July 14, 2026

The Untapped Resource Hiding in Plain Sight: America's Coal Waste and the Critical Minerals Revolution

For decades, the global mining industry has oriented itself around a familiar model: find a deposit, permit a mine, extract ore, process it. This linear approach served well enough in an era of stable geopolitics and predictable supply chains. However, that era has passed. The DOE coal waste critical minerals pilot projects represent a pivotal shift in how America is rethinking domestic supply. China's dominance over rare earth element (REE) processing, its near-total control of gallium and germanium output, and its demonstrated willingness to weaponise that control through export restrictions have exposed a structural vulnerability at the heart of the U.S. industrial economy.

The question now is not simply where America finds new mineral deposits, but how it finds them faster, cheaper, and with fewer geopolitical strings attached. The answer, increasingly, lies beneath the surface of a problem that already exists: hundreds of millions of tonnes of coal ash, tailings, and processing byproducts spread across Appalachia, the Illinois Basin, and the Powder River Basin. These waste streams, generated across more than three centuries of U.S. coal production, contain measurable concentrations of precisely the materials the country needs most.

When big ASX news breaks, our subscribers know first

Why America Cannot Simply Mine Its Way Out of the Problem

The Import Dependency Trap

The depth of U.S. reliance on foreign sources for critical minerals is not broadly appreciated outside specialist circles. Gallium, which is essential for compound semiconductors used in radar systems, satellite communications, and 5G infrastructure, is sourced overwhelmingly from China, which accounts for roughly 80% or more of global refined output. Germanium, used in infrared optics and fibre optic systems with direct defence and telecommunications applications, follows a similar pattern.

Furthermore, the rare earth supply chain presents an even more layered challenge. While REE ore is mined in several countries, the separation and refining of individual rare earth oxides remains highly concentrated in China, which controls an estimated 85 to 90% of global processing capacity. This means that even ore mined domestically often travels overseas for separation before returning as processed material, a supply chain dynamic that undermines the national security logic of domestic extraction.

The Greenfield Mining Bottleneck

Conventional mining is simply too slow to address near-term supply gaps. A new greenfield critical mineral mine in the United States typically requires:

- 7 to 20 years from discovery to first production, accounting for exploration, resource definition, permitting, feasibility, and construction phases

- Hundreds of millions to billions of dollars in capital expenditure before a single tonne of ore is processed

- Navigation of an environmental review process that, while necessary, adds significant time and cost uncertainty

- Downstream processing infrastructure that often does not exist domestically, particularly for REE separation and refining

Policy analysts and supply chain researchers have consequently pointed to unconventional feedstocks, including industrial and mining waste streams, as a faster pathway to domestic supply. The logic is straightforward: these materials have already been brought to the surface. What remains is the processing challenge. In addition, critical minerals processing innovations are emerging rapidly to address exactly this type of low-grade, high-volume feedstock.

What Coal Waste Actually Contains, and Why That Matters

The Geochemistry of Coal Byproducts

Coal is not simply carbon. During its formation, coal absorbs and concentrates trace elements from surrounding geological formations over millions of years. When coal is mined and processed, these trace elements are partitioned into various waste streams: fly ash, bottom ash, coal refuse, and tailings from washing and beneficiation operations.

Different U.S. coal basins produce waste with notably different geochemical signatures. Appalachian coal has been identified in prior Department of Energy assessments as producing some of the highest REE concentrations in domestic coal waste. Certain Appalachian fly ash samples report total rare earth oxide (TREO) concentrations that make them competitive with some lower-grade primary ore deposits.

Powder River Basin coal, by contrast, is geologically younger and formed in a different depositional environment. Its byproducts present a distinct elemental profile, making comparative data across basins scientifically valuable for understanding which feedstocks are most amenable to economic recovery.

A Note on Mineral Grades: Unlike conventional mining, where ore grades are expressed in grams per tonne or percentage by weight, REE concentrations in coal waste are typically reported in parts per million (ppm) of total rare earth oxides. Concentrations in coal ash can range from roughly 200 to over 1,000 ppm TREO depending on basin and coal type, with some Appalachian samples exceeding these ranges.

