July 17, 2026

The Hidden Fracture in the Global Energy Transition

There is a persistent assumption in energy transition discourse that demand growth automatically attracts the capital needed to meet it. In practice, the relationship between demand signals and investment behaviour is far more complicated. Markets respond not just to what is needed, but to what is financially viable, politically stable, and technologically achievable within bankable timeframes. When those conditions are uncertain, capital retreats, regardless of how urgent the underlying need may be.

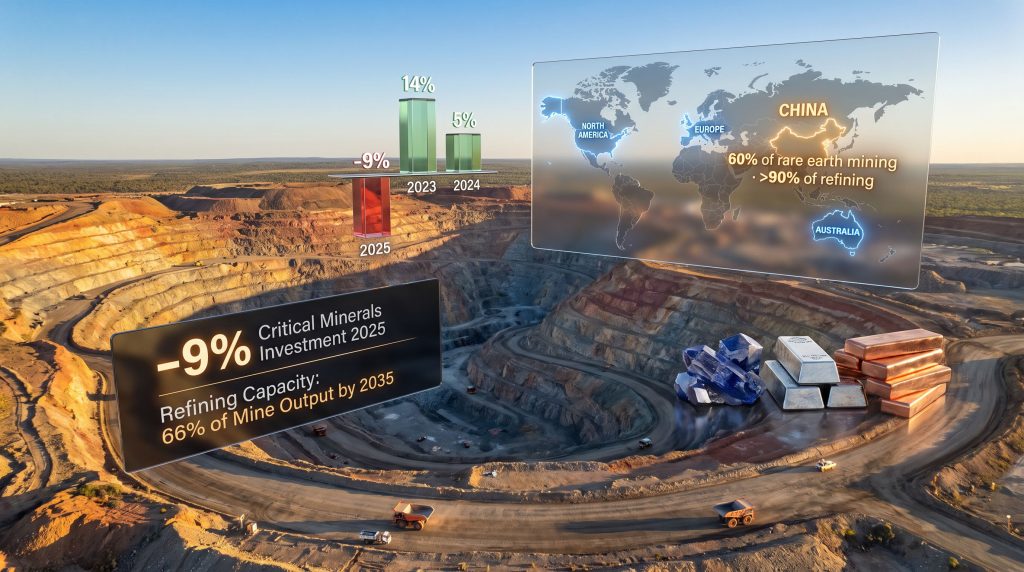

That is precisely the dynamic playing out across global critical minerals demand markets right now. The IEA's Global Critical Minerals Outlook 2026 has confirmed that IEA critical minerals investment falls 9% in 2025, a striking contraction that follows a visible deceleration from 14% growth in 2023 to just 5% in 2024. Simultaneously, exploration spending dropped by more than 10%, hollowing out the earliest and most essential stage of the project development pipeline.

Understanding why this is happening, and what it means for industries ranging from electric vehicles to defence electronics, requires looking beyond the headline figures.

When big ASX news breaks, our subscribers know first

The Investment Deceleration: Numbers Behind the Narrative

The data points in the IEA's 2026 outlook tell a coherent story when read together rather than in isolation.

| Metric | Figure |

|---|---|

| Critical minerals investment change in 2025 | -9% |

| Exploration spending decline | >-10% |

| Public finance commitments (2023-2025) | US$65 billion |

| Increase in public finance vs. prior period | Fourfold |

| IEA-identified critical minerals | 37 |

| Critical mineral share of battery cell cost | ~25% |

| Critical mineral share of average EV price | ~3% |

| Rare earth refining vs. mine output by 2035 | 66% |

| Magnet production vs. mine output by 2035 | ~33% |

The paradox embedded in these numbers is significant. Public finance for critical mineral projects surged fourfold between 2023 and 2025, reaching US$65 billion. Yet private investment contracted sharply in 2025. This divergence reveals a confidence gap that fiscal commitments alone have not resolved. Governments have signalled intent; private capital has not followed.

Exploration activity is the canary in this particular mine. It declined in 2024 before investment contracted in 2025, a sequencing that should not be overlooked. Reduced exploration activity typically precedes project development pullbacks by one to two years, as the pipeline of economically viable assets thins before financing decisions reflect it.

Why Private Capital Has Pulled Back

Several compounding factors explain the retreat of private investment:

- Price volatility in critical mineral markets makes long-term project financing difficult, as lenders require stable price assumptions that concentrated supply structures cannot reliably deliver

- Permitting timelines and regulatory complexity in many jurisdictions extend development risk windows beyond the appetite of most institutional capital

- The technology and workforce barriers specific to processing, particularly for rare earths, elevate technical risk beyond what conventional mining finance frameworks accommodate

- Geopolitical uncertainty around supply chain security creates sovereign risk that is difficult to hedge in project-level finance structures

Concentration Risk: Why Refining, Not Mining, Is the Real Chokepoint

The conventional framing of critical minerals risk focuses on where deposits are located. The more consequential vulnerability, however, sits one step downstream: processing and refining capacity.

