August 2, 2026

Understanding the Democratic Republic of Congo's Critical Role in Global Cobalt Markets

The global battery minerals sector has experienced particularly acute supply chain disruptions as producing nations seek to balance domestic industrial development objectives with international market stability. The battery metals investment landscape continues evolving as governments implement export control mechanisms to manage commodity supply. Furthermore, understanding these dynamics requires examining not just the policy frameworks themselves, but the practical realities of how export controls interact with existing mining infrastructure, transportation networks, and quality verification systems.

The Democratic Republic of Congo has established an unparalleled position in global cobalt supply chains, accounting for more than 70% of worldwide mined cobalt production in recent years. This extraordinary market concentration creates unique dynamics where operational disruptions in a single country can cascade through international battery manufacturing networks, affecting everything from smartphone production to electric vehicle assembly lines.

Cobalt extraction in the DRC operates primarily as a by-product of copper mining operations, creating an integrated metallurgical system where cobalt recovery depends on copper production economics rather than standalone cobalt demand. This structural relationship means that cobalt supply fluctuations often reflect copper market conditions, mining company investment decisions, and operational capacity at major integrated facilities.

The geographic concentration of these operations within specific mining districts creates additional vulnerability points in the global supply chain. When combined with the region's infrastructure challenges and complex regulatory environment, this concentration effect amplifies the impact of any operational or administrative disruptions on international markets.

Strategic Importance for Battery Supply Chains

Cobalt serves as an essential component in nickel-cobalt-manganese (NCM) battery chemistries used across consumer electronics and electric vehicle applications. The material's role in battery cathode formulations makes it critical for energy density and thermal stability characteristics that determine battery performance parameters.

The established supply chain pathway involves a three-stage international movement from DRC mining operations through South African port facilities to Chinese refinery processing centers. This routing reflects both historical trade relationships and current infrastructure capabilities, with cobalt hydroxide typically transported by truck to Durban port before maritime shipment to Chinese processing facilities.

This supply chain architecture creates multiple potential disruption points where delays, capacity constraints, or regulatory changes can impact material flow. Understanding these vulnerabilities helps explain why relatively small operational disruptions in the DRC can produce outsized effects on global cobalt availability and pricing.

Cobalt Hydroxide Specifications and Quality Requirements

Cobalt hydroxide 30% Co minimum represents the standard specification for international trade, with the "30% Co min" designation indicating minimum cobalt content requirements at the point of delivery to Chinese facilities. This specification standard reflects both technical requirements for downstream processing and quality assurance needs for consistent refinery operations.

The technical requirements for cobalt hydroxide involve multiple quality parameters beyond simple cobalt content, including moisture levels, impurity concentrations, and physical characteristics that affect transportation and processing efficiency. These specifications must be verified through laboratory analysis before export clearance, creating quality control checkpoints that can become bottlenecks when administrative or testing capacity constraints emerge.

When big ASX news breaks, our subscribers know first

What Triggered the Implementation of DRC's Export Quota System?

The evolution from unrestricted exports to comprehensive quota management reflects the DRC government's assessment of global market conditions and domestic industrial development priorities. During February through October 2025, the government implemented a complete export ban to address what officials characterized as oversupply conditions affecting global cobalt markets.

This nine-month embargo period represented an unprecedented intervention in cobalt markets, effectively removing the world's largest producer from international supply chains. The policy reflected government conclusions that unrestricted exports were contributing to price weakness and inventory accumulation that undermined both producer revenues and government mineral royalties.

The transition to a quota system in October 2025 marked a shift from binary export control to graduated supply management. This evolution suggested recognition that complete export cessation, while dramatic in market impact, was unsustainable for both government revenues and international supply chain stability.

