August 3, 2026

Europe's Industrial Security Reckoning: Why Sovereign Mineral Reserves Are Now a Strategic Imperative

For most of the post-Cold War era, Western industrial economies operated on a foundational assumption: that global commodity markets would reliably supply whatever raw materials manufacturing required, at prices shaped by competition rather than geopolitics. That assumption has been systematically dismantled over the past several years, and nowhere is the correction more visible than in Europe's accelerating push to build a physical EU emergency stockpile of critical minerals.

The decision to accumulate sovereign mineral reserves is not simply a policy adjustment. It represents a structural rethinking of how industrial supply chains interact with national security, and what role state intervention must play when market mechanisms cannot be trusted to deliver strategically essential inputs.

When big ASX news breaks, our subscribers know first

The Architecture of Vulnerability: How Europe Got Here

Europe's critical minerals supply chain exposure to supply disruption was not sudden. It accumulated gradually across decades of optimising supply chains for cost rather than resilience. The result was a continent heavily dependent on a single dominant processing nation, China, for materials that underpin nearly every advanced technology sector from electric vehicles and renewable energy to semiconductor fabrication and defence systems.

The breaking point came in stages. China's rare earth export restrictions, most notably on gallium and germanium imposed in 2023, served as a concrete demonstration that dominant supplier nations were prepared to use mineral access as a geopolitical instrument. These were not theoretical risks debated in policy papers. They were live disruptions that sent immediate shockwaves through supply chains across the semiconductor, defence electronics, and advanced manufacturing sectors.

The COVID-19 pandemic had already exposed the fragility of lean, just-in-time logistics for industrial inputs. The combination of pandemic-era disruption and deliberate export controls created the political conditions for a response that would have seemed extreme a decade earlier: treating minerals the way nations treat petroleum, as strategic reserves requiring sovereign management.

What the EU Emergency Stockpile Actually Is

The EU emergency stockpile of critical minerals is a coordinated, bloc-wide reserve system designed to provide European industry and defence sectors with a buffer against supply chain shocks caused by geopolitical events, export restrictions, or logistics failures.

The stockpile framework is conceptually analogous to strategic petroleum reserves, applying the same national security logic to raw materials that advanced technology and defence manufacturing cannot function without.

According to reporting by the Financial Times, key structural features of the programme include:

- First announced by the European Commission in December 2025 as part of a broader industrial preparedness initiative

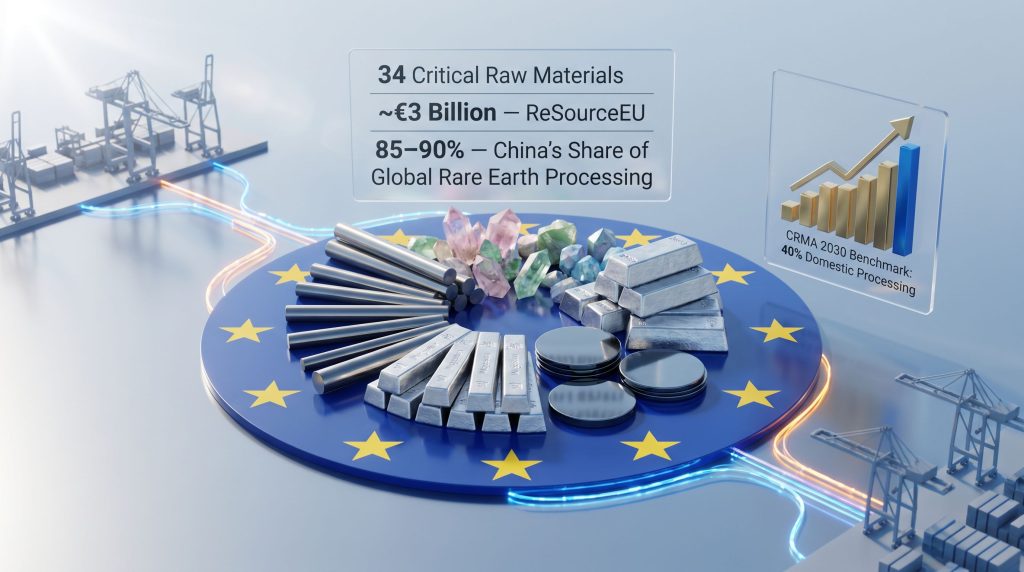

- Operates within the legal framework of the Critical Raw Materials Act (CRMA), which identifies 34 critical raw materials across the EU's strategic supply list

