June 4, 2026

The Hidden Chokepoint: Why America's Critical Mineral Problem Is Bigger Than Most Realise

Long before geopolitical tensions surfaced in trade war headlines, a quieter contest was already underway. For decades, while Western economies focused on oil markets, defence procurement, and semiconductor trade, a separate but equally consequential race was being run in the world's mining districts, processing facilities, and resource ministries. That race was for control over the raw materials that make modern civilisation function: the minerals embedded in electric motors, radar systems, smartphone displays, and satellite guidance hardware.

The United States is now reckoning with just how far behind it has fallen. America's critical mineral strategy, while gaining momentum in recent years, faces structural constraints that executive orders and policy frameworks alone cannot quickly resolve. Understanding why requires looking beneath the surface of the political debate and into the technical, financial, and geopolitical realities that shape global mineral supply chains.

When big ASX news breaks, our subscribers know first

What Makes a Mineral Strategic, and Why the Definition Keeps Expanding

The U.S. government defines critical minerals as nonfuel materials whose supply chains are vulnerable to disruption and whose absence would create measurable harm to economic output, national defence capability, or the functioning of clean energy infrastructure. The current list spans dozens of materials, but the highest-priority concerns cluster around several categories:

- Rare earth elements (REEs): Particularly heavy rare earths like dysprosium and terbium, which are irreplaceable in the permanent magnets used across defence systems, EV motors, and wind turbines

- Battery metals: Lithium, cobalt, nickel, and manganese, which underpin electric vehicle and grid storage chemistries

- Semiconductor and electronics inputs: Gallium, germanium, and indium, used in compound semiconductors and advanced displays

- Structural and specialty materials: Graphite (as anode material), antimony (in flame retardants and munitions), and fluorspar

What is less commonly understood is how dynamic this classification system actually is. As battery chemistries evolve, certain materials gain or lose strategic relevance. Sodium-ion battery development, for instance, could reduce lithium dependency over a longer horizon, while the rise of gallium nitride in power electronics has sharply elevated gallium's strategic significance. This fluidity makes long-term supply chain planning extremely difficult, because the goalposts shift with technological change.

"The designation of criticality is not a permanent badge. It reflects a snapshot of technology dependency, geopolitical exposure, and market structure at a given point in time, and those variables are in constant motion."

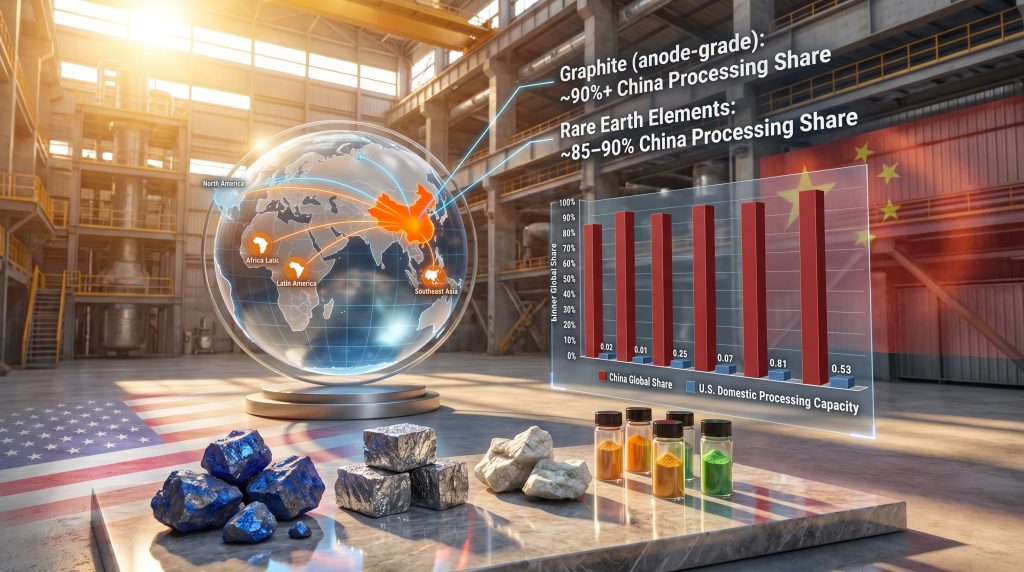

The Processing Chokepoint: Where China's Advantage Is Structural, Not Accidental

One of the most persistent misunderstandings in public discussion of America's critical mineral strategy is the conflation of mining with processing. These are entirely different industrial activities with fundamentally different capital requirements, technical barriers, and strategic implications.

