May 21, 2026

MCA Calls for Critical Minerals Reform to Unlock Australia's Economic Potential

The Minerals Council of Australia's recent advocacy for comprehensive regulatory reform reflects growing industry recognition that Australia's critical minerals strategy requires urgent modernisation to capture expanding global opportunities. As the MCA calls for critical minerals reform, industry leaders emphasise that regulatory bottlenecks are constraining Australia's ability to capitalise on unprecedented demand growth driven by the clean energy transition. Furthermore, these challenges extend beyond simple approval delays to encompass workforce shortages, processing capability gaps, and international competitiveness concerns that collectively threaten Australia's position as a preferred investment destination.

When big ASX news breaks, our subscribers know first

Understanding Australia's Critical Minerals Landscape

Understanding Australia's critical minerals landscape requires examining both the geological advantages and strategic vulnerabilities that define this sector. These materials represent far more than simple commodities; they form the backbone of technological sovereignty and economic resilience in an increasingly complex global environment.

Defining Critical Minerals in the Australian Context

The Australian Government classifies critical minerals as elements essential for clean energy transition, advanced manufacturing, and defence capabilities where supply disruption poses significant economic risk. This definition encompasses 26 specific minerals, including lithium, rare earth elements, cobalt, graphite, and nickel. Unlike traditional bulk commodities such as iron ore and coal, critical minerals often require specialised processing techniques and represent strategic assets rather than purely commercial ventures.

Australia currently holds commanding positions in several key categories. The nation possesses approximately 27% of global lithium resources, concentrated primarily in Western Australia's hard rock deposits. For rare earth elements, Australia controls roughly 17% of known reserves, though processing capacity remains limited compared to extraction capability. Cobalt reserves represent approximately 3% of global totals, primarily as by-products of nickel operations.

Economic Value Chain from Extraction to Processing

The economic structure of critical minerals differs fundamentally from bulk commodities. Raw extraction typically captures only 20-30% of the total value chain, while downstream processing and refining generate 50-70% of final product value. This creates a strategic challenge for Australia, which currently captures disproportionate value in raw extraction whilst losing processing opportunities to nations with more streamlined regulatory environments.

Consider lithium hydroxide production: the conversion from spodumene concentrate to battery-grade lithium hydroxide increases value by approximately 400-600%. Similarly, rare earth separation and purification can multiply raw ore values by factors of 10-20, depending on the specific elements recovered.

Current Economic Contribution:

• Export revenue: AUD $15-18 billion annually (2024-2025)

• Direct employment: Approximately 45,000-50,000 workers

• Regional economic multiplier: AUD 1.40-1.60 per dollar of mining activity

• Processing multiplier: AUD 1.80-2.20 per dollar of processing activity

Strategic Importance for Energy Transition and National Security

Critical minerals serve as the foundation for renewable energy infrastructure. A single electric vehicle battery requires approximately 8 kilograms of lithium, 35 kilograms of nickel, and substantial quantities of cobalt and graphite. Solar panels and wind turbines depend on rare earth elements for permanent magnets and power electronics systems.

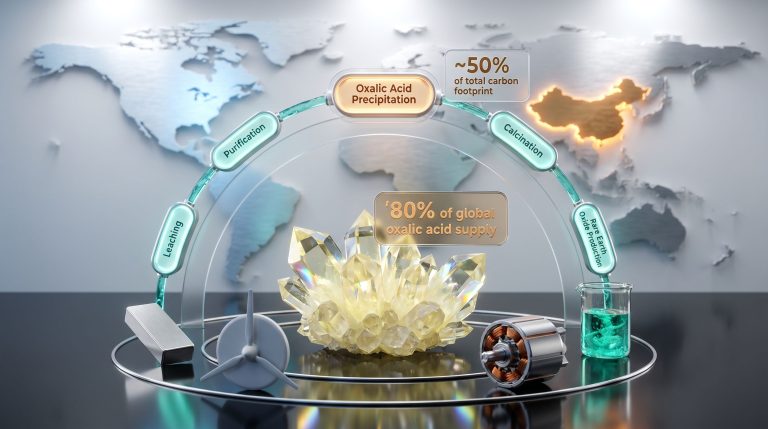

The national security dimension centres on supply chain concentration. China currently controls approximately 70-80% of global rare earth processing capacity despite holding only 37% of proven reserves. This concentration creates geopolitical leverage that extends beyond commercial considerations.

