June 24, 2026

When Gold's Best Assets Trade at Its Worst Valuations: The Activist Logic Behind Elliott's Northern Star Campaign

Sophisticated investors know that valuation gaps in the mining sector rarely emerge from geological uncertainty alone. Some of the most persistent discounts in the global gold market exist not because of what lies underground, but because of what happens above ground: inconsistent leadership, opaque disclosures, and a management culture that repeatedly promises more than it delivers. When that pattern persists long enough, it stops being a temporary dislocation and becomes a structural discount that only external pressure can break.

That is precisely the dynamic now playing out between Elliott Investment Management and Northern Star Resources (ASX: NST), in what has become one of the most closely watched Elliott Investment Management Northern Star Resources activist campaign stories in Australian resources history.

When big ASX news breaks, our subscribers know first

Why Activist Investors Target World-Class Assets With Underperforming Management

The Core Paradox: Premium Resources, Discount Valuations

The foundational logic of activist investing in resource companies rests on a straightforward but powerful observation: when an asset is genuinely world-class but its owner consistently trades at a discount to comparable businesses, the gap is almost never geological. It is managerial.

In the gold mining sector, valuation is typically assessed through two primary lenses:

- P/NAV (Price-to-Net Asset Value): the ratio of a company's market capitalisation to the estimated net present value of its mineral reserves and resources after costs.

- EV/EBITDA: enterprise value divided by earnings before interest, tax, depreciation, and amortisation, widely used to compare operational efficiency and profitability across mining peers.

Miners operating exclusively in Tier-1 jurisdictions (politically stable, low-sovereign-risk countries like Australia, Canada, and the United States) theoretically deserve premium multiples on both measures. Geopolitical risk is lower, permitting environments are more predictable, and institutional capital is more readily available. A Tier-1 miner trading at a persistent discount to peers is therefore sending a clear message to the market: something other than geology is destroying value.

"In the gold mining sector, valuation discounts rarely reflect asset quality alone. When a miner operates exclusively in Tier-1 jurisdictions yet trades at a persistent discount to peers, institutional investors increasingly interpret this as a governance and execution risk premium, not a resource risk."

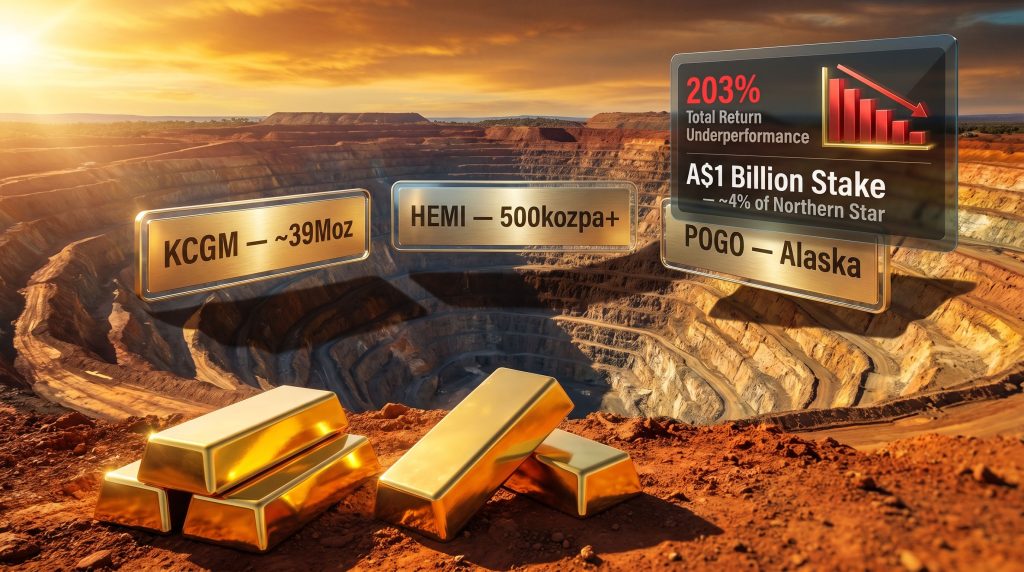

According to Elliott's investor presentation, Northern Star Resources currently holds the lowest P/NAV and EBITDA multiples among global senior gold peers, despite its mines being located entirely within Australia and Alaska. That is not a resource problem. It is a credibility problem.

