June 19, 2026

What Does De Beers $511 Million Loss Signal About Global Luxury Markets?

Global commodity markets face unprecedented headwinds as inflationary pressures, geopolitical tensions, and technological disruption converge to reshape traditional resource extraction economics. The luxury goods sector, particularly natural resource-dependent industries, confronts structural challenges that extend far beyond cyclical demand fluctuations. Moreover, the recent De Beers $511 million loss exemplifies how these macro-economic forces are fundamentally altering investment flows, consumer behavior patterns, and sovereign fiscal stability across resource-rich African economies.

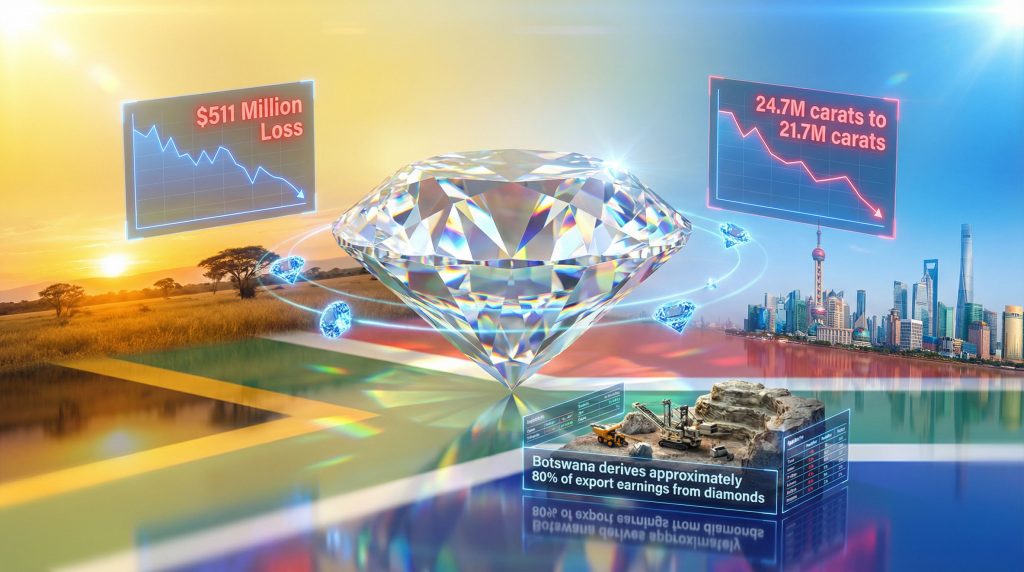

The diamond industry's largest producer has posted catastrophic financial results that illuminate broader structural weaknesses across luxury commodity markets. De Beers recorded an underlying EBITDA loss of $511 million in 2025, representing a dramatic deterioration from the previous year's $25 million loss. This 1,944% year-over-year decline occurred despite maintaining approximately $3.5 billion in total revenue, indicating severe margin compression rather than demand collapse.

Structural Shifts in Consumer Spending Patterns

The disconnect between revenue stability and profitability destruction reveals fundamental changes in consumer luxury spending behavior. Modern affluent consumers increasingly prioritize value transparency, ethical sourcing, and technological innovation over traditional prestige markers. This shift manifests in several key patterns:

- Experience-over-ownership preferences driving discretionary spending toward services rather than durable goods

- Sustainability consciousness creating demand for traceable, conflict-free alternatives

- Digital native purchasing habits favoring online research and direct-to-consumer channels

- Price sensitivity increases as economic uncertainty grows among high-net-worth individuals

Parent company Anglo American recognized a $2.3 billion impairment charge linked to revised long-term price expectations and shifting consumer preferences. This acknowledgment indicates management recognises these changes as structural rather than temporary, particularly in light of broader us economy and tariffs concerns affecting global trade flows.

The Macro-Economic Context Behind Luxury Commodity Declines

Luxury commodity markets operate within complex macro-economic frameworks where multiple forces interact to determine pricing power and demand sustainability. Current market conditions reflect convergence of several destabilising factors.

