July 10, 2026

The Hidden Complexity Behind Aluminium's Most Watched Recovery

The global aluminium industry is built on a paradox: it is one of the most abundant metals on Earth, yet consistent, reliable production depends on extraordinarily complex industrial ecosystems where a single disruption can cascade across multiple markets simultaneously. Unlike most commodity disruptions that affect one stage of a value chain, the forced shutdown of the Al Taweelah industrial complex in late March 2026 removed bauxite refining, electrolytic smelting, and secondary processing capacity all at once from a single geographic footprint. That multi-stage exposure is what made the March 28 event significant far beyond its immediate physical damage.

Understanding why EGA restarts alumina production at Al Taweelah matters to the broader market requires stepping back from the headline and examining what the facility actually does, how it fits into global supply architecture, and what a phased recovery of this complexity truly involves in operational terms. Furthermore, examining bauxite supply dynamics in this context helps illustrate just how interconnected upstream and downstream pressures can become during a significant production disruption.

When big ASX news breaks, our subscribers know first

Al Taweelah: A Facility Unlike Almost Any Other in the World

The Al Taweelah industrial complex in Abu Dhabi occupies a category of its own within the global aluminium industry. It integrates an aluminium smelter, a casthouse, a captive power plant, an alumina refinery, and a recycling facility within a single coordinated industrial zone inside the Khalifa Economic Zone Abu Dhabi (KEZAD). Very few aluminium producers on Earth operate this level of vertical integration at a single site.

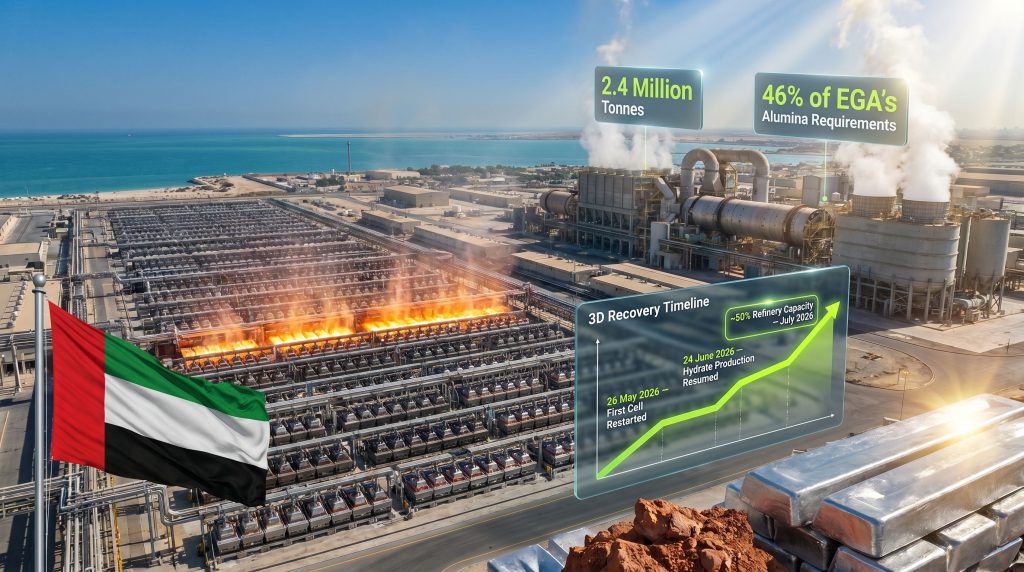

The alumina refinery, commissioned in 2019 as the first facility of its kind in the UAE, reached its designed output within approximately two years of startup. By 2025, it had exceeded nameplate expectations, producing 2.4 million tonnes of alumina annually and covering roughly 46% of EGA's total alumina requirements for its smelting operations.

The Al Taweelah smelter itself operates 1,262 aluminium reduction cells, placing it among the highest single-site electrolytic smelting capacities anywhere in the world. The scale of what was taken offline on March 28 was therefore not comparable to a typical production curtailment. It was the simultaneous removal of an upstream refinery, a mid-stream smelter, and downstream secondary processing from the global supply network.