The global distribution of known mineral deposits is reasonably diverse. Significant rare earth reserves exist in Australia, Brazil, India, Tanzania, Canada, and the United States itself. Lithium deposits span Argentina, Chile, Australia, and increasingly Bolivia. However, the ability to convert raw ore into battery-grade or magnet-grade refined material is concentrated to a degree that has no parallel in other industrial sectors.

| Mineral | China's Estimated Global Processing Share | Western Processing Capacity |

|---|---|---|

| Rare Earth Elements | 85–90% | Minimal, early-stage rebuilding underway |

| Graphite (anode-grade) | 90%+ | Negligible commercial capacity |

| Cobalt (refined) | 70–75% | Near-zero domestic U.S. capacity |

| Lithium (hydroxide/carbonate) | 65–70% | Nascent, several projects in development |

| Gallium and Germanium | Near-total control | Extremely limited outside China |

This dominance was not accidental. China began systematically investing in rare earth and battery material processing infrastructure in the 1980s and 1990s, accepting lower environmental and labour cost structures while Western competitors largely exited the sector. By the time Western governments recognised the strategic implications, China had accumulated decades of technical expertise, sunk capital, and established customer relationships that are extraordinarily difficult to replicate on a compressed timeline.

The distinction matters enormously for policy design. Opening a new lithium mine in Nevada or a rare earth deposit in Wyoming does not automatically create a processing pathway. Without domestic or allied refining capacity at the midstream stage, ore simply travels to China for conversion anyway. This is what analysts describe as the midstream gap, and it is arguably the single most consequential vulnerability in Western supply chain architecture. Furthermore, the challenges surrounding rare earth supply chains extend well beyond processing alone, touching on geopolitical influence, trade leverage, and long-term industrial capacity.

The Acquisition Problem: Losing the Race Before It Starts

Compounding the processing challenge is a less-discussed upstream problem: the systematic acquisition of undeveloped mineral deposits by Chinese-aligned capital across Africa, Latin America, and parts of Southeast Asia. Analysis from the Center for Strategic and International Studies has highlighted that the United States is not merely behind in domestic production but is actively losing competitive access to the world's most significant undeveloped mineral assets to foreign buyers operating with longer planning horizons and fewer political constraints.

The pattern is well documented in African rare earth and battery metal projects. Chinese state-backed entities, and increasingly private Chinese capital with implicit state coordination, have secured offtake agreements, equity stakes, and in some cases outright ownership of projects that would otherwise represent Western supply chain opportunities. Once those offtake agreements are signed, the mineral output effectively flows into Chinese supply chains regardless of where the physical mine is located.

This creates a structural dynamic where even successful Western exploration and project development can be neutralised at the commercial agreement stage if allied-nation governments and private sector actors lack competitive financing terms and the speed to execute deals before Chinese counterparts.

The Four Pillars of America's Critical Mineral Strategy: What Policy Has Been Built So Far

Pillar 1: Accelerating Domestic Production Through Regulatory Reform

The critical minerals executive order, signed in March 2025, directed federal agencies to prioritise and expedite domestic mineral production approvals. The intent was to compress permitting timelines that have historically stretched to seven to ten years for major mining projects in the United States, compared to under three years in several competing jurisdictions.

The core tension here is real and politically difficult. The National Environmental Policy Act (NEPA) review process exists for legitimate reasons, and attempts to streamline it face organised opposition from environmental groups and communities with Indigenous land rights considerations. Proposed categorical exclusions for certain mineral project types, and legislative permitting reform bills, remain contested. This is not simply bureaucratic inertia; it reflects genuine disagreement about how to weigh long-term strategic risk against near-term environmental and social impact.

