July 14, 2026

The Global Race to Break China's Rare Earth Stranglehold

Permanent magnets are invisible to most consumers, yet they sit at the mechanical heart of every electric vehicle motor, every wind turbine generator, and a significant share of advanced defence systems. The rare earth elements that make those magnets work — primarily neodymium, praseodymium, dysprosium, and terbium — flow overwhelmingly through a single national supply chain. China controls an estimated 60% of global rare earth mining output, but its dominance over midstream separation and refining is far more absolute, exceeding 85% by most industry estimates. That concentration is not merely a trade statistic; it is a structural fragility embedded in the energy transition itself.

The question facing Western governments, development finance institutions, and industrial supply chains is no longer whether diversification is necessary. It is whether viable alternatives can be brought to commercial scale fast enough to matter. The Viridis rare earths project in Brazil represents one of the most advanced attempts to answer that question outside of China. Furthermore, understanding the broader rare earth supply chains at play helps contextualise why this project carries such strategic weight.

When big ASX news breaks, our subscribers know first

Understanding Ionic Adsorption Clay: Why Deposit Type Determines Value

What Makes IAC Mineralisation Different From Hard-Rock Deposits?

Not all rare earth deposits are created equal, and deposit type has enormous implications for processing cost, product profile, and ultimate commercial viability. The majority of non-Chinese rare earth projects under development globally are hosted in hard-rock settings — carbonatites, alkaline igneous complexes, or metamorphic terrains — that require energy-intensive crushing, grinding, and flotation before any rare earth content can be recovered.

Ionic Adsorption Clay deposits operate on an entirely different principle. In these systems, rare earth ions have been leached from parent rock over geological time through deep tropical weathering and are now loosely bound to clay mineral surfaces in a physically unconsolidated saprolite profile. Because the ions are adsorbed rather than locked within a crystal lattice, they can be mobilised using a mild leaching solution — typically ammonium sulphate or magnesium sulphate — without the need for high-temperature roasting or aggressive chemical processing.

The processing implications are significant:

- Lower energy consumption per tonne of rare earth oxide recovered compared to hard-rock equivalents

- Simpler beneficiation flowsheets that reduce capital intensity and operational complexity

- Faster pathways to a marketable mixed rare earth carbonate intermediate product

- Lower radionuclide content in many IAC systems, reducing radioactive waste management requirements

The MREO Premium: Why Magnetic Rare Earths Define Commercial Attractiveness

IAC deposits carry a second, less widely understood advantage: their rare earth profiles are disproportionately weighted toward the heavy and magnetic rare earth elements that command the highest prices and are most constrained in global supply. While light rare earth deposits like bastnäsite are globally more abundant, sources rich in dysprosium and terbium — the heavy rare earths that provide high-temperature stability to NdFeB permanent magnets — are rare outside China's Jiangxi province, where IAC mineralisation has been mined since the 1970s.

The rare earth processing challenges associated with hard-rock deposits further reinforce why IAC mineralisation offers such a compelling commercial proposition. As noted by industry analysts:

The critical distinction in rare earth project evaluation is not total rare earth oxide content alone, but the proportion of that content attributable to magnetic rare earth oxides. A deposit grading 3,000 ppm TREO with low MREO is commercially inferior to one grading 2,600 ppm TREO with a high MREO fraction, because the magnetic elements drive the bulk of realised revenue.

This is precisely why the Colossus deposit's reported MREO grade of 740 ppm within a 2,640 ppm TREO reserve grade is analytically significant. The MREO-to-TREO ratio indicates a deposit profile skewed toward the highest-value elements in the rare earth basket.

The Colossus Deposit: Scale, Grade, and Geological Context

Location and Geological Setting

The Colossus deposit sits within the Poços de Caldas Alkaline Complex in Minas Gerais, one of Brazil's most geologically distinctive regions. The complex is a deeply eroded Cretaceous alkaline intrusion spanning roughly 34 kilometres in diameter — one of the largest alkaline complexes in South America. Prolonged tropical weathering over tens of millions of years has produced thick saprolite profiles above the alkaline bedrock, creating ideal conditions for the formation of IAC-style rare earth mineralisation.

