June 15, 2026

The Paradox of Power: Why Africa's Richest Energy Nation Has Some of Its Darkest Homes

Energy poverty rarely stems from a lack of resources. Across history, the most resource-abundant nations have often struggled most acutely with translating raw natural wealth into functional infrastructure for their own citizens. The Democratic Republic of the Congo represents perhaps the most striking example of this paradox anywhere on Earth. It sits atop one of the most extraordinary hydropower endowments ever measured, yet millions of its people live without reliable electricity. Understanding why this gap persists, and whether the DRC energy strategy to expand electricity access can finally close it, requires examining not just policy documents but the deeper institutional, financial, and technical conditions that determine whether reform translates into results.

When big ASX news breaks, our subscribers know first

A Resource Endowment Without Parallel, an Access Rate Without Precedent

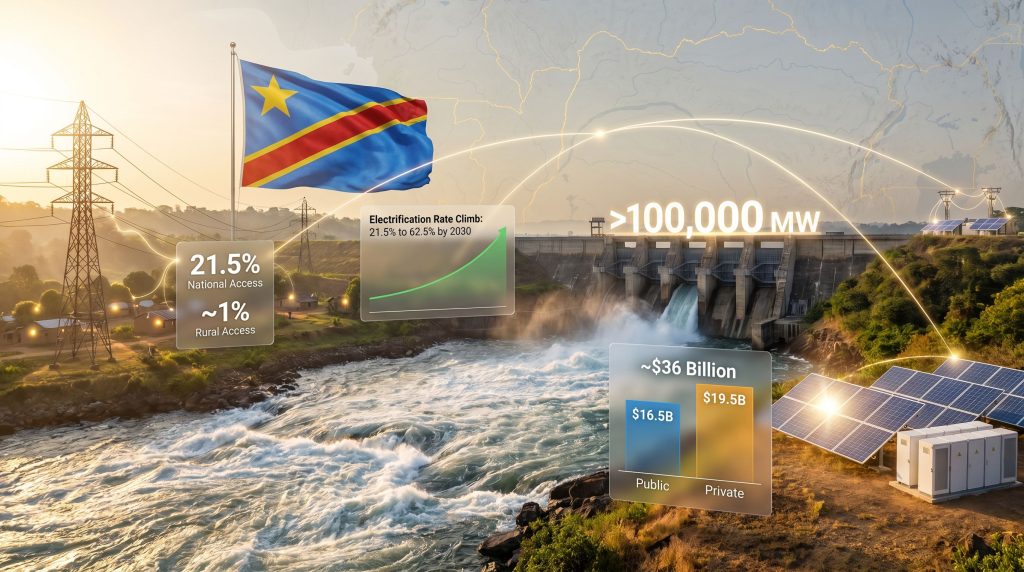

The numbers surrounding the DRC's energy potential are almost difficult to process at scale. The country holds an estimated 13% of global hydropower potential, with a total developable capacity exceeding 100,000 MW. The Inga site on the Congo River alone carries an estimated 40,000 MW of developable capacity, making it one of the largest single energy sites identified anywhere in the world. To put that in perspective, the entire installed generation capacity of South Africa, the continent's most industrialised economy, sits at roughly 58,000 MW across all fuel types.

Yet the national electrification rate in the DRC stands at approximately 21.5%, less than half the sub-Saharan African average of around 48%. In rural areas, the situation is far more severe, with some assessments placing rural access as low as 1%. This is not a geography-is-destiny argument. It is a governance, financing, and institutional failure argument.

| Metric | DRC | Sub-Saharan Africa Average |

|---|---|---|

| National Electrification Rate | ~21.5% | ~48% |

| Rural Electrification Rate | ~1% | ~28% |

| Installed Generation Capacity | ~2,800 MW | Varies |

| Operational Output (SNEL) | ~2,100 MW | — |

| Unmet Mining Sector Demand | >1,500 MW | — |

| Hydropower Potential | >100,000 MW | — |

The gap between resource wealth and citizen access is not accidental. It reflects decades of underinvestment in transmission and distribution infrastructure, chronic underperformance by the state utility, weak regulatory frameworks that have discouraged private capital, and financing structures that have never been designed to reach the populations furthest from existing grids. The broader DRC natural resources picture, furthermore, makes this disparity all the more striking given the country's extraordinary endowment.

How Electricity Scarcity Ripples Through the Entire Economy

The state-owned utility SNEL currently delivers approximately 2,100 MW against an installed capacity of roughly 2,800 MW. That gap between installed and operational output signals something deeper than a generation problem. It reflects persistent failures in operations, maintenance, and technical management that no amount of new generation capacity alone can solve.

