July 9, 2026

Economic Structural Fractures Shape Global Energy Volatility

Modern energy markets operate within increasingly interconnected systems where macroeconomic fundamentals drive price volatility across global commodity exchanges. When major oil-producing nations experience simultaneous currency devaluation, hyperinflation, and fiscal revenue contraction, the resulting supply uncertainty creates cascading effects that extend far beyond regional boundaries. Furthermore, understanding these structural economic pressures provides essential insights into current market dynamics and their implications for global energy security.

Iran's economic landscape exemplifies how multiple structural weaknesses can converge to create unprecedented challenges for both domestic stability and international energy markets. The Iran regime crisis represents more than isolated political unrest; it demonstrates how macroeconomic vulnerabilities interact with geopolitical tensions to generate systemic risks across global energy infrastructure.

When big ASX news breaks, our subscribers know first

Currency Devaluation and Hyperinflationary Dynamics

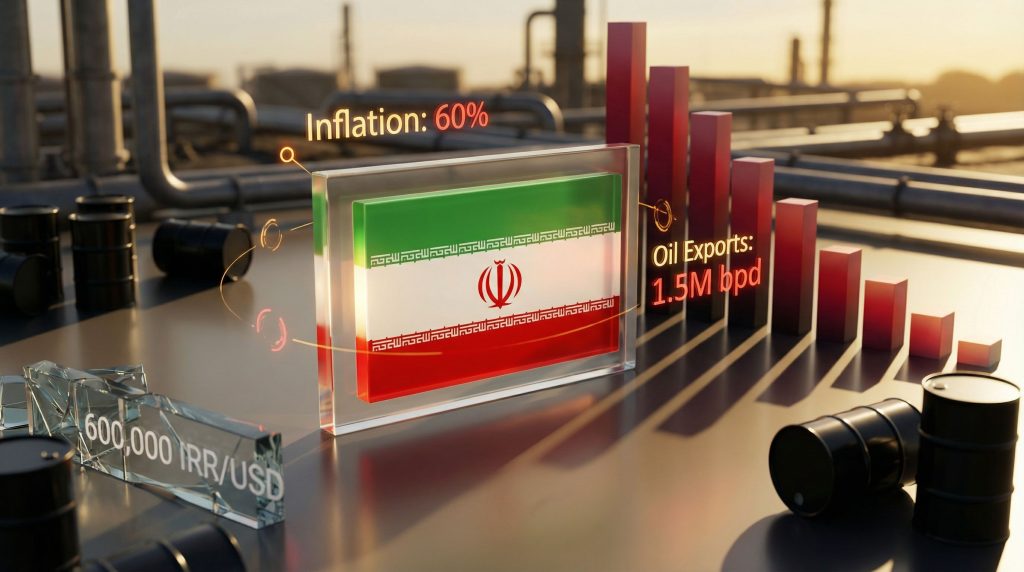

Iran's monetary system shows severe structural damage with inflation rates exceeding 45-60% while the Iranian rial experiences continuous depreciation against major currencies. Recent exchange rates indicate the rial trading at approximately 600,000 IRR per USD, representing a 50% devaluation from baseline levels of around 300,000 IRR per USD within a compressed timeframe.

This hyperinflationary environment creates destructive feedback loops where currency weakness drives import costs substantially higher, further accelerating price increases across essential goods and services. Consequently, the pass-through effect proves particularly devastating given Iran's reliance on foreign components for industrial operations and consumer goods.

Technical Mechanisms of Hyperinflation

In high-inflation environments, several interconnected mechanisms operate simultaneously:

- Import cost amplification: Foreign goods see immediate price increases when currency depreciates

- Wage-price spiral dynamics: Workers demand higher wages to maintain purchasing power, forcing businesses to raise prices further

- Dollarisation pressure: Households and businesses shift savings toward foreign currency to preserve value

- Real wage erosion: Nominal wage growth fails to keep pace with inflation rates, destroying purchasing power

The interaction between external sanctions constraints and domestic currency weakness amplifies import costs, creating conditions where essential goods become increasingly unaffordable for middle-class households. Moreover, banking channel restrictions limit access to foreign exchange markets, exacerbating currency volatility and reducing the effectiveness of monetary policy interventions.