What makes this geological setting particularly compelling is that the same parent rock chemistry that generates elevated rare earth content in the bedrock — alkaline magmas are naturally enriched in incompatible elements including the rare earths — also concentrates the heavy rare earth fraction during the weathering and ion-exchange processes that form the clay horizon. The result is an IAC deposit with a rare earth basket profile more reminiscent of Jiangxi-style mineralisation than most non-Chinese deposits.

Resource and Reserve Metrics

| Project Metric | Reported Figure |

|---|---|

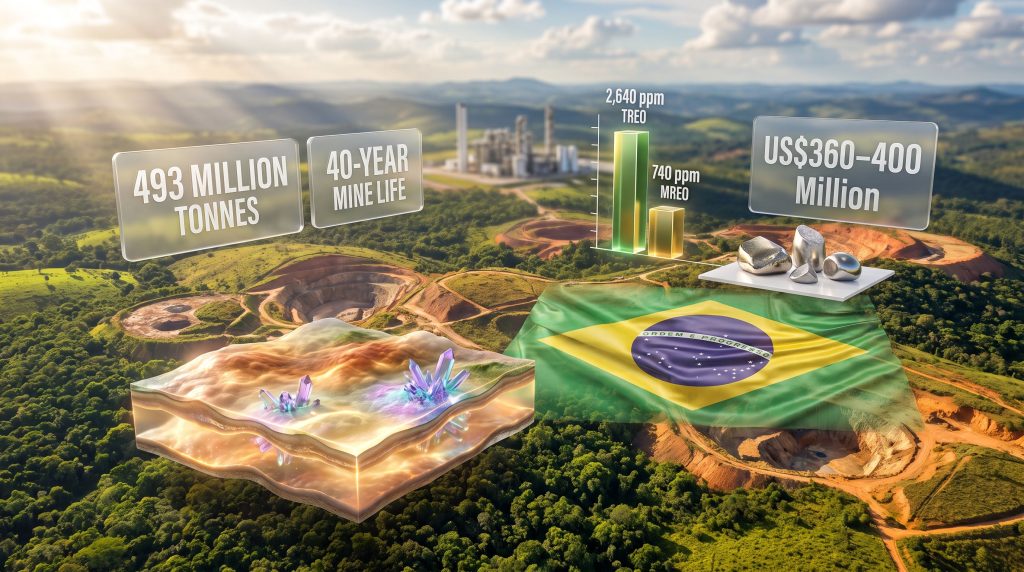

| Total Mineral Resource | 493 million tonnes |

| Resource Grade (TREO) | 2,508 ppm |

| Maiden Ore Reserve | 200.6 million tonnes |

| Reserve Grade (TREO) | 2,640 ppm |

| Reserve Grade (MREO) | 740 ppm |

| Projected Mine Life | 40 years |

| Total Capital Requirement | US$360–400 million |

The conversion of 200.6 million tonnes of the resource into a maiden Ore Reserve is a materially important milestone. An Ore Reserve, prepared under JORC or equivalent internationally recognised reporting standards, incorporates modifying factors including mining, metallurgical, economic, infrastructure, and permitting considerations. It is the figure that debt financiers and offtake counterparties use as the foundation for project bankability assessments.

A 40-year mine life based on the reserve alone is exceptional by any benchmark in the rare earth sector, where many projects struggle to demonstrate more than 20 to 25 years of reserve-supported production. That longevity materially de-risks long-term offtake commitments and improves debt tenor negotiating positions with project finance lenders.