During 2022-2023, global semiconductor shortages demonstrated the vulnerability of supply chains dependent on single processing jurisdictions. Automotive production disruptions across Europe, Japan, and North America illustrated how critical mineral processing bottlenecks can cascade through entire industries. The critical minerals energy transition illustrates these interconnected dependencies.

Australia faces a unique opportunity to capture downstream value whilst supporting allied nations' supply chain diversification goals, potentially increasing annual export revenue by AUD $20-25 billion by 2035 through enhanced processing capacity.

Which Regulatory Bottlenecks Are Constraining Critical Minerals Development?

Australia's regulatory framework for critical minerals projects operates through multiple overlapping jurisdictions, creating complexity that extends project timelines and increases development costs. These bottlenecks represent perhaps the most significant barrier to realising the sector's economic potential.

Project Approval Timeframes vs International Competitors

Comparative analysis reveals significant disadvantages in Australia's approval processes:

| Jurisdiction | Environmental Assessment | Mining Permit | Total Timeline |

|---|---|---|---|

| Australia | 18-24 months | 12-18 months | 30-42 months |

| Canada | 12-18 months | 8-12 months | 20-30 months |

| Chile | 8-12 months | 6-10 months | 14-22 months |

These timelines reflect average durations for major critical minerals projects. Australia's extended assessment periods result from several factors: multiple regulatory jurisdictions operating independently, limited coordination between federal and state agencies, and appeal processes that can extend timelines by additional 12-24 months.

The Greenbushes lithium expansion in Western Australia exemplifies these challenges. The project experienced a 24-month approval extension due to environmental appeals and Indigenous consultation requirements, increasing project costs by approximately AUD $85 million and delaying production commencement by 18 months.

Environmental Assessment Complexity and Duplication

Australia's environmental assessment framework involves multiple overlapping processes. The Commonwealth Environment Protection and Biodiversity Conservation (EPBC) Act operates alongside state-based environmental assessments and local government planning approvals. This creates situations where identical environmental criteria are assessed separately under different legislative requirements without information sharing between agencies.

The EPBC Act assessment pathway requires mandatory referral within 10 business days, followed by either self-assessment (6-12 months) or formal assessment (18-24 months). However, these timelines frequently extend due to:

• Information requests requiring additional studies

• Public consultation periods extending beyond statutory minimums

• Ministerial discretion in final approval decisions

• Environmental group appeal rights

Cultural Heritage Protection Framework Challenges

Native Title claims and consultation requirements represent essential components of project development, ensuring Indigenous partnership and cultural preservation. However, current processes operate without standardised timeframes or streamlined procedures. Some projects experience 2-3 year consultation periods compared to 6-12 months under Canada's consultation protocols with First Nations.

The challenge lies in balancing cultural preservation with economic development objectives. Unlike Canada's integrated consultation framework, Australia's processes often operate separately from environmental and mining approval pathways, creating potential for duplicated requirements and extended timelines.

Key Areas for Improvement:

• Standardised consultation timeframes with clear milestones

• Integration with environmental assessment processes

• Cultural heritage management plans developed concurrently with mining proposals

• Early engagement protocols to identify issues before formal assessment

How Do Workforce Challenges Impact Critical Minerals Project Viability?

Australia's critical minerals sector faces substantial workforce constraints that extend beyond traditional mining skill sets. These challenges encompass technical expertise gaps, migration policy barriers, and regional infrastructure limitations that collectively constrain project development and operational efficiency.

Skills Shortage Analysis Across Mining Disciplines

Critical minerals processing requires specialised expertise distinct from traditional mining operations. Metallurgical engineering, hydrometallurgy, and environmental engineering roles face particular shortages. The sector requires professionals with experience in:

• Rare earth separation and purification processes

• Lithium hydroxide and carbonate production

• Environmental management for chemical processing

• Battery materials quality control and testing

Metallurgical engineering specialisation requires 5-7 years of formal education plus 2-3 years of practical experience, creating extended time-to-productivity for new entrants. Currently, Australian educational institutions offer limited programs specifically focused on critical minerals processing, with only 3-4 dedicated programs nationally.

