May 18, 2026

When Clean Energy Inherits the Sins of Fossil Fuels

Every major energy transition in history has reshuffled geopolitical power and created new categories of strategic vulnerability. The shift from wood to coal enabled industrial empires. The rise of petroleum birthed the modern nation-state system and its attendant conflicts. Today, the transition toward renewable energy and electrified transport is establishing a third category of resource dependency — one built not around barrels of crude but around tonnes of lithium, cobalt, copper, nickel, and rare earth elements. The uncomfortable reality is that critical mineral extraction in clean energy systems may be replicating the very patterns of exploitation, concentration, and environmental degradation that the energy transition was supposed to move beyond.

Understanding this paradox requires looking not at the end product — a gleaming solar panel or a silent electric vehicle — but at the full supply chain behind it, extending deep into mines in the Democratic Republic of Congo, the highlands of Chile, and the processing facilities of eastern China.

When big ASX news breaks, our subscribers know first

The Mineral Portfolio Behind Decarbonisation

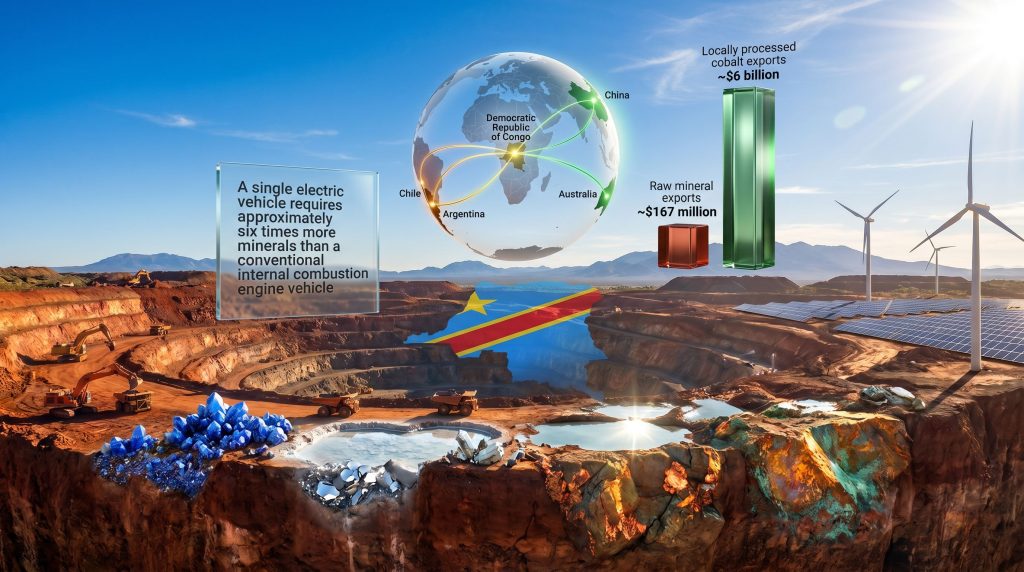

Clean energy infrastructure is fundamentally more mineral-intensive than the fossil fuel systems it replaces. A conventional internal combustion engine vehicle uses a relatively modest mineral package. According to the International Energy Agency, a single electric vehicle requires approximately six times more minerals than its petrol-powered equivalent, spanning lithium, cobalt, nickel, manganese, copper, and graphite across its battery system and drivetrain alone.

The full portfolio of materials underpinning the energy transition is broader still:

| Mineral | Primary Clean Energy Application | Demand Trajectory |

|---|---|---|

| Lithium | EV batteries, grid storage | Could more than double by 2030 |

| Cobalt | Battery cathodes, microchips | Potential quadrupling by 2050 |

| Copper | Grid infrastructure, EV motors | Essential for all electrification pathways |

| Nickel | High-density battery chemistries | Supply shortfall risk emerging in 2030s |

| Rare Earth Elements | Wind turbine motors, EV drivetrains | Processing heavily concentrated in one country |

| Graphite | Battery anodes | Over 70% of supply controlled by a single nation |

| Silicon | Solar photovoltaic cells | Demand scaling with solar deployment |

| Manganese | Battery stabiliser | Growing role in lower-cost chemistries |

What makes this dependency structurally different from oil is that these materials are not interchangeable. Lithium's low atomic mass and high electrochemical potential make it uniquely suited to battery chemistry. Neodymium and dysprosium, both rare earth elements, produce the powerful permanent magnetic fields required by direct-drive wind turbines and high-efficiency EV motors. Furthermore, copper's electrical conductivity — second only to silver among common metals — makes it irreplaceable in transmission systems that renewable energy grids require at far greater scale than conventional power plants.

