June 13, 2026

The Architecture of Dependence: Why Mineral Processing Power Is the New Geopolitical Currency

For decades, the global economy operated under an assumption that raw material access was the primary source of resource leverage. Whoever controlled the mines controlled the market. That assumption has been quietly dismantled over the past two decades as a far more consequential form of industrial power emerged: the ability to process, refine, and separate raw minerals into the high-purity inputs that advanced manufacturing actually requires. This distinction between extraction and processing sits at the heart of why the DOMINANCE Act critical minerals China dependence debate has become one of Washington's most urgent legislative conversations.

The minerals embedded in precision-guided weapons systems, electric vehicle battery cells, semiconductor fabrication lines, and wind turbine generators do not arrive at factories as raw ore. They arrive as chemically refined, application-specific materials that require sophisticated industrial infrastructure to produce. Building that infrastructure takes not months but years, sometimes decades. For the better part of a generation, one country invested more deliberately in that infrastructure than any other.

When big ASX news breaks, our subscribers know first

Understanding the 90% Processing Concentration Problem

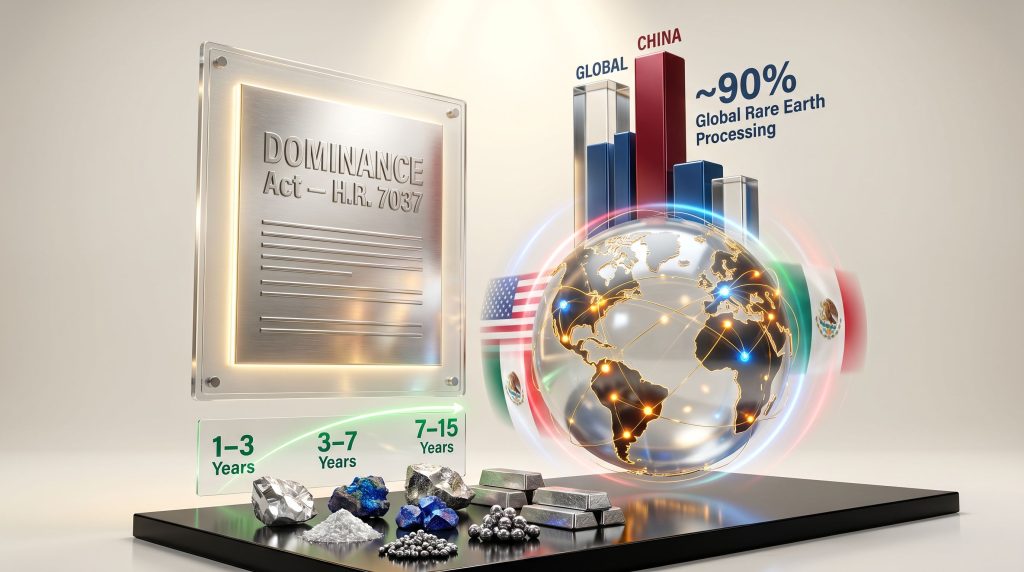

The figure that most clearly defines the strategic stakes of this debate is not difficult to locate. According to statements by Representative Ami Bera accompanying the House passage of the DOMINANCE Act, China currently controls approximately 90% of global rare earth processing capacity. This is not primarily a story about mining output — it is a story about industrial dominance at the transformation stage. Understanding rare earth supply chains is therefore essential to grasping the full scope of this vulnerability.

The rare earth supply chain operates in broadly sequential stages:

- Ore extraction from geological deposits through conventional mining methods

- Physical beneficiation to concentrate the ore and remove gangue material

- Hydrometallurgical processing to chemically separate individual rare earth elements

- Refining and alloying to produce application-specific materials with tight purity tolerances

- Component manufacturing using refined materials in magnets, phosphors, catalysts, and battery chemistries

China's dominance is concentrated in stages three through five. These are the stages that require specialist chemical engineering knowledge, proprietary separation techniques, and infrastructure that has been continuously refined over decades of operational experience. They are also the stages where export restrictions can be applied with surgical precision, affecting the downstream industrial base of competitor nations without directly touching ore extraction.