The mining sector illustrates the cascading economic consequences most clearly. The DRC is among the world's most significant producers of copper and cobalt, two minerals central to global energy transition supply chains. Consequently, the relationship between critical minerals and energy security becomes especially pronounced here, where unmet electricity demand from mining operators alone exceeds 1,500 MW, forcing multiple companies to import power from Zambia, Tanzania, and the Republic of the Congo.

This is a structurally perverse situation: a country exporting the minerals that power global clean energy technologies cannot generate enough electricity to run the mines extracting them. The economic multiplier effects extend far beyond mining. Energy poverty suppresses manufacturing viability, limits cold chain infrastructure for agriculture, constrains healthcare delivery, and caps educational outcomes through inadequate lighting and digital connectivity.

The National Energy Policy: Reform Architecture and What It Actually Mandates

The revised National Energy Policy, known by its French acronym PNE, was formally adopted on June 12, 2026, during the 92nd session of the Council of Ministers. The policy was presented by Minister of Water Resources and Electricity Aimé Sakombi Molendo and represents the culmination of a reform process initiated in 2020, aligned with sector reforms adopted in 2025 and with the country's National Energy Compact commitments.

The PNE is not a standalone document. It functions as a unifying framework intended to bring coherence to a fragmented set of reform initiatives that have developed at varying speeds across different ministries and regulatory bodies. Its core mandate covers four interconnected domains:

- Grid rehabilitation and expansion in technically and economically viable corridors

- Decentralised renewable energy deployment for underserved and remote communities

- Regulatory reform to attract and sustain private investment

- Regional energy partnerships to diversify supply and reduce import dependence

The Headline Target: A Sixfold Acceleration in Annual Electrification Rate

The PNE's most ambitious commitment is raising the national electrification rate from 21.5% to 62.5% by 2030 under the National Energy Compact framework. Achieving that target requires increasing the annual electrification rate from approximately 1% per year to over 6% per year. That is not a marginal improvement. It is a structural transformation in deployment velocity that few developing economies have achieved under comparable starting conditions.

Achieving the 62.5% electrification target by 2030 demands not just capital deployment but a fundamental restructuring of how the DRC licences, finances, and operates energy projects at both grid and off-grid levels.

Whether this trajectory is realistic depends heavily on conditions that are not yet in place, particularly the regulatory environment improvements needed to unlock private capital at scale. In addition, considerations around natural capital in mining will shape how responsibly this expansion integrates with the country's broader environmental commitments.

Financing a $36 Billion Electrification Agenda: The Capital Stack Explained

The estimated total financing requirement to execute the DRC energy strategy to expand electricity access is approximately $36 billion. The government has committed roughly $16.5 billion from public sources, while the remaining $19.5 billion is expected to come from private investment. That private component represents more than 54% of total required financing, which means the entire strategy is structurally dependent on the DRC's ability to create conditions attractive enough for private capital to deploy at unprecedented scale.

| Financing Source | Amount | Share of Total |

|---|---|---|

| Public Sector Commitment | ~$16.5 billion | ~46% |

| Private Investment Target | ~$19.5 billion | ~54% |

| Total Required | ~$36 billion | 100% |

What Private Investors Actually Need to Commit Capital

Private capital in energy infrastructure does not flow toward opportunity alone. It flows toward bankable projects, defined by predictable revenue streams, enforceable contracts, and credible risk mitigation. The PNE explicitly identifies improvements to the legal and regulatory environment as central to attracting private operators, focusing on several key reform areas:

- Clearer and more transparent concession frameworks for energy project developers

- Improved financing mechanisms for renewable energy projects, including blended finance structures

- Streamlined licensing and permitting procedures that reduce project development timelines

- Stronger legal protections for private investment and enforceable off-take agreements

- Tariff frameworks that allow cost recovery without creating consumer affordability crises

Without progress on these dimensions, the private capital component, which represents the majority of the financing plan, will remain structurally inaccessible regardless of the policy commitments on paper.

Existing Programmatic Support Frameworks

Several multilateral and international programmes are already operating within the DRC's energy sector, providing both capital and institutional support:

- World Bank EASE Project: focuses on distributed renewable energy solutions and sector capacity building

- National Mini-Grids Programme: targets underserved communities with decentralised energy infrastructure

- SEforALL UEF Mini-Grid Programme: provides financing and technical support for mini-grid deployment across the country

- Electrifi RDC Programme: launched in May 2026 with $17.4 million in EU-backed funding to finance small-scale renewable projects in underserved areas

These programmes collectively represent meaningful momentum. However, their combined scale remains far below what the $36 billion strategy requires. They function more as proof-of-concept and institutional capacity builders than as the primary financing vehicles for national electrification. According to the World Bank's DRC electricity access report, closing the DRC's electricity gap will require sustained and co-ordinated investment across public and private channels at a scale that has not yet been demonstrated.