Quota Structure and Allocation Framework

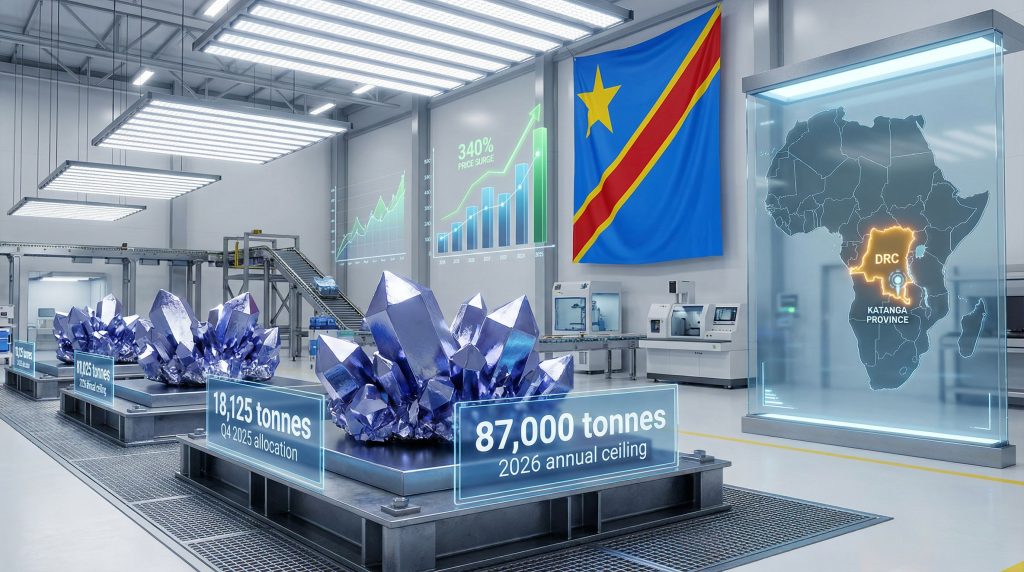

The Q4 2025 allocation of 18,125 tonnes established the initial framework for controlled exports, subsequently extended through Q1 2026 to create a combined six-month allocation period. This approach allowed administrative systems time to develop operational procedures while providing market participants with some supply continuity.

Table: DRC Cobalt Export Quota Structure

| Period | Allocation (Tonnes) | Monthly Equivalent | Additional Reserves |

|---|---|---|---|

| Q4 2025 – Q1 2026 | 18,125 | ~3,020 | Extension granted |

| 2026 Annual | 87,000 | 7,250 | 9,600 discretionary |

| Strategic Reserve | 9,600 | Variable | Government discretion |

The 2026 annual ceiling of 87,000 tonnes represents approximately 7,250 tonnes monthly baseline capacity, with an additional strategic reserve of 9,600 tonnes available at government discretion. This two-tier structure provides baseline supply certainty while maintaining regulatory flexibility to respond to market conditions.

Administrative Authority and Discretionary Controls

The Authority for the Regulation and Control of Strategic Mineral Substances' Markets (ARECOMS) maintains comprehensive discretion over quota allocations, modifications, and enforcement mechanisms. This centralised authority structure enables rapid policy adjustments but creates uncertainty for mining companies regarding allocation predictability and utilisation requirements.

Moreover, government intervention in mining reflects broader trends across resource sectors globally. Unused quota withdrawal policies create additional operational pressure on allocated companies, establishing "use it or lose it" dynamics that can force suboptimal logistics decisions or penalise companies facing legitimate operational delays.

How Do Laboratory Testing Discrepancies Create Export Bottlenecks?

Multi-laboratory verification requirements represent one of the most significant operational barriers preventing efficient quota utilisation. The mandatory three-laboratory testing protocol involving ARECOMS, CEEC, and private exporter laboratories creates a verification triangle intended to ensure accuracy and prevent fraudulent grade reporting.

However, natural analytical variation in cobalt content measurements creates administrative friction when three independent laboratories produce results within acceptable measurement ranges but with slight numerical differences. For example, laboratories might report 29.8%, 30.1%, and 30.3% cobalt content for identical samples, all within normal analytical precision but creating documentation challenges for export clearance.

Technical Challenges in Assay Harmonisation

Analytical methodology differences between the three required laboratories can produce systematic variations in reported results even when measuring identical material. These differences might involve sample preparation techniques, analytical equipment calibration standards, or reporting conventions that create consistent but conflicting results.

The ±2% tolerance specifications referenced in export documentation create boundary conditions where materials with cobalt content near threshold levels become subject to interpretation disputes. When quota allocation depends on precise grade specifications, this analytical uncertainty translates directly into administrative delays and export clearance complications.