Pillar 2: Federal Finance as a Risk Bridge

Private capital will not flow into greenfield critical mineral processing facilities without meaningful risk mitigation. The capital intensity of building a hydrometallurgical rare earth separation facility or a lithium hydroxide refinery from scratch, combined with long development timelines and volatile commodity prices, creates a return profile that conventional institutional investors find unattractive.

Federal instruments being deployed to bridge this gap include:

- Department of Energy Loan Programs Office (LPO): Providing debt financing for projects that cannot access commercial loans at viable rates

- Export-Import Bank: Extending project finance reach into allied-nation supply chain development

- Defense Production Act support: Enabling direct federal procurement commitments that de-risk demand for domestic processors

- Grants and equity participation mechanisms: Reducing first-mover capital risk for processing infrastructure with no commercial precedent in the U.S. market

Peer nations are deploying analogous instruments. The European Union has committed to processing fund targets exceeding one billion euros under its Critical Raw Materials Act framework. Canada and Australia have similarly mobilised public capital tools, though domestic processing scale-up remains in early stages across all Western jurisdictions.

Pillar 3: Allied Supply Chain Development Through Multilateral Frameworks

No single nation can achieve full critical mineral self-sufficiency. The strategic logic behind the Minerals Security Partnership (MSP) and bilateral frameworks such as the U.S.-Australia Critical Minerals Partnership is to aggregate allied-nation resource endowments into a coordinated supply network. This network is designed to reduce collective dependence on Chinese supply chains, with critical minerals and energy security now firmly intertwined in allied strategic planning.

The concept of friend-shoring in critical minerals is more complex than standard trade liberalisation. It requires sustained diplomatic engagement, aligned investment standards, and mechanisms to prevent partner nations from defaulting to Chinese offtake agreements when commercial terms are more attractive. Several African and Latin American nations that are nominally aligned with Western frameworks continue to sign Chinese processing and offtake deals, because Western financing alternatives arrive too slowly or carry more restrictive conditionality.

A less commonly flagged risk within this framework is that allied-nation mining output can still flow through Chinese processing infrastructure. Australian-mined lithium spodumene, for example, has historically been shipped to China for conversion to battery-grade lithium hydroxide. Until allied nations build their own midstream capacity, friend-shoring diversifies mining geography without fully addressing the processing chokepoint.

Pillar 4: Minerals as a Geopolitical and Defence Instrument

The Trump administration's framing elevated critical mineral access from an industrial policy consideration to a first-order national security priority. This framing unlocked several mechanisms:

- Application of trade tools and tariffs as leverage in mineral diplomacy negotiations

- Explicit linkage between mineral access and technology leadership in artificial intelligence hardware, hypersonic weapons systems, and next-generation energy grid infrastructure

- Increased integration of critical mineral supply chain vulnerability into Department of Defense threat assessments

- Use of the Defense Production Act to designate mineral processing as strategically equivalent to weapons manufacturing

China's January 2025 export controls on gallium, germanium, antimony, and related materials validated the strategic logic of this framing. These controls demonstrated that processing dominance translates directly into export leverage, and that the escalation pathway from trade friction to material denial is shorter than most Western planners had assumed.

Where the Strategy Falls Short: Structural Gaps That Policy Cannot Easily Close

The Timeline Realism Problem

Even under optimistic assumptions, industry specialists and policy analysts broadly agree that building meaningful domestic or allied-nation critical mineral processing capacity requires a sustained investment horizon of ten to fifteen years minimum. This estimate applies to facilities that already have identified ore feedstock, committed capital, and regulatory approvals in place. Greenfield projects starting from exploration stage face longer timelines.

This creates a fundamental mismatch with the pace of geopolitical competition. Chinese supply chain positions were built over three to four decades of sustained state investment. American policy is attempting to compress that timeline through executive action and public financing, but the physical and technical realities of building processing plants, recruiting skilled engineers, and establishing quality-certified supply relationships cannot be fully accelerated by political will alone.

Policy Fragmentation and the Absence of a Unified Framework

A persistent critique from policy analysts is that America's critical mineral strategy, while historically aggressive in the volume and pace of executive actions produced, lacks a unified, cross-agency prioritisation framework with enforceable long-term commitments. Multiple executive orders, agency programs, and congressional initiatives operate in parallel without a single coordinating authority accountable for integrated outcomes.

