May 13, 2026

When Global Supply Chains Fracture, Trade Policy Becomes Agriculture's Front Line

Commodity markets rarely move in straight lines, but nitrogen fertilizer has spent much of 2025 and 2026 defying the cyclical logic traders typically rely on. The combination of shipping corridor disruption, geopolitical conflict, and tightening domestic supply buffers across major producing nations has created a pricing environment that is forcing governments to act defensively. The Egypt fertilizer export tax, introduced in May 2026, is not simply a bureaucratic trade measure. It represents a concrete expression of how agricultural resource nationalism is replacing open-market assumptions at the policy level.

Understanding why this matters requires stepping back from the headline rate and examining the structural forces that made this intervention inevitable, the mechanics of how it operates, and what cascading effects it carries for global nitrogen markets already stretched thin. Furthermore, supply chain disruptions across multiple sectors have primed governments to act defensively well before price spikes reach their peak.

When big ASX news breaks, our subscribers know first

What the Egypt Fertilizer Export Tax Actually Does

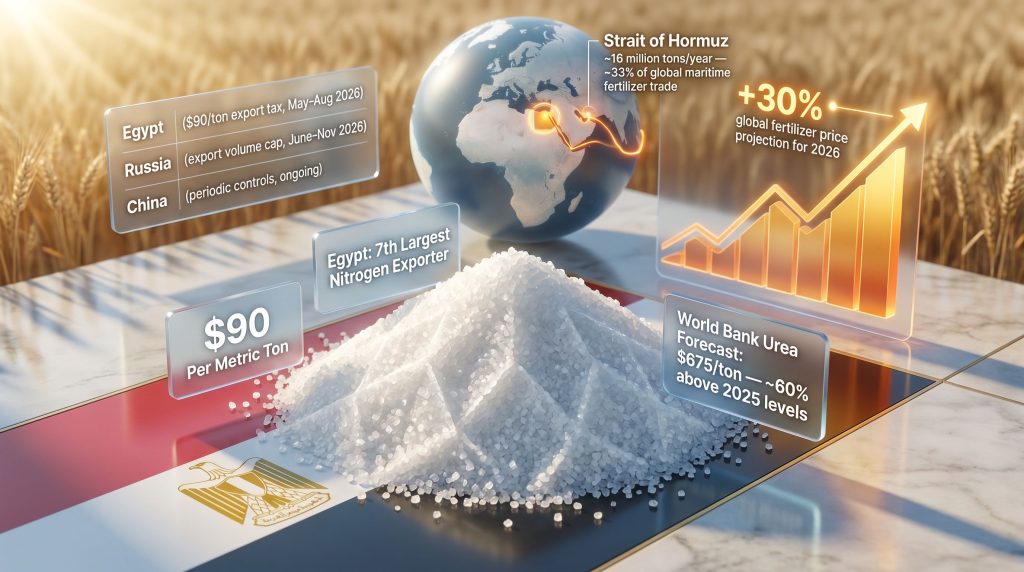

Egypt's Ministry of Investment and Trade implemented a $90 per metric ton export duty on nitrogen-based fertilizers, published in the country's Official Gazette and effective from May 5, 2026, for a fixed three-month window. The payment mechanism carries a notable design feature: while the rate is denominated in US dollars, exporters pay the equivalent in Egyptian pounds at the Central Bank of Egypt's prevailing exchange rate at the time of each transaction.

This currency-linked conversion introduces a second layer of cost variability beyond the nominal levy. As the EGP/USD rate fluctuates, the real burden on Egyptian exporters moves with it, meaning the effective cost of the tax is not fixed even though the headline figure appears straightforward. In periods of EGP depreciation, the pound-equivalent payment rises, compressing exporter margins further than the $90/ton figure implies.

The scope of the measure is narrow by design. It applies exclusively to nitrogen-based fertilizers, with urea and ammonium nitrate as the primary product categories. Phosphatic fertilizer exports remain entirely unaffected.

Why an Export Tax Rather Than a Quota or Ban?

The choice of policy instrument is itself analytically significant. Governments facing domestic supply pressure have several tools available, each with distinct trade-offs:

| Policy Tool | Revenue Generated | Supply Control | Market Signal | Reversibility |

|---|---|---|---|---|

| Export Tax ($90/ton) | Yes | Partial | Moderate | High |

| Export Quota | No | Strong | Strong | Moderate |

| Export Ban | No | Total | Severe | Low |

| Voluntary Restraint | No | Partial | Weak | High |

Egypt's selection of a per-unit tax rather than a quota or outright ban preserves export optionality while simultaneously generating fiscal upside. As reporting from Ecofin Agency notes, at elevated global prices, Egyptian producers may maintain export volumes to capture favourable market conditions despite absorbing the levy, which would convert the tax into a proportional revenue stream for the state. This dual-purpose design distinguishes it from harder interventions that sacrifice revenue for supply control.