The Gallium and Germanium Connection

Gallium and germanium are classified as byproduct metals in conventional metallurgy, meaning they are not the primary target of any mine but are instead recovered as co-products of other processes. Their occurrence in coal waste follows a similar logic: they concentrate in coal during geological formation and partition into fly ash during combustion.

China's export controls on gallium and germanium in 2023 sent immediate reverberations through Western semiconductor supply chains. The U.S. Geological Survey lists both as critical minerals, and their recovery from domestic coal waste represents one of the few near-term pathways to reducing import dependency without waiting for new primary production to come online.

The DOE Coal Waste Critical Minerals Pilot Projects: Architecture and Intent

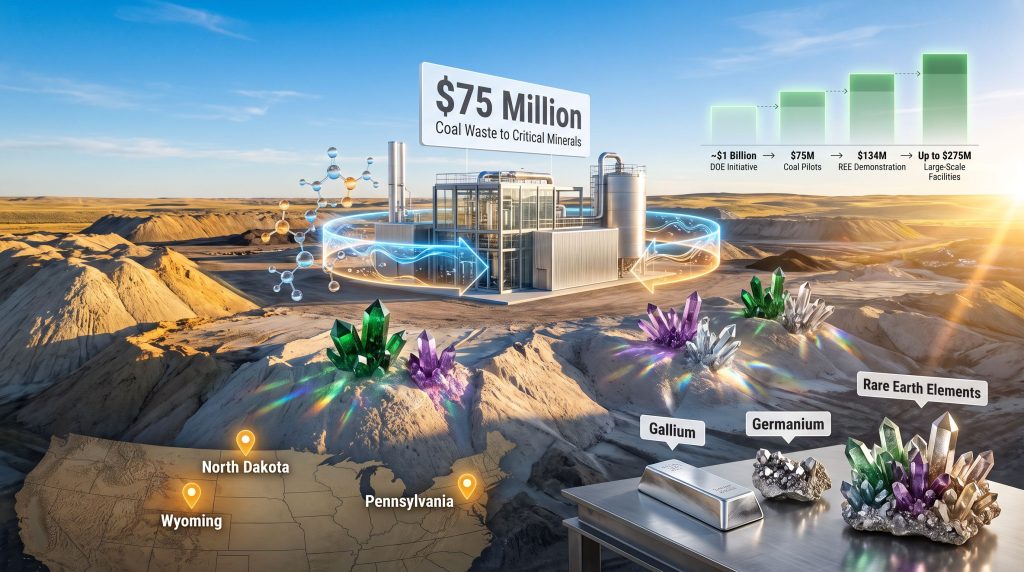

A $75 Million Program Within a Much Larger Framework

The five DOE coal waste critical minerals pilot projects announced in mid-2026 sit within a carefully structured investment hierarchy. Understanding that structure is important for interpreting what these projects are, and are not, designed to accomplish.

| DOE Program Component | Funding Level | Focus |

|---|---|---|

| Coal-Based Feedstock Pilots (Topic Area 1) | $75 million | Five projects recovering REEs, gallium, germanium, aluminium from coal waste |

| Rare Earth Elements Demonstration Facility Program | $134 million | REE recovery from mining and industrial waste streams |

| Larger-Scale Pilot Facilities (DE-FOA-0003583) | Up to $275 million | 1:50-scale or larger facilities |

| Total DOE Critical Minerals Initiative | ~$1 billion | Broad supply chain strengthening across multiple sectors |

The five pilot projects are managed by the DOE's National Energy Technology Laboratory (NETL). In 2023, NETL distributed $19 million across 13 regional initiatives to assess REE and critical mineral occurrences across U.S. coal basins. That earlier work produced the feedstock characterisation data that directly informs the current pilot selections, creating a logical and deliberate progression from resource assessment to technology demonstration.

Important Caveat for Investors and Observers: Selections for award negotiations are not final funding commitments. Each of the five projects must complete a negotiation process before funding is confirmed. This distinction matters, particularly for publicly traded companies involved in these projects.