Technology Pathways: The Dual-Track Deployment Model

The PNE adopts a deployment architecture that runs two tracks simultaneously rather than sequencing grid expansion before decentralised solutions. This is a significant policy design choice with real implications for deployment speed and capital efficiency.

Track 1 focuses on rehabilitating and expanding the national grid in corridors where population density and economic activity make grid extension financially viable. This includes upgrading transmission infrastructure and improving SNEL's operational performance so that existing installed capacity can actually be utilised.

Track 2 prioritises distributed renewable systems for faster electrification in remote and underserved areas. World Bank and sector assessments consistently recommend off-grid solar, mini-grids, and mid-sized hydropower near demand centres as more cost-effective and faster to deploy than large-scale grid extension in low-density environments. The role of renewable energy for mining operations within this framework is, furthermore, becoming an increasingly compelling model for anchor-load investment.

The Kamoa-Kakula Solar Project: A Private Renewable Blueprint

In February 2026, the Electricity Sector Regulatory Authority (ARE) approved a project by CrossBoundary Energy to construct a 233 MWp solar power plant with integrated battery storage to supply the Kamoa-Kakula mining complex in Lualaba province. This approval is significant beyond its headline capacity figure.

It demonstrates that large-scale private renewable energy investment can be structured, approved, and financed within the DRC's existing regulatory environment. It also points toward an underappreciated dynamic in African energy development: mining operations, with their large and predictable electricity loads, can function as anchor off-takers that make renewable projects financially viable. Once that anchor load is secured, surplus capacity and associated infrastructure can create spillover benefits for surrounding communities at marginal additional cost.

Mini-Grids and Off-Grid Solar: The Rural Electrification Engine

For the roughly 1% of rural Congolese currently with electricity access, decentralised solutions are not a complement to grid expansion. They are the primary viable pathway. Mini-grid economics offer lower upfront capital requirements, faster deployment timelines, and modular scalability that grid extension in low-density areas simply cannot match.

Sustaining these markets over time requires more than installation. Standardised tariff frameworks, consumer financing mechanisms, and after-sales service networks are essential to prevent the common failure pattern in African off-grid markets where systems are deployed but become non-functional within a few years due to maintenance gaps. The broader mining decarbonisation benefits argument also reinforces the case for integrating clean distributed energy into DRC's industrial electrification planning.

The next major ASX story will hit our subscribers first

Regional Power Partnerships: Strategic Opportunity and Execution Risk

Inga 3: Transformative Potential, Decades of Delay

The DRC continues active discussions with South Africa regarding the Inga 3 hydropower project. The broader Grand Inga development has faced repeated delays spanning decades, attributable to financing gaps, governance challenges, evolving political priorities, and the sheer complexity of structuring a project at that scale with multiple international off-takers.

The current policy environment has not yet created the institutional conditions necessary to move Inga 3 decisively beyond the planning stage. Its inclusion in the DRC energy strategy to expand electricity access signals continued political commitment, but independent energy analysts have consistently noted that the project's realisation depends on factors that extend well beyond any single national policy document.

The Angola-DRC Interconnection: A Bilateral Power Trade with Continental Significance

A more near-term and potentially more executable regional development is the bilateral power interconnection project under discussion between the DRC and Angola. Angola holds an estimated 4,000 MW power surplus, a portion of which could be exported to the DRC under the proposed arrangement. This project could become one of the longest electricity transmission links on the African continent.

The strategic importance of this interconnection extends beyond megawatt figures. It begins to shift the DRC's position in regional energy trade from a net importer, currently drawing power from Zambia, Tanzania, and the Republic of the Congo, toward a more balanced participant in a functioning southern and central African power market. According to Africa Energy Portal data, the DRC's regional energy trade relationships are evolving rapidly as neighbouring nations reassess their own surplus and deficit positions.

| Partnership | Type | Status | Potential Capacity |

|---|---|---|---|

| DRC – South Africa (Inga 3) | Hydropower Export | Under Negotiation | Up to 40,000 MW (site potential) |

| DRC – Angola | Power Interconnection | Advanced Discussions | ~4,000 MW (Angola surplus) |

| DRC – Zambia | Import Arrangement | Active | Undisclosed |

| DRC – Tanzania | Import Arrangement | Active | Undisclosed |

| DRC – Republic of Congo | Import Arrangement | Active | Undisclosed |

Structural Barriers That Could Determine Whether the PNE Delivers

Utility Reform Is a Prerequisite, Not a Parallel Track

SNEL's delivery of only 2,100 MW against 2,800 MW of installed capacity is more than an operational inconvenience. It represents a fundamental constraint on the credibility of grid-based electrification plans. Any strategy that expands grid infrastructure without simultaneously reforming SNEL's operational management risks replicating the existing pattern: installed capacity that cannot be effectively utilised.