The contrast with China's approach is instructive. China's mineral strategy operates under centralised multi-decade planning that does not reset with each leadership transition. American policy, by contrast, has historically been vulnerable to administration-cycle reversals, where programs initiated under one administration are defunded, restructured, or deprioritised by the next. This structural vulnerability undermines the private sector confidence needed to commit long-cycle capital to processing infrastructure.

The Midstream Gap: Stranded Upstream Assets as an Emerging Risk

A scenario that has not received sufficient attention in mainstream coverage is the risk of stranded upstream assets: mines that successfully reach production but find no viable domestic or allied-nation processing pathway. If a domestic rare earth mine produces ore that must be shipped to China for separation because no alternative commercial refinery exists, the strategic benefit of domestic mining is substantially negated.

Avoiding this outcome requires that processing investment precedes or accompanies mining development, not follows it. Current policy sequencing has tended to prioritise the more politically visible activity of opening mines, while the less glamorous but more strategically critical work of building refineries lags behind. In addition, the broader challenge of surging critical minerals demand further compresses the timeline within which these infrastructure gaps must be addressed.

The next major ASX story will hit our subscribers first

Comparative Policy Architecture: How the U.S. Stacks Up Globally

| Policy Dimension | United States | European Union | Australia | Canada | China |

|---|---|---|---|---|---|

| Domestic Mining Acceleration | EO 14241, federal land access reform | Critical Raw Materials Act | State-level fast-tracking programs | Impact Assessment Act reform | State-directed expansion |

| Processing Investment | DOE LPO, Ex-Im Bank, DPA Title III | €1B+ processing fund targets | Limited domestic refining | Early-stage initiatives | Decades of state-backed capacity |

| Allied Supply Frameworks | MSP, bilateral agreements | Strategic Partnerships (Chile, Canada) | U.S.-Australia CMP | Canada-U.S. alignment | Belt and Road mineral corridors |

| Permitting Speed | Slow (NEPA reform ongoing) | Moderate (CRMA 24-month target) | Variable by state | Moderate | Fast (state-controlled) |

| Long-Term Planning Horizon | Administration-cycle dependent | 2030/2050 framework targets | 10-year resource strategies | Budget-cycle dependent | 2030–2060 strategic plans |

The most significant structural advantage China maintains is not financial but temporal: its industrial planning operates on timescales that span political cycles rather than being constrained by them. For a deeper examination of how the U.S.-Australia minerals framework addresses some of these planning gaps, the bilateral documentation offers considerable detail on aligned investment standards and processing commitments.

What Genuine Supply Chain Resilience Would Actually Require

Based on the structural analysis above, achieving meaningful independence from Chinese mineral processing dominance by any strategically relevant horizon would require several conditions to be met simultaneously:

- Sustained bipartisan political commitment across a minimum of two to three administration cycles, with protected funding mechanisms that survive partisan transitions

- Capital deployment at unprecedented scale, with industry and policy estimates pointing to a multi-hundred-billion-dollar investment requirement in processing infrastructure over the coming decade

- Permitting reform that reduces approval timelines from seven-to-ten years to under three years for priority processing and mining projects, without eliminating environmental review entirely

- Binding allied coordination that includes provisions preventing partner nations from signing Chinese offtake agreements for minerals designated under shared security frameworks

- Midstream processing prioritisation that ensures refinery investment precedes or accompanies upstream mining development rather than being deferred to a later stage

The investment gap in critical mineral processing infrastructure is not measured in billions but in multiples of hundreds of billions. Private capital at this scale requires de-risking mechanisms well beyond what current federal programs provide. Royalty streaming structures, government-backed offtake guarantees, and blended public-private finance vehicles represent the most credible pathways to unlocking institutional investment at the required volume.

Frequently Asked Questions: America's Critical Mineral Strategy

What is America's critical mineral strategy?

America's critical mineral strategy is a multi-pillar federal policy framework designed to reduce U.S. vulnerability to supply disruptions in minerals essential to defence manufacturing, technology hardware, and clean energy infrastructure. It combines domestic production reform, public financing tools, multilateral allied supply chain development, and the application of trade mechanisms to address structural dependencies on Chinese-controlled processing capacity.