Why Integrated Facilities Create Amplified Disruption Risk

Most commodity market participants understand that supply disruptions reduce available output. What is less commonly appreciated is how integration within a single industrial zone creates compound disruption effects that exceed the sum of their parts.

KEZAD is not simply a collection of factories sharing a postcode. It is a purpose-designed industrial and logistics ecosystem with shared utility infrastructure, including power distribution, water treatment, and port access. When the March 28 attacks struck this zone, the damage was not limited to production equipment. The disruption propagated through shared infrastructure dependencies, creating cascading operational challenges that extended well beyond direct physical damage to plant and machinery.

This is a critical nuance for anyone modelling the impact of such an event. A standalone smelter losing power for 48 hours faces a very different recovery calculus than an integrated complex losing coordinated access to port logistics, water supply, and interconnected processing circuits simultaneously.

The lesson from Al Taweelah is that geographic integration of production assets, while operationally efficient in normal conditions, concentrates vulnerability in ways that traditional single-facility risk models underestimate.

Decoding the Two-Track Recovery: Smelter and Refinery Are Not the Same Problem

One of the most important technical distinctions in understanding the Al Taweelah recovery is that the alumina refinery restart and the aluminium smelter restart represent entirely separate engineering challenges with different timelines, constraints, and risk factors. In addition, the parallel nature of these recovery tracks reflects a level of operational complexity that sets this event apart from more straightforward production stoppages.

| Facility Component | Status as of Early July 2026 | Target for Full Recovery |

|---|---|---|

| Aluminium Smelter | 89 of 1,262 reduction cells active as of 2 July 2026 | Approximately 6 months from July 2026 |

| Alumina Refinery | Hydrate production resumed 24 June; alumina targeting ~50% capacity by mid-July | Full technical capability by end of 2026 |

| Recycling Plant | Under ongoing damage assessment | Timeline subject to infrastructure review |

What Hydrate Production Resumption Actually Signals

The restart of hydrate production on 24 June 2026 was a technically significant milestone that deserves more attention than it typically receives in market commentary. Alumina refining follows a sequential chemical process:

- Bauxite digestion in hot caustic soda (sodium hydroxide) solution under pressure, dissolving aluminium-bearing minerals

- Clarification and settling to separate undissolved solids (red mud) from the sodium aluminate liquor

- Precipitation to crystallise aluminium hydroxide (gibbsite/hydrate) from the supersaturated liquor

- Calcination to drive off chemically bound water and convert hydrate to calcined alumina (Al₂O₃)

The resumption of hydrate production confirms that the first three stages of this chain have been sufficiently restored. Calcination is the final conversion step and, depending on calciner condition and thermal readiness, typically follows hydrate production by days to weeks rather than months. The June 24 milestone therefore functioned as a reliable leading indicator that alumina output was genuinely imminent rather than speculative.

The Alumina Supply Gap: Quantifying What the Market Lost

With 2.4 million tonnes of annual refinery output suspended from late March 2026, the global alumina market faced a meaningful single-source reduction during a period when supply was already navigating constraints from several directions. The disruption occurred against a background of elevated alumina prices that had been building through late 2024 and into 2025. Notably, bauxite production trends from key supplying regions had already been signalling tightening conditions well before the Al Taweelah event compounded the pressure.

EGA's internal alumina shortfall had a dual market impact that is important to understand:

- Direct supply reduction: Approximately 2.4 million tonnes of annual refinery capacity was removed from global availability.

- Indirect demand creation: EGA was simultaneously forced to enter spot and contract markets to source alumina externally, adding procurement demand at precisely the moment it was no longer contributing supply.

This dual-sided dynamic is precisely what amplifies price sensitivity in tight markets. EGA went from being a net supplier of roughly 46% of its own alumina needs to being a substantial net buyer in international markets — a swing in market positioning that few individual corporate events can replicate at that scale.