Capital Structure and Financing Progress

The $360–400 Million Investment Stack

Bringing the Viridis rare earths project in Brazil to production requires between US$360 million and US$400 million in total capital. The financing architecture assembled to date draws on multiple instruments from distinct capital pools:

| Financing Instrument | Provider | Quantum |

|---|---|---|

| Joint Development Support Plan | BNDES / FINEP (Brazil) | Up to R$5 billion (~US$903 million program) |

| Debt Facility | Export Finance Australia | Up to A$77 million |

| Strategic Equity Investment | ORE Investments and Régia Capital | US$30 million |

Several dimensions of this financing structure merit attention beyond the headline numbers. Brazil's national development bank BNDES and its innovation financing arm FINEP operate a joint program with a total envelope of up to R$5 billion. Viridis's selection into this program is a meaningful validation of the project's technical and commercial credentials within Brazil's institutional framework, though it represents program-level capacity rather than a committed project-specific disbursement at this stage.

Export Finance Australia's involvement reflects a broader pattern of allied-nation export credit agencies providing concessional or sub-commercial debt to underpin critical mineral supply chains outside their home countries. Australia's strategic interest is traceable to the involvement of Australian-linked entities in the project's corporate structure, combined with the broader national interest in establishing non-Chinese rare earth supply chains. The American rare earth supply chain faces similar pressures, reinforcing why allied nations are actively co-investing in projects like Colossus.

The US$30 million strategic equity commitment from ORE Investments and Régia Capital addresses near-term development expenditure requirements and signals private sector conviction in the project's trajectory. However, the gap between committed financing and total capital requirement remains the critical variable for achieving Final Investment Decision.

Development Timeline and Key Milestones

The pathway from current development stage to first commercial production involves a sequenced set of technical, regulatory, and financial milestones:

- Q1 2026: The CPTR demonstration plant becomes operational, producing mixed rare earth carbonate at 100 kg per hour throughput. This rate validates the scalability of the processing flowsheet at a scale meaningful for commercial plant design extrapolation.

- May 2026: Submission of the Installation Licence application to Brazilian environmental authorities, triggering the second stage of the three-stage licensing process.

- H2 2026: Final Investment Decision targeted, contingent on financing close and regulatory approvals proceeding on schedule.

- Q3 2026: Installation Licence approval targeted from the relevant state environmental agency.

- 2028: First commercial production expected, with a ramp-up period to nameplate capacity anticipated over the following 12 to 24 months.

The demonstration plant's role extends beyond technical validation. At 100 kg per hour of mixed rare earth carbonate output, the CPTR facility generates real product that can be provided to prospective offtake counterparties for qualification testing within their own supply chains. Western magnet manufacturers and EV original equipment manufacturers require extensive qualification periods before committing to new suppliers, and demonstration plant product is the starting point for that process.

Processing Strategy and the Viridion Joint Venture

From Ore to Separated Oxide: Why Integration Determines Margin

Mixed rare earth carbonate is an intermediate product. While it can be sold, the price differential between carbonate and fully separated individual rare earth oxides is substantial. Historically, the separation margin has been captured almost exclusively by Chinese processors, who control the global separation and refining infrastructure. Projects that sell carbonate to Chinese intermediaries effectively transfer a significant portion of their potential revenue to the very supply chain they are nominally diversifying.

The Viridion joint venture between Viridis and Ionic Rare Earths addresses this structural issue directly. Viridion is designed to provide Brazil-based separation, refining, and recycling capacity, creating a vertically integrated value chain that retains margin within the project economics. Viridis Mining and Minerals has been deliberate in pursuing this downstream integration strategy from an early stage of project development.

The joint venture's planned 30 tonne per annum magnet recycling facility adds a dimension increasingly valued by Western buyers: circular economy credentials. As the EU's Critical Raw Materials Act and equivalent US frameworks begin incorporating recycled content requirements into procurement specifications, projects that can demonstrate both primary and secondary supply capability occupy a strategically superior market position.