Fiscal Revenue Erosion Under Economic Pressure

Oil export restrictions have fundamentally altered Iran's fiscal capacity, with petroleum revenues declining while domestic expenditure requirements increase due to social unrest management costs. Current oil exports operate at approximately 1.5 million barrels per day, down from pre-crisis levels of 2.5 million barrels per day, representing a 40% reduction in export capacity.

This revenue contraction creates a classic fiscal squeeze where traditional income streams contract while security and subsidy obligations expand. In addition, the government faces increasing pressure to maintain energy subsidies and social services while simultaneously funding extensive security operations across multiple regions.

Sanctions Impact on Revenue Streams

Current sanctions mechanisms operate through multiple channels:

- Primary restrictions: Direct limitations on Iran's oil exports and financial access

- Secondary enforcement: Penalties on third-party purchasers and financial institutions

- Extraterritorial application: U.S. sanctions applying to foreign entities, reducing willing export customers

- Banking channel constraints: Limited access to international financial systems

Based on current global oil prices around $65-70 per barrel, Iran's annual oil revenue has likely contracted from historical levels of $50-60 billion to an estimated $20-30 billion range. This represents a fundamental shift in fiscal capacity that constrains government operations across multiple sectors, including the Trump tariff impact on global trade relationships affecting regional partners.

Demographic Pressures and Economic Convergence

Unlike previous protest cycles, current unrest coincides with Iran's worst economic performance in decades. Youth unemployment rates have reached approximately 35%, compared to baseline levels of 25%, creating widespread discontent among educated populations seeking employment opportunities in a contracted economy.

The combination of widespread unemployment among educated youth, middle-class purchasing power destruction, and basic service deterioration creates unprecedented breadth of discontent across traditional regime support bases. Furthermore, this demographic pressure intersects with economic constraints to produce social instability that extends beyond typical political protest patterns.

Educational Mismatch and Labour Market Dynamics

Iran's demographic structure, with approximately 60% of the population under 35, creates substantial labour supply that exceeds economic demand. University graduation rates continue producing educated workers seeking employment in import-dependent retail and service sectors that have been most disrupted by sanctions and inflation.

Economic constraints prevent family formation among young adults, reducing social stability anchors and creating conditions where traditional sources of regime legitimacy no longer function effectively. Consequently, marriage and household formation delays reflect deeper structural economic problems that cannot be addressed through political measures alone.

Institutional Legitimacy Breakdown

The reformist political pathway, which historically provided hope for gradual change, has lost credibility entirely. This eliminates a crucial pressure release valve that previously channelled dissent into manageable political processes rather than street confrontations. According to reports from the 2025–2026 Iran internal crisis, security forces have reportedly been involved in situations where activist groups estimate more than 7,000 people have been killed, including numerous minors.

Government control extends to territorial administration but not to public sentiment or institutional legitimacy. However, the reliance on sustained force to address nationwide protests indicates dependence on coercion rather than consent-based governance, fundamentally altering the relationship between state and society.

Legitimacy Erosion Pathways

Multiple forms of legitimacy face simultaneous challenges:

- Performance legitimacy: Failed economic improvements destroy government credibility

- Procedural legitimacy: Elections perceived as predetermined; institutional channels seen as ineffective

- Ideological legitimacy: Revolutionary narrative exhausted after 47 years; generational replacement fails to accept founding ideology

Historical Iranian protest cycles were channelled through reformist political figures who provided negotiated outlets for dissent. Current conditions show reformist politicians detained or marginalised, with no viable political outlet emerging and security apparatus responding primarily through repression rather than co-optation.

Energy Infrastructure Vulnerability

Iran's oil production infrastructure faces dual pressures from sanctions-related maintenance challenges and potential internal disruptions or work stoppages. Current production levels remain substantially below pre-sanctions capacity, with technical degradation accelerating due to limited access to advanced equipment and specialised expertise.

