May 14, 2026

The Quiet Mineral Powering a Geopolitical Realignment

Supply chain architecture rarely makes headlines until it breaks. For decades, the global cobalt trade operated as a largely invisible thread connecting African mining communities to the batteries powering smartphones, jet engines, and electric vehicles. That invisibility is ending. A convergence of industrial demand growth, concentrated geography, and strategic competition between Western and Chinese supply chain models has elevated cobalt from an obscure industrial input to one of the most contested minerals in international trade diplomacy.

The DRC-US cobalt supply chain is now at the centre of this realignment, and the commercial structures being assembled to operationalise that corridor will have consequences extending well beyond commodity markets.

When big ASX news breaks, our subscribers know first

Why One Country's Geology Shapes Global Industrial Strategy

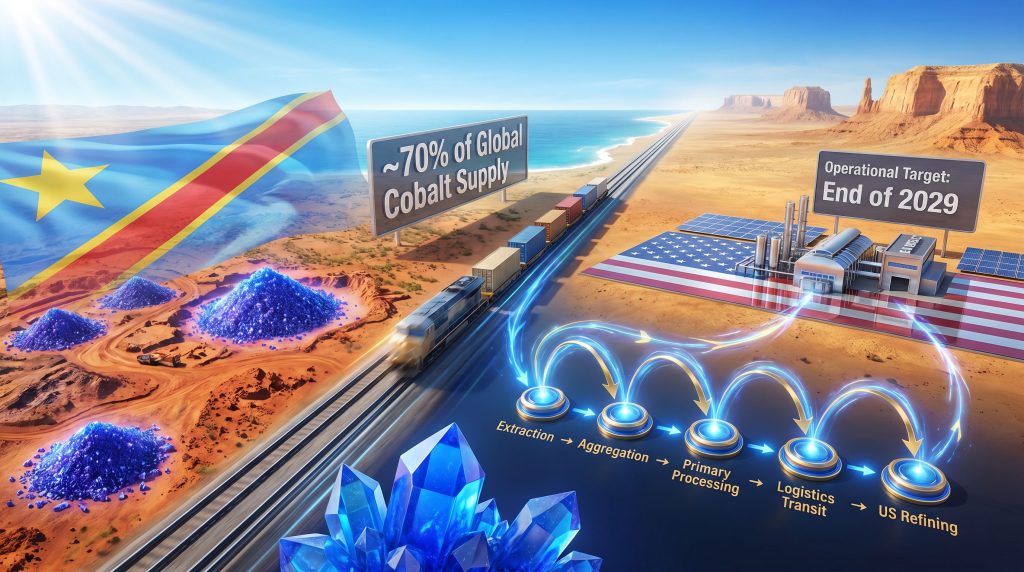

The Democratic Republic of Congo sits atop one of the most extraordinary concentrations of mineral wealth on Earth. The copper-cobalt belt stretching across the Lualaba and Haut-Katanga provinces contains cobalt deposits formed through geological processes that created sediment-hosted stratiform mineralisation over hundreds of millions of years. This geological endowment has made the DRC responsible for approximately 70% of global cobalt production, a figure that would be considered implausibly concentrated for any mineral occupying a genuinely critical industrial role.

Yet cobalt does occupy precisely that role. Its electrochemical stability makes it an essential component in the cathode chemistry of high-performance lithium-ion batteries. In nickel-manganese-cobalt (NMC) and nickel-cobalt-aluminium (NCA) formulations used in electric vehicles and aerospace-grade energy storage, cobalt contributes to thermal stability and energy density in ways that current battery chemistry has not fully replicated through substitution.

In parallel, cobalt-containing superalloys used in jet engine turbine blades and aerospace structural components retain properties at extreme temperatures that alternative materials cannot yet match at comparable cost and scale. The consequence of this combination is a mineral whose substitutability is theoretically possible but practically constrained, particularly within timeframes relevant to defence procurement and EV manufacturing expansion.

The broader critical minerals policy community increasingly treats geographic concentration not just as a market risk but as a strategic vulnerability requiring structural intervention rather than market adaptation.

What the 1976 Embargo Taught Western Governments

History provides a precise illustration of what geographic dependency looks like under pressure. During the Shaba II conflict in what was then Zaire in 1978, cobalt supply disruptions reduced US cobalt availability by an estimated 30%, triggering price spikes and forcing procurement adjustments across defence and industrial manufacturing. The episode became a reference case in US strategic minerals thinking, informing stockpile policies and supply diversification discussions that persisted for decades.

