June 16, 2026

The Geology of Timing: Why Identifying a Commodity Supercycle in Real Time Is Nearly Impossible

Every major commodity supercycle in modern history has shared one uncomfortable characteristic: the participants living through it rarely agreed it was happening until years after it had begun. The 2000s iron ore boom, which transformed Australia's fiscal landscape and reshaped global trade flows, was debated as a temporary price spike for years before analysts reached consensus that something structurally different was underway. The critical minerals supercycle debate unfolding today carries the same hallmarks of gradual emergence, expert disagreement, and inconvenient data cutting in multiple directions simultaneously.

Understanding whether the current surge in critical minerals demand for copper, lithium, cobalt, nickel, graphite, and rare earth elements constitutes a genuine supercycle, rather than an extended cyclical rally, is not an academic exercise. It shapes capital allocation decisions worth hundreds of billions of dollars, informs national strategic policy, and determines which mining jurisdictions capture generational wealth creation versus which ones watch the opportunity pass.

When big ASX news breaks, our subscribers know first

What Separates a Supercycle From an Ordinary Price Rally?

The distinction matters enormously, yet the definition itself remains contested. A standard commodity price rally reflects temporary supply shortages, speculative positioning, or short-term demand spikes. A supercycle, by contrast, reflects a fundamental and sustained realignment of the global economy's underlying material requirements, one that persists across multiple years and reshapes entire industrial supply chains.

Two diagnostic benchmarks have emerged from academic and professional commodity analysis as necessary conditions for supercycle classification:

- Scale: Year-on-year price increases of between 25 and 50 percent, sustained across consecutive years rather than confined to a single spike event.

- Duration: Elevated price conditions persisting for a minimum of three to five years, with ten-year cycles representing the analytical gold standard for confident classification.

Professor Michael Tamvakis of Bayes Business School identifies timing as the central challenge in supercycle identification, noting that while the scale of price increases is observable in real time, the duration requirement means analysts are perpetually working with incomplete data. Price levels need to hold for at least three years before the signal becomes meaningful, and five years provides a considerably more reliable confirmation threshold.

How Long Does a True Supercycle Last?

Mineral economist Professor Allan Trench of the University of Western Australia favours an even more demanding framework, suggesting that a genuine supercycle follows a decade-long upswing followed by a decade-long correction, implying a full 20-year cycle structure. This stricter definition would mean that even a five-year period of elevated prices might represent only an extended boom rather than a true supercycle.

The methodological disagreement between these two frameworks is itself analytically significant: it confirms that supercycle classification is not a standardised discipline with universal acceptance, but rather a judgement call made under uncertainty.

The "boiling frog" dynamic captures the practical problem precisely. Because supercycles emerge gradually through accumulating structural changes rather than through sudden dramatic shifts, participants embedded in the industry often cannot perceive the transition until it is well advanced. This is why supercycle classification has historically been retrospective rather than prospective.

Australia's Last Supercycle: The China Benchmark and Why It Matters

To calibrate the current critical minerals supercycle debate, the China infrastructure boom of the early 2000s provides the clearest modern reference point for Australian mining. Between 1999 and 2011, Australian iron ore exports grew from 26 million tonnes to 305 million tonnes, representing an increase of over 1,000 percent across twelve years. By any definition, this qualified as a supercycle: scale was present, duration exceeded a decade, and the structural driver was unambiguous.

That boom had a defining characteristic that simplified its analysis in retrospect: it was a single-driver supercycle. One country, one infrastructure programme, one commodity class. When China's construction activity eventually moderated, the cycle's endpoint became identifiable.

Why the Current Cycle Is Structurally Different

The current critical minerals surge is structurally different in ways that cut in both bullish and cautionary directions. Rather than a single demand engine, analysts identify at least four simultaneous megatrends driving mineral consumption:

- Global electrification and the renewable energy buildout across solar, wind, and storage infrastructure.

- Electric vehicle fleet expansion, following an S-curve technology adoption pattern with acceleration concentrated between 2025 and 2035.

- Artificial intelligence data centre construction, representing a demand layer for copper, tantalum, gallium, and rare earth hardware components that did not exist in previous commodity cycles.

- Grid modernisation programmes across North America, Europe, and Asia, involving infrastructure replacement cycles spanning 30 to 50 years.