Sampling and preparation variables add additional complexity to the testing process. Cobalt hydroxide samples require proper moisture correction, particle size homogenisation, and representative sub-sampling techniques to ensure analytical accuracy. Variations in these preparatory steps can legitimately produce different analytical results independent of laboratory competence or equipment precision.

Administrative Resolution Mechanisms

Current protocols for resolving conflicting laboratory results remain under development, with market participants reporting unclear guidance on decision hierarchies when test results differ. This regulatory ambiguity creates delays as export documentation awaits ministerial interpretation or additional testing cycles to achieve consensus results.

Resolution timeline extensions have become commonplace as administrative systems struggle to balance quality assurance requirements with operational efficiency needs. These delays compound throughout the export process, creating cascading effects that impact shipping schedules and customer delivery commitments.

What Are the Primary Operational Barriers Preventing Full Quota Utilisation?

Export clearance data reveals the severity of operational constraints affecting DRC cobalt flows. Between December 2025 and February 2026, only 7,800 tonnes received export clearance despite allocated quota availability significantly exceeding this volume. This clearance rate of approximately 2,600 tonnes monthly falls well below the theoretical capacity suggested by quota allocations.

Critically, clearance does not equal shipment due to downstream logistics constraints that prevent physically cleared material from reaching international markets. This distinction between administrative approval and actual export represents a fundamental gap in the quota system's effectiveness.

Infrastructure and Transportation Disruptions

Bridge collapses on key trucking routes have created immediate transportation bottlenecks affecting material movement from mining operations to port facilities. These infrastructure failures represent the type of unexpected disruptions that can paralyse export flows regardless of quota availability or administrative clearances.

Weather-related delays during heavy rainfall periods compound transportation challenges, particularly affecting truck transport over unpaved or partially paved route segments. The seasonal nature of these disruptions creates predictable but difficult-to-manage bottlenecks that affect export scheduling and inventory management.

Port capacity limitations at Durban create additional constraints on material throughput, particularly during peak shipping periods when cobalt hydroxide competes with other bulk commodities for handling capacity and berth availability. These limitations can create queuing delays that extend well beyond DRC border clearance timelines.

Documentation and Regulatory Processing Delays

Ministerial oversight requirements for border clearance procedures create administrative bottlenecks that concentrate decision-making authority in limited personnel resources. This centralised approval structure, while ensuring government control, creates single points of failure where personnel availability directly impacts export processing speed.

Non-transferable quota allocations prevent efficient utilisation by limiting companies' ability to trade unused capacity with operators capable of immediate shipment. This inflexibility can result in quota waste when individual companies face specific operational delays while other producers have available capacity.

The complexity of export documentation requirements, combined with limited processing capacity at border control points, creates systematic delays that extend beyond individual company control. These institutional constraints affect all market participants regardless of their operational efficiency or preparation quality.

How Severe Is the Gap Between Allocated Quotas and Actual Exports?

Market participants describe the export shortfall as "massive discrepancies" between allocated quotas and actual material shipments. DRC-based logistics operators estimate that less than 50% of Q4 2025/Q1 2026 quota allocations resulted in actual material exports, with some estimates suggesting the figure may be closer to one-third of allocated volumes.

This utilisation rate indicates systematic constraints affecting the entire industry rather than company-specific operational issues. The widespread nature of these shortfalls suggests that quota allocation methodology may not adequately account for practical implementation barriers.

Furthermore, the discrepancy in DRC cobalt exports highlights fundamental challenges in supply chain management that extend beyond regulatory frameworks. According to Argus Media's analysis, these disruptions reflect complex interactions between regulatory requirements and practical operational constraints.

Industry Assessment:

DRC-based logistics operators report that material continues to accumulate at mining facilities and border crossing points despite administrative clearances, indicating that transportation and port capacity constraints represent the primary bottleneck in export flows.

Timeline Analysis of Export Performance

December 2025 through February 2026 clearance volumes of 7,800 tonnes represent significantly reduced throughput compared to historical export levels prior to the quota implementation. This three-month period encompasses both the extended Q4 2025 quota period and initial Q1 2026 allocations.

