June 13, 2026

Critical Materials Market Dynamics in Defense Manufacturing

Modern defense manufacturing operates within an intricate web of specialized materials, where certain metals possess properties that cannot be replicated or substituted without significant performance degradation. Among these materials, tungsten occupies an extraordinary position due to its exceptional physical characteristics that make it indispensable for military applications requiring extreme durability and precision. The recent tungsten prices surge amid Middle East conflict has highlighted the vulnerability of global supply chains for strategic materials.

The global tungsten market represents a microcosm of broader critical materials vulnerabilities, where concentrated production, technical complexity, and strategic importance create conditions for dramatic price volatility. Understanding these dynamics requires examining the fundamental properties that drive demand, the supply chain bottlenecks that constrain availability, and the geopolitical factors that amplify market disruptions.

When big ASX news breaks, our subscribers know first

Physical Properties Driving Strategic Applications

Tungsten's unique metallurgical characteristics establish it as irreplaceable in high-performance military systems. With a density of 19.3 grams per cubic centimeter, tungsten approaches twice the density of lead, providing kinetic energy advantages in ballistic applications that no alternative material can match. This density, combined with its melting point of 3,422°C (the highest among all metallic elements), creates performance capabilities that define modern military effectiveness.

Defense-Critical Applications Include:

- Armor-piercing ammunition cores requiring maximum kinetic penetration

- Aircraft engine components withstanding extreme temperature cycling

- Missile guidance systems demanding precision under high-stress conditions

- Military vehicle armor plating providing ballistic protection

The technical specifications for military-grade tungsten exceed civilian standards significantly. Defense applications typically require purity levels above 99.9%, dimensional tolerances measured in microns, and material traceability documenting the complete supply chain from ore extraction through final component manufacturing.

Supply Concentration Creates Market Vulnerability

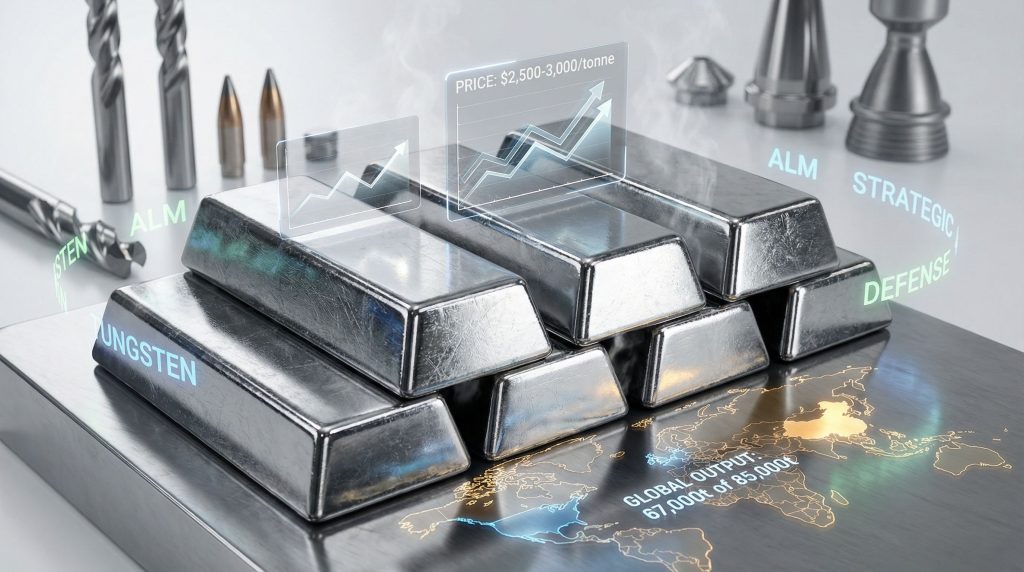

The tungsten market operates under extreme concentration that amplifies price responses to any supply disruption. Analysis of global production reveals a market structure where a single nation controls the overwhelming majority of both raw material extraction and processing capabilities. This concentration has become a key factor in the ongoing critical minerals strategy discussions globally.

2025 Global Tungsten Production Analysis:

| Producer | Output (Tonnes) | Market Share | Processing Capacity |

|---|---|---|---|

| China | 67,000 | 78.8% | Integrated ore-to-product |

| Vietnam | 3,000 | 3.5% | Limited processing |

| Rest of World | <15,000 | 17.7% | Fragmented capacity |

| Total Global | 85,000 | 100% | Variable standards |

This concentration creates a supply environment where Chinese production decisions directly determine global availability. The market structure becomes particularly problematic when considering that military tungsten demand, while representing approximately 12% of total consumption, operates under procurement constraints that cannot accommodate delays or quality compromises.