Monetary Policy Tightening Effects:

Central bank interest rate increases across major economies have reduced liquidity available for discretionary luxury purchases whilst strengthening alternative investment returns. When risk-free government bonds yield 4-5%, luxury goods must compete against financial assets for consumer capital allocation.

Inflation-Adjusted Purchasing Power:

Despite nominal income growth in developed markets, real purchasing power has declined as inflation outpaces wage increases. Luxury consumers face higher costs for essentials (housing, energy, food), constraining discretionary spending capacity. Furthermore, concerns about the tariff impact on investments continue to influence consumer confidence.

Wealth Distribution Concentration:

Growing wealth inequality paradoxically reduces luxury market size as middle-class consumers exit the premium segment whilst ultra-high-net-worth individuals represent insufficient volume to maintain industry revenues.

When big ASX news breaks, our subscribers know first

How Are Synthetic Diamonds Disrupting Traditional Mining Economics?

Laboratory-grown diamonds represent perhaps the most significant technological disruption to traditional mining economics since mechanisation. Unlike cyclical demand fluctuations, synthetic diamond competition creates permanent structural pressure on natural diamond pricing and market share.

Technology-Driven Market Share Erosion Analysis

Synthetic diamond production utilises two primary methodologies that deliver chemically and optically identical products to mined diamonds:

High Pressure High Temperature (HPHT) Process:

- Replicates natural diamond formation conditions in controlled laboratory environments

- Produces high-quality gems suitable for jewelry applications

- Offers predictable quality grades and reduced production timelines

Chemical Vapor Deposition (CVD) Technology:

- Creates diamonds through carbon atom deposition in vacuum chambers

- Enables precise control over diamond characteristics and properties

- Supports industrial applications requiring specific performance parameters

The fundamental economics favour synthetic production: laboratory facilities require significant upfront capital investment but operate with predictable costs, controlled quality, and no geological exploration risk. Mining operations face ongoing discovery costs, environmental compliance, labour management, and resource depletion challenges.

Price Competition Between Natural and Lab-Grown Alternatives

De Beers management explicitly cited competition from lab-grown diamonds as a material factor contributing to revenue pressure and inventory accumulation. This acknowledgment represents a strategic shift from previous industry dismissal of synthetic alternatives as inferior or temporary market phenomena.

Cost Structure Advantages:

- Laboratory production costs remain relatively fixed per carat regardless of market demand

- Mining costs increase as easily accessible deposits deplete, requiring deeper excavation

- Synthetic producers avoid transportation costs from remote African mining locations

- Quality control enables consistent grading and reduced sorting/processing expenses

Consumer Value Proposition:

Modern consumers, particularly millennials and Gen Z demographics, demonstrate reduced attachment to traditional diamond marketing narratives around rarity and romance. Instead, they prioritise:

- Ethical sourcing transparency without concerns about conflict mining

- Environmental impact reduction through laboratory production

- Value optimisation with identical physical properties at lower prices

- Customisation options available through controlled production processes

Consumer Preference Evolution in Luxury Goods

The synthetic diamond phenomenon exemplifies broader consumer preference evolution across luxury categories. Traditional luxury positioning based on scarcity, heritage, and exclusivity faces challenges from technology-enabled alternatives offering superior value propositions.

Anglo American's impairment charge explicitly referenced shifting consumer preferences, indicating corporate recognition that synthetic diamond adoption represents permanent market structure change rather than temporary competitive pressure.

De Beers Origins Strategy Response:

The company now pursues an Origins strategy focused on streamlining operations and stimulating natural diamond demand through marketing campaigns and industry agreements. This dual approach of cost reduction and demand stimulation suggests management views the competitive challenge as partially addressable through differentiation and brand positioning.

Why Is Chinese Demand Weakness Critical for African Mining Economies?

Chinese luxury consumption represents a critical demand pillar for global diamond markets, making economic slowdown in China particularly damaging for African diamond-dependent economies. The interconnection between Chinese growth, luxury spending, and African fiscal stability creates cascading risks across multiple economic systems.