Multi-driver demand structures are theoretically more durable than single-driver cycles because a collapse across all four vectors simultaneously is less probable than a single driver losing momentum. However, they are also considerably harder to model, and their complexity makes confident forecasting more difficult. Furthermore, the critical minerals energy transition adds an entirely new dimension of policy-driven demand that previous supercycles simply did not face.

The Numbers Behind the Critical Minerals Supercycle Debate

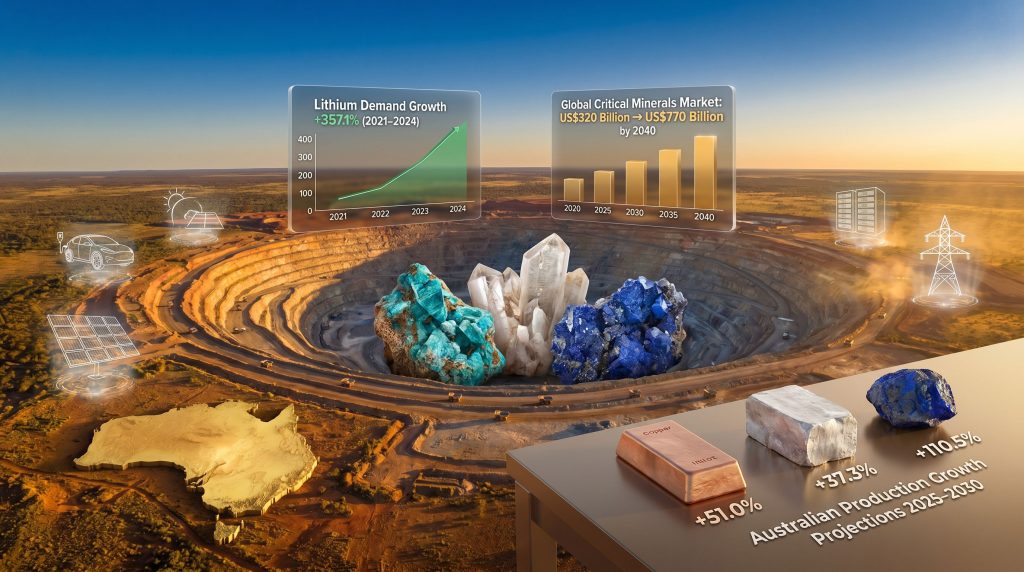

The International Energy Agency's 2025 Critical Minerals Outlook provides the most comprehensive demand data currently available for evaluating supercycle conditions. Demand growth across the 2021 to 2024 period and projected cleantech growth through 2040 are summarised below:

| Mineral | Demand Growth 2021–2024 | Projected Cleantech Demand Growth 2024–2040 |

|---|---|---|

| Copper | +28.9% | +57.2% |

| Lithium | +357.1% | +532.0% |

| Nickel | +148.7% | +323.7% |

| Cobalt | +91.8% | Not specified |

| Graphite | +209.0% | Not specified |

| Rare Earths | +72.7% | Not specified |

Source: IEA 2025 Critical Minerals Outlook

The IEA projects the global market for critical energy transition minerals will expand from US$320 billion in 2022 to US$770 billion by 2040, representing a 141 percent increase across 18 years. JP Morgan has assessed that the clean energy technology transition is actively igniting a new supercycle in critical commodities, with natural resources companies positioned as primary beneficiaries. For a deeper look at the copper investment outlook specifically, the supply-demand dynamics present a particularly compelling case.

These figures represent powerful evidence in favour of a structural demand transformation. However, they also require careful interpretation. Lithium's 357 percent demand growth between 2021 and 2024 was followed by a significant price correction in 2024 and 2025 driven by oversupply, demonstrating that individual mineral markets can diverge sharply from aggregate demand narratives even within the same structural cycle. A mineral experiencing demand growth of hundreds of percent can simultaneously experience price collapse if supply grows faster than demand.

Is the Supercycle Already Underway, or Still Contested?

The bull case rests on several structurally compelling arguments. Chronic underinvestment in new mine development during the 2015 to 2020 commodity price downturn has created a supply lag that is measured in years, not months. Given that mine development timelines typically run 10 to 15 years from initial discovery through to sustained production, the supply response to current demand growth cannot be rapid. Mines that have not been permitted today cannot contribute production this decade.