The regulatory authority ARE also faces capacity constraints. To meet 2030 targets, ARE must be equipped to process, approve, and monitor a volume of energy project applications that is categorically higher than historical norms. Institutional capacity building within the regulator is not a secondary concern but a rate-limiting factor in the entire reform programme.

Investment Risk and Contract Enforceability

The $19.5 billion private capital target presupposes a level of investor confidence that requires demonstrated progress on contract enforceability, concession security, tariff stability, and political risk mitigation. These are not conditions that can be created by policy declaration. They are built through track record, institutional credibility, and the accumulation of successfully executed projects that demonstrate the DRC can be a reliable counterparty for long-term energy infrastructure investment.

Logistics and Supply Chain Constraints

The DRC's geographic scale, combined with limited road and transport infrastructure in many regions, creates significant logistical barriers to equipment deployment. Shipping solar panels, battery storage systems, and mini-grid components to remote communities requires supply chain development that must be treated as part of the electrification implementation framework, not as an afterthought to be resolved project by project.

Key Statistics at a Glance

| Indicator | Value |

|---|---|

| DRC Hydropower Potential | >100,000 MW |

| Inga Site Capacity Potential | ~40,000 MW |

| Current National Electrification Rate | ~21.5% |

| 2030 Electrification Target | 62.5% |

| Required Annual Electrification Rate | >6% per year |

| Total Financing Required | ~$36 billion |

| Public Sector Financing | ~$16.5 billion |

| Private Investment Target | ~$19.5 billion |

| SNEL Operational Output | ~2,100 MW |

| SNEL Installed Capacity | ~2,800 MW |

| Mining Sector Unmet Demand | >1,500 MW |

| Kamoa-Kakula Solar Project | 233 MWp |

| Electrifi RDC Programme Funding | $17.4 million (EU-backed) |

| Angola Power Surplus Available | ~4,000 MW |

Frequently Asked Questions: DRC Energy Strategy and Electricity Access

What is the DRC's current electricity access rate?

The national electrification rate is approximately 21.5%, with rural access estimated as low as 1% in some assessments, placing the DRC among the lowest-access nations on the continent despite holding one of the world's largest energy resource bases.

What is the DRC's electricity access target for 2030?

Under its National Energy Compact, the DRC has committed to raising the national electrification rate from 21.5% to 62.5% by 2030, requiring annual electrification deployment to accelerate from roughly 1% to over 6% per year.

How much funding does the DRC's energy strategy require?

The government estimates a total financing requirement of approximately $36 billion, comprising roughly $16.5 billion from the public sector and $19.5 billion targeted from private investment.

What is the significance of the Inga hydropower site?

The Inga site on the Congo River holds an estimated 40,000 MW of developable capacity, within a national hydropower resource base estimated at over 100,000 MW, representing approximately 13% of total global hydropower potential.

Why is the DRC currently importing electricity from neighbouring countries?

Unmet electricity demand from the mining sector alone exceeds 1,500 MW, while SNEL's operational underperformance leaves significant installed capacity unused. This forces mining operators and other industrial users to source power from Zambia, Tanzania, and the Republic of the Congo.

What decentralised energy solutions is the DRC prioritising?

The DRC energy strategy to expand electricity access prioritises off-grid solar systems, mini-grids, and mid-sized hydropower near demand centres as the primary tools for rapidly expanding electricity access in underserved areas. These are supported by multilateral programmes including the World Bank EASE project, the SEforALL UEF Mini-Grid Programme, and the EU-backed Electrifi RDC initiative.

This article is intended for informational purposes only and does not constitute financial or investment advice. All statistics and projections referenced reflect publicly available data and announced policy targets. Readers should conduct independent research before drawing conclusions about investment conditions or policy outcomes in the DRC energy sector. Forward-looking targets involve significant uncertainty and are subject to change based on political, financial, and operational developments.

Want to Track the ASX Mining Stocks Positioned to Benefit From Africa's Energy Transition?

The minerals driving the DRC's electrification ambitions — copper, cobalt, and the critical commodities underpinning global clean energy infrastructure — are the same ones generating significant discovery opportunities on the ASX. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries are announced on the ASX, transforming complex geological data into actionable insights for both traders and long-term investors. Explore historic discovery returns on Discovery Alert's dedicated discoveries page and begin a 14-day free trial to position yourself ahead of the broader market.