China's Economic Slowdown Impact on Commodity Imports

China's economic deceleration stems from multiple structural factors that specifically impact luxury goods consumption:

Real Estate Sector Stress:

- Property market correction reduces household wealth effects that previously drove luxury spending

- Real estate represents primary savings vehicle for Chinese middle class, creating negative wealth effects

- Construction industry slowdown reduces employment in high-income sectors

Zero-COVID Policy Aftermath:

- Extended lockdowns disrupted consumer behaviour patterns and business confidence

- Supply chain disruptions reduced manufacturing profitability and export competitiveness

- Service sector employment recovery remains incomplete, constraining disposable income growth

Demographic Transition Challenges:

- Ageing population structure reduces economic growth potential and consumption capacity

- One-child policy effects create eldercare cost pressures on working-age population

- Youth unemployment rates remain elevated, limiting entry-level luxury consumption

Luxury Consumption Trends in Emerging Markets

Chinese luxury demand weakness occurs within broader emerging market consumption pattern changes that affect African commodity exporters:

| Market Segment | 2024 Performance | 2025 Trends | African Impact |

|---|---|---|---|

| Chinese luxury jewelry | -15% volume decline | Continued weakness | Direct revenue loss |

| Indian processing demand | Stable volumes | Tariff uncertainty | Supply chain disruption |

| Middle East consumption | +5% growth | Political stability dependent | Partial offset potential |

| Russian market access | Sanctions-limited | Minimal recovery expected | Permanent market loss |

Foreign Exchange Implications for Resource-Dependent Nations

Chinese demand weakness creates immediate foreign exchange pressures for African diamond exporters, particularly countries like Botswana where diamond revenues represent approximately 80% of export earnings.

Currency Pressure Mechanisms:

When Chinese luxury consumption declines, African diamond export volumes and prices fall simultaneously. This creates multiple transmission effects:

- Reduced foreign currency inflows constrain central bank reserves and currency stability

- Import cost inflation occurs as local currencies weaken against major trading currencies

- Debt servicing challenges emerge for countries with foreign currency-denominated obligations

- Fiscal revenue decline forces government spending cuts or increased domestic borrowing

Botswana Specific Vulnerability:

The Botswana Pula faces particular pressure during diamond market weakness due to the economy's concentrated exposure. Government revenues, foreign exchange reserves, and monetary policy all depend heavily on diamond export performance, creating pro-cyclical economic volatility.

What Do Global Trade Tensions Mean for Diamond Supply Chains?

International trade policy volatility has introduced unprecedented uncertainty into global diamond supply chains, with particularly severe implications for the India-centred cutting and polishing industry. President Donald Trump's introduction of 50% tariffs on India in August 2025 has fundamentally disrupted established trade flows and pricing mechanisms.

US Tariff Policy Effects on Indian Diamond Processing

India's dominance as the world's largest diamond cutting and exporting hub creates systemic vulnerability when trade barriers target Indian processing facilities. The 50% tariff rate represents a severe cost burden that affects multiple supply chain participants. Indeed, these developments are closely tied to broader us-china trade war effects rippling through global markets.

Impact Distribution Analysis:

| Supply Chain Stage | Tariff Burden | Adaptation Strategy | Timeline |

|---|---|---|---|

| Indian cutting facilities | Direct cost absorption | Margin compression | Immediate |

| African rough producers | Indirect price pressure | Alternative processing routes | 6-12 months |

| US retail consumers | Price pass-through | Demand destruction | 3-6 months |

| Alternative cutting hubs | Capacity expansion opportunity | Investment planning | 12-24 months |

Supply Chain Vulnerability Assessment

The concentration of diamond processing in India creates single-point-of-failure risks that tariff policies can exploit. Approximately 85% of global diamond processing occurs in Indian facilities, primarily concentrated in Surat and Mumbai, creating geographic and political risk exposure.