How Activist Campaigns Are Constructed: The Elliott Playbook

Elliott Investment Management is not a typical institutional investor. The New York-based firm, founded by Paul Singer in 1977, has built a global reputation for methodical, research-intensive activist campaigns across energy, resources, and industrials. Its interventions at Suncor, Marathon Petroleum, and BHP all followed a recognisable architecture:

- Identify a company with genuinely exceptional underlying assets.

- Catalogue a pattern of operational underperformance and governance deficits.

- Build a sufficiently large stake to command Board attention.

- Present a dual-track proposal: pursue strategic alternatives including a potential sale, or undertake a comprehensive operational and leadership reset.

Elliott's position in Northern Star is reported at approximately A$1 billion, representing roughly 4% of the company, making it the firm's largest Australian-listed investment since its BHP campaign in 2017. That level of financial commitment signals deep conviction, not opportunistic positioning.

What the Elliott Investment Management Northern Star Campaign Is Actually About

Separating Asset Quality From Execution Credibility

A critical and deliberate feature of Elliott's campaign is the explicit separation between Northern Star's asset portfolio and its management performance. The activist is not arguing that the mines are poor. It is arguing the opposite: that the mines are exceptional and are being systematically undervalued by a management team that cannot execute consistently.

The three assets at the centre of this thesis represent a genuinely rare concentration of Tier-1 gold inventory:

| Asset | Key Metrics | Strategic Significance |

|---|---|---|

| KCGM (Kalgoorlie, WA) | ~39Moz resource base | Potential to become the world's second-largest Tier-1 gold mine post Fimiston mill expansion |

| Hemi (Pilbara, WA) | 500kozpa+ expected production | Australia's largest gold development project; one of only four greenfield Tier-1 projects globally at this scale |

| Pogo (Alaska, USA) | High-grade, 10+ year mine life | Cash-generative with meaningful exploration upside in a Tier-1 US jurisdiction |

What makes the Hemi asset particularly noteworthy from a technical standpoint is its classification as an intrusive-hosted gold deposit, a geological style that was considered highly unusual in the Pilbara until De Grey Mining's discovery in 2020. These deposits are characterised by large, bulk-tonnage ore bodies with consistent grade distribution, which lends itself to efficient, large-scale open-pit or underground extraction.

Northern Star acquired Hemi through Northern Star's De Grey acquisition, gaining exposure to what is broadly considered the most significant Australian gold discovery in decades. The KCGM operation at Kalgoorlie, furthermore, sits atop the famous Golden Mile, one of the richest gold-bearing structures on Earth. The proposed Fimiston mill expansion would substantially increase throughput capacity, potentially transforming KCGM's production profile over the next decade.

The Guidance Credibility Crisis: Seven Misses in Four Years

For institutional investors, consistent guidance delivery is not a minor administrative matter. It is the primary mechanism through which management teams build or destroy credibility with capital allocators. According to Elliott's investor presentation, Northern Star has missed production or cost guidance seven times across four financial years, including four separate downward revisions in the first three months of 2026 alone.

This pattern creates what analysts refer to as an execution risk premium: an additional discount the market applies to companies with a demonstrated history of over-promising and under-delivering. In practical terms, even if Northern Star achieves strong operational results in any given quarter, the market discounts forward guidance by a scepticism factor that compounds into a structurally lower valuation.

Featured Snippet: How many times has Northern Star Resources missed guidance? According to Elliott Investment Management's investor presentation, Northern Star missed production or cost guidance seven times across four financial years, including four separate downward revisions within the first three months of 2026.

The compounding effect of repeated guidance misses is particularly damaging in the gold sector because gold equity investors already apply a leverage premium to miners relative to the spot gold price. When operational misses erode that leverage, the valuation case collapses rapidly. Understanding the gold price impact on mining equities is consequently essential context for evaluating the full scale of Northern Star's underperformance.

Disclosure Deficits and the Institutional Transparency Gap

Beyond operational performance, Elliott's presentation identifies a structural disclosure failure that is less visible to retail investors but critically important to institutional capital allocation. According to the activist, Northern Star provides no publicly available detailed technical reports to support the multi-billion-dollar capital investment decisions it is asking the market to fund.