The core vulnerability facing the United States and its allies is not geological in nature. Combined, allied nations possess substantial mineral reserves across most critical mineral categories. The vulnerability is industrial: the absence of sufficient allied-controlled processing, refining, and separation infrastructure creates structural dependency regardless of where ore is physically extracted.

Furthermore, China's ability to deploy export restrictions on processed mineral intermediates represents an asymmetric coercive tool that operates largely outside the reach of conventional trade agreements. Historical episodes in which rare earth export constraints triggered supply shocks across electronics and defense manufacturing sectors have demonstrated that this leverage is not theoretical. It has already been exercised.

Why Rapid Diversification Remains Structurally Difficult

The reason rapid diversification is structurally difficult comes down to the economics of processing infrastructure. The rare earth processing challenges involved are substantial: a separation facility requires capital expenditure measured in hundreds of millions of dollars, specialised chemical engineering expertise that cannot be quickly recruited, environmental permitting processes that span multiple years in most allied jurisdictions, and an operational learning curve before consistent product quality can be achieved. These are not obstacles that respond to short-term policy gestures.

What the DOMINANCE Act Actually Establishes

The Developing Overseas Mineral Investments and New Allied Networks for Critical Energies (DOMINANCE) Act, designated H.R. 7037, passed the US House of Representatives on June 8, 2026. The legislation was introduced by Representatives Ami Bera (D-CA) and Young Kim (R-CA), a bipartisan authorship that itself signals how thoroughly critical mineral security has transcended conventional partisan divides.

The bill's core architecture rests on five interconnected policy pillars:

| Policy Pillar | Operational Focus |

|---|---|

| Allied Network Expansion | Formalise cooperation with trusted partner nations on mineral sourcing and processing |

| Investment Mobilisation | Direct capital toward strategic mineral projects in allied economies |

| Energy Diplomacy | Align US diplomatic resources with mineral and energy security objectives |

| Workforce Development | Build technical expertise in mining, processing, and refining across allied nations |

| Supply Chain Resilience | Reduce exposure to single-nation processing chokepoints |

What the legislation does not do is as analytically significant as what it does. The DOMINANCE Act does not mandate domestic-only sourcing, does not impose trade barriers on allied mineral exporters, and explicitly rejects the premise that the United States can achieve supply chain resilience through unilateral domestic expansion alone. The framing is networked multilateralism rather than resource nationalism — a meaningful philosophical distinction that shapes how allied partners are likely to receive the legislation.

How Does the DOMINANCE Act Compare to Parallel Legislation?

Comparing this bill to parallel legislative activity in the same policy space clarifies its scope:

| Feature | DOMINANCE Act | Critical Minerals Security Act |

|---|---|---|

| Primary Focus | Allied investment and diplomatic coordination | Domestic assessment and divestment from foreign-controlled operations |

| Mechanism | International cooperation frameworks | Interior Department supply assessments |

| Scope | Global allied network building | US firm exposure to foreign-controlled mineral operations |

| Legislative Status (June 2026) | Passed House, advancing to Senate | Parallel legislative track |

Sector Exposure: Why Industries Are Driving Legislative Urgency

The breadth of industrial sectors affected by critical mineral supply concentration helps explain why the DOMINANCE Act attracted support from organisations as ideologically diverse as the Climate Leadership Council and the National Association of Manufacturers. The minerals in question are not niche industrial inputs. They are foundational to virtually every high-value manufacturing category in the modern economy. Indeed, the scale of critical minerals demand across these sectors is only accelerating.

Defense and aerospace present perhaps the most strategically sensitive exposure. Rare earth elements are physically embedded in the permanent magnets used in precision-guided munitions, radar systems, electronic warfare equipment, and advanced propulsion technologies. There is no near-term substitute for neodymium-iron-boron magnets in many of these applications, and the magnet supply chain runs through Chinese processing capacity.