The Price Environment That Made This Policy Inevitable

The timing of the Egypt fertilizer export tax cannot be separated from the global commodity backdrop against which it was introduced. The World Bank's Commodity Markets Outlook, published on April 28, 2026, provided the clearest signal of what policymakers were responding to. Indeed, commodity market volatility has increasingly shaped the speed and severity of these national responses.

Key projections from that report include:

- Global fertilizer prices are forecast to climb more than 30% in 2026.

- Urea, the dominant nitrogen fertilizer globally, is projected to reach an average of $675 per metric ton in 2026, approximately 60% above 2025 average levels.

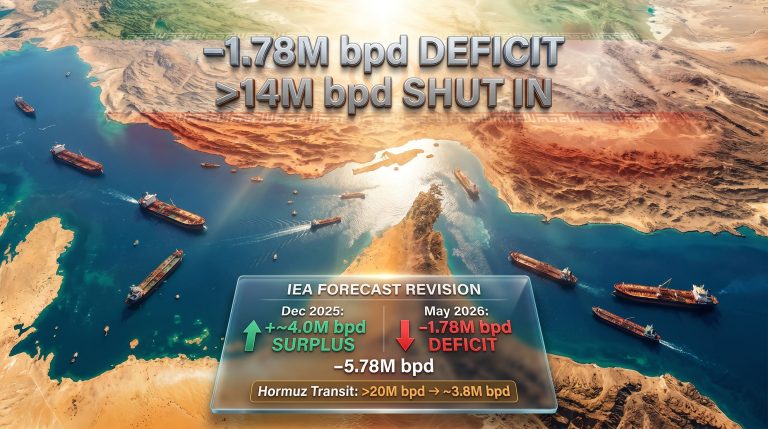

- The principal driver of this escalation is disruption to maritime shipping through the Strait of Hormuz, a corridor through which roughly one-third of global maritime fertilizer trade transits, representing approximately 16 million metric tons annually.

The World Bank report also explicitly warned that domestic supply concerns could prompt major exporting countries to implement trade restrictions. Egypt's measure appears to be among the earliest direct policy responses to that forecast materialising in practice.

The Strait of Hormuz: An Often Underappreciated Fertilizer Chokepoint

Most commodity market observers associate the Strait of Hormuz with oil and gas flows, but its significance for agricultural inputs is equally consequential and far less discussed. Approximately 16 million tons of fertilizer per year depend on safe transit through this passage. Geopolitical shipping disruptions in this region have become a defining variable for landed fertilizer costs across importing nations.

Freight cost increases, insurance premium surges, and routing disruptions caused by regional conflict dynamics translate directly into landed cost increases for importing nations, accelerating the price trajectory that the World Bank's forecast captures.

The convergence of a constrained shipping corridor with simultaneous export restriction signals from multiple producing countries creates a compounding supply shock that individual policy measures cannot fully account for in isolation.

Egypt's Weight in the Global Nitrogen Export Hierarchy

To assess how consequential the Egypt fertilizer export tax is for international markets, Egypt's position within the global export landscape must be understood clearly. According to Trade Map data cited by Ecofin Agency, Egypt exported approximately 3.54 million metric tons of nitrogen fertilizers in 2024, ranking seventh globally.

| Rank | Country | Notable Context |

|---|---|---|

| 1 | China | Dominant volume exporter; periodic export controls |

| 2 | Russia | 2026 export cap announced for June–November period |

| 3 | Oman | Gulf-based natural gas feedstock advantage |

| 4 | Netherlands | European trading and processing hub |

| 5 | Belgium | Integrated chemical production base |

| 6 | United States | Domestic demand constraints limit export volumes |

| 7 | Egypt | $90/ton export tax effective May 5, 2026 |

Egypt supplies an estimated 5 to 10% of global nitrogen fertilizer imports, with key destination markets including India, Brazil, and European agricultural buyers. That market share is significant enough that even marginal reductions in Egyptian export availability tighten an already constrained global supply pool. In addition, fertilizer import reliance among major agricultural economies means that supply disruptions carry outsized consequences for downstream food production costs.