Equipment aging presents ongoing challenges as Iranian oilfields rely primarily on 1970s-1990s technology, while modern extraction equipment requires Western suppliers currently under sanctions restrictions. In addition, spare parts scarcity forces periodic field shutdowns for maintenance, reducing overall production efficiency and increasing extraction costs per barrel, contributing to broader oil price movements in global markets.

Russian Partnership Development

Iran has increasingly pursued Russian technological partnerships to address capacity constraints resulting from Western sanctions limiting access to traditional equipment suppliers. These arrangements represent attempts to circumvent technology transfer restrictions while developing alternative supply chains for critical petroleum infrastructure components.

Enhanced oil recovery methods, including waterflooding and gas injection techniques, require precise equipment and monitoring capabilities that sanctions currently limit. Consequently, this constrains Iran's ability to maximise output from existing fields while accelerating infrastructure deterioration that requires substantial future capital investment.

The next major ASX story will hit our subscribers first

Regional Energy Market Implications

Iran's current instability creates uncertainty around 2.5-3 million barrels per day of potential oil supply, representing approximately 3% of global production. Market volatility increases as traders incorporate various scenarios from complete production shutdown to gradual capacity restoration under different political outcomes.

Regional energy producers and global markets reassess supply chain resilience, with increased focus on spare capacity utilisation and strategic reserve deployment. This creates upward pressure on global energy prices even without actual Iranian supply disruptions, as markets price in potential supply shock scenarios, particularly given recent concerns about US oil production decline affecting global supply balances.

Supply Chain Risk Assessment

Iran's energy exports rely heavily on specific geographic chokepoints and shipping arrangements that become increasingly vulnerable during periods of internal instability. Recent naval exercises temporarily closing sections of the Strait of Hormuz demonstrate how domestic pressures translate into regional energy security concerns.

The Strait of Hormuz carries approximately 21% of globally traded petroleum, with Iran's historical contribution representing 3-5% of global production. Furthermore, closure demonstrations reveal Iran's capacity to disrupt global energy supplies, connecting internal unrest to external market vulnerability through critical infrastructure control.

Sanctions Economics and Social Dynamics

Current sanctions achieve maximum economic impact precisely because they coincide with domestic legitimacy challenges. The regime cannot credibly attribute economic hardship solely to external pressure when internal opposition remains visible and widespread, reducing sanctions' traditional effectiveness in rallying nationalist support around leadership.

The interaction between external economic pressure and internal social breakdown creates conditions where each factor amplifies the other. Sanctions-induced economic hardship fuels protests, while protest-related instability makes sanctions relief negotiations increasingly difficult to achieve, particularly amid broader US‑China trade war impact on global economic relationships.

Economic Warfare Effectiveness

Banking channel limitations restrict Iran's ability to conduct international commerce, while currency weakness and inflation erode household savings. State revenue constraints occur simultaneously with rising costs for households facing dwindling economic opportunities, creating dual pressure on both government capacity and popular support.

This timing correlation proves significant because protest escalation from 2022-2026 coincided with post-JCPOA sanctions reimposition beginning in 2018 and global oil price volatility. Consequently, the convergence creates conditions where external pressure reinforces internal dissent rather than consolidating support around leadership.

Global Energy Security Architecture

Iran's crisis affects regional stability calculations for major energy producers, potentially influencing production and investment decisions across the Persian Gulf region. Neighbouring countries must balance energy market opportunities against regional security concerns while maintaining stable export operations.

Global strategic petroleum reserves face increased utilisation pressure as markets hedge against Iranian supply disruptions. This reduces buffer capacity available for other potential supply shocks, creating systemic vulnerability in global energy security architecture that extends beyond immediate Iranian supply concerns, particularly when considering the OPEC production impact on global supply coordination.

Alternative Supply Activation

International energy markets demonstrate increased focus on spare capacity utilisation and strategic reserve deployment as hedge against supply uncertainty. Major consuming nations reassess storage policies and alternative supplier relationships to maintain energy security amid potential supply disruptions.

