its geological potential, with several large-scale porphyry systems at early development stages. Canada's Yukon and British Columbia host past-producing copper assets with existing infrastructure. South Australia's Olympic Copper Province contains multiple Tier-1 scale deposits at various stages of exploration and development.

What acquirers are prioritising across all jurisdictions can be distilled into four criteria:

- Grade: High-grade deposits reduce operating costs per pound and maintain project economics across wider price ranges

- Scale: Large resource bases justify the capital intensity of new development through long mine lives

- Jurisdiction: Stable permitting environments reduce execution risk and timeline uncertainty

- Infrastructure proximity: Access to existing processing facilities, power, and transport networks compresses capital requirements

The Long-Term Investment Case: A Decade-Long Structural Theme

The zero-dollar copper treatment charges benchmark is not a one-year anomaly that will self-correct when the next price cycle turns. It is the clearest market signal yet that the copper industry has entered a prolonged period of mine supply scarcity, with consequences that extend well beyond smelter profitability metrics.

The demand side of the equation provides no relief from the pressure. Electrification of transportation and power systems, grid investment programmes across North America, Europe, and Asia, and the rapid expansion of data centre infrastructure driven by artificial intelligence and cloud computing all operate on multi-decade investment cycles. Each of these end markets requires substantially more copper per unit of delivered energy or computing capacity than the conventional infrastructure it replaces.

The supply response, by contrast, will be slow and structurally constrained. The global copper project development pipeline contains insufficient near-term production to offset declining output from mature operations. Furthermore, rising capital intensity, increasing permitting complexity, and declining ore grades at existing mines collectively cap the pace at which new supply can reach the market. As Bloomberg's reporting on Chinese smelter fee negotiations confirms, the record-low fee environment is being recognised at the highest levels of the global financial press.

The implication for investors is that the structural case for copper exposure across the project development spectrum has rarely been more analytically grounded. Development-stage projects with strong economics, past-producing assets with existing infrastructure, and high-grade exploration discoveries in established Tier-1 provinces are all positioned to benefit from a market in which new mine supply remains exceptionally difficult to replace over multiple years.

Most industry analysts expect TC/RC rates to remain structurally depressed until a meaningful volume of new mine supply reaches production, a scenario that appears unlikely before the early 2030s at the earliest. For investors and project developers navigating this environment, the zero-dollar copper treatment charges benchmark is not just a data point. It is a decade-long structural theme written in the language of supply chain economics.

Disclaimer: This article is intended for informational purposes only and does not constitute financial advice. Forecasts, projections, and long-term price assumptions involve inherent uncertainty. Past performance of commodity markets is not indicative of future results. Investors should conduct independent due diligence before making investment decisions.

Want to Be First to Capitalise on the Next Major Copper Discovery?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant copper and mineral discoveries so subscribers can act ahead of the broader market — explore historic discovery returns to understand what's at stake, then begin your 14-day free trial at Discovery Alert to position yourself at the forefront of the next major find.