The Technology Readiness Level Context

A concept central to understanding what the DOE pilot programme is actually doing is the Technology Readiness Level (TRL) scale, a nine-point framework used across government and industry to assess the maturity of a technology.

TRL 1-3: Basic Research and Proof of Concept (Laboratory)

TRL 4-6: Technology Validation (Bench and Pilot Scale) ← Target Zone for This Program

TRL 7-9: Commercial Demonstration and Full Deployment

Most coal-based critical mineral recovery technologies currently sit at TRL 4 to 5. The DOE pilot programme is designed to advance projects toward TRL 6 to 7, the threshold at which private capital typically becomes available for commercial scale-up.

The Five Selected Projects: What Makes Each Distinctive

University of North Dakota at Falkirk Mine

Situating a pilot facility at an active operating coal mine rather than a legacy waste site introduces important advantages. Real-time access to freshly generated byproducts allows researchers to characterise feedstock variability as it occurs, rather than working with stockpiled material whose geochemistry may have shifted through weathering or leaching. The academic-industry partnership model also builds domestic human capital, a frequently overlooked but strategically significant dimension of supply chain development.

Valor Metals and Electrochemical Liquid-Liquid Extraction

The e-LLE technology being commercialised by Valor Metals represents a genuinely novel approach to metal separation. Electrochemical liquid-liquid extraction operates on a fundamentally different principle from conventional solvent extraction. An applied electrical potential drives the selective transfer of target metal ions across the interface between two immiscible liquids. Because the driving force is electrical rather than thermal, the process can operate at ambient or near-ambient temperatures, potentially reducing both energy consumption and the carbon footprint of critical mineral recovery.

The significance for coal-based feedstocks is considerable. Coal ash and tailings typically produce dilute leach solutions where conventional solvent extraction faces economic headwinds. Electrochemical methods may offer a selectivity advantage in these dilute conditions, though industrial-scale validation remains the critical unknown.

CONSOL Innovations in Pennsylvania

Appalachian coal waste tailings are among the most thoroughly characterised feedstocks in the DOE's existing research base. CONSOL Innovations brings the advantage of operating within a region where baseline geochemical data is already relatively mature, reducing the feedstock uncertainty that typically accompanies early-stage pilot programmes. Furthermore, the DOE's selection of Core Natural Resources underscores how seriously established coal operators are taking this emerging opportunity.

American Resources: The Integration Approach

Rather than constructing a standalone pilot facility, the American Resources approach involves integrating proprietary recovery technology into existing operational infrastructure. This philosophy, sometimes termed brownfield process integration, targets a structural inefficiency in critical mineral supply chain development: the capital cost of building dedicated processing facilities. By embedding recovery technology within existing industrial footprints, the approach can potentially reduce both capital expenditure and time-to-first-production.

Peabody Energy's Wyoming Rare Earths Project

The Powder River Basin is the largest coal-producing region in the United States by volume, and Peabody Energy operates at significant scale within it. The Wyoming Rare Earths Project is strategically significant not only for its feedstock volume potential but for the comparative geological data it will generate. Understanding how REE and critical mineral concentrations vary across basin types is essential for building a nationally distributed recovery industry.

All Five Projects at a Glance

| Project Lead | Location | Primary Technology or Focus | Feedstock Type |

|---|---|---|---|

| University of North Dakota | Falkirk Mine, North Dakota | Multi-mineral recovery at active operation | Coal and associated waste streams |

| Valor Metals | Undisclosed | Electrochemical liquid-liquid extraction (e-LLE) | Coal byproducts and other feedstocks |

| CONSOL Innovations | Pennsylvania | REE extraction from coal waste tailings | Coal processing tailings |

| American Resources | Undisclosed | Commercial-scale process technology integration | Coal and coal-based feedstocks |

| Peabody Energy | Powder River Basin, Wyoming | Wyoming Rare Earths Project | Coal combustion byproducts |

The Broader Economic and Geopolitical Calculus

From Environmental Liability to Industrial Asset

Coal waste impoundments and ash disposal facilities represent ongoing financial and legal obligations for operators. The economic logic of converting these liabilities into revenue-generating feedstocks is compelling on its own terms. For coal-producing states like Wyoming, North Dakota, and Pennsylvania, where energy transition pressures are already reshaping the economic outlook, successful critical mineral recovery offers a concrete diversification pathway rooted in existing industrial infrastructure.

