July 9, 2026

The Supply Reckoning Reshaping Modern Gold Markets

The economics of gold discovery have fundamentally changed. Where surface mines at the turn of the twentieth century routinely processed ore grading 10 grams per tonne or higher, the average operating gold mine today runs closer to 1 gram per tonne. That compression in grade, combined with roughly fifteen years of underinvestment in exploration budgets, has created a structural supply problem that no short-term price correction can resolve. Understanding that backdrop is essential context before evaluating any specific gold development story, including the case being built around Bob Quartermain on Dakota Gold and Richmond Hill.

When big ASX news breaks, our subscribers know first

Who Is Bob Quartermain and Why Does His Involvement Matter?

A Career Measured in Discoveries, Not Quarters

Few individuals in the resource sector carry the operational depth that Robert Quartermain has accumulated across nearly five decades. His career began in 1976, when gold traded at approximately $140 per ounce and the Dow Jones Industrial Average sat near 1,000 points. From those early years as a mine geologist working underground at the Lac Gold Mine in Ontario, through his involvement in the discovery of the Hemlo Gold Camp alongside David Bell, Quartermain developed a practitioner's understanding of what genuine mineralisation looks like versus what merely appears promising on surface sampling.

He went on to build Silver Standard Resources into a diversified precious metals company alongside colleagues Joe Ovanic and Ken Bengot, before founding Pretium Resources and executing one of the most consequential mine builds in recent Canadian history: the Brucejack project in northern British Columbia. Brucejack, constructed in one of the province's highest snowfall environments and requiring a 100-kilometre power line through remote terrain, was delivered from a team of four people in an office to a peak construction workforce of approximately 2,000. It subsequently sold to Newcrest Mining for around $3.5 billion, cementing Quartermain's reputation as someone who can take a geological concept all the way to a producing asset and then execute a disciplined exit.

The Order of Canada Signal

In 2025, Quartermain was named to the Order of Canada, the country's highest civilian honour. Within the context of resource investment evaluation, such recognition is not merely biographical colour. It reflects a career of sustained contribution spanning discovery, mine construction, corporate leadership, and community engagement. For investors assessing management credibility in the junior mining space, where promoter culture remains pervasive, Quartermain's leadership background provides an unusually verifiable foundation for confidence.

What Makes the Current Gold Cycle Structurally Different?

Sovereign Accumulation Has Changed the Demand Architecture

The 2011 gold bull market was, by most assessments, largely speculative in character. Retail investors flowed into exchange-traded funds, momentum traders chased price, and the rally ultimately reversed when sentiment shifted. The current cycle is being underwritten by a qualitatively different buyer: central banks. Furthermore, understanding gold as a safe haven has become increasingly important for portfolio managers navigating geopolitical uncertainty.

According to World Gold Council data, gold now represents approximately 23 to 25 percent of global central bank monetary reserves, and the metal has surpassed US Treasuries as a reserve asset category. That is a structural repositioning, not a tactical trade. The scale of central bank gold reserves has grown considerably over the past decade, reflecting a broader reassessment of dollar-denominated assets.

| Reserve Metric | Circa 2010 | Current Position (2025) |

|---|---|---|

| China Gold Reserves | ~33 million oz | 75+ million oz and rising |

| Gold Share of Central Bank Holdings | Minority position | ~23-25% of reserves |

| Gold vs. US Treasuries | Treasuries dominant | Gold has surpassed US Treasuries |

| Primary Demand Driver | Retail and speculative | Sovereign and institutional |

China's trajectory is illustrative. When Pretium began development work on Brucejack around 2010, China held approximately 33 million ounces of gold in reserves. That figure has now surpassed 75 million ounces and continues to grow. The pattern is not unique to China; numerous central banks across emerging markets have been systematically increasing gold allocations as an alternative to dollar-denominated instruments.

Institutional Capital Returning With Different Motivations

Beyond sovereign buyers, fund managers are re-entering gold positions, but with a notably different rationale than in previous cycles. Rather than speculative positioning, the current institutional interest reflects portfolio insurance logic: a desire to hold assets that are uncorrelated to geopolitical disruption and sovereign debt risk. That framing, Quartermain has observed, is more durable than momentum-driven demand because it does not evaporate when headlines change.