Defense contractors typically establish long-term supply agreements with fixed pricing structures, creating additional complexity when spot market prices experience rapid increases. These contracts often include specifications that exceed civilian-grade materials, requiring suppliers to maintain separate production lines and quality control systems.

Export Control Mechanisms Amplify Tightness

The implementation of strategic export controls represents a sophisticated tool for leveraging commodity markets in geopolitical disputes. Recent policy changes have created measurable impacts on global tungsten availability, with quantified effects on international supply chains. Furthermore, the trade war impact has intensified these dynamics significantly.

February 2025 Export Control Implementation:

Chinese authorities added specific tungsten products to controlled export lists, targeting materials with direct military applications. This policy change created immediate market effects:

- Supply reduction: Exports of restricted tungsten products declined 40% in the following year

- Price discovery disruption: Limited transparent pricing mechanisms outside Chinese markets

- Stockpile depletion: Western inventories drawn down faster than replacement rates

- Alternative sourcing pressure: Increased demand concentrated on limited non-Chinese suppliers

Controlled Product Categories:

-

Military-Grade Tungsten Powder

- Specifications: 99.9%+ purity requirements

- Applications: Ammunition cores, ballistic protection

- Processing: Chemical precipitation and reduction techniques

-

Tungsten Carbide Tools

- Properties: Vickers hardness 1,400-1,700 HV

- Applications: Precision machining, drilling equipment

- Manufacturing: Specialised sintering processes

-

Aerospace-Grade Alloys

- Composition: Tungsten with nickel, iron, molybdenum additions

- Standards: AS9100 quality management requirements

- Properties: High-temperature stability, controlled thermal expansion

The export restrictions operate through licensing requirements that create processing delays and regulatory uncertainty for international buyers. These mechanisms effectively reduce available supply without formal embargoes, creating plausible diplomatic cover while achieving strategic objectives.

Alternative Production Sources Face Technical Barriers

Development of non-Chinese tungsten production encounters substantial technical and economic challenges that extend far beyond simple mining operations. Successful tungsten projects require integrated capabilities spanning extraction, chemical processing, and specialised manufacturing. The mining industry evolution has highlighted these complex requirements across multiple sectors.

Almonty Industries South Korean Operations:

The restart of the Sandong mine in South Korea represents the first significant non-Chinese capacity addition in recent years. This facility, originally developed during Japanese occupation (1910-1945), required extensive modernisation to meet current military specifications.

Operational Characteristics:

- Location: Sandong mine, South Korea

- Status: Operational as of March 2026

- Capacity allocation: Approximately 50% designated for Pennsylvania munitions manufacturing

- Strategic significance: Direct engagement with US government procurement agencies

- Timeline: Two-year development cycle for full production capability

The Pennsylvania connection illustrates integrated defense supply chain planning, where tungsten production directly supports ammunition manufacturing for military applications. This vertical integration approach reduces supply chain vulnerabilities whilst ensuring material traceability requirements.

North American Development Pipeline:

Montana Projects:

- Operator: Almonty Industries

- Development status: Planning and permitting phases

- Challenges: Environmental regulations, infrastructure requirements

- Timeline: Minimum 24-month development period

Canadian Potential:

- Cantung mine: Closed in 2015 following North American Tungsten bankruptcy

- Location: Yukon-Northwest Territories border

- Redevelopment barriers: Capital requirements, processing infrastructure

- Strategic considerations: Allied nation production advantages

Technical Processing Requirements Create Entry Barriers

Tungsten extraction and processing involve complex metallurgical procedures that require specialised equipment, technical expertise, and substantial capital investment. These requirements create significant barriers for new market entrants and explain the persistence of supply concentration.

Processing Complexity Analysis:

Ore Extraction and Concentration:

- Tungsten occurs in scheelite and wolframite ores requiring selective mining

- Concentration processes involve flotation and magnetic separation

- Ore grades typically range from 0.1% to 1.5% tungsten trioxide

- Processing generates significant waste streams requiring environmental management

Chemical Processing Requirements:

- Acid leaching: Hydrochloric or hydrofluoric acid systems

- Precipitation: Controlled pH and temperature conditions

- Purification: Ion exchange or solvent extraction techniques

- Reduction: High-temperature hydrogen atmosphere furnaces

Military Specification Manufacturing:

- Powder production: Particle size distribution controls

- Alloy formulation: Precise composition ratios

- Quality testing: Extensive analytical and physical property verification

- Traceability documentation: Complete supply chain records

The technical barriers become particularly significant for military-grade materials, where specification deviations can result in component failure under operational conditions. Defense contractors maintain approved supplier lists that require extensive qualification processes, creating additional market entry challenges.