This creates what materials scientists sometimes describe as mineral lock-in: demand for specific elements that engineering cannot easily circumvent, regardless of price signals or policy intent. Critical minerals and energy security are consequently becoming inseparable considerations in national strategic planning.

What Makes a Mineral Officially "Critical"?

The term critical carries specific technical and policy meaning. A mineral is generally classified as critical when two conditions are simultaneously satisfied: it is economically essential to modern technology or national development, and its supply is vulnerable to disruption.

Criticality frameworks have grown increasingly sophisticated in recent years. The United States Geological Survey (USGS) identified 50 critical minerals in its 2022 assessment, up from 35 in 2018, reflecting how rapidly technological change is expanding the list. The European Union's 2023 Critical Raw Materials Act designated 34 materials, with rare earth elements, lithium, cobalt, and graphite classified as strategically critical due to projected supply deficits that could exceed 80% of demand by 2030 under current trajectories.

Crucially, the definition is not static. Minerals can enter or exit critical status as:

- New reserves are discovered or made economically viable through processing advances

- Battery chemistries evolve and alter which elements are required

- Recycling infrastructure scales and reduces dependence on primary extraction

- Geopolitical events shift supply chain risk profiles

What amplifies the strategic concern further is the convergence of sectors competing for the same minerals simultaneously. Clean energy, defence systems, consumer electronics, and healthcare technology each draw from the same finite mineral pool. This compound demand pressure means that a supply disruption affecting one sector cascades rapidly across others — a vulnerability with no real equivalent in the oil era.

The Geography of Vulnerability: Why Concentration Is the Core Problem

Mining activity for most critical minerals is heavily concentrated in a small number of countries. This is not merely a commercial inconvenience. It is a structural fragility embedded in the entire clean energy transition.

Consider the current distribution:

- The Democratic Republic of Congo accounts for approximately 70% of global cobalt production

- The Lithium Triangle (Argentina, Bolivia, Chile) holds around 60% of global lithium reserves

- Indonesia supplies over 50% of global nickel production

- China controls an estimated 60–70% of global rare earth element processing capacity, despite holding only around 35% of identified reserves

- Graphite supply exceeds 70% concentration in a single producing nation

How Does China's Dominance Affect Supply Chains?

The China dimension deserves particular attention. Beijing's dominance extends beyond raw mining into the processing and refining infrastructure that converts ore into battery-grade materials. Nations with significant domestic mining capacity, including Australia and Canada, still depend on Chinese industrial systems to transform their raw output into commercially usable product. Moreover, China's rare earth restrictions have demonstrated precisely how this processing bottleneck can be wielded as a strategic instrument, representing the deepest and most difficult-to-resolve vulnerability in the current supply chain architecture.

The 2022 episode involving nickel is instructive. Following Russia's invasion of Ukraine, nickel prices briefly surged more than 250% on the London Metal Exchange, forcing multiple EV manufacturers to accelerate redesigns of battery chemistries that reduced nickel content. A single geopolitical event cascaded into automotive R&D schedules within weeks.

The Human and Environmental Cost in Producer Nations

The clean energy transition's supply chain carries a cost that is largely invisible to consumers in wealthy importing nations but acutely felt in mineral-producing regions. A 2025 report by the United Nations University Institute for Water, Environment and Health (UNU-INWEH) documented the scale of this burden across major mining regions in Africa and Latin America.

The findings were significant:

- Severe water table depletion in arid mining regions, threatening agricultural communities that depend on groundwater

- Contamination of rivers and waterways used for drinking, fishing, and irrigation in communities adjacent to extraction zones

- Toxic heavy metal exposure among workers and residents in mining settlements

- Documented reproductive health impacts among women engaged in or living near extraction sites

In the DRC's Lualaba province, one of the world's most important cobalt-producing regions, extraction activities have generated widespread contamination of waterways that communities rely on for basic survival. The scale of this harm exists alongside a striking statistic: despite the cobalt sector's growing contribution to national revenue, approximately 64% of people in the DRC still lacked basic access to water as of 2024, according to data cited in the UNU-INWEH analysis.

Rare earth element production presents a parallel environmental challenge that receives even less public attention. Global rare earth production in 2024 generated approximately 700 million tonnes of waste material, including radioactive tailings, acid mine drainage, and chemical processing byproducts. The long-term liability associated with this waste frequently falls on host communities rather than the companies that generated it.