Daily price volatility driven by news cycles, including fluctuations around central bank policy signals or geopolitical events, should be understood as short-term noise within a longer-term structural trend that is being anchored by sovereign accumulation and institutional repositioning.

Why American Gold Production Has Become a Strategic Concern

The Homestake Closure and Its Lasting Consequences

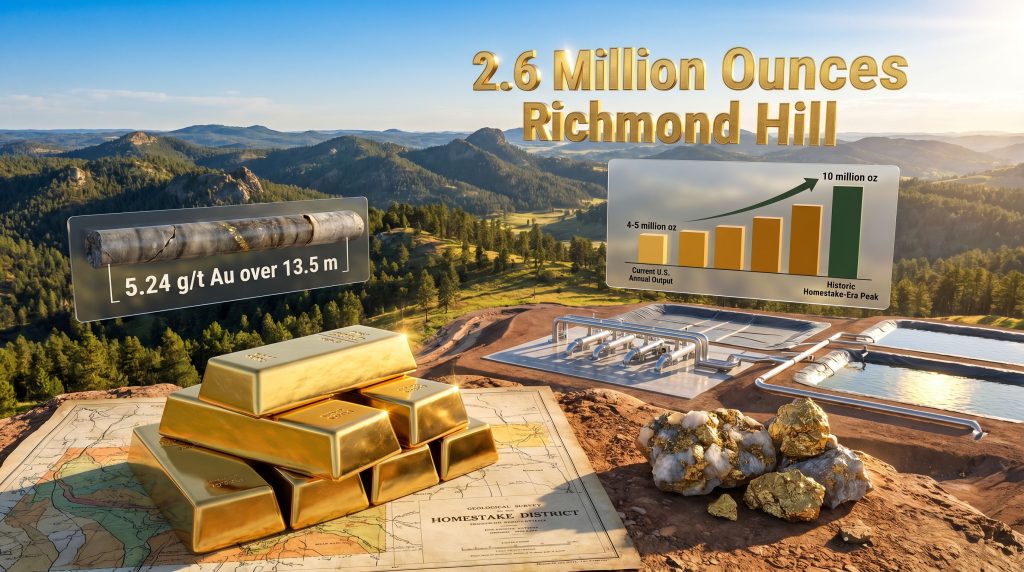

When Homestake Mining shut down operations in 2002 after more than a century of continuous production, it marked more than the end of an era for the Black Hills. It contributed to a significant contraction in US domestic gold output. At the time Homestake closed, American gold production exceeded 10 million ounces per year. Current domestic output has declined to approximately 4 to 5 million ounces annually, representing a roughly 50 percent reduction in national production capacity.

That gap sits uncomfortably against rising demand from technology manufacturing, defence applications, and industrial uses embedded in everyday consumer electronics. Gold is present in smartphones, circuit boards, aerospace components, and medical devices. Sourcing that gold domestically rather than through global supply chains subject to geopolitical disruption carries an obvious strategic logic.

Jurisdictional Risk as a Portfolio-Level Consideration

Mining investors have watched with increasing concern as governments across parts of Africa and Latin America have revised mining codes, adjusted royalty structures, or created regulatory uncertainty that diminishes asset values without warning. That pattern has concentrated capital toward jurisdictions with stable rule of law, transparent regulatory frameworks, and predictable permitting processes.

South Dakota, as an active mining state with established county-level familiarity with operating mines, represents exactly this kind of environment. The nearby Warf Mine operated by Coeur Mining has been producing gold for more than 40 years, giving local regulators and communities a functional relationship with the industry that new entrants can build on. In addition, current gold exploration trends increasingly favour established jurisdictions with predictable regulatory frameworks.

Richmond Hill: The Asset at the Centre of Dakota Gold's Thesis

Location, Geology, and Historical Context

Richmond Hill sits approximately 2 miles north of the operating Warf Mine in the Black Hills of South Dakota, within the historic Homestake District. The district has supported continuous mining activity for 145 years, and its geological endowment is well-documented. Critically, the West Ledges deposit, located along the same structural corridor, produced 6 million ounces at approximately 11 grams per tonne, providing direct validation of the district's capacity to host high-grade mineralisation at meaningful scale.