The clearance versus actual shipment distinction has become critical for understanding market supply conditions. Material that receives administrative approval for export may remain in-country for weeks or months awaiting transportation capacity or favourable shipping schedules.

Cumulative impact analysis suggests that delayed shipments from Q4 2025 and Q1 2026 may create inventory buildup that affects subsequent quota period utilisation, potentially compounding delays as storage capacity becomes constrained.

What Market Impacts Result from Constrained DRC Cobalt Exports?

Cobalt hydroxide pricing has experienced dramatic increases reflecting constrained supply availability. Average pricing of $25.44-25.80 per lb during January-February 2026 represents approximately 340% year-over-year increases compared to pre-quota pricing levels.

This pricing surge reflects both actual supply shortages and market anticipation of continued constraints. Spot market availability has become severely restricted, with buyers reporting difficulty securing material at any price level.

Chinese Refinery Supply Constraints

Declining import volumes of cobalt intermediates into China have forced refineries to modify operational plans and draw down existing inventory stockpiles. Chinese import statistics show continued deterioration in feedstock availability throughout early 2026.

Market analysts project annual deficits of 5,000-6,000 tonnes for 2026-2027, assuming continuation of current quota enforcement levels and operational constraints. These projected shortfalls would represent significant tightening relative to typical market balances and could force additional price increases or demand destruction.

Chinese refinery operational adjustments include shift strategies toward cobalt metal dissolution processes to maximise utilisation of available feedstock. This operational pivot reflects the severity of intermediate supply constraints and the economic pressure to maintain production despite input limitations.

Global Supply Chain Implications

Battery manufacturers face increased input cost pressures and potential supply security concerns as cobalt availability tightens. Long-term contract negotiations have become increasingly complex as suppliers struggle to guarantee delivery volumes against quota uncertainties.

Electronic device manufacturers similarly face cost pressures and potential substitution pressures toward battery chemistries with reduced cobalt content requirements. This demand-side response could provide some market balance but requires significant technical development and qualification timelines.

The next major ASX story will hit our subscribers first

How Are Mining Companies and Traders Adapting to Quota Limitations?

Strategic adaptation responses include operational modifications to maximise quota utilisation efficiency and alternative sourcing strategies to maintain customer relationships. Companies are developing contingency plans for different quota enforcement scenarios and investing in improved logistics coordination.

The cobalt blue expansion represents one example of how companies are seeking to diversify supply sources beyond the DRC. Alternative sourcing strategies for Chinese refineries include increased focus on non-DRC cobalt development projects and expanded recycling programme investments.

Regulatory Compliance and Risk Management

ARECOMS discretionary authority over quota modifications creates ongoing uncertainty for operational planning and contract commitment decisions. Companies must balance quota utilisation pressure with market timing considerations and customer delivery obligations.

Force majeure considerations for long-term supply contracts have become increasingly relevant as companies evaluate whether quota constraints and infrastructure disruptions constitute unforeseeable circumstances excusing delivery obligations.

Unused allocation withdrawal policies require companies to develop utilisation strategies that prioritise quota preservation over optimal market timing, potentially forcing subeconomic shipping decisions to maintain allocation rights.

What Does Demand Softening Mean for Future Quota Enforcement?

Electric vehicle adoption rates have fallen below earlier projections, reducing pressure on cobalt supply chains and potentially providing breathing room for quota system implementation. Slower EV growth rates affect both near-term demand levels and long-term supply planning assumptions.

Consumer electronics demand moderation similarly reduces pressure on cobalt supply, particularly as manufacturers continue developing battery chemistries with reduced cobalt content requirements. This demand-side softening may influence government decisions about quota enforcement stringency.

Battery Chemistry Evolution and Demand Implications

Technology development toward lower-cobalt formulations continues advancing, with manufacturers increasingly focused on lithium iron phosphate (LFP) and other chemistries that reduce or eliminate cobalt requirements. These technological trends create long-term demand uncertainty that may influence quota policy decisions.

