June 4, 2026

The Intelligence Deficit at the Heart of Global Rare Earth Markets

For decades, the rare earth elements sector has operated with a peculiar asymmetry: nations that consume the most have known the least about what is actually happening inside the rare earth supply chains they depend on. Market participants from buyers to policymakers have historically relied on quarterly reports, trade flow data released weeks or months after the fact, and fragmented industry commentary.

In a commodity class where a single export restriction or processing bottleneck can send magnet-grade material prices surging by double digits within weeks, this intelligence lag is not merely inconvenient. It is a structural vulnerability.

India's position within this dynamic has been particularly exposed. As one of the world's fastest-growing consumers of rare earth permanent magnets, and a country with significant stated ambitions across electric vehicle manufacturing, renewable energy deployment, and advanced defence procurement, India has been operating with limited visibility into the very supply chains its industrial future depends on. The GMDC Cambridge rare earth observatory represents a direct institutional response to this gap.

When big ASX news breaks, our subscribers know first

Understanding the Rare Earth Elements Landscape Before the Observatory

What Makes Rare Earth Elements Strategically Irreplaceable

Rare earth elements are a group of 17 metallic elements that include the lanthanide series alongside scandium and yttrium. Despite the word "rare" in their name, most REEs are relatively abundant in the Earth's crust. What makes them genuinely scarce is the concentration of economically viable deposits in a small number of locations, and more critically, the extreme geographic concentration of processing and separation infrastructure.

Several characteristics make REEs uniquely difficult to substitute in high-performance applications:

- Neodymium and praseodymium form the basis of neodymium-iron-boron (NdFeB) permanent magnets, which generate superior magnetic flux density compared to any alternative magnet technology currently at commercial scale

- Dysprosium and terbium are added to NdFeB magnets to maintain coercivity (resistance to demagnetisation) at elevated operating temperatures, a property critical in EV traction motors and aerospace systems

- Lanthanum and cerium, while lower in value, serve as essential inputs in fluid catalytic cracking for petroleum refining and in polishing compounds for semiconductor and optical manufacturing

- Europium, terbium, and yttrium have historically been essential in phosphor applications for lighting and display technologies

The challenge is not simply mining these materials. Rare earth ore bodies are typically low-grade and mineralogically complex. Separation requires a multi-stage solvent extraction process that is technically demanding, chemically intensive, and environmentally sensitive. This processing complexity is precisely why the overwhelming majority of global rare earth separation capacity remains concentrated in a single country. Indeed, the rare earth processing challenges involved at this stage represent one of the sector's most persistent structural bottlenecks.

The Supply Concentration Problem in Numbers

| Supply Chain Stage | Dominant Geography | Approximate Share of Global Capacity |

|---|---|---|

| Rare earth mining | China | ~60% of global mine output |

| Rare earth separation/processing | China | ~85-90% of global capacity |

| NdFeB magnet manufacturing | China | ~90% of global output |

| Dysprosium and terbium refining | China | Near-total dominance |

This concentration means that disruptions at any stage of the Chinese rare earth processing chain reverberate instantly across global industrial supply chains. Export quota changes, environmental compliance crackdowns on Chinese separation facilities, or geopolitically motivated trade restrictions can create price spikes that cascade from raw ore through to finished motor assemblies within weeks. Furthermore, China's rare earth strategy has increasingly been wielded as a geopolitical lever, adding another dimension of risk for import-dependent nations.

The separation of heavy rare earth elements such as dysprosium and terbium is particularly capital-intensive and technically demanding. Outside of China, only a handful of facilities globally are capable of producing commercial-scale separated heavy rare earth oxides, meaning supply chain diversification in this segment remains years away even under optimistic investment scenarios.