The parallel to current circumstances is intentional. Policymakers citing this historical episode are implicitly arguing that the combination of geographic concentration and potential geopolitical disruption creates a structural risk requiring preemptive supply chain architecture, not reactive adjustment. Furthermore, concerns around defence critical minerals supply chains have intensified considerably in recent years, lending additional urgency to these efforts.

Mapping the Commercial Architecture of the Three-Party MoU

The memorandum of understanding signed between Trafigura, Entreprise Générale du Cobalt (EGC), and EVelution Energy in May 2026 represents an attempt to translate diplomatic frameworks into functional commercial infrastructure. The three parties occupy distinct and complementary positions across the cobalt value chain, and the structural logic of the arrangement is worth examining carefully.

| Partner | Primary Role | Key Function |

|---|---|---|

| Entreprise Générale du Cobalt (EGC) | Upstream supply and responsible sourcing | Cobalt hydroxide procurement under Congolese state mandate (est. 2019) |

| Trafigura | Midstream logistics and commercial coordination | Transportation management, marketing, and supply chain structuring |

| EVelution Energy | Downstream US-based processing | Battery-grade cobalt sulphate and alloy-grade metal production |

Each layer of this structure addresses a specific failure in the existing cobalt supply chain. EGC's state mandate closes the traceability gap at the artisanal sourcing level. Trafigura's logistics expertise addresses the inland transit challenge from the DRC's landlocked mining provinces. EVelution's Arizona facility targets the refining bottleneck that has historically required routing through Chinese processing operations.

EGC's Mandate and the Formalisation Challenge

EGC was established in 2019 under Congolese law with a specific mandate to formalise artisanal cobalt procurement within the DRC. This mandate is structurally significant because artisanal and small-scale mining (ASM) accounts for an estimated 15 to 30% of DRC cobalt production while supporting the livelihoods of over 2 million people across mining communities.

The challenge that EGC's model is designed to address involves what supply chain specialists call the traceability gap: the multiple informal intermediary layers through which artisanal cobalt passes before entering formal commercial channels. Traditional supply chains in artisanal cobalt involve at minimum four tiers, including miners, small-scale traders known locally as négociants, mineral depot operators, and processing facilities. Materials frequently bypass nominal steps entirely, creating documented opacity around provenance, labour conditions, and human rights compliance.

EGC's state-mandated aggregation model is intended to provide a legally structured collection point that brings artisanal output into a framework aligned with OECD due diligence guidelines and international responsible sourcing standards. EGC's CEO characterised the partnership as a structural milestone that creates a high-value commercial pathway for artisanal production while embedding American industrial expertise within Congolese capacity development.

This framing matters because it distinguishes the arrangement from conventional commodity trading. The inclusion of technical training programmes for EGC personnel and discussions around potential equity participation by EGC in EVelution's infrastructure signal an economic integration model with deeper institutional roots than a standard offtake agreement.

The Logistics Equation: Why the Lobito Atlantic Railway Changes the Economics

The inland geography of DRC cobalt mining creates a fundamental cost challenge. The primary mining regions around Kolwezi sit deep within the continent, requiring significant overland transit to reach port infrastructure. Historically, this transit routed through southern African corridors with variable reliability and cost structures that disadvantaged US-bound supply relative to Chinese-controlled alternatives with established logistics networks.

The Lobito Atlantic Railway corridor changes this equation by connecting the DRC's interior mining regions to an Atlantic port, meaningfully reducing inland transit distances and improving supply reliability. The railway has received significant infrastructure investment from both US and South African sources, reflecting the shared strategic interest in developing Western-aligned logistics corridors from African mineral regions. For the DRC-US cobalt supply chain, lower logistics costs and improved transit reliability directly affect the commercial competitiveness of US-bound cobalt relative to Chinese-processed alternatives.