Why Egypt's Natural Gas Position Amplifies the Policy's Significance

Nitrogen fertilizer production via the Haber-Bosch process is highly energy-intensive, with natural gas serving as both the primary feedstock and the dominant cost input for urea synthesis. Egypt's access to domestic natural gas reserves has historically provided its producers with a competitive cost advantage over suppliers dependent on imported feedstock or higher-priced energy sources.

This cost advantage is precisely what has enabled Egypt to reach seventh place in global nitrogen exports despite not being among the largest economies. The $90/ton levy partially erodes this cost differential, narrowing the price gap between Egyptian product and competing suppliers from higher-cost production environments. If the tax persists or escalates, the structural competitiveness that Egypt has built over decades in nitrogen fertilizer trade begins to erode, with market share potentially migrating to alternative suppliers in Oman, the Gulf, or Central Asia.

The Russia Parallel and the Dual-Supplier Contraction Risk

Egypt's policy does not exist in a vacuum. In April 2026, Russia announced plans to cap total fertilizer exports, including nitrogen types, for the June through November 2026 period. Russia occupies second place in the global nitrogen export hierarchy, representing a volume profile vastly larger than Egypt's. The simultaneous presence of restrictions from the second and seventh largest nitrogen exporters creates a compounding dynamic that amplifies price risk beyond what either measure would generate independently.

The overlap window is particularly sensitive. If Egyptian restrictions remain in force through early August 2026 and Russian caps take effect from June, the two-month overlap period from June to August 2026 concentrates supply pressure at a point when agricultural purchasing cycles for key import markets are often at their most active.

A simple price sensitivity illustration clarifies the stakes:

- At the World Bank's forecast price of $675/ton for urea, Egypt's $90/ton levy represents a ~13.3% cost addition for international buyers sourcing Egyptian product.

- Even if this cost increase reduces Egyptian export volumes by only 5 to 8% during the restriction period, the combination with Russian supply limits could push spot urea prices meaningfully above the $675/ton forecast.

Disclaimer: Price scenario projections are illustrative and based on World Bank forecasts. Actual market outcomes depend on numerous variables including shipping conditions, weather events, purchasing decisions by major importers, and policy implementation details. This does not constitute financial advice.

Downstream Consequences for African Agricultural Economies

A dimension of the Egypt fertilizer export tax that receives less international attention is its potential impact on nitrogen-dependent agricultural systems across Africa. As a major exporter within the continent, Egyptian supply disruption carries direct relevance for farming economies from North Africa through Sub-Saharan regions.

Countries that have historically relied on proximity to Egyptian production capacity may face:

- Higher landed fertilizer costs during the restriction window.

- Reduced availability in local distribution channels as exporters redirect inventory decisions.

- Downstream cost pass-through to smallholder and commercial farm operators, affecting input budgets for the 2026/27 planting season.

- Second-order effects on food production costs and consumer price levels in markets with limited import diversification.

This dynamic also fits within a broader African trade pattern. The Ecofin Agency notes that Nigeria LNG has redirected all cooking gas supply toward its domestic market, while West African rice trade routes have tightened under new restrictions. Egypt's nitrogen fertilizer tax adds another thread to this pattern of inward resource redirection across African commodity exporters responding to external price pressure.

The next major ASX story will hit our subscribers first

The Global Fertilizer Policy Landscape in 2026

Egypt's measure is best understood not as an isolated national decision but as part of a structural shift in how major fertilizer-exporting governments are managing the tension between global price incentives and domestic supply security. Consequently, global commodity tariffs are reshaping how producers and importers alike assess procurement risk.

| Country | Policy Action | Fertilizer Type | Timeline | Primary Driver |

|---|---|---|---|---|

| Egypt | $90/ton export tax | Nitrogen (urea, ammonium nitrate) | May–August 2026 | Domestic supply and price stability |

| Russia | Export volume cap | All fertilizers including nitrogen | June–November 2026 | Domestic market protection |

| China | Periodic export controls | Urea and phosphates | Ongoing from 2023 to 2026 | Domestic food security |

What is structurally significant about this convergence is the absence of any multilateral coordination mechanism for fertilizer trade. Unlike oil, where OPEC frameworks provide at least a nominal governance structure for production and export decisions, fertilizer trade lacks any equivalent oversight body. Restrictions accumulate across national jurisdictions without systemic review, meaning the aggregate supply impact of simultaneous national measures is never formally assessed until market prices reflect the damage.

The World Bank's April 2026 warning about a potential cascade of national trade restrictions has proven prescient. Egypt's tax validates that forecast and may increase the probability that other mid-tier nitrogen exporters, watching global prices climb and domestic procurement costs rise, adopt similar defensive postures before the year ends.