Restructuring Pathways:

Despite Trump's indication that tariff rollback could occur by April 2026, industry participants remain cautious about near-term demand recovery. This uncertainty has prompted several adaptation strategies:

- Direct Africa-to-US routing bypasses Indian processing but requires investment in alternative cutting facilities

- Third-country processing through Belgium, Israel, or South Africa increases costs but reduces tariff exposure

- Inventory management adjustments as companies prepare for extended tariff periods

- Contract renegotiation throughout supply chains to redistribute tariff burden

Geopolitical Risk Factors in Commodity Trading

Diamond trade tensions illustrate broader geopolitical risk factors affecting commodity markets globally. Trade policy uncertainty creates investment hesitation, supply chain diversification costs, and price volatility that extends beyond immediate tariff effects.

Policy Uncertainty Premiums:

Even when policymakers signal potential tariff reversals, market participants must plan for scenarios where policies remain in place longer than announced. This uncertainty premium manifests as:

- Reduced capital investment in processing facilities pending policy clarity

- Higher financing costs as lenders price geopolitical risks into credit decisions

- Inventory management conservatism as companies avoid excess exposure to tariff-sensitive trade routes

- Contract term adjustments incorporating force majeure clauses for trade policy changes

How Are African Economies Adapting to Diamond Market Volatility?

African diamond-producing nations face existential fiscal challenges as sustained market weakness threatens government revenues, foreign exchange stability, and economic development financing. The adaptation strategies reveal both the depth of economic dependency and the limited short-term alternatives available to resource-dependent states.

Botswana's Fiscal Dependency on Mining Revenues

Botswana represents the most extreme case of diamond revenue dependency among African economies, with mining income comprising approximately 80% of export earnings and forming the backbone of government fiscal capacity.

Fiscal Transmission Mechanisms:

Diamond revenue weakness creates cascading effects throughout Botswana's economic system:

Botswana derives approximately 80% of export earnings from diamonds, making the country particularly vulnerable to sustained price weakness. The current downturn poses significant challenges for government revenues and foreign exchange stability.

Government Revenue Structure:

- Direct mining taxes and royalties provide substantial budget income

- Corporate income taxes from De Beers and joint venture operations

- Foreign exchange earnings support import capacity and currency stability

- Employment effects throughout mining supply chains affect broader tax base

The Jwaneng mine, recognised as the world's most valuable diamond mine by revenue, serves as a critical fiscal anchor for the Botswana government. Operational pressure at Jwaneng directly translates to national budget constraints and policy limitations.

Economic Diversification Strategies in Resource States

Sustained diamond market weakness has accelerated economic diversification discussions across African diamond-producing countries, though implementation faces significant structural challenges. These efforts are particularly crucial given the broader mining industry evolution taking place globally.

Botswana Diversification Initiatives:

- Financial services hub development leveraging political stability and regulatory frameworks

- Beef production expansion targeting regional and international markets

- Tourism sector growth capitalising on wildlife resources and safari infrastructure

- Manufacturing promotion through industrial park development and investment incentives

South Africa Adaptation Approaches:

The Venetia mine's transition to underground operations represents technological advancement amid market pressure, whilst broader South African mining policy emphasises:

- Local beneficiation requirements encouraging domestic processing capacity

- Black Economic Empowerment policies promoting ownership transformation

- Infrastructure development supporting multiple mining sectors simultaneously

- Regional hub positioning for southern African mineral processing and logistics

Namibia Maritime Strategy:

Debmarine Namibia's offshore operations provide some insulation from land-based mining challenges whilst the country develops:

- Port infrastructure expansion supporting regional trade facilitation

- Green hydrogen production leveraging renewable energy resources

- Marine resource management balancing diamond extraction with fishing industry needs

Currency Stability Challenges in Commodity-Dependent Nations

Diamond market weakness creates foreign exchange pressures that compound fiscal challenges and constrain policy responses across African diamond producers.