Kaveh Madani, Director of the UNU-INWEH, has argued publicly that critical minerals risk becoming the defining resource exploitation issue of the current century, warning that what is promoted as a sustainability solution may be actively harming communities in other parts of the world. His challenge, as reported in The Guardian in April 2026, was whether an energy transition built on these conditions can genuinely be described as green or clean.

The 15-Year Development Gap and Why It Matters

One of the most underappreciated structural constraints in the critical minerals sector is the sheer time required to bring new supply online. On average, developing a new mining project from initial discovery through to first commercial production takes 15.5 years. This figure, widely cited across industry and policy analysis, can be broken down across four phases:

- Exploration (2–5 years): Geological surveys, resource estimation, drilling programs, and preliminary feasibility assessment

- Permitting and environmental assessment (3–7 years): Community consultation, environmental impact studies, regulatory approvals across multiple jurisdictions

- Construction and commissioning (2–5 years): Mine development, processing infrastructure, logistics connectivity

- Production ramp-up (1–3 years): Scaling to nameplate capacity and achieving consistent output quality

This extended timeline creates a structural lag that no policy intervention can quickly compress. Demand signals arriving today will not translate into new mine supply until the late 2030s at the earliest for projects that enter exploration now. Meanwhile, existing copper, nickel, and cobalt reserves are already projected to be insufficient to meet mid-century clean energy scenarios, pushing exploration into increasingly remote, environmentally sensitive, and politically complex territories.

The permitting phase is where projects most frequently stall. Environmental impact assessments for large-scale mining projects in ecologically sensitive regions can extend well beyond initial estimates, particularly where Indigenous land rights require formal free, prior, and informed consent processes.

The next major ASX story will hit our subscribers first

Deep-Sea Mining: Expanding the Frontier or Exporting the Problem?

The inadequacy of known terrestrial reserves has focused attention on a new extraction frontier: polymetallic nodules and seafloor massive sulphide deposits on the ocean floor. These formations contain significant concentrations of cobalt, nickel, manganese, and copper, theoretically sufficient to meaningfully reduce supply concentration risks if extracted at scale.

The United States, under the Trump administration, has engaged in preliminary discussions around unilateral deep-sea mining authorisation, driven primarily by supply security concerns and a broader strategy of reducing dependence on Chinese-controlled supply chains.

The international community has responded with considerable alarm, and for substantive reasons. The deep-sea mining controversy has intensified as analysts warn that proceeding without governance frameworks risks setting irreversible precedents:

- No internationally agreed regulatory framework currently governs seabed mineral extraction in international waters

- Unilateral national action risks undermining the International Seabed Authority's multilateral governance process, which took decades to establish

- Marine ecologists warn that sediment plumes, noise pollution, and habitat destruction from seabed mining could cause irreversible damage to deep-sea ecosystems, many of which remain scientifically undocumented

- Indigenous and coastal communities with cultural and subsistence connections to marine environments have raised formal objections through international forums

The debate encapsulates a broader tension running through the entire critical minerals challenge: the urgency of supply security on one side, and the imperative to avoid ecological irreversibility on the other.

The UN Framework and the Value-Addition Opportunity

In June 2025, the United Nations published comprehensive guidance on critical energy transition minerals, establishing three foundational principles that must govern extraction activities:

- Human rights centrality: All mineral development must uphold the rights of affected communities, workers, and Indigenous peoples without exception

- Environmental and planetary integrity: Extraction must operate within defined ecological boundaries and avoid actions that cause irreversible environmental harm

- Justice and equity throughout the value chain: Benefits must be distributed equitably, and the costs of extraction must not disproportionately burden vulnerable populations

Alongside this normative framework, the UN Trade and Development Agency (UNCTAD) has reframed the critical minerals challenge as a potential development opportunity for resource-rich nations, provided the right policy architecture is in place. The key mechanism is value addition: the transition from exporting raw ore to conducting local processing and manufacturing.

The figures that illustrate this opportunity are striking:

| Processing Stage | DRC Cobalt Export Value (2022) |

|---|---|

| Raw mineral exports | ~$167 million |

| Locally processed cobalt exports | ~$6 billion |

| Value multiplication factor | Approximately 36x increase |

Achieving this kind of value capture requires governments to negotiate meaningful equity stakes, technology transfer agreements, and local employment mandates with private mining investors. The Minerals Security Partnership represents one such attempt to align producing and consuming nations around more equitable frameworks, rather than simply granting extraction licences in exchange for royalty streams.