Semiconductor and advanced electronics manufacturing relies on a different subset of critical minerals, including high-purity germanium, gallium, and indium, as well as specialised rare earth compounds used in phosphors and polishing compounds. The intersection of semiconductors and critical minerals creates vulnerabilities that affect both consumer electronics and the leading-edge chip fabrication lines underpinning AI hardware development.

Electric vehicle and battery production depends on lithium, cobalt, nickel, and manganese — minerals for which processing and refining infrastructure is substantially concentrated in China or in Chinese-controlled operations in third countries. Even where ore originates in Australia, Chile, or the Democratic Republic of Congo, the transformation into battery-grade cathode material frequently passes through Chinese industrial facilities.

Clean energy infrastructure, including utility-scale wind, solar, and grid storage, requires rare earth magnets, specialty glass, and battery chemistry inputs that face similar processing concentration issues. Consequently, energy transition mining ambitions in allied economies are partially hostage to Chinese processing decisions, which directly affects decarbonisation timelines.

The Time Lag Problem

A less widely understood dimension of this industrial exposure involves the time lag between policy intervention and supply chain change. Even if the DOMINANCE Act is enacted and investment begins flowing immediately, the processing facilities it helps finance will not reach commercial-scale output for several years. This means the near-term supply chain vulnerability persists regardless of legislative action, and policy frameworks must account for that gap through strategic stockpiling and demand-side flexibility measures.

The North American Dimension: Mexico as a Strategic Minerals Partner

The DOMINANCE Act's allied network concept extends meaningfully into North America, where Mexico has positioned itself as an increasingly significant participant in regional critical mineral supply chains. The United States and Mexico established a bilateral Critical Minerals Action Plan earlier in 2026, designed to coordinate trade policy, attract investment, and strengthen supply chain resilience across the region.

Mexico is actively pursuing access to 13 critical minerals through international negotiations while leveraging its domestic production assets to strengthen its regional supply chain role. The country's strategic positioning spans multiple end-use sectors:

- Automotive manufacturing, where Mexico's deep integration with North American vehicle production creates natural demand for domestically sourced battery and electronics minerals

- Electronics and advanced manufacturing, where nearshoring trends are driving investment in Mexican industrial capacity

- Energy transition infrastructure, where renewable energy project pipelines create growing domestic demand for critical mineral inputs

- USMCA-linked supply chain commitments, where trade architecture is being used as a vehicle to embed mineral security provisions into binding North American trade governance

The USMCA dimension is particularly notable from a policy architecture perspective. Rather than treating mineral supply chain coordination as a standalone industrial policy challenge, the approach of embedding resource security commitments into established trade agreement review processes creates a more durable governance structure with clearer enforcement mechanisms.

The Coalition Behind the Legislation and What It Signals

The organisations that formally supported the DOMINANCE Act span a political and sectoral range that would be difficult to assemble around almost any other legislative proposal:

- National Association of Manufacturers

- Information Technology Industry Council

- Climate Leadership Council

- Bipartisan Policy Center Action

- Progressive Policy Institute

- Third Way

- SAFE Center for Critical Minerals Strategy

- US-ASEAN Business Council

The inclusion of climate-aligned organisations alongside defense-focused think tanks reflects a recognition that clean energy transition goals and national security imperatives are not in tension on this issue. Both require the same outcome: reliable, non-coercible access to critical mineral processing capacity outside Chinese control.

The presence of the US-ASEAN Business Council in the coalition is also analytically significant. It signals that the allied network envisioned by the legislation is not confined to traditional Five Eyes partners or NATO allies. Southeast Asian economies — several of which possess significant mineral deposits and developing processing capabilities — are explicitly part of the strategic architecture being constructed.