The project sits on approximately 3,000 acres of private land, which is a material differentiating factor from projects subject to federal public land permitting processes. Private land status in a mine-friendly jurisdiction compresses the permitting pathway significantly.

Resource Scale and Project Parameters

Richmond Hill's current resource base and projected operating parameters are substantial by junior developer standards.

| Project Metric | Current Position |

|---|---|

| Measured and Indicated Resource | ~2.6 million oz gold |

| Average Grade | ~0.5-0.6 g/t Au |

| Projected Annual Production | ~150,000-153,000 oz/year |

| Mine Life Projection | 17 years |

| Processing Rate | 30,000 tonnes per day |

| Processing Method | Oxide heap leach |

The oxide heap leach processing method is particularly significant from a capital intensity perspective. Unlike refractory ore deposits that require pressure oxidation or roasting circuits, oxide heap leach operations involve considerably simpler metallurgy, lower upfront capital requirements, and reduced technical execution risk. For a junior developer working to demonstrate project economics, that simplicity is a genuine competitive advantage.

The Homestake District's Geological Advantage

One underappreciated aspect of Richmond Hill's position is the information density available in the district. More than 900 historical drill holes exist across the project area, accumulated over decades of exploration activity by previous operators including Barrick Gold. When Homestake began winding down operations in 1996, the company was applying a cutoff grade of approximately 0.2 ounces per tonne, equivalent to around 6 grams per tonne, reflecting a gold price environment of $200 to $250 per ounce.

Material that was uneconomic at those prices and that cutoff is now ore at current gold prices. Zones that were drilled, documented, and set aside because they were too low-grade to justify extraction are now being re-evaluated as potentially viable resources. This dynamic, where existing geological data gains economic relevance as prices rise, is a core part of the thesis for operators re-entering established mining districts.

What Recent Drilling Is Revealing About Deposit Upside

June 2026 Expansion Results

The most recent expansion drilling at Richmond Hill has returned results that suggest meaningful resource growth potential beyond the existing pit boundary. Properly interpreting gold drill results is essential when evaluating these intercepts, as isolated high-grade intersections must be considered alongside grade continuity and structural context. Key intercepts from the June 2026 programme include:

- A high-grade intersection of 5.24 g/t gold and 4.43 g/t silver over 13.5 meters in expansion zones

- Outlier intercepts exceeding 30 g/t gold over 20+ meters identified outside the current resource envelope

- Multiple consistent intersections of 1.0 to 2.0 g/t over 15 to 20 meter widths across broader portions of the deposit

The significance of high-grade intercepts outside the existing pit shell is that they represent potential resource additions not yet captured in the current 2.6 million ounce estimate. When these results are incorporated into the updated resource ahead of the Pre-Feasibility Study, they could support a larger mine life, higher annual production rates, or improved project economics.

The Maitland Parallel and District-Scale Implications

Dakota Gold's Maitland project, acquired from Barrick, has returned 47 drill intersections averaging approximately 11 grams per tonne over 4 metres. That grade profile, along its strike proximity to the West Ledges deposit, positions Maitland as a potential high-grade complement to Richmond Hill's bulk tonnage oxide resource. Together, these two assets suggest the company is building a district-scale position rather than a single-asset story.

The next major ASX story will hit our subscribers first

Development Roadmap: From Pre-Feasibility to First Production

Stage-by-Stage Timeline

- Pre-Feasibility Drilling Completed – 17,273 meters across 112 holes incorporated into the resource update

- Initial Assessment with Cash Flow – Published July 2025, confirming project economics at current gold prices

- Pre-Feasibility Study – Expected Q4 2026; will define mine plan, capital costs, and processing design

- Feasibility Study – Follows PFS completion; the feasibility study process triggers formal permitting application

- Permitting Process – Estimated at approximately 18 months on private land in South Dakota

- Construction Phase – Expected to commence following permit approval

- Target Commercial Production – Late 2029

Financial Position and Dilution Considerations

Dakota Gold reported a cash balance of approximately $47 million, providing runway to fund the Pre-Feasibility Study and advance engineering work without immediate pressure on shareholders from dilutive equity raises. For junior developers, preserving capital while progressing technical milestones is a discipline that separates well-managed companies from those that consume shareholder value through repeated financing rounds at progressively worse terms.