In comparable international markets, senior gold miners typically publish comprehensive technical documents, such as NI 43-101 reports (the Canadian standard) or detailed JORC-compliant reserve statements, that allow institutional investors to independently model project economics, assess geological risk, and verify management assumptions. Without these documents, investors must either accept management's projections on faith, or apply an additional discount to compensate for the informational asymmetry.

This is not a trivial point. For a company asking the market to back billion-dollar development decisions at Hemi and the KCGM expansion simultaneously, the absence of detailed technical reports materially raises the cost of capital.

How Does Northern Star's Shareholder Return Compare to Global Gold Mining Peers?

The 203% Underperformance Gap: Unpacking the Numbers

Elliott's central performance claim is striking in its scale. According to the firm's investor presentation, Northern Star has delivered a 203% total return underperformance relative to its senior global gold peer group over three years. To contextualise what this means in practical terms: an investor who chose a diversified basket of Northern Star's peers instead of holding Northern Star itself would have captured returns more than twice as large over the same period.

More telling still, Northern Star's relative return has lagged:

- Its direct gold mining peer group.

- The VanEck Gold Miners ETF (GDX), a broad-based benchmark for gold equity exposure. VanEck ETF diversification is increasingly used by institutional investors as a reference point for sector-wide performance benchmarking.

- The gold spot price itself.

"When a gold producer's total shareholder return consistently trails the commodity it extracts, it signals to sophisticated investors that operational costs, capital misallocation, or governance failures are consuming the value that rising gold prices should be delivering to shareholders."

This is the core paradox that gives Elliott's campaign its analytical power. Gold prices have been elevated by global macro forces, central bank buying, and geopolitical uncertainty. A gold miner with world-class assets in stable jurisdictions should be among the primary beneficiaries. Instead, Northern Star shareholders have watched their returns trail the commodity itself.

Peer Valuation Comparison: Where Northern Star Sits in the Global Rankings

The valuation data presented by Elliott positions Northern Star at the bottom of the senior gold peer group across multiple metrics, including P/NAV and EV/EBITDA. This is despite the company operating exclusively in Tier-1 jurisdictions, a characteristic that should theoretically justify a premium to peers with assets in higher-risk geographies.

The spread between Northern Star's intrinsic asset value and its current market price represents what Elliott describes as the actionable opportunity. In activist investing terminology, this is the NAV discount, and it is the primary target of the campaign's value unlock thesis.

What Does Elliott Investment Management Want Northern Star to Do?

Demand Track 1: A Formal Strategic Review and Potential Sale

Elliott's primary demand is that the Northern Star Board formally explore all strategic alternatives, with a potential sale of the company as an explicitly stated option. The timing of this demand is not coincidental. Several macro conditions currently align to make a transaction particularly compelling from a value-maximisation standpoint:

- Gold prices are near multi-year highs, supporting premium transaction valuations.

- Tier-1 gold assets are in acute global supply scarcity, with very few new large-scale deposits being discovered.

- Senior gold miners are generating strong free cash flow and carry robust balance sheets capable of supporting major acquisitions.

- Northern Star is currently operating without a permanent CEO, creating a natural governance inflection point that a strategic review process could frame constructively.

The logic Elliott presents is that a formal sale process forces the Board into a quantitative comparison: what is the transaction value a buyer would pay today, versus the time, capital expenditure, execution risk, and reputational rehabilitation required to deliver a multi-year internal turnaround?

Demand Track 2: Comprehensive Operational and Leadership Reset

If no sale proceeds, Elliott's reform agenda is detailed and specific. The firm calls for:

- Appointment of an external CEO with demonstrable operational turnaround credentials, directly challenging the likelihood of internal succession.

- A comprehensive operational review across all three asset sites to identify cost, productivity, and capital allocation inefficiencies.

- Board composition enhancement, adding independent directors with direct gold mining operational experience.

- New operational and financial KPI frameworks with independent accountability mechanisms.

- Publication of detailed technical reports for major capital projects, bringing disclosure standards in line with global senior peers.

