July 5, 2026

The global mining royalty landscape stands at a transformative crossroads, where traditional investment models are converging with innovative financial structures to create unprecedented opportunities for portfolio diversification. As institutional investors increasingly seek exposure to critical minerals strategy while avoiding operational risks, royalty companies have emerged as sophisticated vehicles that blend commodity price leverage with reduced capital intensity. This structural shift represents more than market evolution—it signals a fundamental reimagining of how investors can participate in resource extraction cycles.

Strategic Market Positioning Analysis

The merger between Sweetwater Royalties and Uranium Royalty Corp creates North America's most diversified critical minerals platform, combining uranium sector exposure with industrial commodity stability through dominant soda ash market positioning. This strategic consolidation addresses two fundamental market drivers: nuclear energy transition uranium demand and stable industrial commodity cash flows, whilst acknowledging the broader uranium market volatility currently affecting the sector.

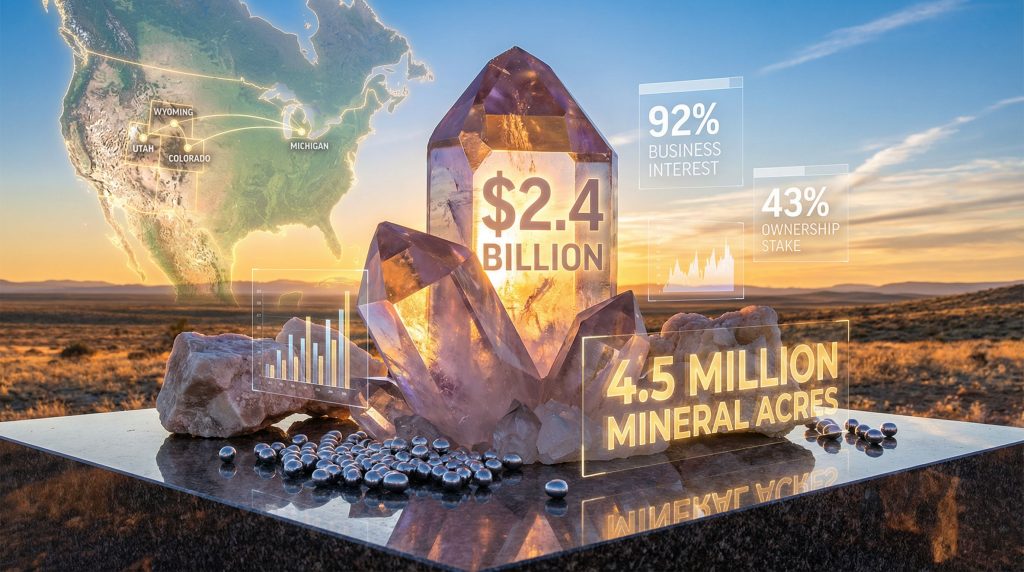

The transaction structure reveals compelling strategic metrics that position the combined entity as a market leader. With a combined enterprise value of $2.4 billion, the merger brings together 4.5 million mineral acres of Sweetwater's holdings with URC's established uranium royalty expertise across almost 30 uranium operations spanning the US, Canada, Spain, and Namibia.

Geographic Concentration and Resource Control

Sweetwater's asset portfolio demonstrates exceptional geographic concentration across proven geological formations. The company controls 850,000 surface acres across Wyoming, Utah, and Colorado, plus 450,000 mineral acres in Upper Michigan. Most significantly, Sweetwater owns approximately 50% of the world's largest known trona deposit, representing roughly 90% of global known trona resources.

This resource concentration provides substantial competitive advantages. Trona serves as the primary feedstock for soda ash production, a critical industrial material used in glassmaking, chemical manufacturing, paper production, and detergent formulation. The scarcity of global trona deposits creates natural barriers to entry and pricing power for existing producers.

URC's complementary positioning as what industry sources describe as "the world's only pure-play uranium royalty company" adds cyclical commodity exposure to Sweetwater's stable industrial mineral base. This combination creates revenue stream diversification that theoretically smooths cash flow volatility across different commodity cycles.