The critical minerals demand surge anticipated through the remainder of this decade only strengthens that economic case, as clean energy and defence sectors compete for the same finite pool of materials.

The Scaling Question: From Pilot to Commercial

Pilot success is necessary but not sufficient for commercial viability. The pathway from TRL 6 to commercial deployment requires a further set of conditions to align:

- Demonstrated recovery efficiency at scale that matches or approaches laboratory benchmarks

- Processing costs that remain competitive against prevailing market prices for recovered materials

- Offtake agreements or downstream market access for market-ready critical materials

- Access to the DOE's larger-scale funding tier (up to $275 million under DE-FOA-0003583) for progression to 1:50-scale or larger facilities

- Private capital engagement, which typically requires TRL 7 or above and demonstrated project economics

Speculative Perspective: If the five pilot projects collectively demonstrate that coal waste can serve as a consistent, economically recoverable feedstock, the broader implications extend well beyond the five projects themselves. Tens of millions of tonnes of legacy coal ash exist in disposal sites across the U.S. A proven recovery model could catalyse a geographically distributed domestic supply chain that no single greenfield mine could replicate.

China's Export Restrictions: The Catalyst That Cannot Be Ignored

China's 2023 export restrictions on gallium and germanium were a deliberate signal, not merely a trade policy adjustment. They demonstrated that critical mineral supply chains can be disrupted at will by a single dominant processor. The Defense Production Act has consequently been invoked as part of a broader suite of policy tools aimed at accelerating US critical minerals production across unconventional as well as conventional sources.

Whether these five pilot projects can meaningfully shift the supply balance within a commercially relevant timeframe depends heavily on how quickly successful pilots can attract the private investment required for commercial deployment.

The next major ASX story will hit our subscribers first

Frequently Asked Questions

Are the five DOE coal waste critical minerals pilot projects confirmed for funding?

No. The five projects have been selected for award negotiations, which is a preliminary stage. Final funding commitments are subject to the outcome of those negotiations. Investors and analysts should treat selections as conditional, not confirmed.

What critical minerals are recoverable from coal waste?

The primary targets in these pilot projects are rare earth elements, gallium, germanium, and aluminium. The specific mix and concentration of recoverable minerals varies by coal basin and feedstock type, with Appalachian sources generally showing higher TREO concentrations and Powder River Basin material presenting a distinct elemental profile suitable for comparative research.

How does coal-based critical mineral recovery differ from conventional mining?

The extraction phase has already occurred. Coal waste feedstocks are at surface, reducing extraction costs and permitting complexity. The challenge shifts to the processing side: coal waste typically contains lower mineral concentrations than primary ore deposits, demanding highly efficient separation technologies to achieve economic recovery rates.

What is the significance of electrochemical liquid-liquid extraction?

e-LLE offers a potential alternative to conventional solvent extraction for recovering metals from dilute leach solutions. It operates at lower temperatures than smelting and may offer better selectivity in dilute feed conditions, which are common in coal waste processing. It remains at an early commercialisation stage, and the DOE pilot represents a significant real-world test of its industrial applicability.

What comes after the pilot stage?

Successful pilots are expected to qualify projects for progression toward the DOE's larger funding tier (DE-FOA-0003583), which offers up to $275 million for 1:50-scale or larger facilities. Commercial deployment beyond that level would require private capital engagement, which typically follows technology validation at TRL 7 or above.

Disclaimer: This article contains forward-looking analysis and scenario projections related to technology development, market outcomes, and policy trajectories. These scenarios involve assumptions and uncertainties that may differ materially from actual outcomes. Nothing in this article constitutes financial or investment advice. Readers should conduct their own due diligence before making investment decisions.

Want to Track the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries, turning complex critical mineral data into actionable investment insights — explore the historic returns major discoveries have generated and begin your 14-day free trial to position yourself ahead of the market.