- Currently driven by 10 EU member states through specialised working groups co-led by Germany, France, and Italy

- Governed by a proposed permanent secretariat specifically designed to insulate the initiative from disruption caused by the EU's six-month rotating Council presidency

- Distinct from commercial inventory held by private operators, the stockpile is intended for release only under formally defined crisis conditions

The permanent secretariat model deserves particular attention. The EU's historical difficulty in maintaining long-term industrial policy coherence across rotating presidencies has repeatedly undermined bloc-wide initiatives. Structuring the stockpile governance outside that rotation cycle reflects a maturation in how European policymakers are approaching industrial resilience.

Which Minerals Made the Shortlist and Why

The materials under consideration for the inaugural stockpile were not selected arbitrarily. Each occupies a unique position of strategic importance combined with acute supply concentration risk.

| Mineral | Primary Application | Key Supply Risk |

|---|---|---|

| Tungsten | Defence hardware, cutting tools, radiation shielding | Dominant Chinese export position |

| Rare Earth Elements | EV motors, wind turbines, defence electronics | Near-total Chinese processing control (~85-90%) |

| Gallium | Semiconductors, radar, power electronics | Subject to Chinese export restrictions since 2023 |

| Magnesium | Lightweight alloys, automotive manufacturing | Highly concentrated Chinese production base |

| Germanium | Fibre optics, infrared systems, semiconductors | Chinese export controls imposed 2023 |

| Graphite | EV battery anodes, fuel cells | China controls approximately 80% of global supply |

Three sources familiar with EU planning confirmed tungsten, rare earths, and gallium as shortlisted, with two additional sources indicating magnesium would also feature, and a further source pointing to germanium and graphite as likely inclusions.

The NATO Connection: Where Industrial Policy Meets Defence Doctrine

One dimension of the shortlist that receives insufficient attention in mainstream analysis is its alignment with NATO's own strategic materials register. Nearly all minerals under consideration appear on NATO's list of 12 elements deemed critical to the defence industrial base. This convergence is not coincidental.

The overlap between the EU's stockpile shortlist and NATO's critical materials register signals a formal elevation of mineral supply security from economic policy to defence preparedness doctrine.

The EU's preparedness documentation explicitly references war-risk scenarios and cyberattack-driven logistics disruptions as conditions that could trigger reserve drawdowns. This language marks a fundamental shift from how European policymakers have historically framed raw material supply questions.

A less widely understood dimension involves the processing bottleneck problem. Even if the EU were to successfully diversify its mining supply sources, the reality is that China controls an estimated 85 to 90 percent of global rare earth processing capacity. Raw ore extracted from Australian, Canadian, or African deposits often still requires routing through Chinese refiners before it reaches a form that European manufacturers can actually use.

This means that stockpiling unrefined ore offers limited protection in a genuine supply emergency. Furthermore, the most strategically valuable reserves would consist of processed and refined materials, such as permanent magnets and refined rare earth compounds, ready for direct industrial application.

Infrastructure: Where the Reserves Will Be Held

The physical storage architecture being developed reflects a dual-hub model designed to provide geographic redundancy across Europe's northern and southern maritime corridors.

Northern Anchor: Port of Rotterdam

The Port of Rotterdam, Europe's largest maritime hub, is in advanced discussions with both the Dutch Ministry and EU officials regarding its role as the primary northern storage facility. A Rotterdam port authority spokesperson confirmed active engagement with national and EU-level stakeholders on critical raw material storage objectives, noting the port's strong positioning to contribute to regional goals in this area.

Rotterdam's existing bonded warehousing capacity, multimodal logistics connectivity, and established customs infrastructure make it the operationally logical choice for northern European storage. Its deep-water access also positions it to receive large shipments from allied-nation suppliers across the Atlantic and Pacific.