Liontown Resources (ASX: LTR) partnered with Edith Cowan University's Mental Awareness, Respect and Safety (MARS) Centre to study FIFO worker wellbeing at the Kathleen Valley lithium operation. Research conducted between March and April 2024, involving 72 Liontown employees, examined how team belongingness influences mental health outcomes for remote site workers, addressing recruitment and retention challenges inherent in regional operations.

Migration Policy Barriers for Specialist Roles

Australia's skilled occupation list (SOL) pathways for mining metallurgists and processing specialists remain limited. Visa approval rates for mining sector roles average 65-75% despite positions being listed as in-demand. Processing specialists face particular barriers as these roles are not categorised within primary migration pathways.

The technical nature of critical minerals processing creates additional complications. Unlike traditional mining roles, processing positions require knowledge of complex chemical processes, environmental controls, and quality assurance systems. These specialised requirements often do not align with standard occupational classifications used in migration assessments.

Regional Employment and Training Infrastructure Gaps

Critical minerals processing typically requires locations near ports, energy infrastructure, and technical services. However, regional mining communities often lack the secondary and tertiary service sectors necessary to support family-friendly employment. This infrastructure gap contributes to recruitment challenges and higher turnover rates. Additionally, mining industry trends suggest increasing demand for specialised skills.

Fly-in/fly-out (FIFO) employment models, whilst enabling workforce access to remote locations, contribute to 25-30% annual turnover rates in critical minerals operations compared to 15-18% in comparable Canadian operations with permanent regional employment models.

Skills shortages in critical minerals processing represent a bottleneck that could limit Australia's ability to capture downstream value, with current training pipelines producing fewer than 200 qualified metallurgists annually against projected demand for 800-1000 specialists by 2030.

What Economic Opportunities Could Reform Unlock?

Regulatory reform in Australia's critical minerals sector could generate substantial economic benefits through accelerated project development, enhanced processing capabilities, and improved international competitiveness. These opportunities extend beyond direct mining revenue to encompass regional development and export diversification.

Revenue Projections from Accelerated Project Development

Current critical minerals export revenue totals approximately AUD $15-18 billion annually. Reform scenarios suggest potential expansion to AUD $35-45 billion annually by 2035, representing growth of 150-200%. This projection assumes:

• Reduced project approval timeframes from 30-42 months to 18-24 months

• Enhanced processing capacity capturing 40-50% of value chain

• Increased production volumes across lithium, rare earths, and battery materials

Production Potential Analysis:

| Mineral | Current Production | Potential with Reform | Value Increase |

|---|---|---|---|

| Lithium | 55,000 tonnes | 85,000 tonnes | +AUD $3-4 billion |

| Rare Earths | 22,000 tonnes | 45,000 tonnes | +AUD $2-3 billion |

| Nickel Sulfate | 15,000 tonnes | 35,000 tonnes | +AUD $1-2 billion |

These projections reflect both increased extraction capacity and enhanced processing capabilities. The value increases assume downstream processing development rather than raw material exports.

Regional Economic Multiplier Effects

Critical minerals development generates significant regional economic activity beyond direct employment. Mining operations create AUD 1.40-1.60 in broader economic activity per dollar of direct revenue, while processing operations generate AUD 1.80-2.20 multipliers.

Processing facilities typically employ 200-400 workers directly and support 600-1,200 indirect jobs in supporting services, logistics, and maintenance. These operations also require substantial infrastructure investment:

• Power generation and transmission infrastructure

• Water treatment and supply systems

• Transport and logistics networks

• Technical and professional services

Export Diversification and Trade Balance Improvements

Enhanced critical minerals production would reduce Australia's dependence on bulk commodity exports whilst supporting trade relationships with allied nations seeking supply chain diversification. The strategic value extends beyond commercial considerations to encompass geopolitical advantages. The development of a critical minerals reserve could further enhance Australia's strategic position.

Critical minerals exports to the United States, European Union, Japan, and South Korea could increase by AUD $8-12 billion annually through expanded production and processing capacity. These markets offer premium pricing for sustainably produced materials with transparent supply chains.

Hypothetical Reform Impact Scenario:

If regulatory reforms reduced project approval timeframes by 40% and enhanced workforce development addressed 60% of skills shortages, Australia could capture an additional AUD $8.5 billion in critical minerals export value by 2030, supporting 25,000 direct and indirect jobs across regional communities.

Which International Models Could Inform Australian Reform Strategies?