Exchange Rate Pressure Analysis:

| Country | Currency Exposure | Stabilisation Measures | Effectiveness |

|---|---|---|---|

| Botswana | Pula depreciation risk | Foreign reserve management | Temporary relief |

| South Africa | Rand volatility | Monetary policy adjustment | Limited impact |

| Namibia | Peg to South African Rand | External stability anchor | Dependent on RSA policy |

Central Bank Response Strategies:

African central banks face difficult tradeoffs when diamond revenues decline:

- Interest rate increases defend currency but constrain domestic economic activity

- Foreign reserve depletion maintains exchange rate stability but reduces crisis buffers

- Import restrictions preserve foreign exchange but increase inflation and reduce living standards

- Fiscal austerity coordination with governments reduces demand for foreign exchange but constrains public investment

What Does Production Strategy Reveal About Market Fundamentals?

De Beers' production strategy adjustments provide critical insights into industry assessment of market fundamentals versus temporary demand fluctuations. The company's decision to reduce rough diamond production by 12% to 21.7 million carats reflects strategic positioning for extended market weakness rather than short-term inventory management.

Inventory Management in Commodity Cycles

Diamond inventory dynamics differ significantly from other commodities due to the industry's unique market structure and consumer purchase patterns. The De Beers $511 million loss and accompanying inventory strategy reveals management's expectations about demand recovery timing and price trajectory.

Strategic Production Curtailment:

The company has adopted disciplined production strategy, aligning output more closely with market conditions as industry stockpiles expanded over the past year. This approach indicates several strategic assessments:

- Extended weakness expectations requiring sustained production discipline rather than temporary adjustments

- Price support prioritisation over market share maintenance during demand weakness

- Cash flow preservation through operational efficiency rather than volume maximisation

- Inventory normalisation timeline extending beyond typical commodity cycle recovery periods

Demand-Supply Balance Management:

| Production Target | 2024 Actual | 2025 Actual | 2026 Forecast |

|---|---|---|---|

| De Beers output (M carats) | 24.7 | 21.7 | 21-26 (demand-aligned) |

| Global market estimate | ~135 | ~130 | Conservative approach |

| Inventory strategy | Accumulation | Normalisation | Gradual drawdown |

Capital Allocation During Market Downturns

De Beers reduced capital expenditure to $353 million, prioritising cash preservation and operational efficiency over expansion or exploration investments. This capital allocation strategy reveals management's assessment of investment return prospects during market stress.

Investment Priority Framework:

- Maintenance capital receives priority to preserve existing asset productivity

- Cost reduction initiatives generate immediate cash flow improvements

- Technology investments focus on efficiency rather than capacity expansion

- Exploration activities reduced pending improved market fundamentals

Strategic Cost Management:

The company's focus on unit cost reductions addresses both cyclical margin pressure and structural competitive threats from synthetic diamonds. This dual approach suggests management recognises current challenges combine temporary demand weakness with permanent market structure changes.

Strategic Output Adjustments vs Market Demand

For 2026, De Beers forecasts production between 21 million and 26 million carats, providing flexibility to align output with demand conditions. This range-based guidance reflects uncertainty about recovery timing whilst maintaining operational flexibility.

Adaptive Production Framework:

- Lower range utilisation during continued demand weakness preserves pricing discipline

- Upper range deployment enables rapid response to demand recovery signals

- Quarterly adjustment capability allows fine-tuning based on market feedback

- Regional production optimisation balances operational costs with transportation efficiency

The next major ASX story will hit our subscribers first

How Do Impairment Charges Reflect Long-Term Value Expectations?

Anglo American's $2.3 billion impairment charge related to De Beers operations represents a fundamental revaluation of asset value expectations, reflecting management's revised assessment of long-term market conditions and competitive dynamics.

Asset Valuation Methodology in Volatile Markets

Impairment charges occur when asset carrying values exceed expected future cash generation capacity, requiring asset revaluation to reflect changed market conditions or operational prospects. The preliminary financial results from De Beers provide additional context for these valuation adjustments.