The GMDC Cambridge Rare Earth Observatory: Architecture and Ambition

What the Platform Is Designed to Do

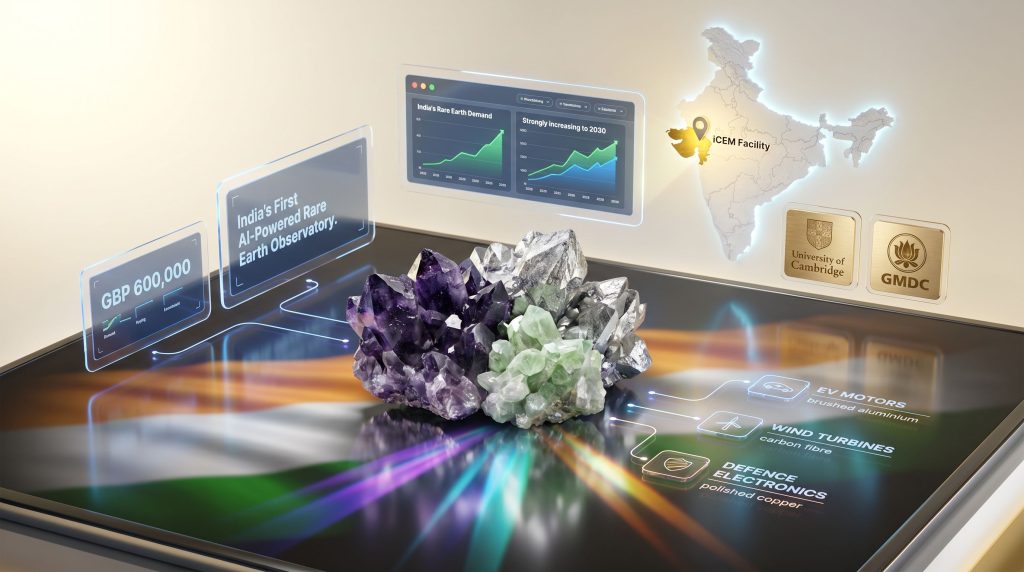

The GMDC Cambridge rare earth observatory is structured as India's first AI-powered monitoring platform covering the entire rare earth value chain. The initiative brings together Gujarat Mineral Development Corporation (GMDC) and the University of Cambridge's Institute for Manufacturing (IfM), combining institutional mining sector expertise with world-class supply chain analytics research capability.

The observatory will be housed at GMDC's International Centre of Excellence in Mining (iCEM) in Gujarat, operating over a two-year development horizon with a total investment commitment of GBP 600,000 (approximately USD 805,965).

The platform's monitoring mandate covers the following intelligence domains:

| Intelligence Domain | Scope of Monitoring |

|---|---|

| Rare earth pricing | Global spot and contract price movements across key REE categories |

| Processing capacity | Global and regional refining and separation capacity utilisation |

| Supply chain disruptions | Mining output interruptions, export restrictions, and logistics bottlenecks |

| Geopolitical risk signals | Policy shifts, trade restrictions, and bilateral mineral agreements |

| Downstream demand signals | EV, renewables, electronics, and defence sector consumption trends |

Why AI Architecture Is Specifically Required Here

The rare earth market generates an extraordinary volume of relevant signals simultaneously. Spot price movements, shipping data, plant utilisation announcements, export licensing changes, junior mining company exploration results, battery chemistry research publications, and government procurement tender releases all carry varying degrees of intelligence value. No conventional analytical team can process this data volume in real time.

The AI-powered architecture of the observatory is designed to address this challenge through several mechanisms:

- Automated data ingestion across structured sources (price databases, trade statistics, capacity registries) and unstructured sources (news feeds, regulatory filings, research publications)

- Pattern recognition to identify early signals of supply disruptions before they manifest in price movements

- Demand-side modelling integrating EV sales data, renewable energy capacity additions, and defence procurement signals to project forward demand trajectories

- Geopolitical risk scoring to contextualise policy announcements from major REE-producing and processing jurisdictions

- Policy-ready output generation translating raw market signals into decision-relevant intelligence for procurement teams and government advisers

GMDC and Cambridge: Why This Partnership Carries Weight

GMDC's Strategic Repositioning

Gujarat Mineral Development Corporation has historically been associated with lignite extraction and industrial minerals across Gujarat. The organisation's pivot toward critical minerals reflects a broader recognition within India's state-owned enterprise sector that the energy transition is fundamentally reshaping which mineral assets carry long-term strategic value.

GMDC's International Centre of Excellence in Mining (iCEM) represents the institutional infrastructure through which this repositioning is being executed. The observatory's placement within iCEM signals that the organisation views rare earth intelligence as a foundational capability, not an ancillary research exercise.

Separately, GMDC has entered into a collaboration with NMDC to jointly develop opportunities spanning the full rare earth value chain, from exploration and mine development through ore processing and downstream manufacturing. This vertical ambition contextualises the observatory's role: intelligence infrastructure designed to support a planned end-to-end industrial capability, not simply a market-watching exercise.

Cambridge's Institute for Manufacturing: Technical Credibility

The IfM at Cambridge has built a substantial research reputation in industrial systems, manufacturing strategy, and supply chain resilience. Its involvement in the observatory lends both methodological rigour and international credibility to the platform's analytical outputs. Crucially, the IfM's network of industrial and academic relationships provides access to data partnerships and research collaborations that would be difficult for a standalone government enterprise to replicate independently.

India's Rare Earth Demand Trajectory: The Numbers Behind the Urgency

India's demand for rare earth permanent magnets is projected to grow substantially through 2030, driven by intersecting demand vectors across multiple sectors.

Sector-by-Sector Demand Breakdown

| Application Sector | REE Dependency | India Demand Trajectory to 2030 |

|---|---|---|

| Electric vehicles | High (NdFeB traction magnets) | Strongly increasing |

| Wind energy | High (direct-drive turbine generators) | Increasing with capacity targets |

| Consumer electronics | Moderate | Stable to moderate growth |

| Defence systems | High (sensors, guidance, communications) | Strategically sensitive |

| Industrial motors and HVAC | Moderate | Steady growth |

The EV Magnet Demand Dynamic

Each NdFeB traction motor in a battery electric vehicle typically contains between 1 and 3 kilograms of rare earth permanent magnet material, depending on motor architecture and vehicle size. As India scales domestic EV manufacturing, the cumulative demand for magnet-grade neodymium, praseodymium, dysprosium, and terbium increases in direct proportion to production volumes.