The next major ASX story will hit our subscribers first

Military Demand Patterns Drive Price Volatility

Defense procurement operates under unique constraints that amplify tungsten market volatility. Military tungsten demand exhibits characteristics that differ fundamentally from civilian applications, creating price dynamics that traditional commodity analysis fails to capture. The development of a critical minerals reserve has become increasingly important in this context.

Defense Procurement Characteristics:

Specification Requirements:

- Ballistics applications: Density uniformity within ±0.1% tolerance

- Aerospace components: Temperature cycling resistance (-55°C to +200°C)

- Guidance systems: Dimensional precision to micron tolerances

- Armor applications: Hardness specifications exceeding 350 HV

Procurement Timeline Constraints:

- Production schedules: Fixed delivery requirements regardless of market conditions

- Quality verification: Extended testing protocols before acceptance

- Strategic stockpiling: Accelerated acquisition during geopolitical tensions

- Budget cycles: Concentrated purchasing within fiscal year periods

Recent Middle East conflict escalation has created measurable increases in tungsten prices surge amid Middle East conflict, with defense procurement agencies actively seeking immediate material availability. Reports indicate military tungsten consumption projected to increase 12% during the current year, representing significant demand growth in an already constrained market.

Government engagement extends beyond standard procurement processes, with authorities directly contacting suppliers regarding immediate availability. This direct engagement indicates supply concerns at policy levels and suggests strategic material priorities that transcend normal market mechanisms.

Investment Market Response to Supply Constraints

Financial markets have responded to tungsten supply dynamics through both direct equity investments and broader strategic materials positioning. The concentrated market structure creates unique investment opportunities whilst presenting substantial risk factors.

Direct Exposure Investment Vehicles:

Almonty Industries (NASDAQ: ALM):

- Primary pure-play tungsten producer outside China

- South Korean operations providing immediate production capability

- Montana development projects offering North American supply diversity

- Direct government procurement relationships

Indirect Beneficiary Analysis:

- Defense contractors: Material cost pass-through mechanisms in government contracts

- Tungsten carbide tool manufacturers: Industrial demand growth from defense production

- Recycling operations: Higher scrap tungsten values improving processing economics

- Mining equipment suppliers: Tungsten carbide cutting tool demand increases

Strategic Materials Investment Considerations:

Positive Investment Factors:

- Supply concentration advantages: Limited competition for established producers

- Demand inelasticity: Few viable substitute materials for critical applications

- Strategic government support: Policy incentives for domestic production development

- Recycling value enhancement: Growing secondary supply economics

Investment Risk Factors:

- Market size limitations: Global market approximately $16 billion constrains scalability

- Technology substitution research: Development of alternative high-performance materials

- Geopolitical policy volatility: Export control changes creating rapid market shifts

- Environmental regulatory increases: Processing restrictions affecting production costs

Price Scenario Analysis Under Geopolitical Stress

Current market conditions create unprecedented tungsten price volatility, with traditional forecasting models providing limited predictive value. Analysis requires considering multiple scenario pathways based on geopolitical developments, supply chain responses, and demand evolution. The recent executive order on minerals has further complicated these dynamics.

Market Driver Assessment:

Short-term Factors (6-12 months):

- Middle East conflict duration and intensity levels

- Chinese export policy adjustments or escalation

- Strategic stockpile acquisition programme implementation

- Alternative supply source development progress

Medium-term Considerations (1-3 years):

- New mine development completion and production ramp-up

- Processing capacity expansion in Western nations

- Technology substitution research breakthrough potential

- Secondary supply infrastructure development

Long-term Structural Changes (3+ years):

- Permanent supply chain diversification achievement

- Advanced material alternatives achieving military qualification

- Recycling technology improvements reducing primary demand dependency

- International cooperation frameworks for critical materials access

The 557% price increase since February 2025 represents more than temporary geopolitical response, indicating fundamental structural changes in critical materials markets. According to industry analysis, this level of price movement suggests supply-demand imbalances that cannot be resolved through traditional market mechanisms alone.

Strategic Material Security Implications

Western governments recognise tungsten supply vulnerability as representative of broader critical materials dependencies that threaten defense industrial base security. Policy responses involve comprehensive strategies extending beyond individual commodity markets.