Multiple simultaneous demand vectors reduce the single-point collapse risk that characterised the end of the China boom. Even if EV adoption growth moderates, grid expansion and AI infrastructure buildout represent independent demand floors.

What Do the Sceptics Argue?

The sceptical case is equally substantive. Research from TS Lombard attributes recent commodity price strength primarily to favourable supply dynamics rather than demand-pull fundamentals. This interpretation suggests that supply disruptions, strategic undersupply by major producers, or temporary production constraints, rather than genuine structural demand exceeding available capacity, may explain a portion of recent price strength.

"The supercycle debate is not simply a bulls versus bears argument. It is a methodological disagreement about whether demand-pull or supply-push forces are the primary driver of current price behaviour, and that distinction has major implications for how long elevated prices can persist."

The broader macroeconomic context adds further complexity. Classic supercycles have historically coincided with periods of strong global economic growth and broad-based commodity demand across multiple industrial sectors simultaneously. The global economy as of mid-2026 does not exhibit the overheating conditions typically associated with textbook supercycle environments, which raises legitimate questions about whether current mineral price strength reflects true structural transformation or a more selective and potentially fragile demand pattern. According to analysis on the green demand supercycle, the energy transition is reshaping commodity demand in ways that don't neatly fit historical supercycle templates.

Geopolitics, Processing Monopolies, and the Hidden Variable in Mineral Pricing

Standard supply and demand models struggle to capture one of the most important distortions in critical minerals markets: China's dominant position in the processing and refining of most critical minerals, regardless of where ore is extracted. China controls an estimated 60 to 80 percent of global processing capacity across multiple critical mineral categories. This concentration allows state-backed producers to influence effective market supply independently of actual ore availability.

Strategic overproduction can suppress prices even during periods of genuine demand growth, obscuring signals that would otherwise confirm supercycle conditions. Conversely, strategic undersupply can create price spikes that appear to validate supercycle thesis but actually reflect deliberate supply management rather than fundamental scarcity.

Efforts by the United States, European Union, and aligned nations to rebuild critical mineral supply chains outside China's processing network, commonly described as friendshoring, represent an attempt to address this distortion. These initiatives typically involve higher cost structures than Chinese-processed equivalents, effectively introducing a geopolitical premium into long-term mineral pricing that does not appear in historical pricing models. Whether this premium sustains elevated prices long enough to satisfy supercycle duration thresholds is genuinely uncertain. In addition, a well-considered critical minerals strategy will need to account for these geopolitical premiums when modelling long-term returns.

The next major ASX story will hit our subscribers first

Artificial Intelligence as an Emerging but Uncertain Demand Layer

The inclusion of AI infrastructure as a critical minerals demand driver represents one of the most analytically novel aspects of the current critical minerals supercycle debate. GPU manufacturing and the physical construction of data centres require meaningful quantities of copper for electrical infrastructure, rare earth elements for hardware components, and tantalum and gallium for semiconductor applications. AI-driven energy consumption growth is simultaneously accelerating grid expansion requirements globally, compounding mineral demand beyond direct hardware requirements.

Some analysts have argued that AI infrastructure buildout alone could sustain a decade-long critical mineral demand cycle independent of EV adoption trajectories. This is a striking claim that requires calibration: AI mineral consumption rates remain difficult to model with precision because actual infrastructure deployment consistently lags announcement timelines, and there is genuine risk that AI demand projections are front-running capital deployment rather than reflecting realised consumption.

The important structural point, however, is that AI infrastructure represents a demand floor that did not exist in previous commodity cycles. Even if projections prove optimistic, the incremental demand contribution from global data centre expansion is both real and persistent.

Australia's Competitive Position: Strengths, Gaps, and Structural Inefficiencies

Australia's critical minerals position makes it a natural primary beneficiary of any sustained critical minerals demand cycle. The government invested AU$6.6 billion in domestic mining projects between 2019 and 2024, and the Critical Minerals Strategy 2023–2030 explicitly targets expanded downstream processing capacity to address Australia's historical weakness in value-added mineral production beyond raw extraction.