Comparative analysis of international regulatory frameworks reveals several successful models for streamlining critical minerals project approvals whilst maintaining environmental and social safeguards. These examples provide practical guidance for Australian policy development.

Canada's One-Window Approval System

Canada implemented the Impact Assessment Act (IAA) in 2019, creating integrated environmental and regulatory assessment processes. The one-window system coordinates federal, provincial, and territorial approvals through a single point of contact, reducing duplication and improving timeline predictability.

Key features include:

• Maximum 600-day assessment timeline with legislated milestones

• Early planning phase to identify issues before formal assessment

• Indigenous consultation integrated throughout the process

• Digital platforms for information sharing between agencies

Canadian critical minerals projects now average 20-30 months for full approval compared to Australia's 30-42 months. The system has maintained environmental standards whilst improving investment certainty.

Chile's Streamlined Environmental Framework

Chile's environmental assessment system operates through the Environmental Assessment Service (SEA), which coordinates all environmental approvals for mining projects. The framework includes:

• Single environmental impact assessment covering all regulatory requirements

• Standardised consultation processes with Indigenous communities

• Electronic submission and tracking systems

• Binding timelines for agency responses

Chile achieves 14-22 month total approval timelines for major projects whilst maintaining robust environmental protection. The system's efficiency has contributed to Chile's position as a leading lithium producer.

Nordic Countries' Stakeholder Engagement Protocols

Sweden and Finland have developed comprehensive stakeholder engagement frameworks that integrate Indigenous rights (Sami reindeer herding communities), environmental protection, and economic development. These protocols include:

• Early consultation requirements before permit applications

• Standardised compensation and benefit-sharing agreements

• Ongoing monitoring and adaptive management systems

• Clear dispute resolution mechanisms

These frameworks have enabled development of critical minerals projects in environmentally sensitive areas whilst maintaining social licence to operate.

The next major ASX story will hit our subscribers first

How Would Workplace Relations Reform Impact Project Economics?

Australia's workplace relations framework significantly influences critical minerals project economics through labour costs, productivity levels, and operational flexibility. Recent developments, particularly the "same job, same pay" legislation, illustrate the complex relationship between regulatory policy and industry competitiveness.

Labour Cost Competitiveness Analysis

Australian mining wages typically range from AUD $120,000-$160,000 annually for skilled trades positions. Comparative analysis with international competitors shows:

• Canada: CAD $90,000-$120,000 (approximately AUD $135,000-$180,000)

• Chile: USD $45,000-$65,000 (approximately AUD $70,000-$100,000)

• South Africa: USD $25,000-$40,000 (approximately AUD $40,000-$60,000)

Whilst Australian wages appear competitive with Canada, the total cost of employment including superannuation, workers' compensation, and FIFO arrangements often exceeds international comparisons by 20-30%.

The Federal Government's "same job, same pay" legislation, implemented in 2024, requires labour-hire workers to receive equivalent wages and conditions as directly employed staff. BHP (ASX: BHP) has challenged this ruling through the High Court, arguing the legislation threatens specialised contractor services essential to mining operations.

Productivity Implications of Current Industrial Relations Framework

Australia's industrial relations system emphasises worker protection and consultation, which can impact operational flexibility in critical minerals processing. Key considerations include:

• Shift arrangements and continuous operation requirements

• Maintenance shutdown scheduling and contractor integration

• Skills training and cross-functional deployment

• Technology adoption and process optimisation

The Minerals Council of Australia calls for critical reforms have expressed concern that same job, same pay requirements could threaten thousands of specialised contractors who provide essential services rather than just workers. This highlights tensions between employment equity objectives and operational efficiency requirements.

Contractor vs Direct Employment Models in Critical Minerals

Critical minerals processing requires diverse specialised services including metallurgical analysis, environmental monitoring, equipment maintenance, and logistics coordination. Many operations rely on contractor arrangements to access specialised expertise without maintaining permanent employment for seasonal or project-specific requirements.

The same job, same pay legislation may influence employment structures by:

• Encouraging direct employment over contractor arrangements

• Increasing costs for specialised technical services

• Potentially reducing operational flexibility

• Affecting regional employment patterns

Resources Minister Madeleine King argues the legislation ensures workplace fairness and could improve morale, potentially enhancing productivity through better worker engagement and retention.

What Role Does Cultural Heritage Protection Play in Project Delays?