Market balancing considerations suggest that government revenue optimisation may require adjusting quota levels to maintain export income while supporting domestic industrial development objectives. This balancing act becomes more complex as demand growth moderates and alternative supply sources develop.

What Are the Broader Implications for Critical Minerals Supply Security?

Western economies' dependency on the DRC-China supply chain corridor has become increasingly apparent through the quota implementation period. This concentration risk extends beyond cobalt to include other critical minerals & energy transition considerations where similar supply chain vulnerabilities exist.

Strategic mineral security initiatives in response to these constraints include government programmes supporting domestic processing capacity development and alternative supply source identification. These initiatives represent long-term structural responses to concentration risks highlighted by current disruptions.

Investment and Development Outlook

Capital allocation toward non-DRC cobalt projects has accelerated as investors and manufacturers seek supply diversification. These investments include both traditional mining development and innovative extraction technologies that could access previously uneconomic resources.

Technology development for cobalt recycling has gained increased priority as supply constraints highlight the value of secondary material sources. Battery recycling programmes and urban mining initiatives could provide meaningful supply contributions as battery waste streams mature.

Supply chain diversification strategies for battery manufacturers include geographic distribution of suppliers, alternative chemistry development, and strategic inventory management programmes designed to buffer against supply disruptions.

Investment and Risk Assessment Considerations

The discrepancy in DRC cobalt exports relative to allocated quotas creates both immediate market opportunities and long-term structural challenges for investors and industry participants. Understanding these dynamics requires careful analysis of operational constraints, policy evolution, and demand trajectory implications.

Short-term trading opportunities exist around supply tightness and pricing volatility, but require careful risk management given the unpredictability of quota enforcement and infrastructure constraints. Market participants must balance opportunity against the potential for rapid policy changes that could affect position profitability.

Long-term investment strategies should consider the probability of continued supply constraints, alternative supply development timelines, and technology evolution that could reduce cobalt demand intensity. These factors suggest that current high prices may not be sustainable indefinitely, requiring careful timing and exit strategy development.

Geological and Technical Risk Factors

Resource grade variability affects the economics of alternative cobalt projects under development outside the DRC. Lower-grade deposits require higher processing costs that may only be economic at elevated price levels sustained by supply constraints.

Processing technology limitations for non-traditional cobalt sources include technical challenges in achieving consistent product specifications and managing impurity concentrations that could affect downstream refinery operations.

Infrastructure development requirements for alternative supply sources include significant capital investment in processing facilities, transportation networks, and port capacity that could take several years to implement even with aggressive development timelines.

Conclusion: Navigating Uncertainty in Critical Minerals Markets

The substantial discrepancy in DRC cobalt exports compared to allocated quotas illustrates the complexity of implementing supply control policies in resource industries. Technical, administrative, and infrastructure constraints can significantly reduce the effectiveness of theoretical quota systems, creating market conditions that diverge substantially from policy intentions.

For market participants, these dynamics require sophisticated risk management approaches that account for both policy uncertainty and operational implementation challenges. The experience with DRC cobalt quotas provides valuable insights for understanding how similar policies might affect other critical minerals markets and how supply chain resilience can be improved through diversification and flexibility.

As detailed in Mysteel's comprehensive analysis, these regulatory hurdles and logistics bottlenecks represent fundamental challenges that extend beyond simple policy adjustments. Furthermore, mining industry trends indicate that such supply chain disruptions may become more frequent as resource-rich countries seek greater control over their mineral exports.

Disclaimer: This article contains analysis of commodity markets and supply chain dynamics that involve inherent uncertainty and speculation. Market conditions, government policies, and operational factors can change rapidly and unexpectedly. Readers should conduct their own research and consult with qualified advisors before making any investment or business decisions based on this information. Price projections and market forecasts represent analytical opinions and should not be considered guaranteed outcomes.

Want to Capitalise on Critical Minerals Supply Disruptions?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, including emerging cobalt and battery metals opportunities that could benefit from the current supply constraints affecting DRC exports. Understanding why major mineral discoveries can lead to substantial market returns by exploring Discovery Alert's dedicated discoveries page, showcasing historic examples of exceptional outcomes, whilst beginning your 14-day free trial today to position yourself ahead of evolving critical minerals markets.