Revenue Generation Framework

The merged entity employs a capital-efficient royalty model that generates income through mineral rights leasing rather than direct mining operations. Sweetwater generates royalty income by leasing its surface and mineral estates for development, providing leveraged commodity exposure while avoiding operational capital requirements, labour management, and environmental liabilities.

This approach offers several strategic advantages:

- Reduced Capital Intensity: No requirement for mining equipment, processing facilities, or operational infrastructure

- Diversified Operator Risk: Multiple lessees across different projects reduce dependence on single operators

- Scalable Revenue Model: Additional acreage can be leased without proportional cost increases

- Commodity Price Leverage: Royalty rates typically tied to commodity prices or production volumes

When big ASX news breaks, our subscribers know first

Operational Synergy Framework

The combination creates operational value through complementary asset portfolios that address different segments of the critical minerals value chain. URC's uranium expertise pairs with Sweetwater's industrial minerals platform to create a diversified royalty company positioned across multiple commodity cycles, reflecting broader mining industry evolution trends.

Geographic Synergies and Infrastructure Advantages

Sweetwater's extensive acreage position across Wyoming, Utah, Colorado, and Upper Michigan provides multiple operational advantages. Wyoming hosts the world's largest trona deposit, while Colorado and Utah offer additional mineral exploration potential in proven geological formations. This geographic concentration enables:

- Shared Infrastructure Utilisation: Proximity to established mining operations and transportation networks

- Regional Expertise Development: Concentrated knowledge of local geology, regulations, and operator relationships

- Cost Optimisation: Reduced administrative and oversight costs through geographic clustering

- Exploration Synergies: Potential for discovering additional mineral resources across contiguous acreage

Revenue Stream Diversification Benefits

The merger creates a multi-commodity platform balancing cyclical and non-cyclical revenue streams:

Uranium Exposure (Cyclical):

- Nuclear energy growth potential driving long-term demand

- Supply deficit conditions creating favourable pricing environment

- Geopolitical factors increasing focus on domestic uranium sources

- Capital investment cycles potentially increasing royalty values

Soda Ash Revenue (Stable):

- Consistent industrial demand from glass, chemical, and detergent industries

- Limited global supply sources creating pricing stability

- Long-term production agreements providing revenue visibility

- Mature end markets with predictable consumption patterns

Surface Rights Opportunities:

- Renewable energy lease potential across 850,000 surface acres

- Infrastructure development rights providing additional income streams

- Agricultural and commercial leasing opportunities

Operational Risk Mitigation

The royalty structure provides inherent operational advantages compared to direct mining operations. By leasing mineral rights to experienced operators, the combined entity avoids:

- Operational Execution Risk: No direct responsibility for mine development or production

- Labour Management: No workforce requirements or labour relations issues

- Environmental Liability: Limited environmental remediation responsibilities

- Capital Market Risk: No requirement for project financing or equipment procurement

Capital Structure and Ownership Analysis

The transaction structure reflects sophisticated financial engineering designed to optimise value creation for all stakeholders while positioning the combined entity for future growth opportunities, exemplifying current industry consolidation trends.

Transaction Mechanics and Valuation Framework

| Transaction Component | Value (USD) | Ownership Structure |

|---|---|---|

| Combined Enterprise Value | $2.4 billion | Total combined entity |

| Sweetwater Enterprise Value | $1.9 billion | 100% basis valuation |

| Attributable Equity Transfer | $1.1 billion | 92% business interest |

| Orion Cash Consideration | $240 million | Immediate liquidity |

| Orion Retained Equity | $592 million | 43% ownership stake |

The transaction values Sweetwater at $1.9 billion on a 100% enterprise value basis, with an equity value of $1.1 billion for the 92% business interest transferring to URC. Orion Resource Partners will receive approximately $832 million total consideration, comprising $240 million in cash and the balance in retained shares.