- A clearly defined capital allocation framework to rebuild institutional confidence in management's investment decision-making.

Why the Dual-Track Structure Is a Deliberate Pressure Mechanism

Presenting two simultaneous pathways is not rhetorical ambiguity. It is a calculated pressure architecture that serves multiple functions at once. It signals to potential acquirers that Northern Star may be available, potentially catalysing inbound interest without requiring a formal auction process. It gives the Board a face-saving route to reform without explicitly conceding to the activist's critique. And it mirrors the structural approach Elliott deployed at BHP in 2017, where the presence of strategic alternatives on the table accelerated internal governance reform even before any transaction was completed.

How Is Northern Star Likely to Respond to Elliott's Campaign?

The Standard ASX Activist Defence Playbook

ASX-listed large-cap companies have a reasonably predictable initial response sequence when confronted with activist pressure. Historical precedents from AGL, BHP, Origin Energy, and AMP all follow a recognisable pattern:

- A public statement committing to constructive engagement with the activist investor.

- Reaffirmation of confidence in the existing long-term strategy and asset quality.

- Emphasis on strategic progress, in Northern Star's case, the KCGM expansion timeline and Hemi development milestones.

- Incremental governance announcements, such as new director appointments, framed as proactive rather than reactive.

What Northern Star Has Already Signalled

Northern Star has announced a A$500 million share buyback and reaffirmed FY2026 production guidance above 1.5 million ounces, moves consistent with a company attempting to demonstrate shareholder responsiveness ahead of formal engagement. Australian gold M&A activity has, furthermore, intensified considerably over this period, adding additional strategic pressure on boards to demonstrate value creation credibility.

The challenge for Northern Star's Board is a fundamental credibility dilemma. Any substantive concession to Elliott's demands implicitly validates the activist's core argument. Yet a purely defensive posture risks institutional shareholder alignment shifting toward the activist, which would dramatically narrow the Board's room to manoeuvre.

The CEO Succession Variable

The leadership transition is arguably the most consequential single variable in this campaign. CEO Stuart Tonkin's departure timeline, already anticipated for FY2027, creates an organic inflection point that Elliott's demands for CEO change intersect with directly. The Board's choice between an internal successor and an externally recruited operational specialist will be read by the market as the clearest available signal of whether genuine reform is underway.

The next major ASX story will hit our subscribers first

What Are the Possible Outcomes for Northern Star Shareholders?

Scenario Modelling: Three Paths Forward

| Scenario | Key Condition | Likely Market Outcome |

|---|---|---|

| Full Strategic Sale | Strong institutional alignment with Elliott; inbound interest from global majors | Significant re-rating toward intrinsic NAV; potential takeover premium of 20-40% |

| Partial Reform (Operational Reset) | Board accepts leadership and disclosure demands without committing to sale | Moderate re-rating as execution credibility rebuilds over 12 to 24 months |

| Defensive Status Quo | Institutional shareholders side with management; Elliott fails to build broader coalition | Continued valuation discount; further share price pressure if operational misses continue |

The outcome hinges critically on whether major institutional shareholders publicly align with Elliott's position. Near-term share price volatility of 10 to 20% is a realistic expectation as the market prices probability-weighted outcomes across these scenarios.

What This Means for the Broader ASX Gold Sector

The implications of this campaign extend beyond Northern Star itself. A successful Elliott intervention, whether resulting in a sale or a credible operational reset, would effectively raise the governance bar across the entire ASX gold sector. Other Australian gold miners carrying similar asset-quality/execution gaps may find that elevated gold prices and heightened institutional scrutiny make them increasingly visible targets for activist capital.

How Does Elliott's Activist Approach Compare to Its Previous Resource Sector Campaigns?

Elliott at BHP: The 2017 Australian Precedent

Elliott's 2017 campaign at BHP remains the closest structural analogue to the Northern Star situation. That campaign similarly combined a substantial stake with dual-track demands focused on capital allocation discipline and strategic alternatives. The fact that Elliott's Northern Star position is described as its largest Australian-listed investment since BHP is a deliberate signal of the firm's conviction level.

The Global Activist Gold Mining Playbook

Globally, activist campaigns at senior gold miners have historically accelerated one of three outcomes:

- Leadership change, typically the appointment of an operationally-focused external CEO.