Cultural heritage protection represents a fundamental component of critical minerals project development, ensuring Indigenous partnership and preservation of significant sites. However, current processes can extend project timelines and create uncertainty without necessarily delivering optimal outcomes for all stakeholders.

Native Title Act Application to Critical Minerals Projects

The Native Title Act 1993 requires consultation and agreement with Indigenous communities for mining activities on traditional lands. This framework applies to most critical minerals deposits, which often occur in remote areas with established Native Title claims or determinations.

Key requirements include:

• Right to negotiate provisions for exploration and mining activities

• Cultural heritage surveys and protection protocols

• Ongoing consultation throughout project development

• Benefit-sharing agreements and employment opportunities

Whilst these protections are essential for Indigenous rights and cultural preservation, the consultation process can extend project timelines by 18-36 months depending on the complexity of claims and stakeholder engagement requirements.

Stakeholder Consultation Requirements and Timeframes

Current consultation processes lack standardised timeframes or integrated coordination with environmental assessments. Some projects experience consultation periods exceeding 3 years, compared to 6-12 months under Canada's consultation protocols with First Nations.

The absence of clear milestone timelines creates uncertainty for project proponents and may not serve Indigenous communities' interests effectively. Extended consultation periods can result in:

• Delayed economic benefits for Indigenous communities

• Increased project costs reducing available benefit-sharing funds

• Potential project cancellation affecting long-term partnership opportunities

Balancing Cultural Preservation with Economic Development

Successful integration of cultural heritage protection with project development requires early engagement, clear processes, and genuine partnership approaches. International examples suggest several improvements:

• Early consultation protocols before formal permit applications

• Cultural heritage management plans developed collaboratively

• Standardised assessment criteria and timeline frameworks

• Integration with environmental assessment processes

The objective should be effective cultural protection whilst providing certainty for all stakeholders. This requires moving beyond minimum consultation requirements toward genuine partnership models that deliver economic benefits alongside cultural preservation.

Effective cultural heritage frameworks can enhance rather than constrain project development by building community support, reducing operational risks, and creating sustainable benefit-sharing arrangements that support long-term project success.

How Could Migration Policy Reform Address Skills Shortages?

Australia's migration framework requires targeted reforms to address critical minerals sector workforce gaps. Current policies inadequately recognise the specialised nature of processing roles and fail to provide streamlined pathways for essential technical expertise.

Specialist Visa Categories for Critical Minerals Expertise

The Global Talent Independent (GTI) program and Employer Nomination Scheme (ENS) provide pathways for skilled migration, but application processes often exceed 12-18 months. Critical minerals projects require faster deployment of specialised expertise, particularly for:

• Hydrometallurgical process engineers

• Rare earth separation specialists

• Battery materials quality control technicians

• Environmental engineers with chemical processing experience

A dedicated critical minerals visa stream could expedite processing for nationally prioritised projects. This might include:

• 6-month maximum processing timeline

• Recognition of international qualifications and experience

• Pathway to permanent residency for long-term projects

• Family reunion provisions for regional deployment

Regional Migration Incentives for Mining Communities

Current regional migration programs focus on population growth rather than specific industry requirements. Critical minerals processing facilities often locate in regional areas with limited existing workforce, requiring targeted migration support.

Potential enhancements include:

• Enhanced regional points systems for mining-related skills

• Reduced income thresholds for critical minerals positions

• Fast-track processing for positions in designated regional projects

• Integration with state government regional development programs

International Talent Attraction Strategies

Australia competes globally for specialised technical talent, particularly with Canada, Chile, and emerging African mining jurisdictions. Competitive advantages include:

• Political stability and regulatory certainty

• Advanced mining education and research institutions

• Established mining services sector

• Geographic proximity to Asian markets

However, lengthy visa processing, complex qualification recognition, and limited pathway certainty reduce Australia's attractiveness compared to competitor jurisdictions. Furthermore, lithium industry innovations demonstrate the need for specialised expertise.

Strategic Recommendations:

• Bilateral skill-sharing agreements with allied nations

• Fast-track visa processing for critical minerals projects

• International qualification recognition protocols

• Targeted recruitment campaigns in key source countries

What Are the Geopolitical Implications of Delayed Reform?

Australia's regulatory reform timeline has significant implications beyond domestic economic considerations. Critical minerals represent strategic assets in global technology competition, supply chain security, and alliance relationships with like-minded nations seeking alternatives to concentrated supply chains.