Ownership Evolution and Value Creation

This transaction represents Orion's third monetisation event since establishing Sweetwater in 2020, demonstrating progressive value creation through strategic development:

- March 2023: Sale of 25% stake at initial valuation

- April 2024: Sale of 8% interest at higher valuation

- Current Transaction: 67% remaining stake merger at $2.4 billion combined entity value

This progression illustrates successful portfolio company development, with each transaction occurring at incrementally higher valuations as asset value and market positioning improved.

Post-Transaction Structure and Governance

Following completion, Orion will become the largest shareholder with 43% ownership in the combined entity. The new structure establishes a US-domiciled parent company designed for Nasdaq listing, providing several strategic advantages:

- Enhanced Institutional Access: US listing improves accessibility for American institutional investors

- Simplified Corporate Structure: Single primary listing reduces regulatory complexity

- Currency Alignment: Dollar-denominated structure matches underlying asset currencies

- Governance Optimisation: Streamlined decision-making through consolidated structure

Market Timing and Industry Context

The merger occurs during a period of significant transformation in global commodity markets, with supply deficit conditions in uranium coinciding with stable industrial demand for soda ash. This timing provides strategic advantages for a diversified royalty platform, particularly given the importance of commodity price hedging strategies in current market conditions.

Uranium Market Dynamics and Investment Drivers

URC President and Director Scott Melbye emphasised current market conditions, stating that "the global uranium market is experiencing a meaningful primary supply deficit, expected to drive significant capital investment in the years ahead." This supply-demand imbalance creates several investment thesis components:

- Primary Supply Deficit: Global production insufficient to meet reactor requirements

- Capital Investment Cycle: Anticipated increases in uranium project development spending

- Nuclear Energy Renaissance: Policy support for nuclear power as clean energy source

- Geopolitical Considerations: Focus on domestic uranium sources reducing import dependence

Industrial Minerals Market Stability

Soda ash markets provide countercyclical stability to uranium's volatility. Industrial applications in glassmaking, chemical production, paper manufacturing, and detergent formulation create consistent demand patterns less sensitive to economic cycles.

Sweetwater's dominant position in global trona resources provides several competitive advantages:

- Resource Scarcity: Limited global trona deposits create natural supply constraints

- Geographic Concentration: Wyoming deposits represent majority of world's accessible reserves

- Processing Advantages: Trona-based soda ash production more cost-efficient than synthetic alternatives

- Long-Term Contracts: Industrial customers typically enter multi-year supply agreements

Strategic Asset Assembly Timeline

Orion Partner and Sweetwater Chairperson Jon Lamb explained the strategic rationale, noting that when Sweetwater was created in 2020, "Orion recognised the opportunity to combine the strength of assets in the soda ash sector with mineral rights and land ownership to build a differentiated mining royalties platform."

This six-year development process demonstrates the extended timeline required for assembling world-class mineral royalty portfolios through strategic acquisitions and organic development.

Growth Strategy Scenarios

The combined entity's extensive acreage position and established market relationships create multiple pathways for organic and acquisition-driven growth across different commodity sectors.

Organic Growth Through Asset Optimisation

Sweetwater's substantial land holdings provide numerous development opportunities that could unlock additional revenue streams without requiring major capital investments:

Soda Ash Capacity Expansions:

- Planned capacity increases on existing trona deposits

- Additional processing facility development by lessees

- Enhanced extraction techniques improving recovery rates

- Extended mine life through deeper deposit development

Renewable Energy Lease Development:

The combination of 850,000 surface acres across Wyoming, Utah, and Colorado positions the entity to capitalise on renewable energy development trends. These states offer excellent wind and solar resources, creating opportunities for:

- Wind farm development leases across Wyoming's windy corridors

- Solar energy projects in Utah and Colorado's high-altitude, sunny regions

- Energy storage facility siting on strategically located acreage

- Transmission line easements connecting renewable projects to grid infrastructure

Mineral Exploration Programmes:

URC's uranium expertise combined with Sweetwater's extensive mineral rights creates exploration synergies:

- Systematic uranium exploration across 4.5 million mineral acres

- Advanced geological surveys identifying additional mineral resources

- Joint venture exploration partnerships with major mining companies

- Technology-driven exploration reducing discovery costs and timelines

Acquisition-Driven Consolidation Strategy

The combined entity's enhanced scale and financial capacity enables strategic acquisitions to expand geographic footprint and commodity exposure:

Target Acquisition Categories:

- Smaller royalty companies with complementary asset portfolios

- Additional mineral rights in proven geological formations

- Strategic surface rights providing infrastructure development opportunities

- Speciality royalty assets in critical minerals (lithium, rare earth elements)

Geographic Expansion Opportunities:

- Canadian uranium and base metal royalties complementing North American focus

- International diversification through established mining jurisdictions

- Adjacent US states with similar geological characteristics

Strategic Partnership Development

The merger creates opportunities for value-enhancing partnerships that leverage the combined entity's asset base and market position:

Operator Partnerships:

- Long-term development agreements with major mining companies

- Technology partnerships for enhanced resource extraction

- Infrastructure sharing agreements reducing operator costs

- Joint marketing arrangements for industrial mineral products

Financial Partnerships:

- Streaming agreements providing upfront capital for expansion projects

- Joint venture structures for large-scale development projects

- Strategic investments in complementary technologies or companies

Risk Assessment Matrix

The combined entity faces various risk factors that could impact financial performance and strategic execution, though the royalty structure provides inherent risk mitigation compared to direct mining operations.

Commodity Price Volatility Risk

| Risk Factor | Probability | Impact Level | Mitigation Strategy |

|---|---|---|---|

| Uranium Price Decline | Medium | High | Diversified revenue streams |

| Soda Ash Price Pressure | Low | Medium | Limited global supply sources |

| Industrial Demand Reduction | Low | Medium | Essential industrial applications |

Uranium Market Volatility:

Uranium prices demonstrate significant cyclical volatility driven by nuclear policy changes, reactor construction schedules, and geopolitical developments. However, current supply deficit conditions and increasing nuclear energy focus provide supportive fundamentals.

Soda Ash Market Stability:

Industrial soda ash demand shows lower volatility due to essential applications in glass manufacturing and chemical processes. The limited number of global trona deposits provides natural supply constraints supporting price stability.

Regulatory and Political Risk

Permitting and Environmental Regulation:

Mining operations face increasing environmental scrutiny and regulatory compliance requirements. The royalty structure limits direct exposure, as lessees bear primary responsibility for permitting and environmental compliance.

Nuclear Policy Changes:

Government nuclear energy policies significantly impact uranium demand. However, increasing focus on clean energy and grid reliability supports long-term nuclear power utilisation.

Critical Minerals Policy:

Government classification of certain minerals as "critical" or "strategic" can create policy support but also regulatory oversight that may impact development timelines.

Operational and Market Risk

Lessee Performance Risk:

The royalty model depends on lessees' operational success and financial stability. Diversification across multiple operators and projects reduces concentration risk.

Market Competition:

Increased interest in royalty investments may intensify competition for quality assets and compress acquisition multiples. The combined entity's scale and established relationships provide competitive advantages.

Technology Disruption:

Alternative production methods or substitute materials could impact demand for traditional mineral resources. However, established industrial applications for both uranium and soda ash provide demand stability.

The next major ASX story will hit our subscribers first

Financial Performance Projections

The merger creates a financially robust platform combining stable soda ash royalties with uranium sector upside potential, though specific financial guidance requires management disclosure or regulatory filings not available in current source materials.