Valuation Methodology Components:

- Discounted cash flow analysis incorporating revised price forecasts and production profiles

- Market multiple comparisons reflecting current industry valuation benchmarks

- Asset replacement cost assessment considering alternative investment opportunities

- Strategic option value evaluating flexibility for operational modifications or asset sales

The $2.3 billion impairment magnitude suggests substantial revision to long-term diamond price assumptions and market structure expectations, particularly regarding synthetic diamond competition and consumer preference evolution. Furthermore, the De Beers $511 million loss underscores the severity of these adjusted expectations.

Investor Sentiment and Resource Sector Valuations

Resource sector asset impairments create cascading effects on investor sentiment toward commodity-dependent companies and economies. The De Beers impairment contributes to broader resource sector revaluation trends affecting African equity markets and sovereign risk assessments.

Capital Market Implications:

- Equity valuation pressure on African mining companies with similar market exposure

- Credit rating reviews for resource-dependent sovereign borrowers

- Investment flow redirection toward less commodity-dependent African opportunities

- Currency pressure amplification through reduced foreign investment confidence

Capital Market Implications for Mining Investments

The impairment charge signals to capital markets that traditional diamond mining faces structural challenges requiring strategic adaptation rather than cyclical patience. This assessment affects investment allocation decisions across the resource sector.

Investment Strategy Adjustments:

- Portfolio diversification away from single-commodity exposure toward multi-resource strategies

- Technology integration investments in mining efficiency and alternative product development

- Geographic risk assessment incorporating political and market access considerations

- ESG compliance prioritisation addressing environmental and social governance requirements increasingly demanded by investors

What Are the Broader Implications for Luxury Goods Industries?

The diamond industry's challenges illuminate broader structural pressures affecting luxury goods sectors globally. Technology disruption, consumer preference evolution, and economic uncertainty create similar challenges across premium market categories.

Cross-Sector Analysis of Premium Market Performance

Luxury goods industries share common vulnerability factors that compound during economic stress periods:

Technology Disruption Patterns:

- Automotive sector: Electric vehicle transition challenging traditional luxury automotive brands

- Watchmaking industry: Smartwatch competition affecting mechanical timepiece demand

- Fashion and leather goods: Direct-to-consumer brands challenging established luxury retailers

- Jewelry and gemstones: Synthetic alternatives providing identical functionality at lower cost

Consumer Behaviour Commonalities:

Modern luxury consumers demonstrate similar preference shifts across categories:

- Value transparency demands requiring clear pricing justification and sourcing information

- Sustainability prioritisation influencing purchase decisions across luxury categories

- Experience preference evolution favouring services and travel over durable luxury goods

- Digital platform adoption changing discovery, research, and purchase patterns

Consumer Behavior Shifts in Discretionary Spending

Macro-economic pressures affecting luxury goods demand reflect broader discretionary spending pattern changes that extend beyond individual product categories.

Spending Priority Reallocation:

- Health and wellness investments receiving increased allocation during economic uncertainty

- Education and skill development prioritised over status symbol purchases

- Housing and security consuming larger portions of discretionary income

- Travel and experiences recovering faster than luxury goods in post-pandemic spending patterns

Technology Disruption Patterns in Traditional Industries

The synthetic diamond phenomenon exemplifies broader technology disruption patterns affecting established industries globally:

Disruption Characteristics:

- Performance equivalency removing technical barriers to adoption

- Cost advantage sustainability through manufacturing scale and learning curve effects

- Regulatory acceptance as safety and quality standards recognise technological alternatives

- Consumer acceptance acceleration as younger demographics show reduced attachment to traditional products

Industry Response Strategies:

Traditional luxury industries adopt similar defensive strategies when facing technology disruption:

- Heritage marketing emphasis highlighting history and craftsmanship narratives

- Exclusive experience creation differentiating through service and access rather than product alone

- Technology integration incorporating innovation whilst maintaining traditional appeal

- Market segmentation focus targeting consumers willing to pay premiums for traditional products

Strategic Outlook: Market Recovery Scenarios and Timeline Projections

Market recovery prospects depend on multiple variables including Chinese economic stabilisation, trade policy normalisation, and synthetic diamond market maturation. Recovery scenarios reflect different combinations of these factors and their timing. Additionally, the global recession outlook continues to influence investor expectations and market dynamics.