Supply Chain Security and Strategic Autonomy

China's dominance in critical minerals processing creates strategic vulnerabilities for allied nations. Rare earth processing concentration of 70-80% in China, despite holding only 37% of reserves, demonstrates how processing capability translates into geopolitical leverage.

Recent developments illustrate these dynamics:

• China escalated trade tensions with BHP over iron ore pricing disputes

• Rare earth export controls were temporarily suspended following US-China trade negotiations

• Deep sea mining initiatives reflect growing competition for alternative supply sources

Australia's delayed development of processing capabilities reduces options for allied nations seeking supply chain diversification. This creates opportunity costs as competitors advance their processing infrastructure.

Competition with China's Integrated Minerals Strategy

China's approach integrates resource extraction, processing, manufacturing, and market access through coordinated government and industry collaboration. This includes:

• Direct investment in overseas mining projects

• Technology transfer requirements for market access

• Coordinated development of processing capabilities

• Strategic stockpiling of critical materials

Australia's fragmented regulatory approach and extended approval timelines provide advantages to competitors with more coordinated policies. China's integrated strategy enables rapid deployment of capital and expertise to develop alternative supply sources.

Allied Nation Cooperation and Critical Minerals Partnerships

The United States, European Union, Japan, and other allied nations actively seek partnerships with Australia for critical minerals supply chain development. These partnerships offer:

• Technology sharing and joint research initiatives

• Investment facilitation and risk mitigation

• Market access and procurement agreements

• Strategic coordination on standards and regulations

However, extended project timelines and regulatory uncertainty limit Australia's ability to capitalise on these partnership opportunities. Other jurisdictions with streamlined approval processes may capture investments and partnerships intended for Australian projects.

President Trump's executive order advancing deep-sea mining reflects growing urgency around supply chain security. This unilateral approach demonstrates how regulatory delays in established mining jurisdictions drive investment toward alternative sources, including untested deep-sea resources.

Delayed regulatory reform risks positioning Australia as a raw materials supplier rather than a strategic partner in allied nations' supply chain diversification efforts, potentially limiting long-term economic and geopolitical advantages.

Which Specific Policy Changes Would Deliver Maximum Impact?

Targeted policy reforms could address Australia's critical minerals bottlenecks whilst maintaining environmental and social safeguards. These changes require coordination across federal, state, and local jurisdictions to deliver meaningful improvements in project timelines and investment certainty.

Environmental Assessment Streamlining Proposals

The most impactful reform involves integrating Commonwealth and state environmental assessment processes through bilateral agreements. This would eliminate duplicated assessments whilst maintaining environmental protection standards.

Specific Recommendations:

• Single environmental assessment process covering federal and state requirements

• Digital information sharing platforms between regulatory agencies

• Binding timeline commitments with deemed approval mechanisms

• Early scoping processes to identify key issues before formal assessment

The Canadian Impact Assessment Act provides a practical model, achieving 20-30 month timelines compared to Australia's 30-42 months whilst maintaining comprehensive environmental evaluation.

Skills-Based Migration Pathway Enhancements

Critical minerals visa pathways should recognise the strategic importance of processing expertise through:

• Fast-track processing (maximum 6 months) for designated skills

• International qualification recognition agreements

• Regional deployment incentives for processing facility locations

• Pathway integration with permanent residency options

These changes would address immediate workforce constraints whilst building long-term capability in specialised technical roles.

Cultural Heritage Consultation Process Optimisation

Improved consultation frameworks should provide certainty for all stakeholders through:

• Standardised consultation timelines with clear milestones

• Early engagement protocols before formal permit applications

• Integration with environmental assessment processes

• Benefit-sharing agreement templates for common arrangements

The objective is effective cultural protection with predictable processes that serve Indigenous communities' economic development objectives alongside cultural preservation.

What Implementation Timeline Would Optimise Economic Benefits?

Strategic reform implementation should prioritise high-impact changes whilst building momentum for comprehensive regulatory transformation. This approach balances immediate improvements with long-term structural reform requirements.

Short-term Regulatory Adjustments (6-12 months)

Immediate improvements can be achieved through administrative changes and existing legislative frameworks:

• Enhanced agency coordination protocols for information sharing

• Digital submission and tracking systems for permit applications

• Standardised assessment criteria to reduce inconsistent requirements

• Fast-track pathways for nationally significant projects

These changes could reduce current timelines by 15-25% without requiring new legislation.