The next major ASX story will hit our subscribers first

Implementation Challenges and the Substitution Imperative

Senate deliberation represents the most immediate legislative risk. The scope of allied investment provisions and the mechanisms for diplomatic coordination may face amendment pressure, and competing Senate priorities create scheduling uncertainty. Beyond the legislative pathway, the structural challenges of actually building allied processing capacity are substantial:

- Capital intensity: Refining and separation facilities require long-term investment commitments with extended payback periods that are difficult to finance purely on commercial terms

- Permitting timelines: Environmental and regulatory approval processes in most allied nations can add years to project development schedules

- Workforce scarcity: Deep technical expertise in hydrometallurgical processing is concentrated in a small number of countries, making rapid workforce scaling a genuine constraint

- Geopolitical coordination complexity: Aligning mineral policy across multiple sovereign nations with different regulatory environments, investment climates, and domestic political pressures introduces friction that slows execution

Policy analysts across multiple research institutions broadly agree that supply-side diversification must be complemented by demand-side strategies. Material substitution research aimed at reducing or eliminating dependence on specific critical minerals in key applications, and closed-loop recycling infrastructure that recovers critical minerals from end-of-life products, represent structurally important hedges that reduce the volume of primary supply required from any single source.

Recycling infrastructure for battery-grade materials and rare earth elements currently remains underdeveloped in most allied economies, representing both a gap and an investment opportunity. The recycling of neodymium from permanent magnets, for example, is technically feasible but has not been deployed at commercial scale outside a small number of specialised facilities. Scaling this capability reduces the net demand that allied processing facilities need to satisfy and shortens the timeline to meaningful supply chain diversification.

The Long Arc: From Reactive Management to Structural Architecture

The DOMINANCE Act critical minerals China dependence framework is best understood not in isolation but as one component within a multi-decade effort to restructure global critical mineral supply chains. The European Union's Critical Raw Materials Act, Japan's strategic mineral stockpiling programmes, South Korea's mineral security frameworks, and Australia's critical minerals strategy all reflect the same underlying analytical conclusion: that the current concentration of processing capacity represents an unacceptable strategic vulnerability requiring coordinated intervention across multiple policy instruments simultaneously.

The convergence of these allied frameworks creates the foundation for what analysts describe as a coordinated Western minerals bloc — a distributed network of processing, refining, and manufacturing capacity that could meaningfully reduce allied dependence on Chinese processing over a 10 to 15 year horizon. However, the timeline matters because it establishes appropriate expectations. This is not a problem that legislation alone can solve, and it is not a problem that resolves quickly even with sustained investment.

What Does a Realistic Structural Outlook Look Like?

A realistic structural outlook across three planning horizons looks as follows:

| Timeframe | Expected Developments |

|---|---|

| Near-term (1–3 years) | Legislative enactment, bilateral agreement formalisation, early-stage investment mobilisation |

| Medium-term (3–7 years) | Processing facility development in allied nations, workforce scaling, recycling infrastructure buildout |

| Long-term (7–15 years) | Meaningful reduction in allied Chinese processing dependence, supported by materials innovation and closed-loop supply chains |

What makes this policy moment distinctive is the convergence of legislative, diplomatic, and commercial actors around a shared diagnosis. For the first time, manufacturers, technology companies, clean energy advocates, and national security institutions are operating from the same analytical framework. Analysts have noted that China's dominance of critical mineral markets did not emerge by accident but through deliberate, decades-long industrial strategy — a reality that underscores why the DOMINANCE Act critical minerals China dependence agenda requires an equally sustained and coordinated allied response. That convergence is itself a structural shift, and it is the precondition for the kind of multi-decade investment programme the scale of the challenge actually requires.

Disclaimer: This article is intended for informational purposes only and does not constitute financial, investment, or policy advice. Forward-looking statements regarding legislative outcomes, supply chain timelines, and market developments involve inherent uncertainty and should not be relied upon as predictions of future events.

Want to Identify ASX Mineral Discoveries Before the Broader Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across critical minerals and rare earths, translating complex geological and market data into clear, actionable investment insights — begin your 14-day free trial today, or explore Discovery Alert's dedicated discoveries page to understand how historic mineral discoveries have generated substantial returns for early-positioned investors.