China currently controls approximately 60% of global rare earth mining output and more than 90% of refining capacity. For non-rare earth minerals, the single largest refining country held an average 72% market share in 2025. Indonesia and China together accounted for more than 75% of total growth in refined supply during the reporting period, driven primarily by nickel refining in Indonesia and multi-mineral processing in China.

This is not merely a market share statistic. It represents a structural dependency that affects every downstream manufacturer relying on these materials. Furthermore, the IEA's Fatih Birol has noted that vast economic value depends on relatively small volumes of critical minerals whose supply chains remain highly concentrated and therefore vulnerable, while also identifying targeted policies and investment support in rare earth supply chains as encouraging early signals of progress.

The April 2025 Export Control Event: A Case Study in Cascade Risk

China's imposition of rare earth export controls in April 2025 functioned as an unplanned stress test of global supply chain resilience. The results were sobering. Several automotive manufacturers were forced to suspend or curtail production lines not because of any mine closure or geological event, but because a policy decision in one country's regulatory apparatus could not be absorbed by a supply chain with no redundancy in the processing stage.

This episode illustrates a critical insight that is often underappreciated: geographic diversification of mining does not provide supply chain security if refining capacity remains concentrated. A deposit in Canada or Australia that must be shipped to China for processing before returning as a usable input material is not a diversified supply chain. It is simply a longer version of the same dependency.

The 37 Critical Minerals: Risk Is Not Uniform

The IEA has formally classified 37 minerals as critical across aerospace, energy infrastructure, and consumer electronics applications. Each carries a materially different risk profile:

- Rare earths, cobalt, and graphite present the highest barriers to supply diversification, combining technical processing complexity with extreme geographic concentration and long capital payback periods

- Copper and lithium have seen more meaningful progress, with projects narrowing the gap between projected demand and anticipated supply more effectively than other categories

- Gallium and germanium, critical for semiconductor production, operate in even more narrowly concentrated supply chains than rare earths and have received comparatively less diversification investment

- Nickel presents a more nuanced picture, with Indonesia's rapid refining expansion creating new supply but simultaneously reinforcing a two-country concentration dynamic alongside China

The Processing Gap: A 2035 Bottleneck Already Visible Today

The IEA's projection that refining capacity will meet only 66% of expected rare earth mine output by 2035 is among the most technically significant findings in the Global Critical Minerals Outlook 2026. For magnet production capacity specifically, the figure drops to approximately one-third of mine output.

This is not a future problem. The investment decisions that will determine 2035 processing capacity need to be made now, given that refinery construction and commissioning timelines often span five to ten years. The window for course correction is narrower than the 2035 date implies.

The gap between expanding mine output and stagnant processing infrastructure is one of the most systematically underappreciated structural risks in advanced manufacturing supply chains.

Several factors explain why processing investment has lagged behind mining investment historically:

- Processing facilities require higher technical expertise and longer construction timelines than equivalent-scale mining operations

- The economics of refining in non-established regions are less attractive without co-located infrastructure, creating a market failure that organic capital flows alone cannot correct

- Rare earth processing equipment and the engineering knowledge to operate it remain largely concentrated in China, creating a technology access barrier that compounds the geographic concentration problem

- Revenue visibility for processing facilities depends on long-term offtake agreements, which are harder to negotiate without established customer relationships in regions that have historically sourced from China

Unlocking Supply From Existing Assets: The Productivity Dividend

One of the more strategically important arguments in the IEA's analysis is that new greenfield development, while necessary, is not the only pathway to near-term supply improvement. Joachim Braun, Global Division President of ABB's Process Industries division, has articulated this point clearly: expanding supply is not only about building new capacity, but about unlocking more value from operations already in existence. Existing mines, in this framing, represent one of the fastest available opportunities to strengthen supply chains through improvements in productivity, mineral recovery, energy efficiency, and operational resilience.

This perspective carries practical weight for several reasons:

- Tailings reprocessing: Legacy mining operations often left behind tailings containing economically viable concentrations of minerals that earlier extraction methods could not recover. Modern hydrometallurgical and bioleaching techniques can recover these materials at costs that are increasingly competitive

- Recovery rate optimisation: Incremental improvements in ore processing recovery rates across large-scale operations can yield supply volumes equivalent to smaller new mine developments, without the decade-plus development timeline

- Asset life extension: Operational efficiency improvements and predictive maintenance reduce downtime and extend productive life at existing facilities

The electrification and automation of mining operations is central to this productivity thesis. ABB's Mining's Moment research found that 77% of mining industry leaders believe electrification, automation, and digitalisation must be implemented together, rather than individually, to achieve sustainable operational transformation. Practical examples are already visible, including the deployment of battery-electric haulage across the Pilbara region of Western Australia by BHP and Rio Tinto in collaboration with Caterpillar.