Medium-term Structural Reforms (1-3 years)

Comprehensive reform requires legislative changes and institutional development:

• Bilateral environmental assessment agreements between jurisdictions

• Critical minerals-specific visa categories and processing pathways

• Integrated cultural heritage consultation frameworks

• One-window approval systems for major projects

These reforms could achieve 30-40% timeline reductions and significantly improve investment certainty.

Long-term Strategic Framework Development (3-5 years)

Sustained competitiveness requires institutional capability building:

• Specialised education and training programs for critical minerals expertise

• Regional infrastructure development supporting processing operations

• International cooperation frameworks with allied nations

• Technology development and commercialisation support

This timeline would position Australia as a preferred destination for critical minerals investment whilst maintaining environmental and social standards.

The Minerals Council of Australia's stance on mining policy and the MCA calls for critical minerals reform reflect industry recognition that opportunities must translate into operational projects to deliver economic benefits. Success requires coordinated action across regulatory, workforce, and infrastructure dimensions to capture Australia's strategic advantages in the global energy transition.

How Do These Reforms Align with Global Energy Transition Goals?

Australia's critical minerals reform agenda intersects directly with global decarbonisation timelines and clean energy infrastructure deployment. The pace of regulatory improvement will determine whether Australia captures its proportionate share of the expanding clean technology market.

Critical Minerals Demand Projections for Clean Energy

International Energy Agency projections indicate critical minerals demand will increase by 300-500% by 2035 under net-zero emission scenarios. Specific requirements include:

• Lithium demand: 400-500% increase for battery storage and electric vehicles

• Rare earth elements: 300-400% increase for permanent magnets in wind turbines

• Cobalt and nickel: 200-300% increase for battery cathode materials

• Graphite: 250-350% increase for battery anode materials

This demand growth creates unprecedented opportunities for resource-rich nations with appropriate processing capabilities. However, supply development must align with technology deployment timelines to capture premium pricing and strategic partnerships.

Australia's Competitive Advantages in Sustainable Mining

Australia possesses several structural advantages for sustainable critical minerals production:

• Abundant renewable energy resources reducing processing emissions

• Established mining expertise and equipment manufacturing capabilities

• Transparent regulatory frameworks and stable political institutions

• Proximity to major Asian manufacturing and technology markets

These advantages become more valuable as environmental, social, and governance (ESG) requirements influence supply chain decisions. European and North American manufacturers increasingly prioritise sustainably sourced materials with traceable supply chains.

Integration with Renewable Energy and Processing Hubs

Critical minerals processing requires substantial electricity consumption, creating opportunities for integration with renewable energy developments. Lithium hydroxide production consumes 15-20 MWh per tonne, whilst rare earth separation requires 50-100 MWh per tonne.

Australia's renewable energy expansion could support processing hub development through:

• Co-located solar and wind generation with processing facilities

• Battery storage systems utilising locally produced lithium

• Hydrogen production for chemical processing applications

• Grid stabilisation services from integrated industrial loads

This integration would reduce processing costs whilst supporting renewable energy deployment goals. The model creates sustainable competitive advantages as carbon pricing and emissions regulations influence global supply chain decisions.

Reform success requires alignment between regulatory timelines and global energy transition schedules. Delayed development risks market share capture by competitors with more responsive policy frameworks, whilst successful reform positions Australia as an essential partner in global decarbonisation efforts. Consequently, the MCA calls for critical minerals reform represent a crucial step toward capturing Australia's strategic advantages in the global energy transition.

Disclaimer: This article contains forward-looking projections and market analysis based on current industry trends and policy proposals. Actual outcomes may vary significantly due to regulatory changes, market conditions, technological developments, and geopolitical factors. Readers should conduct independent research and seek professional advice before making investment or policy decisions based on this analysis.

Looking to Capitalise on Australia's Critical Minerals Boom?

Discovery Alert's proprietary Discovery IQ model delivers real-time notifications on significant ASX mineral discoveries, empowering subscribers to identify actionable opportunities as regulatory reforms unlock unprecedented potential in Australia's critical minerals sector. Explore historic examples of exceptional returns from major mineral discoveries at Discovery Alert's discoveries page and begin your 14-day free trial today to position yourself ahead of the market.