Speculative consideration: If the global alumina spot market absorbed EGA's procurement needs for approximately nine months, the cumulative price effect on short-duration spot contracts may have been considerably more pronounced than longer-term contract markets would reflect. Traders with exposure to spot alumina during this period faced structurally different conditions than those operating under long-term pricing arrangements.

How the Recovery Timeline Compares to Industry Benchmarks

Aluminium smelter restarts following extended cold shutdowns are among the most technically demanding recovery operations in the metals industry. The core challenge centres on reduction cell cathode integrity. Comparable examples of aluminium operations recovery elsewhere in the world demonstrate just how demanding these processes can be, even when disruption is less severe than what Al Taweelah experienced.

When an electrolytic reduction cell is shut down, the molten bath of cryolite and aluminium solidifies. The frozen mass contracts at different rates from the surrounding cathode lining, creating mechanical stress that can cause cracking, spalling, or delamination of the carbon cathode blocks. Cells that have been cold for extended periods cannot simply be reheated and restarted. They must be carefully inspected, and those with compromised cathode linings must be relined before restart.

Relining a single reduction cell is not a quick process. Depending on contractor availability, cathode material supply, and curing requirements, relining a cell typically takes several weeks. Across a facility with 1,262 cells, the sequencing, prioritisation, and resource allocation decisions involved in managing the restart programme represent an enormous operational undertaking.

Industry precedent suggests that large-scale smelter restarts following extended outages require 6 to 18 months for full capacity recovery, with the specific timeline shaped by:

- The proportion of cells requiring relining versus simple restart

- The availability of anode carbon supply

- External alumina procurement to support partial smelter operation during refinery recovery

- Utility and infrastructure stability during the restart sequence

EGA's trajectory, with the original estimate of approximately 12 months now appearing achievable within roughly 6 months from July 2026, represents a recovery pace at the more capable end of what industry experience would predict for a facility of this scale.

The next major ASX story will hit our subscribers first

Structural Market Consequences as Production Normalises

As EGA restarts alumina production at Al Taweelah and progressively restores smelter capacity, the market implications are meaningful across several dimensions. Consequently, both upstream and downstream participants will need to reassess supply planning assumptions as output levels climb.

For alumina markets:

- Progressive reduction in EGA's spot market alumina procurement requirements will ease the dual-sided pressure that characterised the disruption period

- Spot alumina prices that incorporated a scarcity premium following the March 2026 event should face downward normalisation as refinery output climbs toward 50% capacity and beyond

- Seaborne alumina traders who had extended contracts or spot exposure during the disruption period face mark-to-market adjustments as the supply gap closes

For primary aluminium markets:

- Reactivation of smelter reduction cells progressively restores hot metal production, contributing to global aluminium supply in H2 2026

- Downstream consumers in automotive, construction, packaging, and renewable energy infrastructure sectors had factored Al Taweelah's extended outage into supply planning; its earlier-than-expected recovery reduces the risk of structural deficits forming

For regional market dynamics:

- The UAE's position as a globally significant aluminium producer is reaffirmed as Al Taweelah returns to operation

- The event has almost certainly accelerated internal industry discussion around infrastructure resilience, insurance frameworks, and the risk management implications of highly integrated production zones in geopolitically complex regions

For context, aluminium sector investment activity more broadly has reflected growing awareness of these resilience considerations, with major producers reassessing how capital is deployed across integrated versus distributed production models.

Risks That Could Still Extend the Recovery

Despite the positive operational trajectory, several risk factors remain capable of disrupting the recovery timeline. However, understanding these risks in detail is essential for any market participant drawing conclusions from the current progress reports provided by EGA's Al Taweelah site.

Cathode integrity constraints: Cells that cannot be safely restarted without relining create a hard floor on the pace of smelter capacity restoration. The proportion of the 1,262 cells requiring full relining versus direct restart is not publicly disclosed, but it is the single most important variable in determining whether the six-month trajectory is achievable.

Bauxite logistics: The alumina refinery's ramp-up speed depends on reliable bauxite supply through KEZAD's port infrastructure. Any logistics disruption affecting inbound bauxite volumes would throttle refinery output growth independently of equipment readiness.