Government Response Mechanisms:

Strategic Stockpile Expansion:

- Multi-year acquisition programmes for tungsten and related materials

- Budget allocations for strategic material inventory building

- Coordination between allied nations for collective stockpiling

- Priority purchasing agreements with domestic and allied producers

Production Incentive Programmes:

- Tax credits for domestic tungsten production development

- Loan guarantee programmes for mining project financing

- Accelerated permitting for strategic material projects

- Research funding for processing technology advancement

Supply Chain Resilience Initiatives:

- Vertical integration between defense contractors and material suppliers

- Supplier diversification requirements for defense contracts

- Alternative material qualification and testing programmes

- International cooperation agreements for mutual supply security

Canada, the United States, and the European Union have classified tungsten as a critical mineral, reflecting recognition of its strategic importance beyond current market dynamics. This classification provides policy frameworks for government intervention during supply disruptions and justification for supporting domestic production development.

Why Are Alternative Materials Struggling to Replace Tungsten?

While tungsten's unique properties make substitution difficult, ongoing research efforts focus on alternative materials and processing improvements that could reduce dependence on primary tungsten supply. These developments represent potential long-term market disruptors.

Alternative Material Research:

Advanced Ceramic Composites:

- Silicon carbide-based materials for certain high-temperature applications

- Aluminium oxide combinations achieving improved hardness characteristics

- Composite materials combining multiple elements for specific performance requirements

- Processing improvements reducing manufacturing costs

Recycling Technology Advancement:

- Closed-loop material recovery systems for tungsten carbide tools

- Chemical processing improvements for tungsten reclamation from scrap

- Quality improvement techniques for recycled tungsten meeting military specifications

- Economic optimisation making recycled tungsten cost-competitive

Processing Efficiency Improvements:

- Ore processing techniques improving tungsten recovery rates

- Energy efficiency improvements reducing production costs

- Quality control automation reducing manufacturing variability

- Environmental impact reduction technologies

However, military qualification processes for alternative materials require extensive testing protocols spanning multiple years. Defense applications cannot accept performance uncertainties, creating substantial barriers for material substitution even when alternatives demonstrate promise in laboratory conditions.

Market Structure Evolution and Investment Implications

The current tungsten prices surge amid Middle East conflict represents a fundamental test case for Western strategic material security policies. Market responses, government interventions, and industry adaptations will establish precedents for managing other critical material dependencies.

Structural Change Indicators:

Supply Chain Diversification Progress:

- South Korean production restart providing immediate non-Chinese capacity

- Montana development projects advancing through permitting processes

- Canadian redevelopment possibilities under active consideration

- International cooperation frameworks facilitating allied nation production

Industry Response Evolution:

- Defense contractor vertical integration strategies

- Strategic material inventory management improvements

- Supplier qualification process modifications

- Long-term contract structure adjustments

Policy Framework Development:

- Critical material classification systems implementation

- Strategic stockpile management modernisation

- International cooperation mechanisms enhancement

- Emergency production capability maintenance

The tungsten market's extreme concentration and price volatility demonstrate vulnerabilities that extend throughout critical materials markets. Success in diversifying tungsten supply will influence approaches to other strategic materials experiencing similar challenges.

Investment Strategy Considerations for Critical Materials Exposure

Investors approaching tungsten and related critical materials markets must navigate unprecedented volatility whilst positioning for long-term structural changes. Traditional commodity investment approaches require modification for markets characterised by geopolitical intervention and strategic government involvement. Furthermore, market research indicates that tungsten's performance has significantly outpaced traditional precious metals.

Investment Approach Strategies:

Direct Exposure Considerations:

- Pure-play tungsten producers offering concentrated exposure to price movements

- Diversified mining companies with tungsten assets providing reduced volatility

- Processing and manufacturing companies benefiting from higher tungsten values

- Technology companies developing alternative materials or processing improvements

Risk Management Techniques:

- Position sizing reflecting extreme volatility potential

- Diversification across multiple critical materials reducing single-commodity risk

- Time horizon consideration for long development cycles

- Geopolitical risk assessment integration into investment decisions

Market Timing Factors:

- Supply development timelines creating investment opportunity windows

- Government policy implementation affecting market dynamics

- Geopolitical tension cycles influencing demand patterns

- Technology development breakthrough potential

The current market environment offers opportunities for investors willing to accept substantial volatility in exchange for exposure to structural changes in global critical materials markets. However, these investments require sophisticated risk management and thorough understanding of the technical, political, and economic factors driving market evolution.

This analysis is for informational purposes only and does not constitute investment advice. Tungsten and critical materials markets involve substantial risks including extreme price volatility, geopolitical intervention, and technological disruption. Past performance does not indicate future results. Investors should conduct thorough research and consider their risk tolerance before making investment decisions in these markets.

Ready to Capitalise on Critical Materials Discoveries?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, instantly empowering subscribers to identify actionable opportunities in critical materials like tungsten ahead of the broader market. Understand why historic discoveries can generate substantial returns by exploring major mineral breakthroughs, then begin your 14-day free trial today to position yourself ahead of evolving market dynamics.