At the inaugural global conference on transitioning away from fossil fuels, held in April 2026, Indigenous delegates formally declared that the energy transition must not function as a new justification for appropriating Indigenous territories. The message was direct: renewable energy rollout must be conditional on the protection of ecologically intact landscapes and the genuine, documented consent of affected peoples.

The Recycling Gap and the Circular Economy Promise

Battery recycling and circular economy strategies feature prominently in government supply chain resilience frameworks across the United States, European Union, and Australia. The logic is straightforward: if end-of-life batteries can be efficiently processed to recover lithium, cobalt, and nickel, the dependence on primary mining diminishes over time.

The challenge is timing. Lithium recycling rates currently sit below 5% globally, and the volume of end-of-life batteries entering waste streams today is insufficient to meaningfully offset primary mining demand. The battery recycling process is, however, advancing rapidly, and the critical inflection point arrives when the current generation of electric vehicles reaches end-of-life in the early-to-mid 2030s, at which point feedstock volumes will begin to scale.

Policy mechanisms being deployed to accelerate this transition include:

- Extended producer responsibility (EPR) legislation, requiring manufacturers to fund and manage end-of-life mineral recovery programs

- Battery passport regulations (EU), mandating full transparency on mineral provenance, carbon footprint, and recycled content

- Critical mineral stockpiling programs in the US and allied nations to buffer against supply disruptions during the transition period

- R&D investment in hydrometallurgical and direct recycling technologies to improve recovery rates for lithium, cobalt, and nickel beyond current thresholds

Even under optimistic projections, recycled supply will cover only a fraction of primary mining demand through 2040. Consequently, the central policy challenge of this decade is not eliminating primary extraction, but ensuring it is conducted under governance standards that are fundamentally different from those of the 20th century extractive economy.

Critical Minerals Diplomacy: The New Architecture of Supply Security

Governments are constructing new diplomatic frameworks specifically designed to secure critical mineral supply chains outside of Chinese-dominated processing networks. The most significant emerging structures include:

- The US Minerals Security Partnership (MSP): A multilateral initiative linking the United States with allied nations to diversify supply chains and reduce single-country dependencies across the mineral value chain

- The EU Critical Raw Materials Act: Establishing binding domestic processing targets and strategic stockpiling requirements, with the explicit goal of processing at least 40% of annual consumption within EU borders by 2030

- Australia's Critical Minerals Strategy: Positioning Australia as a preferred supplier to allied nations, leveraging its significant reserves of lithium, cobalt, nickel, and rare earth elements alongside relatively stable governance and environmental frameworks

The fundamental bottleneck these frameworks must address is not mining capacity — which is geographically distributed across multiple continents — but processing and refining infrastructure, which remains dangerously concentrated. Furthermore, as ARENA notes, building hydrometallurgical processing facilities, training workforces, and establishing quality certification systems for battery-grade materials is a decade-scale undertaking, reinforcing the same timeline constraint that affects new mine development.

The Central Contradiction the Sector Must Resolve

The energy transition faces a legitimacy problem that cannot be resolved through technology alone. If the environmental and social costs of critical mineral extraction in clean energy systems are simply displaced from wealthy consuming nations onto producing ones, the transition cannot credibly claim to be sustainable in any meaningful sense.

The minerals powering tomorrow's wind farms and electric vehicle fleets must be extracted under governance conditions that bear no resemblance to the extractive industries of the 20th century. That means binding human rights standards embedded in supply agreements, genuine benefit-sharing that allows producer nations to capture value through processing rather than raw exports, functional multilateral governance for emerging frontiers like deep-sea mining, and recycling infrastructure scaled to absorb end-of-life battery volumes as they arrive in the 2030s.

Whether the critical minerals sector achieves this distinction — or quietly repeats the patterns of resource colonialism that defined the oil era — will determine the moral and practical legitimacy of the green transition for generations. The technical capacity to build a clean energy economy exists. The governance architecture to do so justly is still being constructed, and the window for getting those foundations right is narrower than most policymakers appear to appreciate.

This article is intended for informational purposes only and does not constitute financial, legal, or investment advice. Demand projections, supply forecasts, and policy outcomes discussed in this article involve significant uncertainty and should not be relied upon as predictions of future performance. Readers should conduct independent research and consult qualified advisers before making decisions based on the information presented here.

Want To Stay Ahead of the Critical Mineral Discoveries Shaping the Energy Transition?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — including lithium, cobalt, copper, and rare earth elements — turning complex geological data into actionable investment insights the moment they hit the market. Explore historic discoveries and the substantial returns they have generated, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.