GlobalData estimates place projected Australian production growth between 2025 and 2030 as follows:

| Mineral | Projected Australian Production Growth (2025–2030) |

|---|---|

| Copper | +51.0% |

| Lithium | +37.3% |

| Cobalt | +110.5% |

Source: GlobalData estimates

Australia's lithium sector is particularly well positioned. The country maintained its status as the world's largest lithium producer in 2024, with production growing 14 percent year-on-year despite global price pressures. Cobalt reserves are substantial, with projected production growth of more than 100 percent through 2030 representing significant potential upside.

Where Are the Structural Gaps?

However, structural inefficiencies remain pronounced. The most striking is Australia's copper position. Despite holding the third-largest copper reserves globally, Australia ranked only eighth in copper production in 2024. This gap between in-ground resource endowment and actual production represents both a significant underperformance and a substantial opportunity.

The reserve-to-production disconnect reflects permitting complexity, infrastructure gaps, and the time-consuming nature of greenfield mine development rather than geological limitations. Downstream processing and manufacturing remain underdeveloped across most critical mineral categories. Australia continues to export predominantly raw materials rather than processed intermediate products or refined materials, limiting its ability to capture the full value chain. According to big funds betting on a mining supercycle, institutional capital is increasingly targeting exactly the processing and production gaps that Australia is working to close.

Key Risk Factors That Could Interrupt the Cycle

Any honest assessment of the critical minerals supercycle debate must account for the realistic scenarios under which the cycle could be interrupted or fail to materialise at supercycle scale:

- Battery chemistry substitution: Advances in sodium-ion and solid-state battery technologies could reduce demand for specific minerals, particularly lithium and cobalt. Diversified demand across multiple end-use sectors partially mitigates this risk but does not eliminate it.

- Geopolitical fragmentation: Competing friendshoring blocs may create parallel supply chains that are economically inefficient and produce regional price divergence rather than a unified global supercycle signal.

- Capital market instability: Critical minerals markets are small relative to global equity and bond markets, making them disproportionately vulnerable to capital flow disruptions. Junior mining companies face particular exposure during sharp price corrections.

- Permitting and regulatory constraints: Environmental and heritage protection requirements impose binding constraints on mine development timelines. The gap between geological potential and permitted production represents a structural ceiling on supply response speed.

Evaluating the Evidence: A Three-Condition Assessment

Applying the formal diagnostic benchmarks discussed by analysts to current conditions produces the following status assessment:

| Condition | Current Status | Assessment |

|---|---|---|

| Scale (25–50%+ annual price increases) | Met for lithium, cobalt, and graphite 2021–2024 | Partially confirmed |

| Duration (3–5+ years of elevated prices) | Cycle began approximately 2021; some minerals showing correction | Under evaluation |

| Structural driver (economy-wide transformation) | Energy transition, AI infrastructure, and defence demand confirmed | Confirmed |

The structural driver condition is the most clearly satisfied. A genuine and measurable realignment of global material requirements is underway. The scale condition has been met for several minerals during specific periods. The duration condition remains the open question, as the 2024 to 2025 corrections in lithium and nickel markets demonstrate that individual mineral prices can fall even within a broader structural demand expansion.

"Whether the current critical minerals surge ultimately earns the supercycle label may only become clear in retrospect. The more actionable question is whether Australia's strategic and operational positioning is adequate to capture the value of a structural demand transformation that is already measurably underway."

For investors, policymakers, and industry participants navigating the critical minerals supercycle debate in real time, the asymmetric risk is clear: the cost of under-positioning for a supercycle that fully materialises is considerably higher than the cost of over-positioning for one that falls short. Australia's resource endowment is exceptional. Whether the country's industrial, regulatory, and processing infrastructure can move quickly enough to match the opportunity being created by global demand transformation remains the defining question of this commodity cycle.

Disclaimer: This article contains forward-looking projections, market forecasts, and analytical assessments drawn from third-party sources including the IEA 2025 Critical Minerals Outlook, GlobalData, JP Morgan, and TS Lombard research. These projections involve material uncertainty and should not be interpreted as financial advice. Past commodity cycle performance does not guarantee future outcomes. Readers should conduct independent due diligence before making investment decisions related to critical minerals or mining sector equities.

Want to Position Yourself Ahead of the Next Major Critical Minerals Discovery?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across copper, lithium, cobalt, and beyond, instantly transforming complex mineral data into actionable investment insights for both short-term traders and long-term investors. Explore historic examples of exceptional discovery outcomes and begin your 14-day free trial today to secure a market-leading edge before the broader market catches on.