Geopolitical recurrence: The original shutdown was caused by an external security event. Any recurrence of hostilities affecting KEZAD would reset timelines and introduce new risk premiums across insurance, financing, and operational planning for the entire complex.

Utility stability: The highly sensitive restart phase for both reduction cells and refinery circuits demands consistent power and water supply. Utility interruptions during this window carry disproportionate consequences compared to the same interruption during stable full-capacity operation.

FAQ: EGA Al Taweelah Alumina Restart

What triggered the Al Taweelah shutdown?

Iranian attacks on the Khalifa Economic Zone Abu Dhabi on 28 March 2026 disrupted the shared infrastructure of the Al Taweelah industrial complex, forcing an emergency suspension across all production operations.

Has alumina production genuinely restarted?

As of 10 July 2026, EGA confirmed alumina production has resumed and is targeting approximately 50% of refinery capacity within days. The earlier resumption of hydrate production on 24 June 2026 confirmed that upstream refining circuits had been restored sufficiently to support this transition. According to Reuters reporting on the ramp-up, EGA's recovery trajectory is being closely monitored by global commodity markets.

Why does the refinery restart matter separately from the smelter restart?

The two recovery tracks are operationally independent. The smelter involves progressively reactivating 1,262 electrolytic reduction cells, while the refinery involves restoring a multi-stage chemical process from bauxite digestion through to calcined alumina output. Progress on one does not directly pace the other.

When will Al Taweelah return to full production?

EGA has indicated the technical capability to return the alumina refinery to full output by the end of 2026. Smelter recovery appears to be tracking ahead of the original 12-month estimate, with potential for full cell reactivation within approximately six months of July 2026. As LME Insight has noted, this would represent a notably efficient recovery for a complex of this scale.

What is the significance of hydrate in alumina refining?

Hydrate, or aluminium hydroxide, is the intermediate product formed before the final calcination step that converts it into usable alumina. Its production resumption on 24 June 2026 confirmed that the upstream stages of the refinery had been successfully restored, making alumina output a near-term operational step rather than a distant goal.

Key Takeaways for Market Participants

-

Integration amplifies disruption: Al Taweelah's single-zone model created compound vulnerability across multiple production stages simultaneously — a risk profile that concentrated facilities in coordinated industrial zones carry but that market models often underweight. Leading aluminium industry leaders are increasingly factoring this into their operational strategy.

-

Decoupled recovery is a strategic choice: EGA's decision to manage smelter and refinery restarts as separate operational programmes, with the smelter using externally sourced alumina during the refinery ramp-up, reflects sophisticated crisis planning rather than sequential dependency management.

-

The recovery pace is ahead of precedent: A trajectory toward full restoration within approximately six months from July 2026 would represent best-in-class performance against industry benchmarks for facilities of comparable scale and complexity.

-

Market normalisation is a process, not an event: As alumina refinery output climbs toward 50% and then toward full capacity, and as smelter cells are progressively reactivated, the supply premiums and spot price pressures that emerged post-March 2026 will ease gradually rather than disappear immediately.

-

Geopolitical risk has been repriced: The Al Taweelah event has permanently altered how the aluminium industry, insurers, and commodity traders assess concentration risk in integrated production complexes located in regions exposed to geopolitical volatility. As EGA restarts alumina production at Al Taweelah, this broader lesson will continue to shape capital allocation and risk modelling decisions across the industry for years to come.

This article contains forward-looking statements and scenario projections based on publicly available information as of July 2026. Actual outcomes will depend on operational, geopolitical, and market variables that may differ materially from current trajectories. Nothing in this article constitutes financial or investment advice.

Want to Track the Next Major Mineral Discovery Before the Market Moves?

The Al Taweelah disruption illustrates how rapidly supply shocks can reshape commodity markets — and how critical it is to identify emerging opportunities ahead of the crowd. Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries across aluminium, bauxite, and more than 30 other commodities, turning complex data into actionable insights the moment announcements hit the exchange — explore historic examples of exceptional discovery returns and begin your 14-day free trial today to position yourself ahead of the market.