Three Scenarios for What Happens After August 2026

The three-month fixed duration of the Egypt fertilizer export tax means market participants must already be pricing in scenario uncertainty for the post-August period. Three plausible pathways exist:

-

Extension Scenario: If global urea prices remain near or above $675/ton and domestic Egyptian supply pressure persists through the summer growing season, the tax is extended, potentially at a revised rate reflecting updated market conditions.

-

Expiry Scenario: If Strait of Hormuz disruptions ease, Russian export restrictions prove less severe than announced, and domestic Egyptian agricultural procurement is satisfied, the tax lapses in early August 2026, and Egyptian export flows normalise, providing temporary relief to international buyers.

-

Escalation Scenario: If domestic fertilizer shortages worsen or global prices spike further beyond forecast levels, Egypt converts the tax into a harder restriction such as an export quota or temporary ban, producing a more severe and less reversible supply shock for importing nations.

The variables most likely to determine which scenario materialises include:

- The trajectory of conflict dynamics affecting Strait of Hormuz shipping through June and July 2026.

- Whether Russia enforces its announced export cap with the rigour its communication implies.

- Egyptian domestic agricultural demand levels entering the 2026/27 crop preparation window.

- CBE exchange rate movements and their effect on the real pound-denominated cost burden facing Egyptian exporters.

Frequently Asked Questions: Egypt Fertilizer Export Tax

What fertilizers does Egypt's export tax cover?

The duty applies specifically to nitrogen-based fertilizers, principally urea and ammonium nitrate. Phosphatic fertilizers, another significant Egyptian export category, are not subject to this tax.

How long will the Egypt fertilizer export tax remain in effect?

The measure took effect on May 5, 2026, for a fixed three-month period, placing its scheduled expiry in early August 2026. Extension is possible depending on domestic supply and global market conditions.

How is the tax rate structured?

The rate is set at $90 per metric ton, payable in Egyptian pounds at the Central Bank of Egypt's exchange rate prevailing at the time of each transaction, introducing a variable EGP/USD conversion element. As detailed reporting from Hydrocarbon Processing confirms, this structure adds a layer of unpredictability for exporters managing currency exposure.

Which import markets face the greatest exposure?

India, Brazil, and European agricultural buyers represent the principal importers of Egyptian nitrogen fertilizers and face the most direct risk of supply tightening or price increases.

Is Egypt acting alone?

No. Russia announced plans to restrict total fertilizer exports, including nitrogen types, between June and November 2026. China has maintained periodic urea and phosphate export controls since 2023. Egypt's measure reflects a broader pattern of managed export regimes emerging across major producing nations.

Why does the Strait of Hormuz matter so specifically for fertilizers?

Approximately one-third of global maritime fertilizer trade, roughly 16 million metric tons per year, transits through this passage. Regional conflict dynamics that elevate freight costs or disrupt routing directly translate into higher landed prices for importing nations worldwide.

Key Figures at a Glance

| Metric | Detail |

|---|---|

| Tax Rate | $90 per metric ton |

| Effective Date | May 5, 2026 |

| Duration | 3 months (expires approximately early August 2026) |

| Fertilizer Scope | Nitrogen-based only (urea, ammonium nitrate) |

| Egypt's 2024 Export Volume | Approximately 3.54 million metric tons |

| Egypt's Global Export Rank | 7th largest nitrogen fertilizer exporter |

| World Bank Urea Price Forecast (2026) | Approximately $675/ton (~60% above 2025 levels) |

| Global Fertilizer Price Outlook | More than 30% increase projected for 2026 |

| Strait of Hormuz Fertilizer Trade | Approximately 16 million tons/year (~33% of maritime trade) |

The statistical data in this article references World Bank Commodity Markets Outlook projections (April 2026) and Trade Map data as reported by Ecofin Agency. Price forecasts are subject to revision based on evolving market, geopolitical, and weather conditions. This article is for informational purposes only and does not constitute investment or financial advice.

Want to Capitalise on the Commodity Disruptions Reshaping Global Markets?

As nitrogen fertiliser prices surge past $675 per metric ton and export restrictions cascade across major producing nations, Discovery Alert's proprietary Discovery IQ model delivers real-time alerts on significant ASX mineral discoveries — instantly converting complex commodity data into actionable investment insights for traders and long-term investors alike. Start your 14-day free trial with Discovery Alert today, or explore the historic returns major mineral discoveries have generated to understand the scale of opportunity these market dislocations can create.