The Price Architecture of Rare Earth Integration

To understand why downstream integration matters economically, consider the approximate price structure across the value chain for NdPr oxide:

- NdPr mixed carbonate (expressed as oxide equivalent): typically priced at a significant discount to separated oxide, reflecting processing risk and further capital requirements

- Separated NdPr oxide: the benchmark price quoted in market reporting, representing the fully refined product used directly by magnet manufacturers

- NdFeB magnet alloy: commands a further premium reflecting alloying and casting expertise

Projects that reach separated oxide status capture a materially larger share of the value chain than carbonate-only producers. For a deposit of Colossus's scale and longevity, the cumulative revenue differential over a 40-year mine life from integration versus carbonate sales is measured in billions of dollars.

The next major ASX story will hit our subscribers first

Offtake Strategy: Deliberately Excluding Chinese Buyers

One of the more strategically consequential decisions embedded in the Viridis project's commercial framework is the explicit exclusion of Chinese entities from offtake negotiations. This is not merely a geopolitical posture; it is a deliberate market positioning strategy designed to align the project with Western critical mineral security frameworks. In addition, China's export restrictions on rare earths have significantly accelerated Western appetite for alternative sources like Colossus.

The practical effect is that Viridis is negotiating with a buyer universe that includes:

- US and European magnet manufacturers seeking to establish non-Chinese rare earth supply lines ahead of anticipated regulatory requirements

- Electric vehicle OEMs under pressure from domestic content rules embedded in frameworks like the US Inflation Reduction Act

- Defence supply chain participants subject to restrictions on sourcing from foreign entity of concern-linked suppliers

This buyer base is willing to pay a premium for supply chain provenance, ESG certification, and jurisdictional stability. Brazil's combination of democratic governance, established mining law, and institutional infrastructure compares favourably to many competing rare earth jurisdictions in Africa and Central Asia on these criteria.

Environmental Licensing: Brazil's Three-Stage Framework

Brazil's environmental licensing system for mining projects operates through three sequential approvals:

- Preliminary Licence (Licença Prévia): Confirms the project's environmental viability in principle and approves the environmental impact study. Viridis received this approval in December 2025.

- Installation Licence (Licença de Instalação): Permits physical construction to commence. Application submitted May 2026, with approval targeted for Q3 2026.

- Operating Licence (Licença de Operação): Authorises the commencement of commercial operations. Required before first production in 2028.

The Preliminary Licence is the most substantive of the three approvals because it requires a full environmental impact assessment and public consultation process. Its successful completion significantly reduces the regulatory risk profile for the Installation and Operating Licences, which are more narrowly scoped reviews of construction and operational plans respectively.

Risk Matrix: What Could Derail the Timeline?

Key Uncertainties Facing the Project

Investors and stakeholders evaluating the Viridis rare earths project in Brazil should be aware of several categories of material risk.

Financing execution risk remains the most proximate challenge. The gap between confirmed financing commitments and total capital requirement must be closed before FID can be declared. Junior mining sector equity market conditions, rare earth price movements, and the pace of permitting progress all influence the attractiveness of the project to prospective equity investors.

Permitting timeline risk is inherent in any large-scale mining project in a jurisdiction with multi-agency environmental oversight. Installation Licence delays beyond Q3 2026 would push FID and consequently first production into later periods.

Commodity price risk affects both project NPV and debt serviceability. NdPr oxide prices have experienced significant volatility over the past decade, ranging from below US$40/kg to above US$120/kg. Project economics must remain robust across a realistic price range, not merely at consensus forecasts.

Technical scale-up risk is inherent in the transition from 100 kg per hour demonstration throughput to commercial-scale processing. IAC processing flowsheets that perform well at pilot scale can encounter challenges related to clay mineralogy variability, leach solution management, and raffinate disposal at full commercial volumes.

Disclaimer: The above represents an analytical framework for risk assessment and does not constitute financial advice. Investors should conduct independent due diligence and consult qualified financial advisers before making investment decisions related to any mining project or associated securities.