Critically, not all rare earth magnet grades are interchangeable. High-performance EV traction applications require sintered NdFeB magnets with precisely controlled heavy rare earth additions to maintain coercivity at operating temperatures that can exceed 150 degrees Celsius. This specification sensitivity means Indian manufacturers cannot simply source from the nearest available supplier without risking motor performance degradation.

A less widely appreciated dynamic in the NdFeB magnet supply chain is the role of recycling and secondary supply. Currently, less than 1% of rare earth elements are recovered from end-of-life products at commercial scale globally. As magnet-containing products reach end-of-life in larger volumes over the next decade, the urban mining potential of rare earths from e-waste and retired EV motors could become a meaningful secondary supply source. An intelligence platform capable of tracking this emerging supply vector would consequently have significant forward value.

Renewable Energy and the Wind Turbine Variable

Direct-drive offshore wind turbines represent one of the most REE-intensive renewable energy technologies. A single large offshore wind turbine generator can contain more than 600 kilograms of rare earth permanent magnet material. As India pursues offshore wind development alongside its onshore renewable capacity expansion, the volume of rare earth materials required for the energy system build-out alone represents a substantial and time-sensitive procurement challenge.

Filling the Intelligence Gap: How the Observatory Compares to Existing Tools

| Feature | Conventional Market Reports | Government Trade Data | GMDC Cambridge Observatory |

|---|---|---|---|

| Update frequency | Quarterly or annual | Monthly or quarterly | Real-time (AI-enabled) |

| Value chain coverage | Partial | Trade flows only | Full upstream to downstream |

| AI-driven analytics | No | No | Core architecture |

| Policy-ready outputs | Limited | Limited | Explicitly designed |

| India-specific contextualisation | Minimal | Partial | Core mandate |

| Geopolitical risk integration | Occasional | Absent | Systematic |

The competitive differentiation of the observatory is clearest in two areas. First, the real-time update capability closes the intelligence lag that has historically left Indian policymakers and procurement teams reacting to price movements rather than anticipating them. Second, the India-specific contextualisation of global market data addresses a persistent gap in commercially available rare earth market intelligence, which has typically been produced for Western European or North American audiences with different supply chain structures and procurement priorities. In addition, efforts towards rare earth supply chain diversification globally underscore why India needs its own sovereign intelligence capability rather than relying on externally produced analysis.

The next major ASX story will hit our subscribers first

Strategic Stockpiling: The Policy Use Case That Justifies the Investment

One of the observatory's most consequential potential applications is in supporting government-level decisions around strategic mineral stockpiling. Nations including Japan, the United States, and members of the European Union have demonstrated that well-timed stockpile acquisitions during price troughs can significantly reduce the fiscal cost of securing long-term supply access.

Japan's experience following the 2010 rare earth export restrictions imposed by China is particularly instructive. Japanese manufacturers and government agencies that had invested in stockpile intelligence and diversification programmes prior to the restrictions were materially better positioned to weather the subsequent price spike, during which certain rare earth oxide prices increased by factors of ten or more within a twelve-month period.

India has historically lacked a dedicated institutional mechanism for this function. If the observatory's AI architecture proves capable of identifying price inflection points with sufficient lead time, it could directly inform the timing and composition of strategic stockpile acquisitions, generating fiscal savings that substantially exceed the platform's GBP 600,000 development cost.

What Success Looks Like Over the Two-Year Development Window

Several indicators will determine whether the GMDC Cambridge rare earth observatory achieves its stated objectives:

- AI capability deployment: Whether the platform successfully operationalises real-time monitoring across the full REE value chain within the two-year timeline

- Data partnership breadth: The depth and reliability of intelligence outputs will depend heavily on the quality of data partnerships established with mining companies, processing facilities, logistics providers, and trade bodies

- Policy integration: Evidence that government procurement or stockpiling decisions are informed by observatory outputs will represent the ultimate measure of strategic impact

- Industrial adoption: Uptake among Indian industrial buyers, particularly in EV and renewable energy manufacturing, will signal whether the platform's intelligence is actionable at the commercial procurement level

- Expansion of coverage to emerging supply vectors: Whether the platform incorporates tracking of secondary supply sources, including REE recycling and urban mining, will determine its long-term forward relevance

This article contains forward-looking statements and projections regarding market demand, technology development timelines, and policy outcomes. These projections are inherently uncertain and should not be construed as investment advice. Readers should conduct independent due diligence before making decisions based on information contained herein.

Want to Capitalise on the Next Major Rare Earth Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time ASX alerts the moment significant rare earth and critical mineral discoveries are announced, translating complex geological data into actionable investment insights for traders and long-term investors alike. Explore how historic mineral discoveries have generated extraordinary returns and begin your 14-day free trial today to position yourself ahead of the broader market.