The Importance of Jack Henris as COO

The appointment of Jack Henris as President and Chief Operating Officer represents the transition from exploration-stage to development-stage thinking. Henris brings direct operational experience from both Barrick and Newmont, lives within the district, and has assembled a local team with hands-on knowledge of South Dakota's regulatory environment. At this stage of a project's life cycle, the COO appointment is arguably the most consequential single decision a development company makes.

When a project moves from resource definition toward engineering and permitting, the geological work has largely been done. What determines whether a project becomes a mine is almost entirely about operational leadership, team assembly, and execution discipline.

How Quartermain Distinguishes Real Deposits From Compelling Stories

The Geological Checklist

With exposure to projects across multiple continents over nearly five decades, Quartermain has developed a practitioner's framework for separating genuine mineralisation from well-marketed exploration narratives.

- Drill hole spacing and data density – Enough holes to statistically characterise grade continuity, not just isolated high-grade intercepts

- Structural geological understanding – Knowing what controls where the ore is, not just where it has been found

- Historical precedent and proximity – Nearby producing systems that validate the geological model

- Grade-tonnage relationship – Sufficient contained metal at grades that are economically mineable at realistic gold prices

- Infrastructure access – Power, water, roads, and processing equipment availability that affects capital costs

People Before Geology

Quartermain has consistently described team quality as the primary filter in investment evaluation, prioritised even above geological merit. A world-class deposit in the hands of an inexperienced or misaligned management team will underperform a merely good deposit managed by capable, motivated people who have done it before. This perspective, shaped by direct experience building mines from concept through construction, carries more operational validity than most junior mining investment frameworks. Consequently, Bob Quartermain's revival approach at Dakota Gold reflects precisely this philosophy of prioritising team quality alongside geological merit.

Silver's Structural Position in a Technology-Driven Economy

An Understated Industrial Role

Silver occupies a genuinely unique position among precious metals because its monetary and industrial demand profiles are both real and growing simultaneously. Its status as the highest electrical conductivity metal available, superior even to copper, makes it irreplaceable in certain high-performance applications.

The data centre buildout associated with artificial intelligence infrastructure provides a concrete illustration of silver's industrial exposure. A single acre of data centre construction requires an estimated 300 to 400 tonnes of copper for power distribution. Silver, given its superior conductivity, is embedded throughout the server platforms themselves, including interconnects, contact points, and thermal management components. A large-scale data facility can contain hundreds of kilograms of silver embedded in its technology infrastructure.

| Metric | Gold | Silver |

|---|---|---|

| Annual Production Value | ~$500 billion | ~$30 billion |

| Central Bank Purchasing | Significant and ongoing | Negligible |

| Primary Mine Production | Majority of supply | ~30% (remainder is byproduct) |

| Price Range (Last 20 Years) | $250 to $3,000+ | $4 to $60+ |

| Volatility Profile | Moderate | High |

| AI/Tech Infrastructure Demand | Limited | Growing significantly |

Volatility as a Feature, Not a Flaw

The relatively small size of the silver market, approximately $30 billion in annual production value versus gold's roughly $500 billion, creates significant price volatility when demand spikes or sentiment shifts. The absence of central bank purchasing as a demand stabiliser means silver lacks the structural floor that sovereign accumulation provides for gold.

For investors willing to accept that volatility, the long-term trajectory from $4 per ounce to current levels around $60 has been rewarding over multi-decade holding periods. The gold-silver ratio, which has historically ranged from around 15:1 to over 100:1, provides a relative valuation signal that experienced precious metals investors use to tilt portfolio allocations between the two metals.

The Junior-to-Major Pipeline and M&A Cycle Dynamics

Why Small Teams Consistently Outperform Corporate Exploration Departments

The pattern is well-established across multiple mining cycles: junior exploration companies, typically operating with focused teams of geologists and executives who have previous major-company experience, discover and de-risk assets faster and more capital-efficiently than large mining company exploration departments.

The structural reason is decision velocity. A small team evaluating drill results can pivot within days. A major mining company must route that same decision through geological teams, technical committees, executive review, and board approval processes. By the time the bureaucratic cycle completes, the opportunity has often moved on or been captured by a more agile competitor.