Regional producers evaluate capacity expansion opportunities while considering geopolitical stability factors that could affect long-term investment planning. These calculations influence global supply availability and pricing structures independent of actual Iranian production levels.

Resolution Scenarios and Market Impact

Different political resolution scenarios create varying timelines for sanctions relief and production restoration, with market uncertainty persisting until new arrangements demonstrate stability and gain international recognition.

What Are the Potential Outcome Scenarios?

Regime continuity through repression would likely maintain current sanctions while creating long-term investment uncertainty in Iranian energy sectors. This scenario suggests continued supply constraints with gradual infrastructure degradation over extended periods.

Negotiated sanctions relief could restore Iranian oil exports to global markets, potentially adding 1-2 million barrels daily within 12-18 months. This would create downward pressure on oil prices while requiring market adjustment to increased supply availability.

Political transition scenarios involving constitutional reform or government change would create different timelines for sanctions relief and production restoration. Market uncertainty would persist until new political arrangements demonstrate operational stability and achieve international recognition. Analysis from Brookings Institution suggests various pathways for potential political transformation.

Economic Indicators and Regime Assessment

Government spending patterns on security apparatus versus social services provide key indicators of regime priorities and sustainability measures. Increased security expenditure amid declining social spending suggests short-term stability measures that may undermine long-term legitimacy and popular support.

Private sector responses to ongoing instability, including capital flight patterns and investment decisions, offer insights into elite confidence regarding regime survival prospects. Significantly, capital outflows indicate diminishing confidence among economic elites who traditionally support existing political arrangements.

How Do Fiscal Sustainability Metrics Look?

| Economic Indicator | Current Level | Pre-Crisis Baseline | Impact Assessment |

|---|---|---|---|

| Inflation Rate | 45-60% | 15-20% | Severe purchasing power erosion |

| Oil Export Volume | 1.5M bpd | 2.5M bpd | 40% revenue reduction |

| Currency Exchange Rate | 600,000 IRR/USD | 300,000 IRR/USD | 50% devaluation |

| Youth Unemployment | 35% | 25% | Critical demographic pressure |

| Government Revenue | $20-30B annually | $50-60B annually | Massive fiscal contraction |

Business community adaptation patterns reveal strategic responses to political uncertainty, with companies adjusting operations, supply chains, and investment timelines based on regime stability assessments. These private sector indicators often provide earlier signals of systemic change than official government statistics or political announcements.

Systemic Economic Pressures and Strategic Implications

Iran's regime crisis represents convergence of structural economic weaknesses, demographic pressures, and external sanctions creating unprecedented challenges for political stability. The economic dimensions extend beyond Iran's borders, influencing global energy markets, regional security calculations, and international diplomatic strategies across multiple bilateral and multilateral relationships.

The resolution of this crisis will significantly impact global energy security architecture, Middle Eastern geopolitical balance, and sanctions policy effectiveness in future international conflicts. Understanding these economic fundamentals provides essential context for assessing immediate market risks and longer-term strategic implications for global energy systems.

Current conditions demonstrate how macroeconomic vulnerabilities interact with geopolitical tensions to create systemic risks that require comprehensive analytical frameworks incorporating economic, demographic, and institutional factors. The Iran regime crisis offers crucial insights into modern challenges facing energy-dependent economies under external pressure while managing internal legitimacy challenges.

Disclaimer: This analysis is based on publicly available information and should not be considered investment advice. Economic forecasts and political assessments involve significant uncertainty, and actual outcomes may differ substantially from projected scenarios. Readers should consult multiple sources and professional advisors before making investment or policy decisions related to energy markets or geopolitical developments.

Ready to Capitalise on Global Energy Market Volatility?

Discovery Alert's proprietary Discovery IQ model instantly identifies ASX mineral discoveries that could benefit from global energy market disruptions, providing subscribers with actionable insights into energy transition opportunities before broader market recognition. Begin your 14-day free trial today to secure your market-leading advantage in commodities and energy-related investments.