Why does China dominate critical mineral processing?

China's processing dominance reflects decades of deliberate, state-directed industrial investment that began in the 1980s, when Western producers largely withdrew from the sector due to lower cost competition and declining commodity prices. The result is accumulated technical expertise, physical infrastructure, and supply relationships that took thirty to forty years to build and cannot be replicated on a short timeline.

What executive orders have shaped U.S. critical mineral policy?

Executive Order 14241 (March 2025) directed federal agencies to prioritise and accelerate domestic mineral production and processing approvals. A subsequent executive order in January 2026 targeted specifically processed critical minerals and their derivative products, reflecting recognition that mining without processing does not resolve the core strategic vulnerability.

What is the Minerals Security Partnership?

The Minerals Security Partnership is a multilateral framework involving the United States and a group of allied nations designed to coordinate public and private investment in critical mineral supply chains outside of China. Its goal is to diversify the global supply base by mobilising capital into mining and processing projects in partner countries, consequently reducing collective Western dependence on Chinese-controlled supply chains.

How long will it take to reduce U.S. critical mineral dependency?

Under optimistic assumptions involving sustained political commitment, adequate capital deployment, and successful permitting reform, industry analysts broadly estimate that meaningful domestic and allied-nation processing capacity could begin to materialise within ten to fifteen years. Full supply chain resilience across all critical mineral categories would require a considerably longer horizon.

Which minerals carry the highest strategic risk?

Heavy rare earth elements, particularly dysprosium and terbium used in defence-grade permanent magnets, carry the highest near-term strategic risk due to near-total Chinese processing control and no viable short-term substitute. Gallium and germanium, now subject to Chinese export controls, represent escalating risks in the semiconductor supply chain. Graphite for battery anodes and cobalt for battery cathodes also carry significant exposure.

The Road Ahead: Three Conditions That Will Define Whether the Strategy Succeeds

The trajectory of America's critical mineral strategy ultimately depends on three variables that are interconnected and mutually reinforcing.

Political continuity is the foundational condition. Without bipartisan consensus that critical mineral supply chain resilience is a generational priority rather than an administration-specific agenda, the investment frameworks being built today remain vulnerable to defunding or restructuring with the next change in government.

Capital mobilisation at scale is the operational condition. Policy frameworks without sufficient capital deployment are strategic documents rather than strategic realities. Closing the multi-hundred-billion-dollar processing infrastructure gap requires financial instruments that make long-cycle mineral investment commercially attractive to institutional capital, pension funds, and strategic industrial investors.

Allied coordination depth is the systemic condition. Individual nation strategies, no matter how well designed, cannot replicate the integrated supply chain architecture that China has built through coordinated state investment. Only a genuine coalition of allied nations with aligned permitting standards, shared investment frameworks, and binding commercial coordination can create a credible alternative supply ecosystem.

The broader stakes extend well beyond the mining sector. Critical mineral access is now understood by the U.S. Department of Defense as a precondition for maintaining technological leadership in artificial intelligence hardware, advanced propulsion systems, and next-generation communications infrastructure. The geopolitical signal sent by continued Chinese acquisition of global mineral assets, and by continued Western delay in building processing capacity, is not a signal that can be corrected quickly once it hardens into established supply relationships and sunk capital.

The window for effective action is open, but it will not remain so indefinitely.

Disclaimer: This article presents analytical perspectives on publicly available policy frameworks and industry data for informational purposes only. It does not constitute financial, investment, or legal advice. Forecasts and scenario projections involve inherent uncertainty and should not be relied upon as predictions of future outcomes. Readers should conduct independent research before making any investment or policy-related decisions.

Want to Stay Ahead of the Next Major Mineral Discovery on the ASX?

As geopolitical competition over critical minerals intensifies, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly translating complex data across 30+ commodities into clear, actionable insights for traders and investors at every level. Explore historic discoveries and the exceptional returns they generated, then begin your 14-day free trial at Discovery Alert to position yourself ahead of the market.