This dynamic is not new. It mirrors the model Teck Corporation employed in the 1980s, funding junior exploration groups and using them as an outsourced discovery engine, then acquiring assets as they advanced toward development. The Nikico Eagle consolidation in Finland, where a major allowed a junior to advance an asset before moving to acquire it, represents a modern iteration of the same pattern.

The Brucejack Blueprint as a Repeatable Model

The Brucejack transaction provides a template for understanding value creation in the junior mining space. Pretium discovered, de-risked, and built the mine. Newcrest acquired the producing asset at a significant premium, approximately $3.5 billion, reflecting the value added through that entire de-risking journey. The acquisition made sense for Newcrest because it acquired a proven, producing mine without bearing the discovery and development risk.

Richmond Hill, while structurally simpler than Brucejack, follows a conceptually similar path. Furthermore, a recent Dakota Gold leadership update underscores the company's commitment to assembling the experienced team necessary to advance the project toward a production decision that will either create shareholder value directly or position the asset attractively for larger-company acquisition.

Key Investment Considerations for 2026 and Beyond

The following represents an analytical summary and does not constitute financial advice. All investments in junior mining companies carry significant risk, including potential loss of capital.

- Structural gold demand is now anchored by sovereign accumulation rather than speculation, creating a more durable demand floor than previous cycles

- US domestic gold supply has declined approximately 50 percent since Homestake's closure, creating a strategic gap that onshore projects are positioned to address

- Richmond Hill's private land position provides a materially faster and more predictable permitting pathway compared to projects requiring federal land approvals

- The 2.6 million ounce resource with a projected 17-year mine life positions Richmond Hill among the most significant undeveloped oxide gold assets held by a US-listed junior developer

- The Q4 2026 Pre-Feasibility Study represents the next major technical milestone and potential value catalyst for Dakota Gold shareholders

- Exploration upside remains open beyond current resource boundaries, with high-grade peripheral intercepts suggesting the deposit has not yet reached its full extent

- Grade compression industry-wide means that finding new elephant-scale discoveries is becoming exponentially more expensive, increasing the relative value of already-defined, de-risked resources in established jurisdictions

Frequently Asked Questions

What Is Dakota Gold Corp. and What Is Its Primary Asset?

Dakota Gold Corp. is a US-focused gold development company with Robert Quartermain serving in a senior leadership role. Its flagship asset is the Richmond Hill oxide heap leach gold project located in the Black Hills of South Dakota, targeting commercial production by late 2029.

How Large Is the Richmond Hill Gold Resource?

Richmond Hill hosts approximately 2.6 million ounces of gold in the Measured and Indicated categories. The project is currently modelled at a target production rate of approximately 150,000 to 153,000 ounces per year with a projected mine life of 17 years.

Why Is Richmond Hill's Private Land Status Significant for Investors?

Private land positioning in South Dakota allows Dakota Gold to pursue a permitting process estimated at approximately 18 months, substantially shorter than comparable projects on federal public land that can face multi-year environmental review processes and stakeholder consultation requirements.

What Is the Expected Timeline for Richmond Hill to Reach Production?

The company is targeting commercial production in late 2029, following completion of the Pre-Feasibility Study in Q4 2026, a subsequent feasibility study, and the approximately 18-month permitting process on private land.

What Are Dakota Gold's Most Significant Recent Drilling Results?

June 2026 expansion drilling returned intercepts of 5.24 g/t gold and 4.43 g/t silver over 13.5 meters, with outlier high-grade zones exceeding 30 g/t gold over 20+ meters identified outside the current resource boundary.

What Makes Robert Quartermain's Involvement Credible?

Quartermain has approximately 50 years of resource sector experience including involvement in the Hemlo Gold Camp discovery, building Silver Standard Resources, founding Pretium Resources and delivering the Brucejack mine, which sold to Newcrest Mining for approximately $3.5 billion. He is a recipient of the Order of Canada, the country's highest civilian honour. The story of Bob Quartermain on Dakota Gold and Richmond Hill is, consequently, grounded in one of the most verifiable track records in the junior mining sector.

Want to Be Alerted the Moment the Next Major Gold Discovery Hits the ASX?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries across gold and 30+ other commodities — so subscribers can act before the broader market catches on. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin your 14-day free trial today to secure a genuine market-leading edge.