Revenue Stream Analysis

Diversified Income Sources:

The combined entity generates revenue through multiple channels providing different risk-return profiles:

- Production Royalties: Payments based on mineral extraction volumes or revenues

- Surface Lease Income: Fixed or variable payments for surface rights utilisation

- Minimum Royalty Payments: Guaranteed minimum payments regardless of production levels

- Bonus Payments: Upfront payments for lease extensions or development milestones

Cash Flow Characteristics:

Royalty revenues typically exhibit several attractive characteristics:

- High Margins: Limited ongoing costs after initial lease establishment

- Scalability: Additional acreage can generate incremental revenue with minimal cost increases

- Inflation Protection: Many royalty arrangements include price escalation provisions

- Tax Efficiency: Royalty income may qualify for favourable tax treatment

Capital Allocation Strategy

The royalty model's capital-light structure enables flexible capital allocation across multiple strategic priorities:

Growth Investment:

- Additional mineral rights acquisitions

- Exploration programmes on existing acreage

- Strategic partnerships and joint ventures

- Technology investments enhancing asset value

Shareholder Returns:

- Dividend payments from stable cash flows

- Share repurchase programmes during market dislocations

- Special dividends from exceptional performance periods

Long-Term Value Creation Potential

Several factors support long-term value appreciation:

Asset Appreciation:

Mineral rights values typically increase with commodity price appreciation and resource depletion of competing sources.

Operational Leverage:

Fixed royalty rates provide leveraged exposure to commodity price increases without proportional cost increases.

Compound Growth:

Reinvestment of cash flows into additional royalty assets creates compounding returns over extended periods.

Investor Positioning Strategy

The combined entity appeals to different investor categories seeking exposure to critical minerals through a risk-mitigated investment structure.

Growth-Oriented Investment Thesis

Leveraged Commodity Exposure:

Investors seeking exposure to uranium market recovery can participate through royalty structures without direct operational risks. Uranium supply deficit conditions and nuclear energy policy support create potential for significant price appreciation.

Critical Minerals Positioning:

Both uranium and soda ash qualify as strategically important materials for national security and industrial competitiveness. Government policy support and supply chain security initiatives could provide additional value catalysts.

Exploration Upside:

The extensive 4.5 million mineral acre position provides substantial exploration potential that could unlock additional resource discoveries and royalty opportunities.

Income-Focused Investment Appeal

Stable Cash Flow Generation:

Soda ash royalties provide consistent income from essential industrial applications less sensitive to economic cycles.

Dividend Growth Potential:

As uranium market conditions improve and soda ash capacity expands, dividend payments could increase while maintaining conservative payout ratios.

Defensive Characteristics:

The royalty structure provides downside protection during commodity downturns, as lessees bear operational costs and capital requirements.

Portfolio Diversification Benefits

Inflation Hedge:

Mineral royalties historically provide inflation protection as commodity prices and royalty rates adjust with general price levels.

Currency Hedge:

Dollar-denominated assets provide natural currency hedging for US-based investors.

Sector Diversification:

The combination of nuclear energy and industrial materials exposure provides diversification across different economic sectors and cycles.

Competitive Landscape Impact

The merger creates the largest diversified royalty platform in North America, potentially influencing industry consolidation patterns and competitive dynamics.

Market Leadership Position

The combined entity's scale and asset quality establish several competitive advantages:

Dominant Resource Control:

Ownership of approximately 50% of the world's largest trona deposit creates substantial competitive moats in soda ash markets.

Geographic Concentration:

Asset clustering in Wyoming, Utah, Colorado, and Michigan provides operational efficiencies and regional expertise unavailable to more geographically dispersed competitors.

Operator Relationships:

Established relationships with major mining companies provide preferential access to high-quality development opportunities.

Financial Capacity:

Enhanced scale enables larger acquisitions and more sophisticated financial structures unavailable to smaller royalty companies.

Industry Consolidation Catalyst

The transaction may accelerate broader industry consolidation trends:

Scale Economics:

Demonstrated benefits of combined platforms may encourage similar mergers among smaller royalty companies seeking competitive scale.

Capital Market Access:

Larger entities attract institutional investor attention and improved capital market access, creating acquisition currency for further consolidation.

Operational Synergies:

Successful integration of complementary asset portfolios provides templates for additional industry combinations.

Competitive Response Implications

Competitors may respond to the enlarged entity through various strategic initiatives:

Defensive Consolidation:

Smaller royalty companies may seek merger partners to maintain competitive scale and market relevance.