The Consumer Cost Argument for Diversification Investment

A frequently cited objection to supply chain diversification is cost. Building processing capacity outside China, developing new deposits in higher-cost jurisdictions, and creating supply redundancy all carry price premiums relative to the incumbent concentrated supply structure.

The IEA's data provides important context for evaluating this objection. Critical minerals account for approximately 25% of battery cell manufacturing costs but represent only around 3% of the average electric vehicle's final retail price. This asymmetry means that even a meaningful cost premium on diversified supply, absorbed at the battery cell level, would translate to a negligible increase in consumer-facing vehicle prices.

Fatih Birol has framed this cost premium as a mineral security premium, comparable to an insurance payment against geopolitical supply disruption rather than an economic inefficiency. That reframing has practical policy implications, as it argues for distributing diversification costs across governments, industries, and consumers through structured policy mechanisms rather than expecting market competition alone to drive the investment. Consequently, European supply diversification efforts have emerged as one of the more structured regional responses to this challenge.

Three Scenarios for Critical Minerals Supply Through 2035

| Scenario | Key Conditions | Likely Supply Outcome |

|---|---|---|

| Recovery | Private investment rebounds; processing capacity built outside China | Rare earth refining gap narrows to approximately 20% of mine output |

| Stagnation | Flat investment; export controls persist; workforce gaps unaddressed | 66% refining coverage of mine output; manufacturing bottlenecks intensify |

| Acceleration | Policy frameworks unlock private capital; automation drives productivity gains | Processing gap closes; diversification cost premiums absorbed by efficiency improvements |

The stagnation scenario is not a pessimistic projection. It is, under current investment trajectories, the central case.

The next major ASX story will hit our subscribers first

Workforce and Technology Constraints: The Invisible Bottleneck

Beyond capital and geography, critical minerals supply chains face a third category of constraint that receives less analytical attention: human capital and equipment access.

Rare earth processing expertise remains heavily concentrated in regions with established production histories, primarily China. Developing equivalent expertise in new jurisdictions is not simply a matter of funding training programmes. The tacit knowledge embedded in experienced processing workforces takes years to accumulate and cannot be transferred through formal education alone.

Equipment availability presents a parallel challenge. Much of the specialised processing equipment used in rare earth refining is manufactured in China. Jurisdictions seeking to build independent processing capacity therefore face a dual dependency: on Chinese processing capacity in the short term, and on Chinese-manufactured processing technology in the medium term, unless significant domestic equipment manufacturing capability is developed.

The IEA's policy recommendations address this by suggesting that improvement costs be distributed across stakeholder groups rather than concentrated on any single actor. A critical minerals strategic reserve and co-located stockpiles of low-volume, high-criticality materials are also identified as near-term risk mitigation mechanisms that can reduce vulnerability to supply interruptions without requiring the full development of alternative processing infrastructure.

The Strategic Framing Shift: From Energy Transition to Economic Security

The Global Critical Minerals Outlook 2026 reflects a broader evolution in how governments, industries, and financial institutions are thinking about IEA critical minerals investment falls 9% and what that contraction signals about market confidence. The earlier framing, centred almost exclusively on enabling the energy transition, has given way to a more expansive understanding that encompasses industrial competitiveness, economic security, and supply chain sovereignty.

Joachim Braun has described this shift in terms of where competitive advantage will ultimately reside: not simply in which countries or companies secure access to raw materials, but in which ones develop the intelligence, productivity, and resilience to produce those materials sustainably and efficiently. The countries and companies making those investments today will be structurally best positioned to meet the demand profiles of tomorrow.

This is a meaningful reorientation. It implies that the strategic value of critical minerals and energy security investment lies not only in the physical resources themselves but in the institutional knowledge, processing capability, and operational infrastructure built around them. Nations that invest only in securing access, without developing the downstream processing and manufacturing ecosystem, may find that access alone confers limited economic advantage.

For investors, policymakers, and industrial planners, the IEA's 2026 analysis presents a clear inflection point. The decisions made over the next three to five years will determine whether supply chains for the materials underpinning the energy transition, defence electronics, and advanced manufacturing can keep pace with accelerating demand, or whether concentrated vulnerabilities crystallise into sustained structural shortfalls.

This article draws on data and analysis from the IEA's Global Critical Minerals Outlook 2026 and publicly available statements from industry leaders. Forward-looking projections involve inherent uncertainty and should not be construed as financial advice or definitive supply forecasts.

Want to Track the Next Major Critical Minerals Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across critical commodities and turning complex data into actionable investment insights — explore historic discoveries and their returns to understand the scale of opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the broader market.