Southern Corridor: Italian Ports

Italian Industry Minister Adolfo Urso confirmed that EU officials conducted site inspections at Porto Marghera, near Venice, and the Port of Trieste to evaluate their suitability as Mediterranean storage nodes.

The strategic rationale for a Mediterranean hub is distinct from the northern rationale. The Italian port corridor serves supply routes originating from Africa and the Middle East, regions that are increasingly central to EU supply diversification efforts as the bloc seeks alternatives to Chinese-dominated supply chains. A dual-hub structure also mitigates single-point-of-failure risk in the reserve network.

The CRMA Framework: Binding Benchmarks Driving the Agenda

The emergency stockpile initiative does not exist in isolation. It operates as a demand-side resilience tool within the broader architecture of the Critical Raw Materials Act, which establishes legally binding supply benchmarks that EU member states must achieve by 2030. The establishment of a critical raw materials facility under this framework is central to the EU's long-term industrial strategy.

CRMA 2030 Benchmarks:

- At least 10% of annual EU consumption of strategic raw materials must come from domestically sourced extraction

- At least 40% of annual consumption must be processed internally within the EU

- No single third country may supply more than 65% of any strategic raw material consumed by the EU

These benchmarks represent an ambitious restructuring of European supply chains, and the stockpile provides the emergency buffer while that longer-term restructuring is underway. The 65 percent concentration cap is particularly significant, as China currently exceeds that threshold for multiple shortlisted minerals simultaneously.

The next major ASX story will hit our subscribers first

Global Context: How the EU's Approach Compares

The EU is not operating in isolation. A broader Western realignment toward sovereign mineral reserve strategies is underway across multiple jurisdictions.

| Jurisdiction | Reserve Model | Key Minerals | Funding Mechanism |

|---|---|---|---|

| European Union | Joint bloc-wide emergency stockpile | REEs, tungsten, gallium, germanium, graphite, magnesium | EU coordination + member state co-investment |

| United States | National Defence Stockpile (NDS) | 50+ strategic materials | Congressional appropriations |

| Japan | Government-mandated private reserves | REEs, lithium, cobalt | Subsidised private sector obligations |

| South Korea | State-managed buffer stocks | Lithium, nickel, cobalt | Korea Resources Corporation |

| China | State Reserve Bureau holdings | Broad commodity basket | Central government directive |

The EU's approach is notable for attempting to coordinate reserve-building across 27 sovereign member states with divergent industrial interests, a task considerably more complex than the unilateral programmes operated by the US, Japan, or South Korea.

Complementing the physical stockpile, the EU has committed approximately €3 billion through the ReSourceEU plan to fund upstream and midstream supply chain development, including mine development, domestic refining infrastructure, and allied-nation sourcing partnerships. This dual-track approach recognises that stockpiling buys time but cannot substitute for structural supply chain transformation.

France has used its G7 presidency to accelerate multilateral alignment on supply diversification, pushing partner nations toward coordinated reserve frameworks. The AU$5 billion Australia-US critical minerals partnership is directly relevant to this allied supply strategy, positioning Australia as a preferred source nation for both American and European diversification objectives.

Market Dynamics and Investor Implications

The entry of sovereign entities into mineral markets as buyers for reserve accumulation introduces dynamics that differ fundamentally from commercial procurement.

How Stockpiling Reshapes Mineral Pricing

- Sovereign reserve accumulation creates non-commercial demand that does not respond to price signals in the same way private buyers do, potentially establishing price floors for shortlisted minerals

- Announcement effects alone can trigger forward pricing adjustments in spot and futures markets before a single tonne of material is physically purchased

- The scale of potential EU procurement, combined with matching programmes in the US and allied nations, could represent a structural demand shift for materials like gallium, germanium, and rare earth compounds

Sectors Most Exposed to Supply Disruption

- Electric Vehicle Manufacturing: Rare earth permanent magnets, specifically neodymium-iron-boron (NdFeB) formulations, are not readily substitutable in high-performance EV motors. Gallium and germanium are critical in associated power electronics

- Renewable Energy Infrastructure: Large-scale wind turbines rely heavily on NdFeB magnets, creating a direct linkage between rare earth supply chains and clean energy deployment timelines

- Semiconductor Fabrication: Gallium nitride (GaN) and germanium-based compound semiconductors are foundational to next-generation chip architectures, including those used in defence radar and communications systems

- Defence and Aerospace: Tungsten's extreme density (approximately 19.3 g/cm³), high melting point (3,422°C), and radiation shielding properties make it irreplaceable in armour-penetrating munitions, aerospace components, and nuclear shielding applications. No commercially viable substitute exists at scale

The Allied Supplier Opportunity

For mining jurisdictions positioned as preferred EU supply partners, the formalisation of the EU emergency stockpile of critical minerals represents a multi-year, policy-backed demand signal that extends well beyond normal commodity market cycles.