- M&A consolidation, either through the targeted company being acquired or through it making strategic acquisitions to create scale defences.

- Enhanced capital return programs, including buybacks and special dividends designed to reduce the NAV discount by returning surplus cash.

Gold mining is structurally susceptible to activist intervention because the combination of long project timelines, high capital intensity, complex operational execution, and commodity price leverage creates persistent gaps between intrinsic asset value and market price.

FAQs: Elliott Investment Management and Northern Star Resources

What is Elliott Investment Management's stake in Northern Star Resources?

Elliott has built a position of approximately A$1 billion, representing roughly 4% of Northern Star Resources, making it the firm's largest Australian-listed investment since its BHP campaign in 2017.

What specific changes is Elliott demanding from Northern Star?

Elliott's demands fall into two categories: a formal strategic review including exploration of a potential sale, and if no sale occurs, a comprehensive operational reset including an external CEO appointment, board enhancement, improved disclosure standards, and new financial performance targets.

Why does Elliott argue Northern Star is undervalued?

Elliott contends that Northern Star's assets — specifically KCGM, Hemi, and Pogo — are world-class by any global standard, yet the company trades at the lowest P/NAV and EBITDA multiples among senior global gold peers. Understanding the range of gold mining stock types helps contextualise why senior producers like Northern Star are held to a higher governance standard by institutional investors.

Has Northern Star responded to Elliott's campaign?

Northern Star has announced a A$500 million share buyback and reaffirmed FY2026 production guidance above 1.5 million ounces, moves widely interpreted as pre-emptive shareholder value signals ahead of formal engagement.

Could Northern Star be acquired as a result of this campaign?

A sale is one of the explicitly stated options Elliott is pressing the Board to evaluate. With gold prices elevated, Tier-1 assets in high demand, and major gold miners carrying strong balance sheets, conditions for a transaction are considered favourable. However, Northern Star's management has not indicated any willingness to pursue a sale process at this stage.

What happens if Northern Star's Board rejects Elliott's demands?

If the Board resists and institutional shareholders do not align with Elliott, continued valuation pressure is the most probable outcome. However, if Elliott builds broader institutional support, the Board's options narrow considerably, potentially forcing leadership changes or a formal strategic review regardless of management preference.

Key Takeaways: What the Elliott-Northern Star Campaign Reveals About ASX Governance Standards

The Credibility Premium in Modern Mining Investment

The central lesson of this Elliott Investment Management Northern Star Resources activist campaign is one that has broader relevance across the entire ASX resources sector. In today's institutional investment environment, operational credibility and disclosure quality are not secondary considerations that can be compensated for by asset quality. They are primary valuation drivers in their own right.

What Investors Should Monitor Going Forward

For investors tracking how this campaign evolves, the following indicators will be the most meaningful signals:

- CEO appointment process and timeline: whether the Board selects an external turnaround candidate or pursues internal succession will reveal the depth of its reform commitment.

- Institutional shareholder voting patterns: public alignment with Elliott by major holders would decisively narrow the Board's room to resist substantive change.

- Operational performance against FY2026 guidance: any additional guidance miss would substantially strengthen Elliott's case and likely trigger further institutional frustration.

- Inbound M&A interest from global gold majors: any formal or informal approach from a senior miner would immediately accelerate the strategic review timeline.

- Disclosure improvements: voluntary publication of detailed technical reports for Hemi and the KCGM expansion would represent the clearest available signal of genuine governance reform intent.

This article is general information only and does not constitute financial advice. Past performance is not indicative of future results. Readers should conduct their own research and consult a licensed financial adviser before making investment decisions. Scenario projections and outcome estimates referenced in this article involve inherent uncertainty and should not be treated as forecasts or guarantees.

Want to Track the Next Major ASX Gold Discovery Before the Market Moves?

Discovery Alert's proprietary Discovery IQ model delivers real-time alerts the moment significant mineral discoveries are announced on the ASX, giving subscribers an immediate edge in identifying actionable opportunities in gold and beyond — explore historic discovery returns on the Discovery Alert discoveries page to understand what early positioning can mean for investor outcomes, and begin your 14-day free trial today.