Geographic Focus:

Competitors may concentrate on specific regions or commodities where they maintain competitive advantages.

Strategic Partnerships:

Alternative structures such as joint ventures or strategic alliances may emerge among companies unable to pursue outright mergers.

Regulatory and Approval Considerations

Transaction completion requires satisfaction of multiple regulatory and shareholder approval conditions, with closing targeted for early third quarter 2025.

Required Approval Process

URC Shareholder Approval:

The transaction requires majority approval from URC shareholders, who must evaluate the strategic merits of combining with Sweetwater's assets versus alternative strategic options.

Court Approval:

The arrangement structure requires court approval ensuring fair treatment of all shareholder classes and compliance with corporate law requirements.

Regulatory Clearances:

Stock exchange and regulatory approvals must be obtained from relevant authorities, including:

- TSX approval for URC's current listing obligations

- Nasdaq approval for the new parent company listing

- Securities regulators in relevant jurisdictions

- Antitrust clearance if applicable based on market concentration analysis

Customary Closing Conditions:

Standard transaction conditions must be satisfied, including:

- Material adverse change provisions

- Representation and warranty confirmations

- Third-party consent requirements

- Financing and capital structure finalisations

Timeline and Execution Risk

Targeted Completion Schedule:

Management targets transaction closing in early third quarter 2025, providing several months for completion of required approvals.

Integration Planning:

Successful combination requires careful integration of corporate structures, operational systems, and organisational cultures to realise projected synergies.

Market Condition Sensitivity:

Volatile commodity markets or broader economic disruption could impact shareholder approval likelihood or transaction economics.

Strategic Implications for the Mining Sector

The merger between Sweetwater Royalties and Uranium Royalty Corp represents broader trends reshaping mining industry investment patterns and capital allocation strategies across the resource sector.

Evolution of Mining Investment Models

Risk-Adjusted Returns:

The transaction demonstrates increasing investor preference for mining exposure through royalty structures that provide commodity leverage while avoiding operational execution risks.

Capital Efficiency:

Royalty models require significantly lower capital investments than direct mining operations, enabling higher returns on invested capital and reduced financing requirements.

Portfolio Diversification:

Combined platforms enable exposure across multiple commodities and geological regions through single investment vehicles, reducing concentration risk.

Critical Minerals Strategic Importance

National Security Considerations:

Both uranium and soda ash qualify as strategically important materials for national security and economic competitiveness, potentially attracting policy support.

Supply Chain Resilience:

Domestic resource control reduces import dependence and supply chain disruption risks during geopolitical tensions.

Infrastructure Investment:

Government infrastructure spending and industrial policy initiatives may increase demand for both nuclear energy and industrial materials.

Future Industry Structure

Consolidation Acceleration:

The successful combination of complementary royalty platforms may encourage similar transactions among smaller mining finance companies seeking scale advantages.

Institutional Adoption:

Larger, more diversified royalty companies may attract increased institutional investor allocation as alternative asset classes mature.

Innovation Integration:

Combined entities possess enhanced resources for technology adoption and innovation that could improve resource extraction efficiency and environmental performance.

The merger between Sweetwater Royalties and Uranium Royalty Corp represents a fundamental shift in mining industry capital formation, creating a diversified platform positioned to benefit from critical minerals demand growth whilst providing investors with risk-mitigated commodity exposure. As the transaction progresses toward completion, its success may serve as a template for additional industry consolidation and evolution of mining investment strategies.

Investment decisions should be based on comprehensive analysis of publicly available information and professional financial advice. Commodity investments carry substantial risks, and past performance does not guarantee future results.

Looking to capitalise on critical mineral discoveries before the market reacts?

Discovery Alert's proprietary Discovery IQ model delivers instant notifications on significant ASX mineral discoveries, transforming complex mining data into actionable investment opportunities for both short-term traders and long-term portfolio builders. Explore the historic performance of major mineral discoveries and begin your 14-day free trial today to secure your competitive advantage in mining investment opportunities.