The Five-Stage Value Chain From Mine to Market

Understanding how cobalt actually moves from an artisanal mining cooperative in Lualaba province to an EV battery pack manufactured in the United States requires mapping each stage of transformation:

- Extraction – Artisanal and industrial mining operations across the DRC's copper-cobalt belt, with artisanal miners working shallow deposits using hand tools in many locations

- Aggregation – EGC-managed collection from artisanal cooperatives and négociants, creating a state-supervised aggregation point that introduces traceability documentation

- Primary Processing – Conversion of mixed artisanal cobalt into cobalt hydroxide within the DRC, the form in which it enters international trade

- Logistics Transit – Lobito Atlantic Railway corridor transport to Atlantic port access, followed by maritime freight to the United States

- US Refining – EVelution Energy's planned Arizona facility converts cobalt hydroxide into battery-grade cobalt sulphate for EV applications and alloy-grade metal for defence and aerospace use

Construction of the Arizona facility is scheduled to begin in early 2027, with operational completion targeted toward the end of 2029. The facility is designed to process materials into two differentiated product streams, targeting the distinct technical specifications required by battery manufacturers and defence-industrial suppliers respectively.

The distinction between battery-grade cobalt sulphate and alloy-grade metal matters commercially and technically. Battery applications require precise chemical purity specifications for cathode performance, while defence superalloy applications prioritise metallurgical consistency for high-temperature performance. A facility capable of producing both optimises the economic case for domestic refining investment.

The China Bypass: Strategic Significance of Onshore Refining

The overwhelming majority of DRC cobalt has historically entered Chinese-controlled refining operations before reaching end-use manufacturers globally, including those in the United States. This processing dependency creates what strategic minerals analysts describe as a chokepoint vulnerability: even if cobalt is physically mined outside China, the value-adding transformation into usable industrial inputs flows through Chinese industrial infrastructure.

The Congolese cobalt rivalry between Western and Chinese-aligned supply chain models is consequently less about who controls mining rights and more about who controls refining capacity. The EVelution facility, when operational, would represent a Western-aligned refining node capable of converting DRC hydroxide directly into US-market-ready products without routing through Chinese processing. When considered against the backdrop of the broader Minerals Security Partnership coordinating Western-aligned supply chain development, the Arizona facility's strategic positioning extends beyond its output volumes.

The MoU states that the initiative could potentially address around 40% of US national cobalt requirements, pending finalisation of definitive commercial agreements. This figure, while conditional, provides an indication of the intended scale relative to total US consumption across aerospace, defence, and EV applications.

Governance Frameworks and the Limits of Responsible Sourcing

The DRC-US cobalt supply chain operates within, and in some respects alongside, a complex ecosystem of existing governance frameworks. Understanding where the Trafigura-EGC-EVelution structure differs from these frameworks clarifies its strategic distinctiveness.

| Framework | Operator | Primary Focus |

|---|---|---|

| Responsible Minerals Initiative (RMI) | Industry coalition | Supply chain due diligence and transparency standards |

| Cobalt Action Partnership (CAP) | World Economic Forum | Industry standards for artisanal cobalt aligned with DRC law |

| Global Battery Alliance (GBA) | Multi-stakeholder | Battery supply chain coordination and certification |

| USAID Partnership Programme | US Government | EGC capacity building and artisanal formalisation piloting |

A $2 million USAID-funded pilot programme in Lualaba province has served as a proof-of-concept for responsible artisanal cobalt formalisation, involving organisations including the Fair Cobalt Alliance, Gecamines, the Responsible Minerals Initiative, GIZ-funded Cobalt 4 Development, and RCS Global Group. This pilot provides empirical evidence for what responsible sourcing at the artisanal level can look like when supported by institutional infrastructure.

The fundamental difference with the commercial MoU is structural. Governance frameworks focus on standards, reporting, and compliance verification. The three-party MoU creates a direct commercial pipeline with defined logistics infrastructure, processing endpoints, and economic integration through potential equity participation. Standards frameworks tell participants how to source responsibly. Commercial architecture determines whether responsible sourcing has a viable market to supply.

Persistent Challenges: What Governance Frameworks Identify

The OECD's due diligence guidance for mineral supply chains has identified several categories of risk that responsible sourcing frameworks must address, extending beyond the child labour monitoring that receives most public attention:

- Overlooked linkages between industrial and artisanal mining operations, including undocumented cobalt movement between the two sectors

- Insufficient scrutiny of human rights risks associated with security force involvement at mining sites

- Due diligence gaps around corruption and conflict financing risks that extend beyond child labour

- Price-elastic artisanal production volumes that complicate supply predictability and formalisation continuity

This last point deserves particular attention. Artisanal cobalt production responds to price signals: when cobalt prices rise, informal miners flood into the sector; when prices fall, they exit. This cyclical behaviour creates a structural tension between formalisation objectives, which require consistent supply relationships, and the market dynamics of a commodity prone to significant price volatility. The DRC cobalt export ban introduced earlier in 2025 added further complexity to this picture, underscoring how policy decisions can rapidly reshape supply availability. Commercial agreements structured through this corridor will consequently need to account for these cycles to maintain viability across cobalt price downturns.