Furthermore, the critical minerals demand surge driven by the energy transition and defence spending increases means that Australia's geological endowment across multiple shortlisted minerals, combined with its stable governance framework and existing trade relationships with EU member states, places it in a strong structural position. Australian tungsten, rare earth, and graphite projects that might previously have struggled to attract strategic buyer interest are now operating in a fundamentally different demand environment.

The window for supply agreements and long-term offtake contracts aligned with EU strategic procurement preferences is opening ahead of the stockpile's formal operationalisation, meaning early-stage producers and explorers in allied jurisdictions may benefit from accelerated buyer engagement before reserve-building demand peaks.

Key Programme Statistics at a Glance

| Metric | Figure |

|---|---|

| EU Critical Raw Materials under CRMA | 34 |

| EU member states driving stockpile planning | 10 |

| ReSourceEU investment commitment | ~€3 billion |

| China's share of global rare earth processing | ~85-90% |

| China's share of global graphite supply | ~80% |

| NATO strategic materials list | 12 elements |

| CRMA domestic processing benchmark (by 2030) | 40% of annual consumption |

| CRMA single-supplier concentration cap (by 2030) | 65% maximum from any one country |

| Tungsten melting point | 3,422°C |

Three Structural Risks That Could Undermine the Programme

-

Political Fragmentation: Achieving binding consensus across 27 member states with divergent industrial interests on cost-sharing arrangements, drawdown conditions, and governance authority remains the programme's most significant execution risk. The permanent secretariat model addresses this partially but does not eliminate it.

-

The Refining Bottleneck: Accumulating stockpiles of raw or semi-processed materials without corresponding domestic refining capacity may create reserves of limited utility when they are actually needed. Closing the processing gap requires parallel investment timelines measured in years, not months.

-

Market Distortion Effects: Large-scale sovereign procurement by multiple allied nations simultaneously could create unintended volatility for downstream industrial users who depend on stable spot market pricing. The coordination of drawdown protocols with allied reserve programmes, particularly with the United States, will be essential to managing this risk.

The Long View: From Emergency Buffer to Industrial Sovereignty

The EU emergency stockpile of critical minerals is best understood as a transitional instrument rather than a permanent solution. Its function is to buy Europe time while the deeper structural transformation of its supply chains is completed.

That transformation requires sustained investment across the full mineral value chain: exploration, extraction, processing, refining, and end-of-life recovery through circular economy frameworks. The €3 billion ReSourceEU commitment targets the upstream and midstream segments, while the EU's growing investment in battery recycling and urban mining addresses the downstream recovery dimension.

However, as Reuters has reported, the geopolitical urgency driving this initiative shows no sign of abating. Nations and companies that establish secure, diversified critical mineral supply chains ahead of a potential acute shortage will hold structural competitive advantages in advanced manufacturing, clean energy deployment, and defence procurement that could persist for decades.

The EU's shift from market reliance to sovereign reserve logic is not a temporary overreaction to short-term disruptions. It is a permanent recalibration of how advanced economies manage the raw material foundations of technological and industrial power.

This article contains references to market forecasts, policy projections, and forward-looking analysis. Readers should note that policy timelines, investment figures, and market outcomes are subject to change and should not be construed as financial advice. All statistics cited reflect publicly available information as of the date of publication.

Want to Know Which ASX Explorers Are Positioned for Europe's Critical Minerals Demand?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly alerting subscribers to significant mineral discoveries across tungsten, rare earths, gallium, graphite, and other minerals now central to Europe's sovereign stockpile strategy — explore historic discoveries and their returns to understand the opportunity, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.