Brazil's Structural Advantages as a Rare Earth Jurisdiction

Brazil holds the world's second-largest rare earth reserves by most geological survey estimates, yet has historically been a negligible producer relative to its resource endowment. The gap between geological potential and production reality reflects decades of insufficient processing infrastructure, limited development finance, and the competitive suppression of non-Chinese rare earth prices through the 1990s and 2000s.

The current environment is structurally different. The critical minerals demand surge across clean energy and defence sectors has fundamentally altered the economics of developing new supply. Furthermore, US-China trade tensions and China's use of rare earth export controls as a geopolitical instrument — most recently through expanded export licensing requirements implemented across 2023 to 2025 — have created sustained demand from Western buyers for supply chain alternatives.

Brazil's advantages in this context include:

- Established legal frameworks for foreign mining investment

- Domestic development finance capacity through BNDES and FINEP

- Geographic proximity to Atlantic shipping routes serving both European and US East Coast markets

- An existing industrial base in Minas Gerais with experience in mineral processing and chemical manufacturing

Frequently Asked Questions

What is the Viridis rare earths project in Brazil?

The Viridis rare earths project is centred on the Colossus Ionic Adsorption Clay deposit located within the Poços de Caldas Alkaline Complex in Minas Gerais, Brazil. It is described as the largest undeveloped IAC rare earth deposit outside China, with a mineral resource of 493 million tonnes grading 2,508 ppm TREO and a maiden Ore Reserve of 200.6 million tonnes grading 2,640 ppm TREO. The project is currently in advanced development, targeting Final Investment Decision in H2 2026 and first commercial production in 2028.

What rare earth elements does the Colossus deposit produce?

The primary value-driving elements are the magnetic rare earths: neodymium and praseodymium (collectively NdPr) and dysprosium and terbium (collectively DyTb). NdPr is the dominant rare earth in NdFeB permanent magnets by mass, while DyTb provides thermal stability and coercivity enhancement, enabling magnets to function at the elevated temperatures experienced in EV motors and wind turbine generators.

When will the Viridis project begin production?

First commercial production is targeted for 2028, following a Final Investment Decision expected in H2 2026. The ramp-up period to nameplate capacity is anticipated to extend over 12 to 24 months from first production.

What financing has been secured for the project?

Confirmed financing instruments include selection into the BNDES/FINEP Joint Development Support Plan (program capacity up to approximately US$903 million), an Export Finance Australia debt facility of up to A$77 million, and a US$30 million strategic equity investment from ORE Investments and Régia Capital. The gap between these commitments and the total US$360–400 million capital requirement remains to be closed ahead of FID.

Strategic Outlook: A Test Case for Western Rare Earth Ambition

The Viridis rare earths project in Brazil occupies a unique position in the global critical minerals landscape. Its combination of deposit scale, IAC mineralisation quality, MREO-weighted rare earth basket, integrated downstream strategy through Viridion, and explicit Western-market offtake orientation makes it one of the most structurally complete non-Chinese rare earth development stories currently in the public domain.

Whether it successfully converts that structural completeness into operating reality depends on execution across financing, permitting, and technical scale-up domains that remain partially open. The H2 2026 Final Investment Decision target is achievable but not guaranteed, and the path from FID to first production in 2028 carries the typical execution risks of any large greenfield mining and processing project.

What is already evident is that the Colossus deposit's development would validate Brazil not merely as a rare earth mining jurisdiction, but as a potential hub for the full rare earth value chain from extraction through separation and recycling. That demonstration effect, if achieved, extends well beyond the boundaries of a single project. Consequently, Reuters reporting on Viridis confirms the company's CEO has emphasised the project's commitment to supplying US and European buyers exclusively — a positioning that underscores the project's strategic significance for Western supply chain resilience.

Want to Stay Ahead of the Next Major Mineral Discovery?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, delivering instant alerts on significant mineral discoveries — including critical and rare earth minerals driving the global energy transition — so subscribers can identify actionable opportunities before the broader market reacts. Explore historic discoveries and their returns to understand the potential scale of these opportunities, then begin a 14-day free trial at Discovery Alert to position yourself ahead of the market.