What the 2029 Timeline Means for US Industrial Strategy

The EVelution facility's completion target of late 2029 sits within a specific industrial and geopolitical context. US EV adoption trajectories, defence procurement modernisation timelines, and the competitive dynamics of the broader critical minerals contest between Western-aligned and Chinese-aligned supply chains all converge around a mid-decade inflection point.

Whether the 2029 operational date is fast enough to meaningfully influence these dynamics depends on several factors:

- The pace at which US EV manufacturers seek to diversify away from cobalt sourced through Chinese refining

- The timeline for defence procurement specifications to formalise requirements for domestically processed cobalt

- The degree to which definitive commercial agreements between the three parties can be finalised in the months following the MoU signing

- The scalability of EGC's responsible artisanal sourcing model from current pilot-scale operations to volumes sufficient to supply a commercial processing facility

The cobalt export suspension earlier in 2025 demonstrated, furthermore, just how rapidly supply disruptions can propagate through downstream industries when single-source dependencies remain unaddressed. For investors and industrial planners tracking the DRC-US cobalt supply chain, these timing dependencies represent both the key risks and the central value proposition of the architecture being assembled.

Disclaimer: This article contains forward-looking statements and projections regarding commercial timelines, facility construction, and potential supply addressability. These are based on publicly available information and announced intentions as of May 2026 and are subject to change based on commercial negotiations, regulatory developments, and market conditions. Nothing in this article constitutes investment advice.

The next major ASX story will hit our subscribers first

Key Metrics: The DRC-US Cobalt Corridor in Numbers

| Metric | Figure |

|---|---|

| DRC share of global cobalt production | ~70% |

| US cobalt demand potentially addressable via MoU | ~40% (pending definitive agreements) |

| Artisanal mining share of DRC cobalt output | 15-30% |

| Livelihoods dependent on DRC artisanal cobalt mining | Over 2 million people |

| USAID funding for EGC capacity building pilot | $2 million |

| Historical US supply disruption (1978 Shaba conflict) | ~30% reduction |

| EVelution facility construction start | Early 2027 |

| EVelution facility operational target | End of 2029 |

Frequently Asked Questions

What makes the DRC-US cobalt supply chain strategically important?

The DRC supplies roughly 70% of global cobalt, and the majority of that output has historically been refined through Chinese-controlled processing before reaching Western manufacturers. Establishing a direct, Western-aligned corridor from DRC artisanal production to US-based refining reduces dependency on Chinese processing infrastructure for a mineral critical to EV batteries, aerospace superalloys, and defence applications.

What is EGC's role in responsible sourcing?

Entreprise Générale du Cobalt was established in 2019 under Congolese law with a state mandate to formalise artisanal cobalt procurement. It serves as an aggregation point that introduces traceability documentation and aligns supply with OECD due diligence standards, providing a legally structured pathway for artisanal output to enter compliant international supply chains.

Why does the Lobito Atlantic Railway matter for cobalt logistics?

The DRC's primary mining regions are landlocked, historically requiring lengthy overland transit to reach port infrastructure. The Lobito corridor connects these inland regions to an Atlantic port with improved reliability and lower transit costs, strengthening the commercial case for US-bound cobalt supply relative to established Chinese-controlled logistics alternatives.

When will EVelution's Arizona facility be operational?

Construction is scheduled to begin in early 2027, with completion targeted toward the end of 2029. The facility will produce battery-grade cobalt sulphate for EV applications and alloy-grade metal for defence and aerospace use.

What are the main risks to this supply chain initiative?

Key risks include the complexity of scaling responsible artisanal sourcing from pilot programmes to commercial volumes, cobalt price volatility affecting artisanal supply predictability, the conditional nature of the 40% demand addressability figure pending definitive commercial agreements, and the structural challenges of operating governance frameworks across the DRC's fragmented mining landscape.

Ready to Track the Next Major Mineral Discovery Before the Market Does?

Discovery Alert's proprietary Discovery IQ model scans ASX announcements in real time, instantly identifying significant mineral discoveries — from cobalt to critical minerals — and delivering actionable alerts to subscribers ahead of the broader market. Explore historic discoveries and their extraordinary returns, then begin your 14-day free trial to position yourself at the forefront of the next major find.