Inventory Normalisation Pathways

Diamond market recovery requires inventory normalisation throughout the supply chain, from rough diamond stockpiles to retail jewelry inventory. Current elevated inventory levels suggest extended timeline for market rebalancing.

Recovery Scenario Analysis:

| Timeline | Primary Drivers | Probability Assessment | African Economic Impact |

|---|---|---|---|

| 12-18 months | Chinese demand recovery, tariff removal | Moderate (40%) | Gradual fiscal stabilisation |

| 2-3 years | Synthetic market maturity, production discipline | High (60%) | Structural adjustment required |

| 5+ years | Industry transformation complete | Certain (95%) | Economic diversification imperative |

Demand Recovery Indicators to Monitor

Several key indicators provide early signals of diamond market demand recovery:

Chinese Market Metrics:

- Luxury retail sales data from major Chinese cities and online platforms

- Real estate market stabilisation supporting household wealth effects

- Employment trends in high-income service sectors affecting discretionary spending capacity

- Currency stability influencing travel and international luxury purchases

Global Demand Indicators:

- Wedding industry statistics as primary driver of engagement ring demand

- Tourist spending patterns in major luxury shopping destinations

- High-net-worth individual sentiment surveys and spending intentions

- Economic uncertainty indices affecting discretionary purchase timing

Long-Term Industry Transformation Trends

Regardless of cyclical recovery timing, the diamond industry faces permanent structural changes requiring strategic adaptation:

Technology Integration Requirements:

- Blockchain traceability systems providing transparent supply chain documentation

- AI-powered quality assessment reducing sorting and grading costs

- Automated mining equipment improving operational efficiency and safety

- Digital marketing platforms reaching consumers directly without traditional retail intermediation

Market Structure Evolution:

- Synthetic-natural market segmentation with clear positioning and pricing strategies

- Direct-to-consumer channels reducing retailer margins and improving producer pricing

- Regional processing development reducing dependency on Indian cutting centres

- Speciality product focus emphasising unique characteristics unavailable in synthetic alternatives

Investment Implications for Resource Portfolios:

Resource sector investors must adjust portfolio strategies to address structural changes rather than cyclical recovery positioning:

- Diversification emphasis across multiple commodities and geographic regions

- Technology adoption assessment evaluating mining companies' innovation capabilities

- ESG compliance evaluation incorporating environmental and social governance requirements

- Currency hedging strategies managing foreign exchange exposure for resource-dependent economies

Policy Responses in Resource-Dependent Economies:

African governments face policy challenges requiring both immediate fiscal management and long-term structural reform:

- Fiscal policy discipline maintaining government spending within reduced revenue constraints

- Economic diversification acceleration developing alternative revenue sources and employment opportunities

- Foreign exchange management preserving currency stability during reduced export earnings

- Social policy adaptation managing public expectations during economic adjustment periods

The diamond industry's current challenges illustrate broader themes affecting resource-dependent African economies: technology disruption, changing consumer preferences, and the necessity of economic diversification. While short-term recovery remains possible, long-term structural adaptation appears inevitable across both the diamond industry and resource-dependent African economies. Success will depend on strategic flexibility, investment in alternative economic sectors, and effective management of the transition period's economic and social challenges.

This analysis is based on publicly available information and industry reports. Investors should conduct independent research and consider consulting financial advisors before making investment decisions related to commodity markets or resource-dependent economies.

Ready to Capitalise on the Next Major Mineral Discovery?

While traditional luxury markets face structural challenges, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, empowering subscribers to identify actionable opportunities ahead of the broader market. Understand why historic discoveries can generate substantial returns by exploring the dedicated discoveries page, then begin your 14-day free trial today to position yourself for tomorrow's breakthrough announcements.